Et lille insiderkøb fra en af de nye direktører, Annica Witschard. Jeg formoder dog, at det ikke bliver det eneste af sin slags.

4 Synes om

Jeg kiggede nærmere på denne Ålandsbanken-analyse, som ser ud til, at man bare har trukket tallene ind i fremtiden med en lineal. Det giver et lidt ”rosenrødt” billede af selskabets fremtid. Teksten forklarede på ingen måde selskabets gældssituation eller behov for genfinansiering.

Ifølge rapporten falder nettogælden i forhold til egenkapitalen i år fra 408 % –> 275 %. Kan nogen herinde forklare, hvordan dette overhovedet ville være teknisk muligt i Intrums tilfælde?

Selskabet har foretaget betydelige nedskrivninger i balancen de seneste år, og intet tyder på, at der ikke også vil være behov for nedskrivninger i fremtiden.

2 Synes om

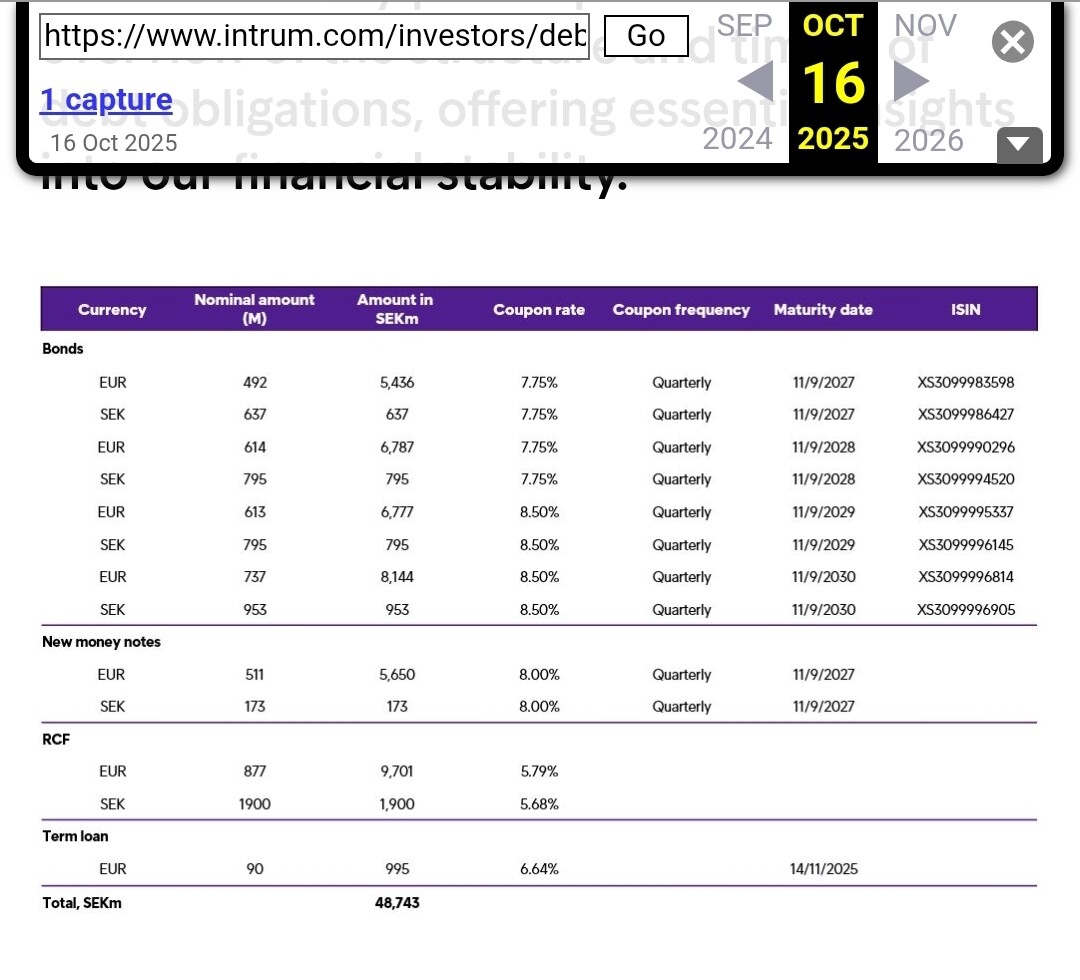

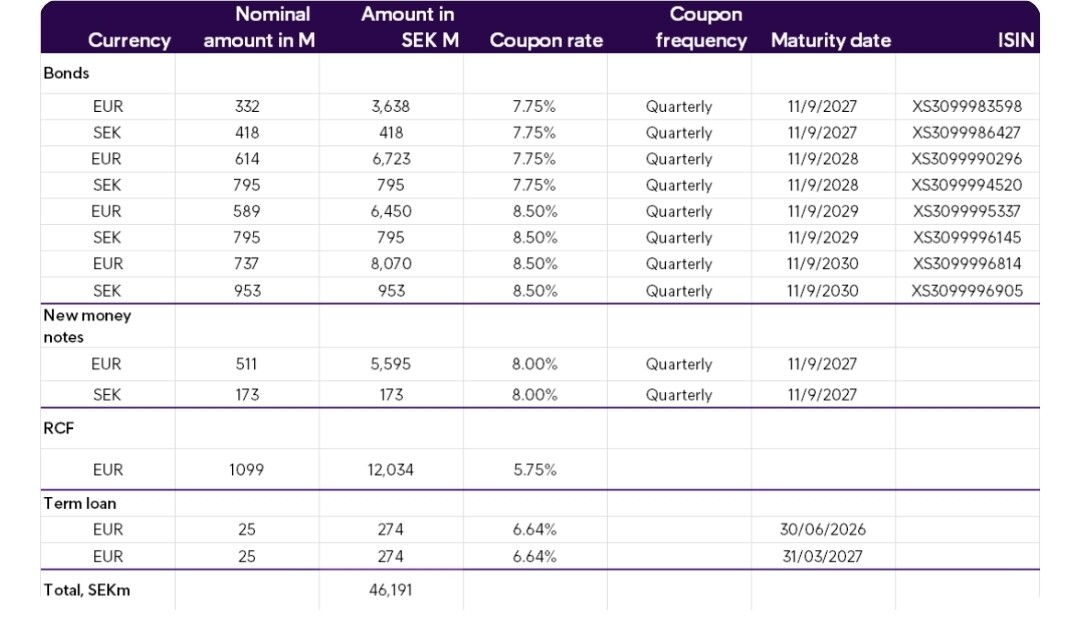

Jeg kom til at tænke på denne tabel, at 2027-obligationerne var tæt på 100 point, mens de andre stadig kravlede.

Så tog jeg et kig på Intrums egen hjemmeside med en tidsmaskine, og de havde købt op i de 27-obligationer.

|16.10.25 | 1.2.2025 |

|— | — | — | —|

|

Jeg ved ikke, hvor ofte de opdaterer den side, men man kan jo holde lidt øje med den.

Og andre stille signaler om de porteføljekøb (capital light), afskedigelser og måske Ophelos-lanceringer eller YouTube-præsentationer.

Jeg har stadig ikke tænkt mig at kaste håndklædet i ringen, da analytikerfronten endelig er ret positivt stemt over for Intrum.

5 Synes om

Flaget vejrer, men det er det helt ”forkerte” flag. NC er tilsyneladende holdt op med at dumpe aktier og er blevet siddende med en bid på 10 %. Hvorfor? De mest ivrige spekulerer naturligvis i, at den bliver solgt videre i sin helhed til en ny hovedaktionær, hvorefter alt vil ændre sig fuldstændigt.

