There’s certainly enough business. Gaming Service would be a truly scalable component, but it only concerns a small portion of Unity’s customers. From that very page, “Beta” and “Free” immediately catch the eye. There are paid services there too, but how much money do these services generate now? What about this year?

For comparison, Unreal Engine’s 5% of all game revenue is a scalable component that Unity lacks.

I’ve interpreted it (I seem to recall reading about it somewhere, but I can’t find it on Google right now) that Operate is essentially revenue-sharing / pay-per-use business. So, its figures should give at least a rough answer to your question.

Create, on the other hand, is more traditional license sales. A relevant question, I suppose, is what the monetization model will be for the capabilities gained through Weta and other acquisitions in the future. Will it be a revenue share model like Unreal, or something else?

Edit: I found it; it’s stated right in the IPO S-1 document:

We generate subscription and associated professional services revenue from the sale of Create Solutions. We generate revenue-share and usage-based revenue from the sale of Operate Solutions

Edit 2: Reading the document more closely, there’s even more detailed information about Operate’s operations (though it’s 1.5 years old and doesn’t cover any subsequent acquisitions):

Our monetization revenue is based on a revenue-share model. Our customers and advertisers use our end-user acquisition solutions to acquire new users on a pay-for-performance basis. Our customers use our monetization solutions to generate revenue through advertising and in-app purchases. We facilitate all of this through our real-time Unified Auction. We retain a share of the revenue that is generated through this auction.

Usage-based revenue primarily comes from our deltaDNA, Multiplay and Vivox products. The majority of revenue from deltaDNA is generated based on the number of active users in the application each month. We generate revenue from Multiplay based on a customer’s hosting needs, including use of storage, compute, processing and bandwidth. We generate revenue from Vivox by charging customers based on the number of peak concurrent users in any given month and offer the product for free for up to 5,000 concurrent users.

