Message merged into topic: Inderes Coffee Room (Part 10)

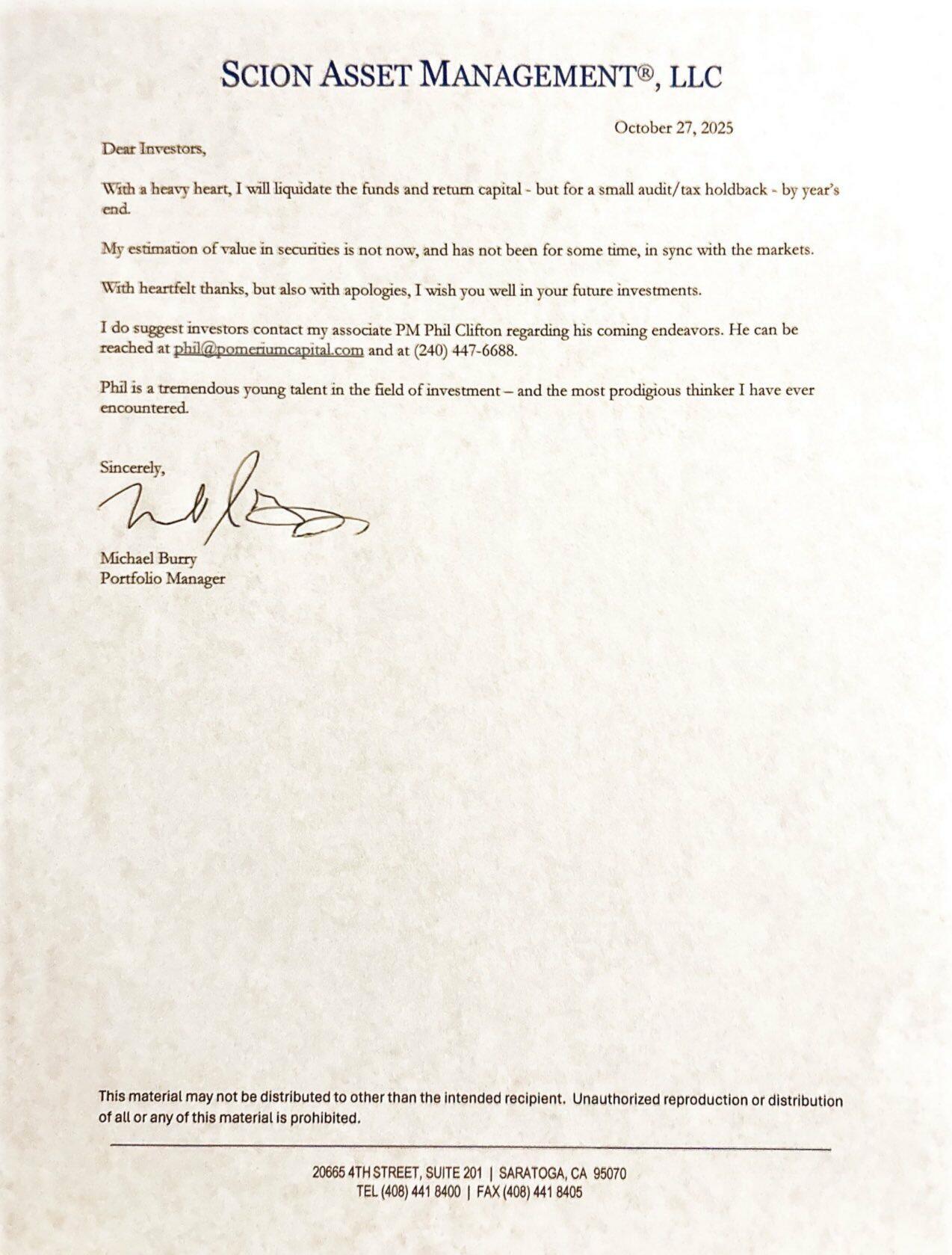

Michael “Big Short” Burry is closing his hedge fund by the end of the year after admitting he doesn’t understand the current markets.