4 Synes om

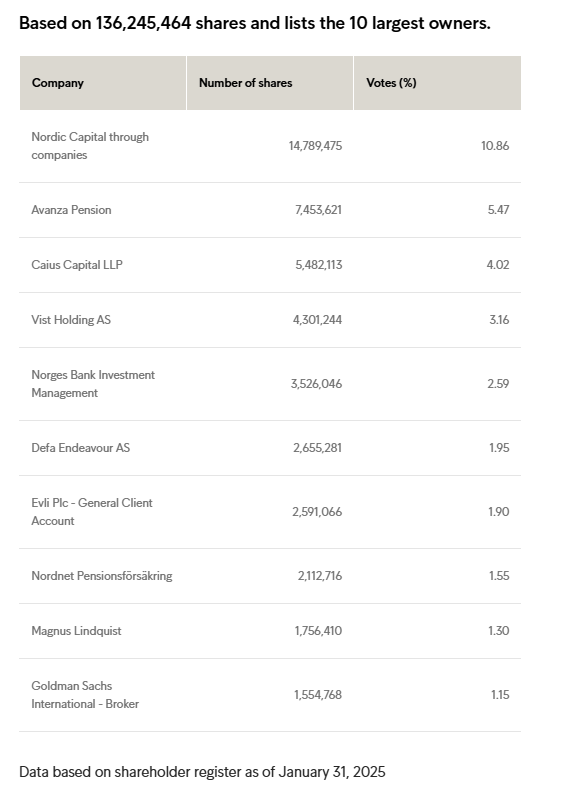

Ny ejeroversigt for januar er kommet. Professionelt nok med det forkerte årstal bagefter.

*NC har ikke rørt sin beholdning, Caius øgede vistnok, og som ny er den seneste tilføjelse Vist Holding AS, der har skovlet aktier ind.

7 Synes om

Tilsyneladende: Vist Holding AS’ moderselskab er Steneken Holding AB, som igen har den almennyttige Vidarstiftelsen bag sig… hvis man kan tro på ChatGPT, ville den post udgøre ~20 % af fondens aktiver. Fuldstændig lyssky forretning med fondens penge, hvis det er tilfældet.

3 Synes om

Nyhedsstrøm (nedenfor er Nordnets AI-resumé i sin helhed):

Kreditvurderingsudsigterne er blevet opjusteret til positive, selvom Moody’s har fastholdt Caa2-vurderingen. Det føles lidt som tom snak, selvom det er en tilsyneladende positiv nyhed.

Derudover har UBS hævet kursmålet, og en shorter har lukket sin position.

Kreditvurderingsinstituttet Moody’s har ændret Intrums kreditvurderingsudsigter fra stabile til positive og bekræftet selskabets Caa2-langsigtede kreditvurdering. Denne opjustering af udsigterne afspejler selskabets fremskridt med at nedbringe gælden takket være tilbagekøb af obligationer og en stabil pengestrøm. Intrums nye strategi, der fokuserer på gældsreduktion og operationel effektivitet, forventes yderligere at forbedre selskabets finansielle stilling, selvom en relativ svaghed forventes at fortsætte i de næste 12–18 måneder.

-

Moody’s hævede Intrums kreditvurderingsudsigter fra stabile til positive og bekræftede den langsigtede Caa2-kreditvurdering.

-

Opjusteringen skyldes forbedringen i Intrums gældsætning efter tilbagekøb af obligationer med udløb i anden halvdel af 2025 samt stabil cash flow-EBITDA og pengestrøm.

-

Intrum planlægger at reducere gælden yderligere i første halvår af dette år gennem salg af en gældsportefølje og tilbagebetaling af obligationer med udløb i 2027.

-

UBS hævede kursmålet for Intrum fra 47 SEK til 54 SEK og fastholdt en neutral anbefaling.

-

Brummer Multi-Strategy reducerede sin short-position i Intrum til under 0,5 procent og ophørte dermed med at være en offentlig shorter, selvom 4,64 % af kapitalen fortsat er shortet.