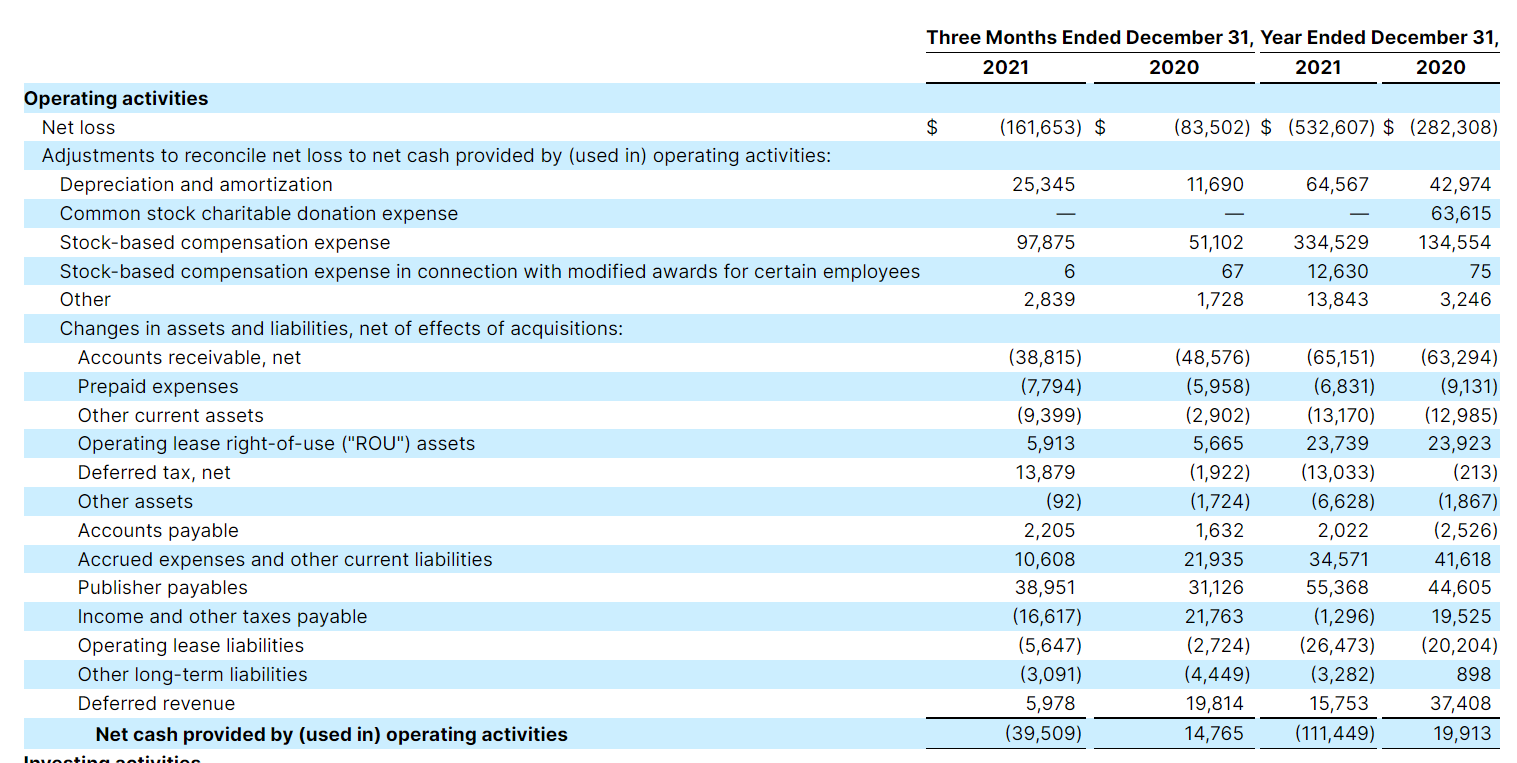

The cash flow adjusted for business combinations is already significantly better than the GAAP result. SBC naturally does not affect cash flows.

The 2021 annual report has not yet been released, but the topic has already been discussed in the 2020 report.

Riccitiello said, if I remember correctly, in the Q4/2020 call that they have no intention of charging developers for their output (like e.g. Qt and distribution licenses), but that they retain all rights to their revenues. But on the other hand, this is related to monetization, which scales with the popularity of the outputs.

I must admit I’ve somewhat underestimated the advertising side of Operate. So, over half of Unity’s revenue is still highly scalable business. I’ll have to crunch some numbers, but it still seems expensive.

The operating cash flow is also quite a bit in the red. The “most unprofitable” SaaS companies run this in the black (e.g., Cloudflare, Datadog, and Snowflake). As do, for example, Spotify on the consumer side and Roblox in gaming.

As I said, operating cash flow is significantly better than GAAP earnings.

As for unprofitability, everything depends on the company’s development stage and growth investments. Unity stated a year ago that they would only become profitable (non-GAAP) in 2023, specifically due to growth investments.

By crunching the numbers, one could also see the situation such that if Unity had frozen its expenses after gross margin (R&D, SG&A) last year at the 2020 level, non-GAAP earnings would be positive by approximately $400 million.

The gross margin is a staggering 80%, so I eagerly await scalable growth in the coming years.