48 Likes

A historical moment, and indicative of the market. Although, Burry is unlikely to stop completely; he will probably continue investing, e.g., under the guise of a “family office.”

Burry has recently criticized the accounting practices of mega tech companies, which downplay depreciation and thus inflate profits. I have also brought up the same point in Vartti. If depreciation periods had not been extended and the results of mega tech companies better reflected their free cash flow, their results would have stagnated or declined for years!

So far, if stock prices are the verdict, all criticism has fallen on deaf ears and been wrong. Still, I cannot help but raise critical points, which are also highlighted in this WSJ article. These could also be raised in the Magnificent7 thread, but I’m raising them here because mega tech companies account for over 30% of the SP500’s value and a significant slice of the world’s total stock market value.

Quarterly profits soared at Nvidia, Alphabet, Amazon and Microsoft as AI-related revenue poured in (Meta’s were wiped out by tax). Cash flows are mostly fine, albeit a lot is now going into building new data centers. Some of the money comes from actually selling AI services to businesses, particularly at Alphabet and Microsoft.

But much of the AI-related profits come from being a supplier to, or investor in, the private companies building the large language models behind AI chatbots—and they’re losing money as fast as they can raise it, and plan to keep on doing so for years.

I know that Meta and Alphabet, for example, achieve better advertising returns for advertisers with AI, which in turn drives the duo’s advertising revenues. In a way, there’s nothing new here: companies have been algorithm developers long before the AI hype. What used to be algorithms, machine learning, and whatever else is now better branded as AI. ![]()

Microsoft and Amazon, on the other hand, boast about being in a constant bottleneck state, meaning customers have more demand for their cloud services than they can supply.

So far, so good.

But a significant part of the AI demand for mega tech companies comes from AI model operators, such as ChatGPT. Every time I ask something from ChatGPT, Microsoft’s Azure runs hot. Or if I generate an image with Adobe Firefly, Amazon’s AWS is probably humming somewhere in the world, depending on which model I choose for image generation.

How much are consumers ultimately willing to pay for these services? So far, OpenAI, Meta, Alphabet, etc., have chosen a path where services are first offered for free. For example, OpenAI’s losses are escalating at an enormous rate. Using AI is genuinely expensive because chips and energy cost money. But the consumer doesn’t pay for it; the shareholders in these companies do, especially in OpenAI. Of course, the assumption is that AI will develop to be so excellent and the service so addictive that eventually, people will pay $200 a month for it, or whatever various estimates have been raised in recent days. Companies are pushing for AI adoption. I recently posted news about Electronic Arts in the thread, where management is pushing for AI use, but employees complain that it’s not sensible beyond a certain point. ![]() Management is under immense pressure here because EA is being bought off the stock market, and buyers are paying a high price for the shares because… they believe AI will vastly enhance EA’s operations.

Management is under immense pressure here because EA is being bought off the stock market, and buyers are paying a high price for the shares because… they believe AI will vastly enhance EA’s operations. ![]()

Even more concerning are the competitive advantages of the models. I’m preparing the next Vartti on the topic of AI’s presumed first victims, and as part of the preparations, I listened to Constellation Software’s investor call on the subject (the stock has plummeted 30%, so the usually taciturn company has suddenly opened its mouth to investors). A comment from a developer struck me: if one model provider starts raising prices, they will replace the model with another quite effortlessly because the models are so similar.

To put it a bit hyperbolically, soon trillions will be invested so that people can freely generate AI-powered cat videos or corporate slaves can compete to send each other CoPilot-generated emails that no one reads.

The results of mega tech companies are traditionally considered high-quality, but an increasing amount of profit practically comes from AI startups incurring heavy losses, and the real free cash flow goes to NVIDIA.

Of course, there’s also a huge amount of useful applications for it, and if you believe the AI bulls, soon AI will do all the work, robots will bring us food home, and we’ll lie passively on the couch as cyborg-human-whales watching the Sora2 feed.

Interesting times indeed.

Correction. Judging by the recently collapsed stock prices of fast-food chains like Chipotle, in an AI bull scenario, we will get our nutrition from pills, not food.