8 Synes om

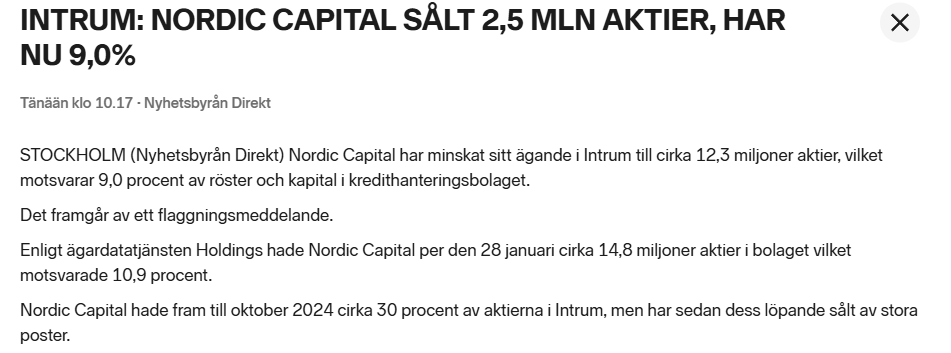

Der kom den forventede flagmeddelelse, hvilket betyder, at NC er fortsat med at sælge, og de røg under 10 %. 2,5 millioner aktier er væk. Tempoet ser altså ud til at være accelereret, da der røg en pæn portion på kort tid.

Januar var af en eller anden grund en undtagelse i NC’s salg, og jeg undrede mig også over, at der ikke kom en flagmeddelelse efter kvartalsrapporten, ligesom januars aktionærliste viste, at de slet ikke havde reduceret.

Med dette tempo ville de være helt ude i løbet af få måneder. Forhåbentlig senest til sommer. Nu begynder mængden at være så lille, at den kunne gå som en block trade til nogen.

6 Synes om

Mon den mængde er blevet solgt som en blok til en part, da flaggrænsen allerede var ret tæt på i forvejen. Og den meddelelse bør gives ret hurtigt, når grænsen overskrides.

NC’s exit er igen et skridt tættere på.

5 Synes om

Blogikirjoitus joka herätti suuria tunteita Sharevillessa Intrumin cheerleadereissa:

Education of a Value Investor (Miscellaneous)

The Pitfalls of Discounted NAV: When Cheap is Actually Expensive

With real-world study cases on JM , UIE and Intrum

Feb 12, 2026

In the world of value investing, few metrics are as seductive as the Discount to Net Asset Value (NAV). It appeals to our most basic instinct: buying a dollar for 50 cents. It suggests a margin of safety, a free lunch, an arbitrage opportunity waiting to be closed. However, as all children growing into adulthood finally realized - parallel to naive value investors learning the hard way - there is no free lunch.

If you buy a holding company or a real estate developer solely because it trades at 30% below its NAV or Book Value, you are not necessarily buying value. You are buying a derivative of the underlying assets, attached to a specific business model, often laden with structural risks that the headline number ignores.

Join me on our journey as we dissect three specific cases where the “Discounted NAV” thesis falls apart when viewed through first principles, bottom-up analysis. This is our menu for today: JM’s illiquid inventory**, UIE’s** cyclical concentration and the accounting assumptions of Intrum.

Disclaimer: This article is not a critique of the long-term viability or quality of the companies mentioned. While there are many compelling reasons to hold these assets, the focus here is to highlight the specific risks of relying solely on a discounted NAV as a primary investment thesis. Valuation is rarely as simple as a single metric.

(All the numbers are written as of 11 Feb 2026 and may be subject to my personal error)

Case Study 1: The Time-Value Trap (JM AB)

The Discounted NAV:

JM AB is a Nordic residential developer. The current market cap is 8.79B SEK, while the reported NAV is 7.9B SEK. The company also reports that there is a massive hidden “surplus value of development properties” in their building rights portfolio (land bank) of ~5.0B SEK that is not reflected in the balance sheet. This hidden NAV is most possibly marked to market.

When adding the hidden surplus (7.9B + 5.0B), the implied NAV suggests that the share price is trading at ~30% discount to its NAV.

The Pitfall:

This argument confuses Inventory with Assets.

JM AB owns land (building rights). They cannot mail you a plot of dirt. To realize this surplus NAV, JM must process, build, and sell apartments over decades. The discount is simply the market applying a discount rate to future cash flows.

The Numbers:

Let’s calculate the Present Value (PV) of that headline 5.0B SEK surplus.

Inventory Size: ~35,400 building rights

Production Rate: ~2,300 starts per year (recent run-rate)

Years to Realization: 35,400 / 2,300 - approx 15.4 years

Nominal Surplus Flow: 5.0B SEK / 15.4 = ~325M SEK / year

Discount rate: 10% (12.5% cost of capital offset by 2.5% land price appreciation)

This is effectively a DCF limited to 15 years. The resulting PV is roughly ~2.5B SEK.

