In the Top-Level Investment Discussion area, you can discuss stock market movements, the market in general, and macroeconomic developments.

While browsing Inderes macro data, I noticed that the price data for forest industry products is missing. Is there a specific reason for this?

1 Like

@Marianne_Palmu hello and good morning!

Since you are Juurikki’s favorite macroeconomist ![]() along with Jan Hurri, could you kindly comment on his latest statement, please.

along with Jan Hurri, could you kindly comment on his latest statement, please. ![]() /

/ ![]() ,

, ![]() /

/![]() ,

, ![]() /

/![]()

You can reply on Monday during work hours too. ![]()

1 Like

Good morning, and thank you for the honor of being your favorite macro-blogger ![]() I just read Hurri’s text, and it certainly contained some seeds of truth. The problem with the sustainability gap indicator is somewhat similar to macro indicators in general: an attempt is made to compress as much information about the entire economy into one figure, and something is always missing. However, the sustainability gap indicator is of particular interest because major political decisions are made based on it.

I just read Hurri’s text, and it certainly contained some seeds of truth. The problem with the sustainability gap indicator is somewhat similar to macro indicators in general: an attempt is made to compress as much information about the entire economy into one figure, and something is always missing. However, the sustainability gap indicator is of particular interest because major political decisions are made based on it.

I noticed from the weekend’s Twitter threads that the National Audit Office (VTV) reached partly the same conclusion as Hurri in a report published in 2019, from which I’ve included a screenshot below:

In other words, other indicators should be used alongside it, and issues related to timing must be taken into account. And it is indeed strange that the current targets for the structural deficit have been set according to the criteria of the Stability and Growth Pact, which have been on hold this year and last, and for which a replacement is being sought at a rapid pace.

Here’s Hurri’s classic article from 2015.

Finland’s credit rating is known to be excellent partly because over 200 billion in pension assets are counted as part of public finances in this review, even though they aren’t strictly so.

Do credit rating agencies also consider what proportion of the state’s debt is debt from the right pocket to the left pocket?

Is this the solution to the debt problem of the broke Southern European countries? It seems so, but it has only recently become a problem, as the ECB has abandoned the spanner (jakoavain), allowing some countries to conjure new money out of thin air more than their share would entitle them to.

If one must scream into the dark forest and invoke the hyperinflation bogeyman, it should at least be done so that all countries benefit equally. Not in a way that the worse you manage your affairs, the greater the reward you receive.

@Marianne_Palmu thanks for this morning’s (and previous mornings’) Macro!

Recession obsession is indeed a fitting description for many writers for over ten years now. After the 2008 circus finally subsided, some people have constantly believed that the Fed’s printing efforts would backfire badly, but the rest of the world continued to absorb dollars, and the United States’ export product was their “inflation.”

Now, however, global trade is faltering, and the increase in money is no longer flowing abroad at the same rate. The spring labor market is “strong,” but this is precisely what the worst recession scenarios are based on. Extreme tightness in the labor market during elevated inflation leads to Fed rate hikes that happen too late. When rate hikes begin to bite and the economy cools slightly, some companies will have lost their workforce and go bankrupt, and others will have hired people at any cost and find themselves in a difficult situation with increased costs and cooling demand.

When people accustomed to higher income levels start getting laid off, that only further cools demand, enabling an unpleasant spiral. On top of this, people imagine that housing price development follows the consumer price index and have taken out loans to buy/invest in housing in cities with extremely low cap rates. However, housing prices move at the pace of wages. When wages and consumer prices do not move at the same rate in stagflation, people laid off from high-paying jobs face rising loan rates and vanished housing demand.

There is potential for several nasty spirals here, but let’s hope for the best.

A recession usually only truly begins after the yield curve inverts, so even the most recession-obsessed probably haven’t said that the recession will start next week, but have been waiting for this inversion and only now truly see the recession hitting.