Addendum. Note that in this free “give give give ask” strategy, for example, it worked brilliantly for Facebook back in the day because an increasing amount of traffic primarily became a cost for the operators running the internet infrastructure, not a burden for FB. FB didn’t have to invest a fortune in its own network infrastructure. And FB (later Meta) was soon able to monetize users by targeting ads. The same applies to Netflix and others. In the AI revolution, companies are forced to build a very expensive data center infrastructure requiring continuous investments, without a clear path to monetizing AI.

156 Likes

A very good and thought-provoking article. What has bothered me is how people talk about the tech giants’ earnings season going well again when revenues and EPS grew. Then, when looking at cash flow valuations, only P/OCF is considered, and it’s justified by saying that it’s now a relevant metric due to AI investments, etc. Ultimately, it is free cash flow that determines what remains for the owners. At the same time, many US-listed SaaS players have taken a serious hit this year, and their EV/FCF multiples have come down significantly. And all this because they are not involved in the AI IaaS business or because AI is feared to take over their business. Examples include many CRM or Project Management software companies (CRM, HUBS, MNDY, etc.). Their multiples are very low compared to their track record and growth.

15 Likes

This market is starting to look interesting. Fed lowers the key interest rate and a preliminary “agreement” is reached with China → indices fall. Government shutdown ends → indices fall. It’s as if Messrs. Buffett and Schiller are winning a round ![]()

28 Likes

The SireenialarmisemiCAPSLOCKKI account reports that apparently market valuations are now higher than ever, well, it could soon collapse, when absolutely everyone has enjoyed princely returns. ![]()

![]() Then we all get to buy as net buyers etc.

Then we all get to buy as net buyers etc.

18 Likes

Tired musings: if the market now believes that companies building data centers won’t get large orders in the near future, and mega-tech stocks haven’t particularly dived, is that then a sign that the market believes either that

- mega-tech companies will stop massive investments and that’s a good thing, because AI is nonsense, or

- mega-tech companies will stop massive investments and that’s a good thing, because they will get the benefits from AI without massive investments?

Or is this more about the market thinking that not all of these neoclouds etc. can win at the same time, and since it’s unclear who will emerge as winners, everything is falling?

I had, of course, thought that a potential bubble would also affect the companies that spend money, not just those that do something with that money, and would bring the entire S&P 500 down significantly due to the heavy weighting of mega-techs.

(The message contains blatant simplifications.)

8 Likes

Nothing much has happened yet, apart from a little fluctuation. Someone here shared news from JPMorgan (?) about how much these investments should yield to get a decent 10% return. At least until yesterday, investors believed in megatech investments, but their valuations are really high while those investments are starting to eat into free cash flow.

Transformer AI is here to stay, but I don’t believe everyone can win. Building models doesn’t seem to achieve very significant competitive advantages (they are all quite similar). And the benefits are certainly greatly exaggerated, but at this point, I might be generalizing my own view too broadly. Even in the Dotcom bubble, all stock prices soared, and this one turned out quite well even though those prices eventually collapsed.

AI stocks in a bubble? Yes. The entire (US) market? At least it’s expensive; miracles must happen from these valuation levels compared to history.

11 Likes

Inflation -0.2% in October 2025 | Statistics Finland

Finland’s inflation fell to negative from September’s +0.5%. Finland’s inflation therefore also includes interest rates.

The European harmonized inflation was 1.4% in Finland and 2.1% in Europe. Both saw a slight decrease from September.

31 Likes

Well, I celebrated too early. This looks really bad.

The deadlock has not been broken. Markets don’t like uncertainty, and now it’s possible that we’ll go into another shutdown. Uncertainty has become the new normal.

“While several government departments will be funded until September in the shutdown-ending agreement, Congress will have to approve spending for the rest of the government by the end of January to avoid another shutdown.”

