I’ve researched but couldn’t find anything, so let’s open a dedicated thread for Elisa.

It’s very quiet regarding the company on the forum, even though it’s a big company. I personally believe the company’s growth will continue in the wake of mobilization, digitalization, and 5G.

Tomorrow is earnings day, from which I expect good results. However, expectations are so high, judging by the valuation, that a strong rocket might be too much work. In my opinion, there are many positive drivers from the past Q3:

The worst of Q2’s coronavirus impact was weathered without significant issues, so I see no reason why this development would have stopped now.

Specifically, Elisa’s 5G construction sites and advertisements have been very numerous in my neighborhood for a long time.

Changes in consumption targets due to the coronavirus, shifting from travel and other activities to subscriptions, phones, and other devices.

Related to the above, exceptionally high consumer spending capacity for private customers in Q3, thanks to holiday bonuses and tax refunds.

On the downside, apparently, roaming revenues are suffering for obvious reasons.

The big drop takes the stock price very close to the consensus from past results. It will be interesting to see what Inderes’ new recommendation will be, as the DCF value will probably rise with the decrease in the risk-free rate. At the same time, the stock price has also fallen significantly since the summer.

Elisa was interviewed for inderesTV for the first time. Here’s the video. We hope to continue doing interviews in the future, which would allow us to delve deeper into individual themes.

After sitting at Elisa’s headquarters for 1.5 hours, listening to questions and assessments from Elisa employees and analysts with half an ear, I thought I’d throw in a few bullet points here that will hopefully give someone a helping hand.

In Pasila, there seemed to be a very strong conviction that Elisa is clearly ahead of DNA and Telia in 5G. A quick glance shows Elisa with 5G in about 50 cities, Telia in about 40, and DNA in about 20. The number itself, of course, doesn’t make anyone better. Based on the comments, at this stage, it’s “good to keep” the biggest “capabilities” hidden from competitors. Who knows.

Apple’s 5G phones are expected to bring more momentum to the 5G market. 5G phones are already at the top of Elisa’s sales lists, but many don’t yet have a 5G subscription.

The conference call lasted over an hour, which surprised me, as it was the “boring” Elisa.

Elisa’s investments grew by 35% year-on-year, which raised some questions among foreign investors today regarding Huawei. Has Elisa started replacing Huawei devices with Nokia and Ericsson equivalents? No, the jump was basically due to “26 GHz frequency license investment” and “lease agreement for a new office space in Tampere”.

According to Elisa, it will use network equipment from all three major vendors: Huawei, Ericsson, and Nokia. Huawei is apparently clearly number one in terms of technology. If changes ever need to be made, they will be made gradually so that investments remain at most 12% of revenue.

A legislative amendment is currently being processed in Parliament, which, if it comes into force, would only allow 12-month fixed-term contracts for phone subscriptions instead of the current 24 months. Elisa (to my understanding) no longer has any fixed-term subscriptions, so from the company’s perspective, this should not have a significant impact.

Elisa is a well-managed, high-quality company, no doubt about it.

I sold the shares in January because they are still buying Huawei for mobile networks. I believe a large part of Elisa’s owners would like it if the link towers said Nokia.

Even at the risk of missing a few cents from EPS on a one-time basis.

A quick Google search reveals that Elisa and DNA are advancing with a three-pronged approach in 5G, using Huawei, Ericsson, and Nokia, while Telia relies solely on Nokia. In 4G, DNA went with Ericsson. More or less, everyone, however, has Huawei technology. Here’s a decent article from Aamulehti, according to which Huawei would not be used in the most critical parts in Finland.

Huawei’s position in operators’ current networks and its role in the construction of the 5G network is certainly a burning question for institutional investors globally at the moment. I don’t know, but I would guess that for some, it’s also a reason not to invest in the company. In investor relations (IR), Huawei certainly creates work in company after company.

Probably about a year ago, I received a sales call from Elisa, offering me several mobile subscriptions at a good price. I told them that my decision was a matter of principle: I would not take a mobile subscription from them as long as they built their networks with Huawei. This was assuming there was another operator at the same time that did not use Chinese suppliers. The next day, I received another call from Elisa. The matter had clearly moved forward, as the woman on the call asked me for my reasons. Even though I was not obligated to give them to her, I reiterated my view and said that because of this, my choice was Telia. She retorted that I didn’t care about paying elsewhere than Finland. All in all, her tone of voice lacked understanding and was simply very rude.

A couple of weeks ago, I received another call from Elisa. They certainly seem to be very active. Once again, I reiterated my view. I even received silent approval from the Elisa salesperson for my opinion. So, I was left with the strong impression that I am certainly not the only one who has thought this way and refrained from making contracts because of it. I also said that if their operations continue as they are, meaning they primarily use Nokia and Ericsson and leave Huawei out, I would consider returning as a customer for mobile networks. Something had changed then – both in the salespeople’s thoughts and on my part – I had started to think more positively about their operations. On my part, this was because I understood that 5G network expansions had been made primarily by relying on Nokia.