The market isn’t ignoring the discounted NAV; it is discounting it for time. By the time JM converts the last building right into cash, the cost of time and capital has eaten 50% of the value. When you add 7.9B and 2.5B, the result is 10.4B SEK. With market cap of 8.79B SEK, this is still a discount of 15% to NAV. Well, there is also the problem with our assumptions. For example, we assume the production rate to be 2,300 starts per year, while in reality the numbers may vary between 1,500 to 4,000 starts per year. We also apply no discount on the not-hidden NAV of 7.9B SEK.

Investing in JM AB needs consideration on the time value of money and the execution risk. This is why the market puts a discount to the their NAV.

So, what’s the alternative?

Use Margin of Safety. Currently we are at ~15% discount to Net Present Value (if you believe my calculation). If the discount widens to >30%, then it is potentially time to look at JM closer.

The pitfall of the pitfall:

This calculation assumes minimal (2.5%) land appreciation. If land prices rise by 5% annually while JM holds it, the “Surplus Value” grows over time, partially offsetting the discount rate. However, trusting a 15-year inflation forecast to bail out your valuation is speculation, not investing.

The most important thing - following Howard Marks

I want my dear readers to use Margin of Safety when evaluating an investment. The Margin of Safety concept is essential regardless of valuation methods.Case Study 2: The Cyclical Peak Trap (UIE vs UP)

The Discounted NAV:

Let’s look at UIE (United International Enterprises). It’s a holding company with a NAV derived largely from the market price of its largest holding, United Plantations (UP). Looking at UIE’s current market cap and NAV, you see a ~30% discount. The logic seems clear: Why buy UP directly when you can buy it through UIE for cheaper?

The Pitfall:

This logic ignores Mean Reversion.

This logic assumes the current market price of the underlying asset (UP) is the correct anchor for value. UIE is not a diversified compounder like Investor AB or Berkshire Hathaway. In those vehicles, if one holding is at the top of its cycle, another might be at the bottom. The portfolio effect smooths the NAV risk.

UIE is effectively a mono-line bet. While UIE does hold a stake in Schörling AB (giving some exposure to diversified basket like Hexagon and Securitas), United Plantations currently accounts for approximately ~80% of UIE’s total NAV. Its fate is mathematically tied to palm oil.

The Numbers:

Let’s look at United Plantations (UP) in terms of P/B (Price-to-Book), EV/Ha (Enterprise Value per hectare of lands) and its premium valuation to peers (based on their Q3 2025 and website).

Market Cap 18.81B MYR

Net Cash 566M MYR

Enterprise Value = 18.81B - 0.566B = 18.24 MYR

Book Value 2.93B MYR

Total Planted Area ~51,000 Hectare

Current P/B: ~6.4x. Historical P/B: ~2.5x

Current EV/Ha: ~350k MYR. Historical EV/Ha: <150k MYR

Current premium to peers: ~5x. Historical premium to peers: 2-3x

UP is currently trading at over ~2.5x its historical median valuation. On top of their record high valuations (a commodity company with a 6.4x P/B is insane to me!), their margins are also near record highs compared to their historical numbers. This signals a peak cycle. The underlying asset is priced for perfection, sitting at a cyclical peak fueled by CPO (Crude Palm Oil) prices. If UP’s valuation mean-reverts to ~3x P/B (still a premium to history) i.e. drop by 50%, the UIE’s NAV would effectively drop by 40%. Did you get the math?

You buy $1.0 of UIE’s NAV for $0.70. You’re happy.

UP mean-reverts**.** That $1 of NAV re-rates to $0.60 - your $0.70 entry is now a massive premium to the new reality. Are you still happy?

So, what’s the alternative?

Don’t Buy the NAV. Buy the Normalized Earnings. Value UIE on “cycle-normalized” earnings of UP. Calculate the average earnings of UP over a full commodity cycle (5-10 years). Apply a historical multiple (e.g. 15x) to those normalized earnings. If UIE trades at a discount to that number, you have a Margin of Safety.