Trump celebrates as Democrats face fallout from end of shutdown - BBC News

9 Likes

Good writing from Verneri and interesting comments. As perhaps a representative of an older generation, I have followed the IT boom a bit. My general opinion is that in the stock market, and perhaps in the economy in general, returns from new technologies are expected too soon. My opinion is that new technology is usually monetized only after 15-20 years. In the case of artificial intelligence, this means sometime in the 2040s. Here are a few examples

Nokia phone

Mobira portable phone in the early 1980s. (Carried in a shoulder bag and was quite heavy)

1985 Mobira Cityman

1988, from memory, Corba used a phone, a kind of breakthrough. Usage was limited by network availability and high cost (investment money was not found, and calls were significantly more expensive than landline calls)

1990s network expansion, GSM network emerges, portable phones become common and everyday items. Nokia phones stood out from Motorola with text messaging on all phones.

Late 1990s WAP, an attempt to bring the Internet to phones, didn’t catch on

2000s Internet craze, the big “app” on phones was ringtones. You called a paid number, from which you then got Thunderstruck as a ringtone, for example. Some games came with the mobile phone; the hit game was Snake.

In the 2000s, Nokia started appearing in American movies (suitable networks even in America). Nokia’s competitive advantage was battery life. An app store that didn’t take off.

Windows and Internet

1985 Windows 1.0. My cousin had a Mikro-Mikko computer with Windows, and it was boring from my perspective, as there were no games.

Early 1990s. I used email for the first time. It was done at the university in an MS-DOS environment. Mail was read by logging in/typing a prompt to connect to the email server network with one’s own ID. The computers had Windows 3.1, and its use was mainly playing Minesweeper. For me, it was a bit difficult to understand why a graphical user interface was needed. Things were usually done with DOS, and Windows was used for playing Minesweeper. There was fierce competition between Windows and OS.

1995 saw the arrival of Windows 95, which shifted usage towards the graphical user interface. Computer use had significantly moved to networks and the Internet. Files were stored on network drives, and significant amounts of movies, games, etc., began to be transferred. Internet search engines started to emerge. The biggest were Alta Vista and Yahoo. I first heard about Google in a TV search engine competition, where users usually won by using Google. Google stood out from Alta Vista and Yahoo because its page was empty and not full of “servers” and ads that significantly consumed network capacity. Very similar to opening Edge with MSN today. People started assembling their own computers, and many companies came to Finland that “made” or assembled computers. Components were bought as needed.

In the 2000s craze, the Internet existed, and it was thought to be connected to mobile phones. However, connections were too slow, and no one bothered to do it on a mobile phone. Usage was cumbersome. The Internet was for free news services, etc. Nothing truly purchasable was looked for there. No car information, no price information was found. Things were looked up in the Yellow Pages of the phone directory. Monetization was a mystery. Phone companies got money from phone subscriptions, internet subscriptions, and mobile phone subscriptions and bought air from Germany ![]() Phone companies tried to create their own servers and Yellow Pages, i.e., to move online advertising services to the web. A bit like Netposti today.

Phone companies tried to create their own servers and Yellow Pages, i.e., to move online advertising services to the web. A bit like Netposti today.

The use of the Internet really started to take over when the iPhone appeared. Was it 2005? That’s about 10 years after Windows 95. From that point, it probably took another 10 years until purchases were primarily made online.

I see AI currently undergoing its first acceleration. We are living in that Windows 95 phase. In five years, we will start to see great expectations, but the grandma from Pihtipudas will not yet be using AI. Someone’s car might be driving with AI, but most people will still think it’s more pleasant to drive themselves. Many consider AI cars too expensive.

In my opinion, the stock market generally expects too much too soon. Systems and companies will still change many times over. Over-investment in new technologies is more the rule than the exception. Of course, some company always makes a good profit from an investment, but at some point, that business then slows down and starts to melt away, perhaps not entirely, but the cycle turns.

47 Likes

The article by the old man (in the profile picture) talking about the IT boom is interesting in itself, though lengthy, but it is very speculative and selectively chooses historical developments to suit the author’s narrative, and above all, it forgets (or does not know) the most important cornerstone of information technology-based technological development, namely Moore’s Law. According to it, processor power doubles every two years (previously every year).

In reality, algorithms and machine learning (=artificial intelligence) have been bringing money to companies for a decade already. The average person indirectly uses artificial intelligence every time they watch television, use a phone, or buy bologna sausage from the grocery store.

