While looking at telecom operators, I came across Vodafone’s stock. Elisa and Telia have performed well in the early year turmoil, and I was looking for competitors with more affordable valuations.

Vodafone’s share price is at its lowest levels in the 21st century; only during the 2020 COVID-19 crisis did it trade below the current price. With a valuation of just under 40 billion euros, the stock trades below its book value, and according to Nordnet’s figures, the P/E ratio is around 15. The dividend yield appears to be 7%.

The company has had trouble making a profit, and revenue has remained flat for a couple of years, but could this be the winning telecom operator stock of the 2020s?

Any thoughts on the company as an investment? For me, this is a new acquaintance, even though the company’s brand has often come up during my travels.

8 Likes

Bumping this. The previous purchase didn’t go quite as planned (-26%, though dividends on top), but a few more thoughts after a quick look at the previous H1:

A debt-laden telecom company with a turnaround hopefully still in progress, which has been paying a dividend that’s almost too good (0.09 per year).

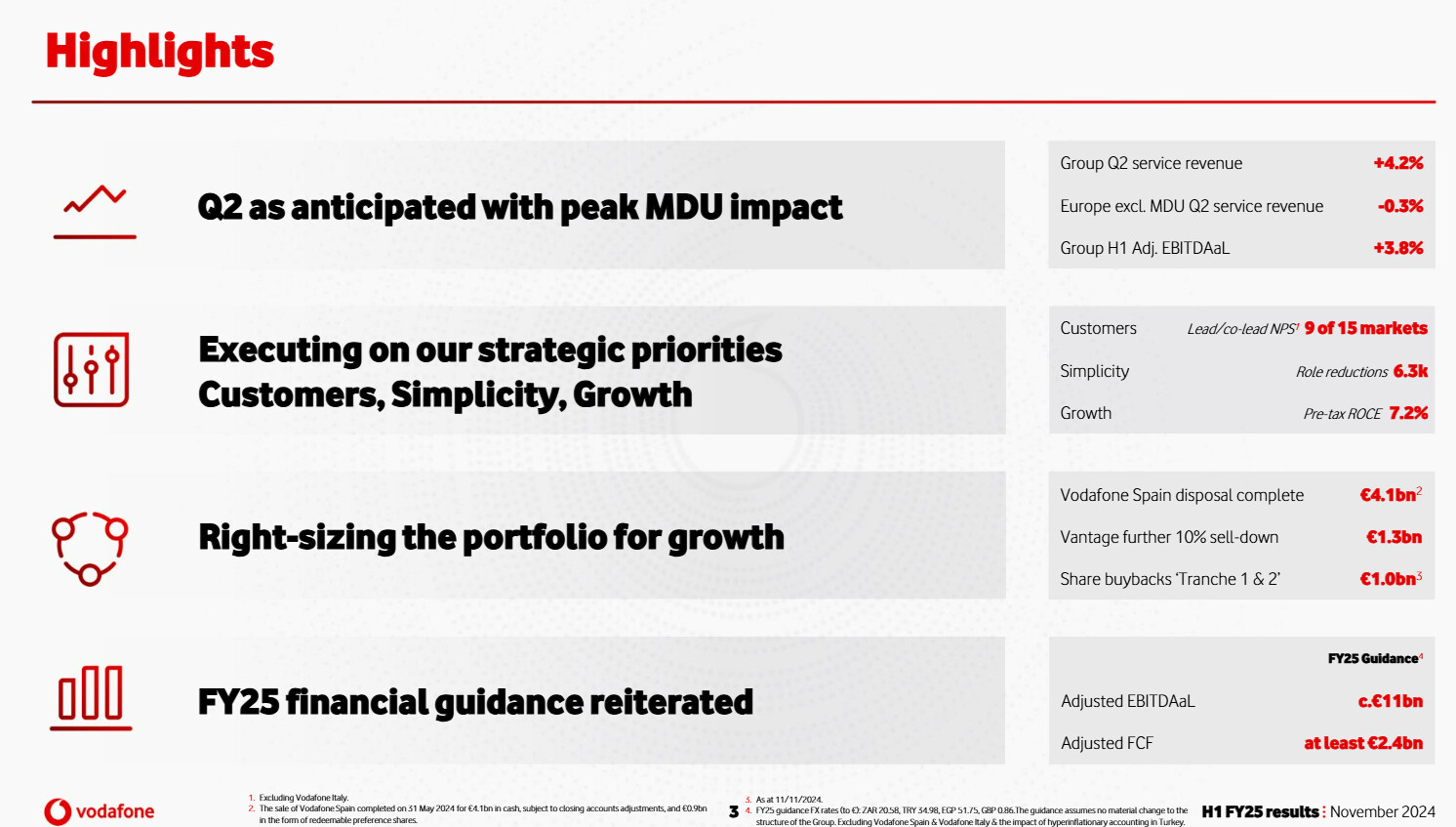

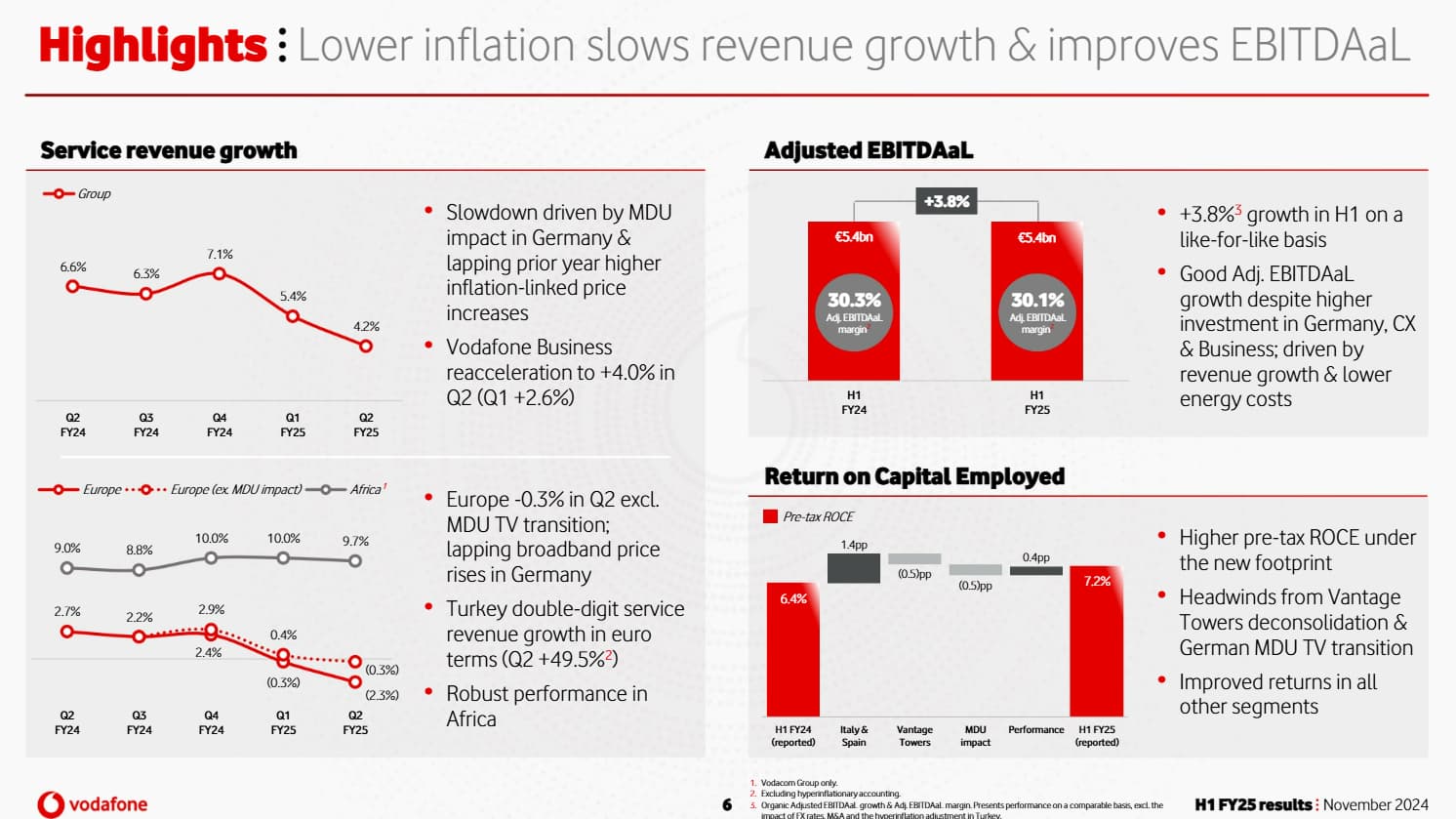

Some highlights from a quick read of the H1 (the Brits don’t really focus on quarterly reporting):

-

Could this be the Deutsche Bank of telecommunications? Although twice as expensive with P/B 0.52 and P/E 13 → 11.