All in all, Huawei’s position in current networks certainly matters to customers, and also, with a delay, to investors. I argue that Elisa must react to the views of customers, especially corporate customers, in order to be able to continue the good performance of their business.

For private customers, it’s probably more a matter of principle which manufacturer’s devices are in use, and network functionality is more essential than the addition of one more Chinese party to all the other spies. For some companies, it’s probably different.

The emphasis on domestic origin that one sometimes encounters is not at all as black and white as is often made out. A great deal of the ownership of Finnish companies is abroad and vice versa, and no matter what nationality a company is, it always employs some number of Finns, and some portion of taxes always ends up in Finland.

We’re living in exciting times with Elisa, as the 40.79 level, a floor established during the corona era, is approaching.

In your opinion, when will the company’s share price be in buying territory?

Currently, the dividend yield is 4.3%. In this sense, it would be a good buy for an investment savings account (OST).

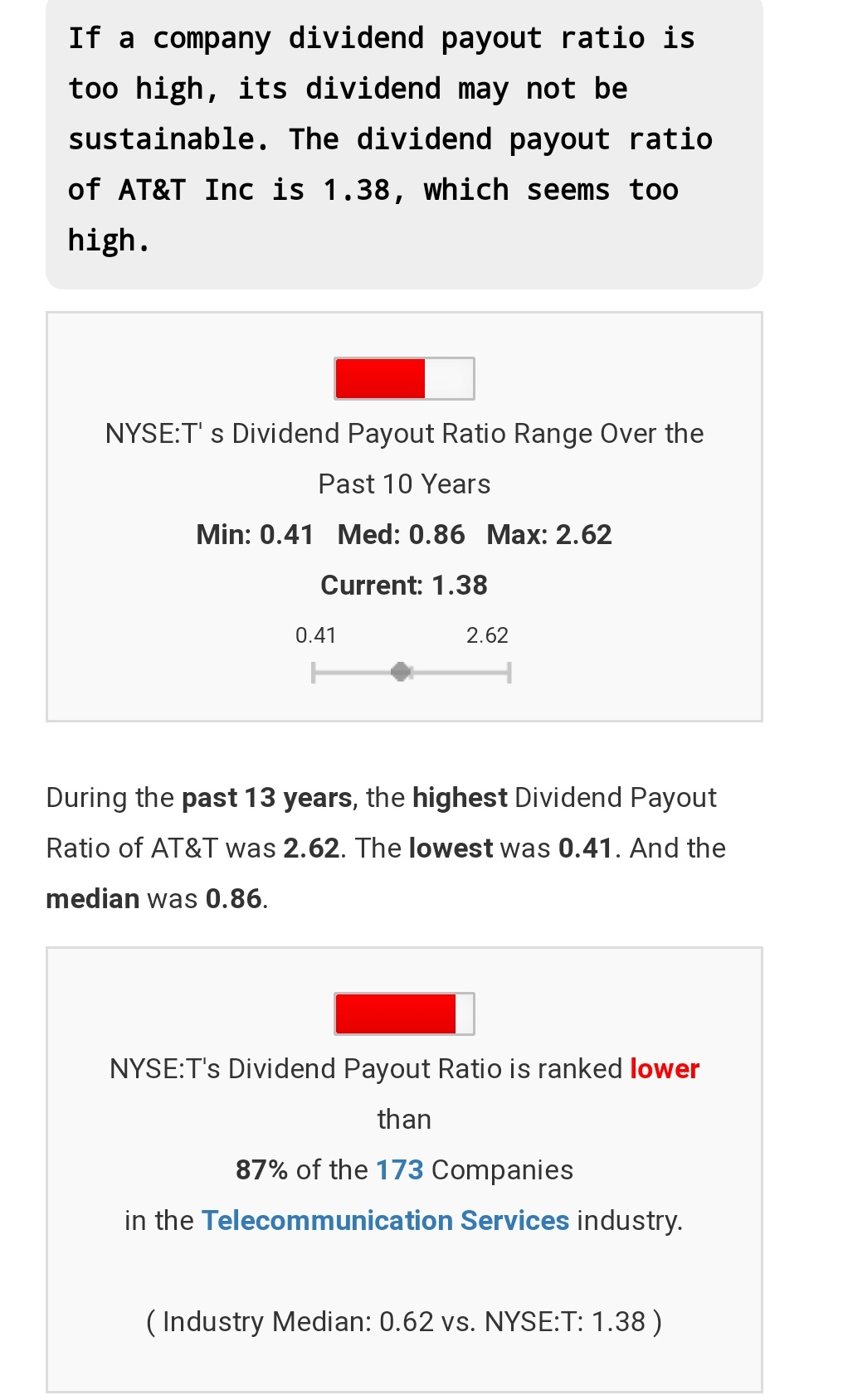

Last year, the dividend payout ratio was 95%. What is the healthy dividend payout ratio % limit for a telecom operator?