From Moore’s Law, it can be deduced that technological development based purely on processing capacity, such as AI, cannot be tied to timelines based on historical events, because in reality, the pace of technological development is constantly accelerating.

This acceleration can, of course, be observed in the world outside of processing power by including all of humanity’s technological development. The current “IT boom” is based on this acceleration and its calculated expectation.

8 Likes

“Traditional” ML has not required the kind of investment boom we see today, and it is indeed a very different incrementation than current transformer/AI/LLM models. ML has never been as sexy as the current AI boom where all sorts of semi-automatic setups are called AI. This has many characteristics of the DotCom bubble, even if it hasn’t been taken to the same extreme. However, the technology will remain and continue to develop.

Edit: No bubble has burst yet, and that fluctuation isn’t even really distinguishable from the SP500 YTD graph. This could grow even larger, and a bubble can really only be confirmed in hindsight, if one exists.

12 Likes

It would indeed be interesting to look at the adjusted key figures.

The immediate next thought is, have these companies become accustomed (even partially) to the idea that if any investments (such as AI now, for example) do not generate cash flow, they can be cleared from the results if necessary? And is this the reason why these companies invest so coolly?

I assume this refers to my own text and that the reply was made to me. My own writing was more based on economics, but when doing science, they very often follow the same paths. The development of innovations, for example, has been observed in economics to follow a similar pattern to population development. I agree that algorithms have existed for a long time, and I do not underestimate what already exists. For example, facial recognition is widely used and a good example of functioning artificial intelligence. Now, a significant leap has been made to perform task series and use data for various purposes. It is typical for new technology that it requires a lot of investment and infrastructure creation. Once the infrastructure/hardware is built, there is usually an economic disappointment. The full economic benefit is usually not realized. There comes a certain phase of slower development, during which the hardware becomes cheaper and easier to acquire. This does not only apply to artificial intelligence but is a general progression in technologies. If we take 3D printing, for example, it had very high expectations. It is already quite widely used, but we are still far from everyone having a 3D printer at home. If we go back to the Windows 95 era, people didn’t have a regular printer. If we go 10 years forward to Apple’s release, almost everyone had a printer, and a little later, for example, Samsung’s Android phones had a printing application, although I haven’t seen anyone actually doing it with a mobile phone. If we return to 3D printing, I haven’t seen a single house being 3D printed yet, for example. (Video examples can be found on YouTube, but basic construction workers are moving around on construction sites, not 3D printers.) We are waiting for the day when we drive to a construction site with a concrete mixer and a slightly larger caliber 3D printer, and in a moment, the house is up.

My own writing and time window were partly based on Kondratiev’s cycle. He has researched long cycles that last an average of about 54 years. It has four seasons, each lasting about 15 years, from which my 15-20 years partly come. In spring, the seeds are sown, which is some technological innovation/advancement step into which people enthusiastically invest. Expectations are high, and borrowed money eventually begins to limit development; some begin to view the matter skeptically. Interest rates rise, and if the desired returns are not obtained from investments, some fare poorly. Verner’s example referred to something similar. Well, some push forward, and after 15 years, the returns truly begin to materialize. Enthusiasm for the matter arises through people and customers. A need arises to buy a mobile phone, Windows, or something else, as neighbors also have them, and they are no longer so expensive. An arms race begins: faster, better, bigger, smaller, etc. The grandmother in Pihtipudas has not yet advertised to me that her AI is bigger than her neighbor’s. Or told me that my Ransu figured out how to tell the Husqvarna robotic lawnmower to cut the lawn before the rain and then drive into the garage for shelter. And then it poured.