The Pitfall of the Pitfall

The analysis assumes historical valuation pattern will repeat. One would argue that the palm oil market has structurally changed (due to ESG planting restrictions limiting supply), meaning UP deserves a permanently higher multiple. If this time is truly different, UP’s share price will stay high and UIE’s NAV will not collapse. On the other hand, I would put my money on history rhyming.

The most important thing: I want my dear readers to critically evaluate an investment thesis on holding companies trading at discounted NAV. Not all holding companies put their eggs in many baskets, some of them put most of their eggs in one basket hanging 10 meters above the ground.

Case Study 3: The Accounting Assumptions (Intrum AB)

The Discounted NAV:

Intrum (the debt collector/credit manager) seems to be deeply undervalued, trading at a fraction of its Book Value (Equity). Investors may point to the fact that they own massive portfolios of NPLs (Non-Performing Loans) and recently sold a chunk to Cerberus at a price close to Book Value, seemingly validating their accounting.

The Pitfall:

The “Book Value” of an NPL portfolio is an “accounting” value, which is entirely dependent on the Discount Rate used to value future cash flows. Intrum uses internal models (ERC) with a discount rate of 10-15%. Quoting from the Q4 2025 report “…discounted at the effective interest rate as determined at the time of the acquisition…“ - the report seems to use 13%. Essentially, the lower the discount rate the more “Book Value” the NPL will show.

On the opposite spectrum, we can see how much the market values the same risks by looking at the yield to maturity of Intrum’s own bonds - which range depending on maturity dates. These yields are higher than 13%, reflecting market concern.

The July 2026 bond yield is ~20%

The March 2028 bond yield is ~13%

The September 2029 bond yield is ~14%

When Cost of Capital > Return on Invested Capital, value is destroyed, not created.

The Numbers:

Let’s strip the accounting and the balance sheet down to see what the equity is really worth if we mark the debt portfolio with another discount rate.

- Value the “GoodCo” (Servicing):

The servicing business is capital-light. Let’s assume a somewhat generous 9x multiple based on the reported FY 2025 reported EBIT of ~3.5bn SEK.

GoodCo’s Intrinsic Value = 31.5B SEK

- Value the “BadCo” (NPL Investments):

According to the Q4 2025 report, the BadCo’s NPL portfolio has a Book Value of ~22bn SEK from a total ERC of ~46B SEK, discounted with 13% effective rate. If we re-price this at 16% yield, the actual present value drops by ~15%.

BadCo’s Intrinsic Value = 22.0 x 0.85 = 18.7B SEK

- Intrum’s Intrinsic value:

Total EV - Net Debt = (31.5B + 18.7B) - 44.0B SEK = 6.2B SEK

The “Book Value” of Equity is reported as 12.78B SEK in the Q4 2025 report, but the economic value might be closer to 6.2B SEK with non-conservative assumptions. If you buy at the current 6.75B SEK valuation thinking you are getting a ~50% discount to Book, you are actually paying at a slight premium to Intrum’s intrinsic value (if you believe my calculation).

So, what’s the alternative?

Value the GoodCo, Zero the Book.

The NPL portfolio is tricky to value due to the accounting assumptions. Let the debt holders own it. Calculate the intrinsic value of Intrum based solely on the Servicing business and the Net Debt. Looking at the current situation, the Servicing’s intrinsic value is actually “underwater” due to the Net Debt. Wait until it grows its EBIT, or the Net Debt lowers significantly (e.g. more sales of the NPL to pay down debt).

The Pitfalls of the Pitfalls

You cannot easily amputate the “BadCo” from the “GoodCo” like I did here. The Servicing business relies on the Investment book to feed it volumes. If Intrum stops investing, servicing revenues may decline. Furthermore, the Cerberus sale suggests someone is willing to pay near the accounting Book Value, though skeptics would argue that the sale was subsidized by the attached long-term servicing contract.

I also must admit that the market’s pessimism may eventually create massive opportunity if Intrum can successfully refinance its debt. However, banking on such a gamble is a speculation, not fundamental investing.