It’s better to look at ‘free cash flow per share’ than ‘earnings per share’. In this case, AT&T has made quite a few write-offs in recent years, for example, from the streaming services it acquired, which affect earnings but not cash flow. I don’t remember the exact figure by heart right now, but AT&T’s free cash flow per share and dividend ratio is at a sustainable level.

Yes, that news initially caused some surprise.

I’ve since learned that the goal is still to automate mobile network cell planning. The resulting software tool can then be sold to other operators. Comptel immediately comes to mind. It was once a very profitable company and sold software internationally to mobile operators for adapting billing data from mobile network exchanges to commercial computers. This acquisition might turn out to be quite good.

This fits perfectly with Elisa’s strategy, which aims to grow its international digital business. Elisa already heavily utilizes artificial intelligence and robotics in its network. The IoT+5G breakthrough in industry, spiced up with CamLine’s software, could be a significant business for Elisa in the future.

Elisa is a familiar and safe investment for everyone, but at least here in the Inderes community, the company doesn’t seem to attract interest.

Based on the “What’s in your portfolio” thread, only a few users have Elisa in their portfolios. Among the typical targets, Sampo and Fortum are in almost everyone’s portfolio.

In the buy/sell thread, Elisa is mentioned very rarely. Around its competitor Telia, there is constant discussion, views, and many transactions.

Can @Joni_Gronqvist estimate why Elisa doesn’t interest the Inderes community? Is the dividend too low? The profit, however, consistently and predictably moves forward year after year.

I could, of course, be wrong, but I think the high price of one share (€50 vs. Telia’s €3) psychologically affects investors’ interest, even though it shouldn’t really matter.

The company should perform a stock split to increase trading and interest.

Interesting question, I can’t say directly, but I have a couple of thoughts on it. First, regarding valuation, Elisa was long at a clear premium to its peer group, which is why peers might have been more interesting. Second, Elisa has been a very well-tuned company for a long time, and significant earnings potential has been difficult to find compared to its peers. Third, if you compare operators to several faster-growing sectors, the organic growth of traditional operator business is challenging and very moderate.

From the latest report, here are a couple of reasons why we turned positive on Elisa after a long period of a negative view:

• 5G and digital services are starting to support moderate growth. The Q4 report and comments on 5G and digital services gave us more confidence in our moderate growth forecasts. During 2020, Elisa’s 5G network coverage expanded to cover 2 million people in Finland, and the number of 5G subscriptions was nearly 200,000. In our view, 5G coverage and Elisa’s existing customer base provide a good basis for 5G sales in 2021 and for accelerating the development of mobile service revenue. The share of digital services is still small compared to the total (estimated at about 15% of revenue), but it is gradually starting to support growth more strongly.

• Valuation outlook has turned cautiously positive. Elisa has a strong market position, and its risk level is among the lowest in the sector and the stock market. The low risk is reflected in the company’s bond, issued last year, having Finland’s lowest coupon rate (0.25%) and the debt portfolio’s very low average interest rate of 1%. Elisa’s earnings-based valuation (P/E and EV/EBIT 2021e 23x and 21x) remained unchanged in Q4 and is cautiously moderate considering the improved earnings growth outlook and the low interest rate environment. The premium to its closest peers Telia and Tele2 is also broadly unchanged, “only” slightly over 20% and 0% above/in line with peers. Thus, the relative difference to its closest peers is not that significant, and it is largely justifiable by Elisa’s lower risk level and stable moderate earnings growth. Our total return expectation for Elisa’s stock (3% earnings growth and 4% dividend) exceeds our required return. In addition, the DCF calculation also supports the valuation, although the value is strongly weighted towards terminal period cash flows. In our view, the clearest risk in the stock is related to rising interest rates, as the company’s history of operational performance is convincing.

If others have their own views on why they have not invested or why they have invested, I would be interested to hear!

I myself only jumped into Elisa after the Q3 “disappointment” caused a drop in the share price, as I interpreted it as a pretty strong overreaction. I’ve been following the company for years and always considered it too expensive, even though I’ve wanted to own it. My take on the earlier messages is that companies with relatively stable and easily predictable businesses but valued at “solid” multiples don’t really generate much discussion here anyway (like Huhtamäki, Kone, etc.). Speculation is difficult to engage in when, until now, revenue and profit could be estimated with ±1…2% changes compared to the previous period. Given this, Elisa’s share price reactions have been quite strong in my opinion. With acquisitions and 5G, there might gradually be more growth speed. OP’s forecasts for this year indicate a 3% and for next year a 5% increase in EPS. I was going to quote parts from OP’s report here, but at the end, there was a note stating “distribution without written permission is not allowed.”