-

As at 30 September 2022, the weighted average of cost of debt was around 2.5% and average bond maturity was 11 years, with all bonds held at fixed interest rates.

-

Current liquidity, which includes cash and equivalents and short-term investments, is €11.5 billion (€12.3 billion as at 31 March 2022). This includes €7.6 billion of net collateral which has been posted to Vodafone from counterparties as a result of positive mark-to-market movements on derivative instruments(€2.2 billion as at 31 March 2022).

And a bit of an image; the Africa option is very interesting, but I don’t want to pay much for it:

https://media.discordapp.net/attachments/750738134349906131/1070378912791658506/d611.png

I still need to read last year’s annual report (this company uses a really strange fiscal calendar, they seem to be in fiscal Q4 2023 right now) and see if I’ll stay on the horse for the long haul, exit, or realize earlier losses for tax purposes.

3 Likes

Vodafone has been paying a 9-cent dividend so far and the share price is around 80 cents. Do the math on that. Langenskiöld hyped this, a noteworthy point.

A 9-cent dividend for now. There is plenty of speculation about a dividend cut. The company has sold off operations aggressively and reduced its debt. Cash flow is declining, and there are cash-guzzling growth projects in its home country. Perhaps it is now doing the things it needs to do. The Spanish and Italian operations were likely sold at a low price, and the market doesn’t really like it, but a patient investor can still succeed with this one. After a few years of ownership and several additional purchases, I am still at a loss with this, but the dividends (even if cut) will eventually turn this into a profit.

• FY24 total ordinary dividend maintained at 9c

• FY25 total ordinary dividend rebased to 4.5c

• Ambition to grow dividend over time

• €2 billion buybacks upon completion of sale of Spain (FY25)

• €2 billion buybacks upon completion of sale of Italy (FY26)

• Subsequent review of potential for further capital return

• Vodafone Group Plc (“Vodafone”) announces today that the sale of Vodafone Spain to Zegona Communications plc (“Zegona”)1 has received final approval from the Spanish authorities. (source: London Stock Exchange | London Stock Exchange)

So the dividend will be halved, approval has been received for the sale of Spanish operations, and as a result, a 12-month €2 billion share buyback program will start tomorrow.

Next year another similar one if/when the Italian operations are sold.

Addition/Edit: oh right, and the intention is to get the merger completed with Three UK this year. Interesting times ahead!

4 Likes

Vodafone reported today. The results seemed to meet expectations. Europe (especially Germany) is still lagging, but Africa is doing great. If/when Europe can eventually be brought back to growth, this could turn out well.

“Vodafone maintained its guidance for its 2025 financial year of adjusted earnings before interest, taxes, depreciation and amortisation after leases of about €11bn and adjusted free cash flow to be at least €2.4bn.”

3 Likes

This week’s shotgun recommendations:

- Bernstein gives a “Sell” recommendation, target price 65 pounds

- UBS gives a “Hold” recommendation, target price 70 pounds

- Deutsche Bank gives a “Buy” recommendation, target price 140 pounds.

Maybe one of these will be right in some timeframe.

4 Likes

Vodafone’s stock is rising after French billionaire Xavier Niel’s investment firm acquired a stake of over 16% in the company. The market views the deal as a positive development, but investors are nevertheless closely watching whether the new largest shareholder intends to increase their influence in the future, etc.

The transaction price comprises approximately 110.5 pence paid in cash and Vodafone’s final FY26 dividend of 2.02 pence per share to be received on July 30, a roughly 15% premium to the July 9 closing share price. Vega has confirmed it does not intend to make a full offer for Vodafone.

As part of the transaction, e& terminated its Relationship Agreement with Vodafone and its board representative resigned from Vodafone’s board, marking “the end of e&’s efforts to exert influence over Vodafone’s strategy,” Barclays said.

https://www.investing.com/news/stock-market-news/vodafone-extends-gains-as-niel-stake-fuels-turnaround-hopes-4788072