The most important thing: I want my dear readers to be patient. I understand that a turnaround may promise an exponential returns. However, Intrum’s turnaround is complex and the numbers show that the investment is in speculation territory. I would bide my time - quoting Peter Lynch “what is important is to wait for the actual evidence of the turnaround occurring, not just the symptoms.”

The Quick-Fire Pitfalls: Other Discounted NAV Illusions

If the above three aren’t enough to make you skeptical, here are some other quick-fire pitfalls:

The “Debt-on-Debt” Trap: A holding company that owns a subsidiary. Both carry debt. Even if the subsidiary makes money, it is forced to keep the cash to please banks and rating agencies. This leaves the parent high and dry, not being able to get the cash and pay its own bills and debts. The NAV is there, but you can’t touch it.

The “Class War” Trap: This is a structural trap where common shareholders are the last to eat. Preference shares act as “proxy debt” with a senior claim on both dividends and assets. In a stagnant company, their mandatory payouts function as a persistent tax, slowly bleeding the common NAV you thought you bought at a discount. If the company’s value drops, the preference holders stay “at par” while the common equity absorbs 100% of the blow.

The “Development Projects” NAV: This is similar to the accounting trap, but often applied to infrastructure projects. The company reported NAVs based on “Mark-to-Model” valuations of development projects (e.g. offshore wind, hydrogen). These are highly sensitive to interest rates. When rates rise, the project NPVs turn negative long before the quarterly report admits it on-paper.

Conclusion

When you see a company with discounted NAV, ask yourself: Is this a mispricing, or is it the market correctly pricing the risks? In most cases, it’s usually the latter.

NAV is an opinion. Cash flow is a fact.…

*

Disclaimer: I am not a licensed financial advisor. I do not hold positions in the securities discussed. The content provided in “The Northside” is for informational and educational purposes only and represents the personal opinions of the author. It is not intended to be, and does not constitute, financial, investment, legal, or tax advice. Investing involves risk, mostly the risk of losing money because you listened to a stranger on the internet. Do your own due diligence.*

Lähde: The Northside | Substack

3 Synes om

Det, der bekymrer mig mest, er, hvorfor hovedaktionæren hele tiden sælger sine aktier i højt tempo til disse priser (der sidder vel heller ikke inkompetente folk dér til at vurdere selskabets værdi og muligheder), og at der tilsvarende ikke er dukket nogen store købere op til at købe dem via blokhandler (samme bemærkning i parentes).

Kommentarerne fra fanklubben på Shareville har mest af alt bragt min finger tættere på salgsknappen.

1 Synes om

Forfatteren Northside havde trukket lidt i land på Placera-forummet. Han havde ikke taget højde for, at '26-gælden allerede var indfriet, og han havde også brugt for høje rentesatser for den resterende gæld. Placera Forum

6 Synes om

Nordic Capitals salg skyldes jo, at de er ved at lukke fonden planmæssigt, og midlerne skal tilbagebetales til investorerne. Intrum har blot været en del af det billede, og selvom de har haft en stor ejerandel i selskabet, har fonden været så stor og langsigtet, at optimering af slutkursen på Intrum-aktierne ikke er afgørende for fondens samlede afkast. De har modtaget store udbytter derfra gennem årene, og der var også andre selskaber i fonden. Fonden skal simpelthen bare lukkes. Det ville selvfølgelig have været bedre, hvis de havde fundet en ny ejer til aktierne gennem en blokhandel, men det ser ikke ud til at være lykkedes endnu. Nu kan man selvfølgelig håbe på, at en blokhandel falder på plads snart.

8 Synes om

Jeg læste også kun starten og Intrum-delen af det Bamford-link. Da de begyndte at tale om 2026-finansiering og finansieringsomkostninger på op mod 20 %, stoppede jeg med at læse. Samtidig blev det overset, hvor meget investeringsporteføljen forventes at give i afkast på lang sigt.

Jeg havde heller ikke lyst til at skyde det ned med det samme; det er jo fint nok i sig selv at dele alle mulige synspunkter.

Men den artikel var godt nok en forbier. Der var mest bare slynget ting ud, præcis som de faldt dem ind.