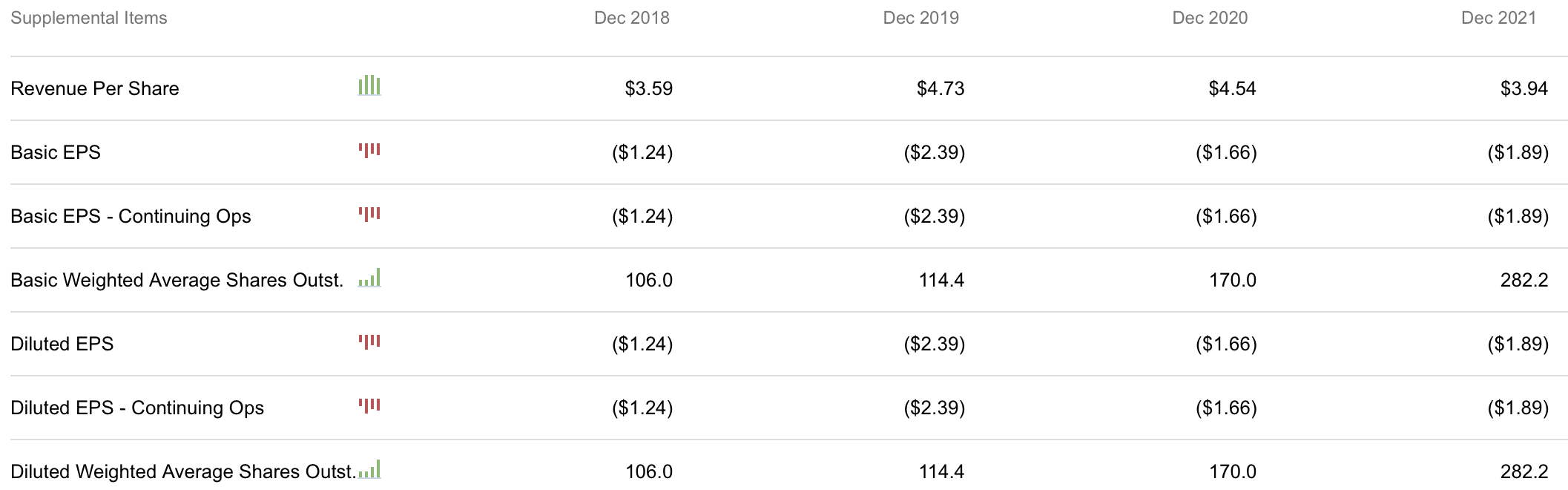

I haven’t looked into the company in detail, but what’s behind the increase in the number of shares (other than excessive share-based compensation)? By the end of 2022, the number of shares is estimated to be 350 million.

The year Unity freezes its R&D expenses, it will fall behind. They have an ever-growing palette of technologies, more demanding customers, and so on, so R&D expenses will continue to grow faster than mere wage inflation, which is also very high in a specialized software company like this one, both now and in the foreseeable future. One cannot achieve over 40% revenue growth and pretend it won’t affect ongoing expenses. Retaining customers also costs money, so SG&A will grow with them.

Those numbers are the averages for the respective years, so the 2020 figure also includes the period before the IPO. That’s a big jump. You can get a better picture by comparing Q4/2020 and Q4/2021 figures, for example: 272 vs 288 million (approx.).

Perhaps my point didn’t quite come across (or you just won’t admit it), but I’ll try to explain how I see the costs.

So Unity has a growing palette of technologies and demanding customers. I agree with this. But the fact is that maintaining existing technology doesn’t cost as much as developing new technology. However, I naturally don’t suggest that developing new technology should be stopped to make the company profitable quickly.

There was talk at the conference that non-GAAP profit will continue to develop in line with operating cash flow. And non-GAAP profit breakeven is expected in 2023; I personally guess it will be this year, as Unity tends to be conservative with its guidance.

Unity is already a 17-year-old game engine and it’s still under development. Technology and requirements change so rapidly that nothing ever becomes “finished” where it would only be maintained. It must also be taken into account that in software, development and maintenance become more expensive as complexity grows superlinearly.

I work in the industry and have over ten years of experience in making game engines and using UE4 and Unity. This is not like the tobacco industry where old investments could simply be used to generate cash flow.

So your take is (correct me if I’m wrong): Unity still needs to significantly increase its investments in the coming years to keep revenue growing, which is why it won’t be profitable for years, and even then, it won’t scale significantly.

My take: non-GAAP and operating cash flow will be positive by 2023 at the latest, and the business will scale nicely after breakeven.

Both of us have probably made our stances clear, so there’s no need to continue this discussion.