22 Likes

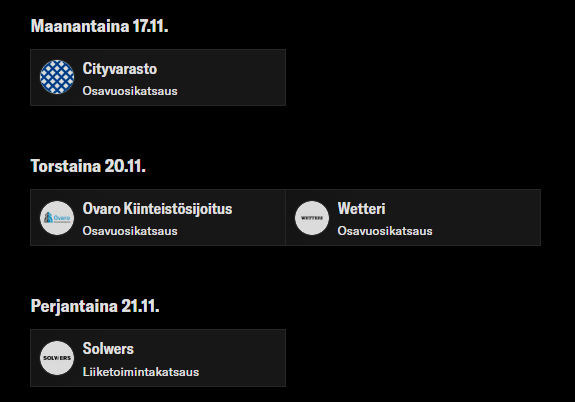

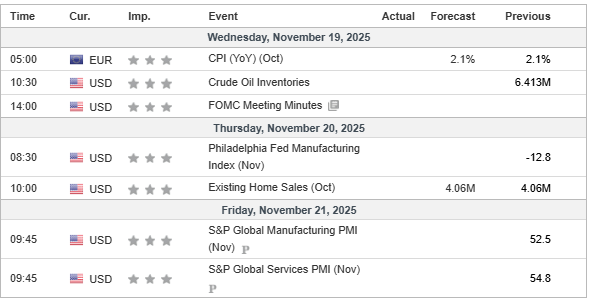

Here are next week’s happenings ![]()

https://x.com/eWhispers/status/1989346865117008279

Here are the events of Finland’s busiest stock exchange ![]()

Here are the macro ramblings ![]()

15 Likes

After 11 PM on Wednesday, Nvidia’s earnings will be released, and the fate of all the world’s stock markets, or at least their near future, depends on it.

The outlook for the Helsinki stock exchange is grim. A common European stock exchange, quickly!

8 Likes

The article below states that the Fed will stop shrinking its balance sheet as early as the beginning of December, but according to Morgan Stanley, this will not have a significant impact on the markets.

So, the Fed is not directly moving to stimulate, but only exchanging MBS securities (MBS = mortgage-backed securities) for short-term government bonds, meaning no new money is pushed into the markets. The increase in repo agreements (repo = repurchase agreement) is also just short-term financing.

Apparently, what is truly decisive is how much debt the United States decides to issue.

https://www.investing.com/news/economy-news/what-does-the-end-of-qt-mean-4346604

9 Likes

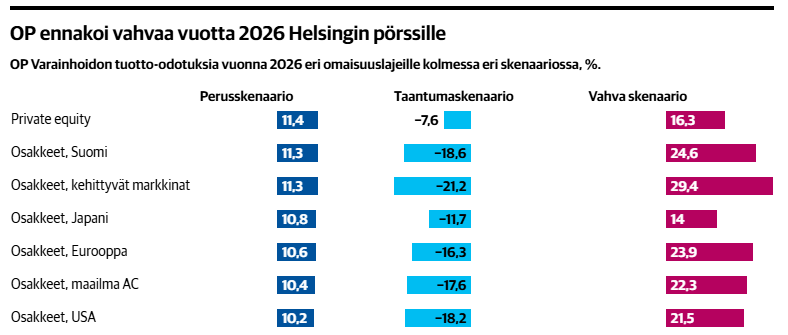

The attached image (Kauppalehti) illustrates well the difficulty of forecasting. First, a forecast is given, followed by a pessimistic and an optimistic scenario. As can be seen, for example, the Finnish stock market is predicted to yield between -19% and +25% next year. This is a good illustration; one should not only focus on the forecast figure but also on the range (to realize that the usefulness of the forecast in the stock market is quite weak).

10 Likes

Bank of Finland Governor Olli Rehn shared his views on the stock markets. ![]() No paywall.

No paywall.

Summary:

- Rehn warns of the risk of stock market overheating.

- Rehn is seeking the position of Vice-President of the European Central Bank, responsible for financial stability.

- In Finland, there are bottlenecks in corporate financing, which could be alleviated by increasing competition between banks.

The potential overheating of stock markets is a considerable risk, says Bank of Finland Governor Olli Rehn.

- “There is an obvious risk of a market correction in the stock markets. That is why it is important that strong capital buffers have been maintained for banks in Europe.”

- ”Stock values are currently quite high due to the AI boom in the United States, relative to real economic development and corporate earnings. For these reasons, caution is warranted now.”

19 Likes