Man kan selvfølgelig lære af det, at lave værdiansættelser i sig selv ikke nødvendigvis betyder en god entry. Der er altid en grund til de lave værdiansættelser, men i samme åndedrag må man bemærke, at en lav værdiansættelse i sig selv heller ikke automatisk betyder en dårlig entry. “Markedet prissætter altid rigtigt” er som tankegang dog blevet modbevist mange gange, selvom det selvfølgelig kan ramme plet ligeså vel.

… Og derfor bør man i forhold til Intrum følge pengestrømmene (cash flows) og fremskrive de kommende års afkast. Den største risiko nu er primært, at der, stik imod ledelsens ord, bliver iværksat en massiv emission og hastet med gældsbyrden, men Intrum er ikke længere på vej mod konkurs.

5 Synes om

Findes der en kilde på dette? Jeg har forsøgt at undersøge det, men har ikke fundet bekræftelse på påstanden, selvom det lader til at være konsensus på flere fora.

Tak til alle, der har kommenteret Northsides blog.

3 Synes om

Jeg kan ikke pege på en kilde, hvor der står sort på hvidt, at NC VIII er ved vejs ende i sin livscyklus, og at de derfor tømmer porteføljen for at kunne begynde at opbygge en ny portefølje, hvor de støtter de næste virksomheder på deres vækst- og udviklingsrejse.

Denne NC VIII blev etableret i 2013; jeg har ikke undersøgt hele historikken for, hvornår Intrum kom ind i billedet. Men på det seneste har de også været i gang med at afvikle deres ejerandel i Noba Bank.

Og på NC’s hjemmeside kan man finde information om, at de ikke har tænkt sig at forblive ejere for evigt. Intrum har tilsyneladende status som “mission fuldført”, og ejerskabet afvikles gradvist.

Jeg har fulgt nogle andre selskaber, hvor denne NC Fund VIII er ejer, og her er salgene også fortsat. Dette exit vedrører ikke kun Intrum og virker mere som logik i fondskonstruktionen og regelbaseret aktivitet snarere end at Intrum er ved at kollapse, og derfor et exit.

6 Synes om

Jeg mistede også selv interessen for den artikel på det samme punkt. Det vil sige, at forarbejdet stort set ikke var gjort, eller også var det bare hurtigt sjusket sammen med AI. Det var dog flot, at forfatteren indrømmede sin fejl ovre på Avanza.

Hvis man vil have en lidt mere dybdegående analyse, som er lidt mere bullish, så er her en, der tilsyneladende er lavet af en norsk junior fra Nordea. Eller det konkluderede jeg i hvert fald ud fra LinkedIn, da vedkommende stadig var studerende.

Intrum writeup.pdf (593,1 KB)

8 Synes om

Sådan er det bare, alle gaps bliver fyldt. Intrum var nede og fylde det gap fra den 9.1, da kursen ramte 40,29 kr. Det går nedad med så stor volumen i dag, at NC vist dumper aktier for alvor nu.

Det er i øvrigt den længste periode med kursfald i 5 år, det vil sige 10 dage med rent rødt uden det mindste rebound. Desværre er vi ikke engang daily OS (oversolgt) endnu, så faldet kan fortsætte længere ned under 40 kr.

11 Synes om

Jeg lyttede til Q4-opkaldet:

-

Man kan læse mellem linjerne, at Investing-delen er ved at blive afhændet helt af nød. De nye mål peger også i denne retning.

-

Den tabte indtægtsside erstattes af en højere overskudsgrad i Service (35 %). Dette sker primært ved at skære i omkostningerne.

-

Intrum refinansierer i H1 i år gælden fra 2027 delvist med pengestrømme (1/3) og delvist ved at låne kapital fra markedet. CFO’en pralede med, at de vil få bedre vilkår på markedet end de nuværende lånevilkår.

Interessant at se, hvordan finansieringen for de kommende år hentes på markedet, sandsynligvis vil det på en eller anden måde være knyttet til egenkapitalen. Er der nogen her, der har bud på, hvordan finansieringen vil blive hentet på markedet?

1 Synes om