Let’s rather talk about this. How do you personally feel about Unity’s tools? Pros, cons? How have they developed over the last couple of years? Compare to U4E? What game engines have you been working with?

Unity’s product is very good and competitive. It’s easy to customize for your own needs, but only up to a certain point because the source codes are not freely available. You could get them for money, but it’s not recommended. With UE4, on the other hand, all source code is freely available and modifiable. You could fix engine bugs yourself and send the fixes to Epic on GitHub. This is what I missed most in Unity.

In the last 5 years, Unity has caught up a lot with UE4 in terms of graphics engine and performance. In places, it has even surpassed it. The editor and tools’ performance is significantly better, which speeds up work tremendously. In UE4, I spent several hours a day just compiling code. I don’t see anything wrong with the product, and it competes equally with its rivals. I haven’t tested UE5, but it seems to have taken a really big leap forward.

I don’t want to talk too much about my own game engines to maintain some level of anonymity, but I’ve worked on in-house 3D game engines for PC and mobile.

In summary, regarding the investment case: Unity’s success will not be due to the product itself.

Edit: @Kesa86 I have no experience with the Unity service part.

Interesting. How do 3D engine products compare to other software products? For example, it’s hard to make good money with web browsers, because big tech companies have their own browsers and there are also open-source alternatives. On the other hand, you can still make money with databases. Is there an open-source risk in this area, or a risk that a big tech company decides to make its own 3D engine?

It’s still possible to make a graphics engine almost competitive as a free open-source product, but the problem becomes tools and multiplatform support. These are more boring things to code but take a lot of work to get really right. These can still be found on the 2D side.

Amazon has made an attempt with the Lumberyard engine. They bought the CryEngine as a base and started developing from there. However, it hasn’t gained any real momentum in my opinion. One reason why I wouldn’t consider this a threat is that game engines are really complex and require years and years of investment. And customers are already committed to the existing ones.

So, even though game engines are expensive to make and maintain, they are still a bit of a niche business. They only manage to capture a small share of the value chain. Epic takes 5%, Unity even less. Then again, the MAGMA crowd takes 30% without really doing anything for it. They just keep the marketplace up and running and handle the money transfers. So there aren’t very big incentives here. Unless they buy an already finished product from somewhere. One reason why giants might want to get into this business is to subtly introduce their own cloud service, ad tracking, etc.

Good to hear that the game engine works. But the success of Unity’s investment case largely depends on how the additional products or services related to the game engine, as well as all non-gaming tools, perform. Do you have experience with anything other than the game engine, e.g., monetization?

