NVIDIA - Enabling the Impossible

NVIDIA provides, both now and in the future, a significant portion of the programming and computing power required globally for customer needs across many industries. In the company’s case, the adjective “disruptive” doesn’t quite do it justice, as its solutions create something unprecedented—entirely new business. In my opinion, it is one of the most innovative companies in the world, capable of combining cutting-edge science and ICT for the benefit of its customers.

NVIDIA could be viewed as a “general store,” and why not? But almost always, the common denominator of its solutions is taking computing capacity to a completely new level. NVIDIA embodies those qualities that often lead to top success in U.S. companies: a founder who is still at the helm and a modern personnel policy: ”There’s only one team at NVIDIA. That means no politics, no hierarchy”. The company understands its responsibility as part of the community, and ESG is taken into account in its operations.

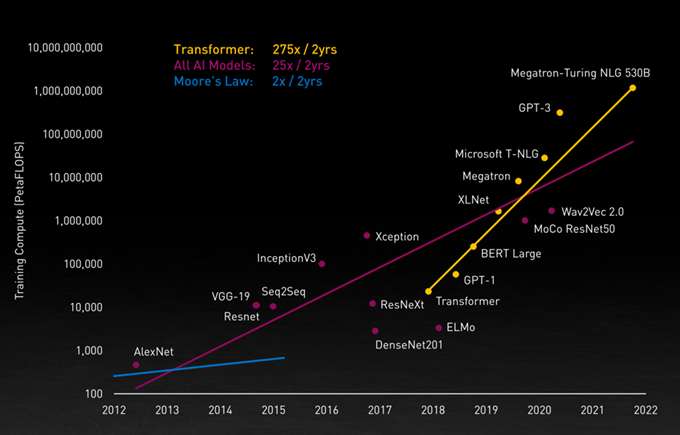

The image below is taken from the company’s Q3 presentation. It shows that the growth in computing capacity has surpassed Moore’s Law (blue line). Megatron-Turing (top right) is a recent joint venture between NVIDIA and Microsoft to develop interaction and understanding between humans and systems. This image perfectly illustrates my summary of the company: it innovates with the power of the best talent → then the company networks → and thus something entirely new is created for this world. This is why NVIDIA deserves its own thread here on the forum.

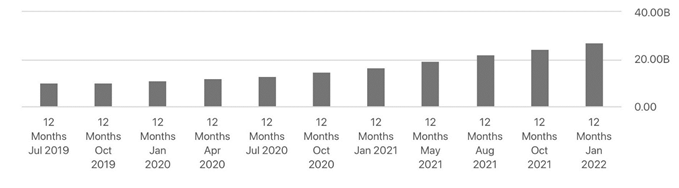

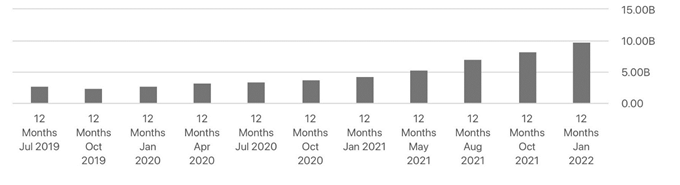

NVIDIA belongs to that class of companies where “holding” requires great staying power and constant reading to have the stamina and courage to ride through dips, stagnant periods, and red days. I believe the latest investor presentation (below) is very much in the moment—and provides a good look into the near future.

https://s22.q4cdn.com/364334381/files/doc_financials/2022/q3/NVDA-F3Q22-Investor-Presentation-FINAL.pdf