1 Like

Hi,

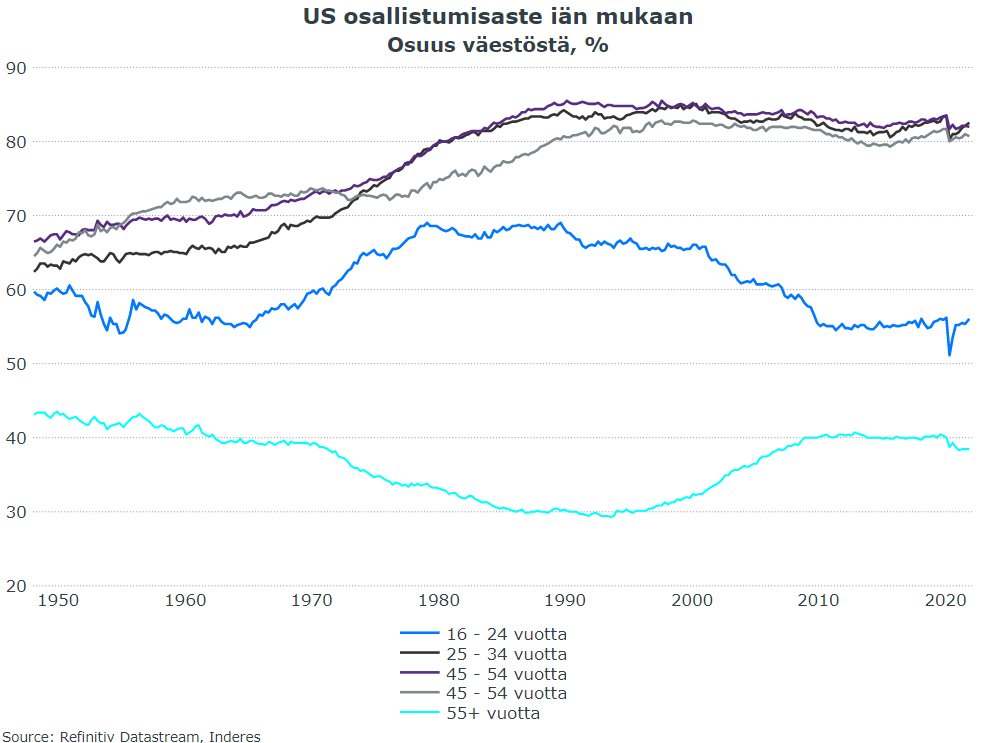

Yes, it’s true that recessions have always been preceded by very strong development in the labor market. Now, the economic situation is further complicated by distortions in the labor market caused by the COVID-19 pandemic. One of the essential questions is whether labor force participation will permanently remain at a lower level in older age groups. If this is the case, the labor market could experience scarcity for a longer period.

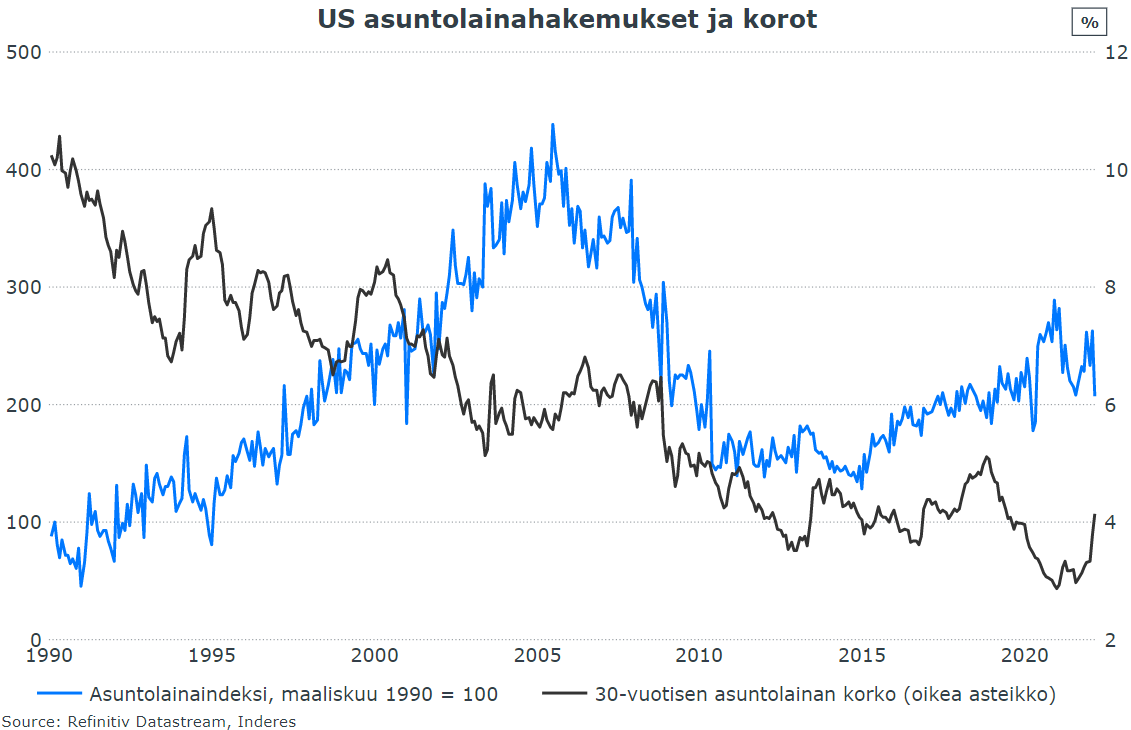

For the corporate sector, the situation is really difficult, as you mentioned, because costs are rising and demand is expected to cool down. For households, on the other hand, increased mortgage rates have already led to a decrease in mortgage applications. In the US, the interest rate on a 30-year mortgage, by the way, has risen by one percentage point in a relatively short period (since August). If the same were to happen to Euribor rates over the same period, a Finnish mortgage holder would certainly be bewildered.

1 Like