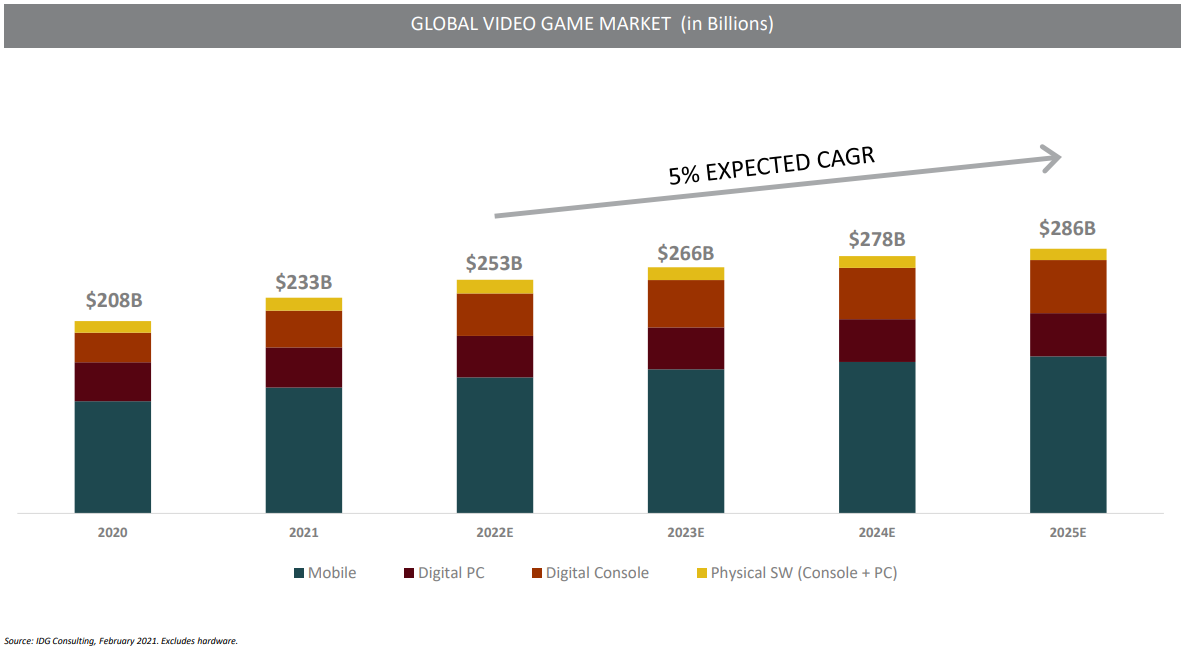

The actual revenue of the gaming industry last year was $233 billion. Growth is estimated at 5% annually.

If we unrealistically assume that Unity would suddenly grow to its entire market potential. Let’s say the market is roughly divided into three parts: In-house engines, Unreal Engine, and Unity. This means games made with Unity would generate $77.6 billion in revenue.

If we assume that Unity captures 5% of this, which is also the slice Epic takes.

So, Unity’s revenue would be $3.88 billion with 5% annual growth. What kind of P/S ratio would one dare to put on something like this? Let’s say 5-10. So the valuation would be something like $19.4-38.8 billion if Unity suddenly reached its maturity. Unity’s market value is now $31 billion.

So, the markets either value Unity’s business from other sectors, a significantly larger share of the gaming market than I assume, or a considerably larger slice of the games made with it. Or perhaps all of these.

Time will tell how wrong I am.

Unity gets over 60% of its revenue from digital advertising, mainly from in-game ads embedded in games. This is due to the Applifier acquisition years ago.

Your estimate of 5% of the global gaming market probably doesn’t include this part of Unity’s business, does it? The global digital ads market is probably something like 400 B USD in addition to the gaming market.

I’m not familiar with the technology, but I would imagine that a game engine product is a “cheap” purchase, and additional services, especially digital marketing tools, can generate high-margin business. Qt is building on the same idea.

In my opinion, it’s quite clear that a large part of Unity’s current market value comes from everything other than the game engine, and partly even from things other than related services/tools. Keywords that Unity cultivates and from which potential is seen to come: AR/VR, RT3D, non-gaming industries (automotive, retail, etc.).

We can, of course, debate whether this should be the case or whether Unity’s value is solely in the game engine. My opinion has probably already become clear.

You can even get that game engine for free, so it’s quite a loss leader.

Global gaming revenue also includes in-game ad revenue. Most digital advertising is not in games. I can’t say how much Unity takes from those ads, but I would roughly estimate 5-10%.

Revenue from in-game ads is expected to continue its remarkable growth, increasing from $42.3B in 2019 to $56B in 2024

A very good and interesting discussion regarding Unity. For me, this investment story is largely based on the megatrend of gaming industry growth and, for example, social gaming and other hockey stick type underlying drivers.

Pricing power and the company’s moat (and its growth potential) are always reasonable questions, but I believe Unity is doing exactly the right things (investing in growth, product development, and several sub-segments) within its ecosystem. I see a lot of similarities here to Amazon’s pre-2013 AWS investments (and the discussion follows similar guidelines ).

Unity has the potential to be one of the winners of the social commerce trends mentioned in Ark’s Big Ideas 2022 report: