Thomas has made a new company report on Tulikivi after Q2.

Tulikivi’s Q2 figures were weaker than our expectations, but the continued growth in order flow balanced the overall picture of the report. With the soft interim report, we expect the company to fall short of its revenue guidance despite positive developments in the latter half of the year. We reiterate our target price of 0.42 euros, but update our recommendation to reduce (previously sell).

Quoted from the report:

Although our forecasts for the end of the year anticipate an improvement in the current year’s performance level, our revenue forecast is still slightly below the previous year’s, and our earnings forecast is in line with the comparison period. Thus, we see a clear earnings warning risk. From an investment story perspective, however, a mild earnings warning would be irrelevant if the recovery in earnings continues as expected during the rest of the year and the company manages to turn its revenue into sustainable growth by expanding its distribution network and investing in new product launches.

Here are also Thomas’s comments on Tulikivi’s negative profit warning.

Tulikivi’s negative profit warning was not a significant surprise, as after a weaker start to the year compared to the reference period, achieving the guidance would have required a really strong end of the year. In our view, looking at the upcoming interim report, it is crucial whether the trend indicating recovering demand seen since the end of last year has broken, or if the profit warning is merely due to a shallower recovery slope than anticipated. With the profit warning, we see downward pressure especially in our profitability forecasts.

Thomas has made a new company report after Tulikivi’s negative outlook.

Tulikivi’s negative profit warning was not a significant surprise, but it makes the recovery of demand seem shakier than before. We have lowered our forecasts, especially for the current year. We still assume that the bottom of the fireplace market demand is behind us and we see Tulikivi having the prerequisites for significant earnings growth as the market recovers. We revise our target price to 0.40 euros (previously 0.42 eur) driven by forecast changes and reiterate our reduce recommendation.

By the way, have sand batteries been considered as a source of income for Tulikivi? In that Polar Night Energy sand battery, Tulikivi’s crushed soapstone was used. So I was thinking, if similar batteries start to be built, Tulikivi’s product is probably the best for them.

Perhaps the real market area for Tulikivi’s raw material would be Finland, which limits its commercial significance. If Polar Night’s solution became truly popular, it would certainly have economic significance for Tulikivi as well.

I myself don’t believe this has very great economic significance for Tulikivi.

The following news update is from Nordic Talc Oy’s website.

Our Talc Project is Advancing Strongly – Responsibly and Diversely

The project is progressing as planned in several areas: permit processes, technical design, utilization of by-products, and sustainability goals support each other and move the overall project forward. We have continued active dialogue with potential customers and financiers – and received positive feedback on the project’s progress. Environmental Actions at the Core

• Pre-monitoring of surface and groundwater continues – for surface waters, at nine points all the way to Kiantajärvi.

• The long-term behavior of mine waste is being studied with humidity cell tests.

• In the summer, we carried out supplementary nature surveys on the conservation values of the Portinvaara Natura area.

• We are awaiting a request for additional information regarding the environmental permit application submitted in spring 2025. Technological Development

• The energy and material efficiency of beneficiation technology was improved through early-year studies, which were tested at GTK/Mintec.

• Based on the results, we are updating the preliminary design of the concentrator – aiming for significant cost-effectiveness.

• Technical design is also progressing regarding the drying of talc concentrate and fine grinding tests. Magnesite – A Critical Mineral at the Core

• Utilizing magnesite from the tailings would support the EU’s self-sufficiency goals for critical minerals – over 90% of the EU’s magnesite is imported from China.

• We continue preliminary studies to increase the value and promote the utilization of magnesite. Towards Sustainable Mining

• Our goal is to create sustainable and impactful practices for the project regarding natural resource use and environmental responsibility.

• We will set clear sustainability goals and metrics to monitor them.

Thomas, you haven’t pre-partied, because Tulikivi will announce its results on Friday.

Tulikivi will publish its Q3 results on Friday, according to our estimate, at 1 PM. During the current year, the company has managed to turn its order flow and backlog back to growth, but based on the profit warning issued in September, the recovery in demand has not been rapid enough to achieve the guidance given at the beginning of the year. After a nearly two-year period of revenue contraction, we expect Tulikivi’s revenue to have returned to growth in Q3. From the report, we are looking for confirmation of the continued recovery in demand.

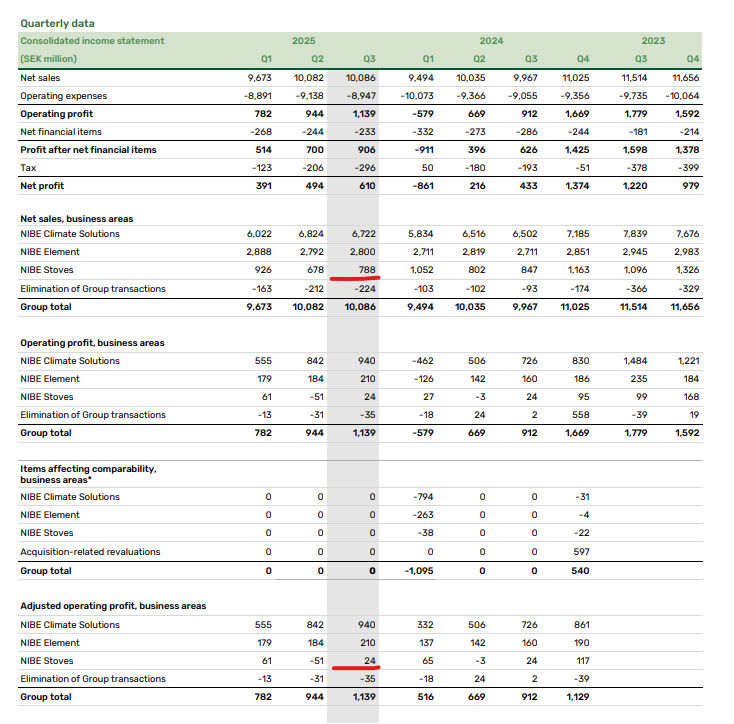

Here is a new company report from Thomas on Tulikivi after Q3.

Tulikivi’s Q3 report fell short of our expectations due to weakened order intake. Looking further ahead, we see the company having the prerequisites for strong earnings growth, supported by an expanded distribution network and the cyclical recovery of the fireplace market. However, at the current valuation level, the waiting period seems too long until we gain visibility into demand recovery. We lower our target price to EUR 0.38 (previously EUR 0.40) and our recommendation to sell (previously reduce).

NIBE published its Q3 report on Friday, which at the group level showed cautious revenue growth and significantly improving relative profitability. However, the most challenging segment for the company was Stoves, which competes with Tulikivi. For this segment, comments indicate a cautious recovery in demand in North America, although this seems to be focused on gas stoves. In Europe, demand for the segment remains at a weak level, and overall demand development for the segment has fallen short of the company’s own expectations. For the Stoves segment, revenue decreased from the comparison period, and operating profit was at the previous year’s weak level. NIBE’s Stoves segment suffers from US tariffs, but European demand also appears challenging based on the comments. In Sweden and Norway, demand for the segment has weakened. In Denmark, there has been a slight improvement. In Germany, demand has sharply declined from a strong comparison period level due due to falling consumer energy prices. In the UK, the market is returning towards traditional consumer behavior, although overall demand has contracted.

My main conclusion based on NIBE’s report is that the subdued development shown by Tulikivi is indeed market-driven, and the demand environment is currently very challenging. If competitors were to start recovering and Tulikivi were to fall behind, I would question the company’s competitive development, but based on the development of the truly high-quality NIBE, I would not take that stance at this stage.

We have submitted the supplements requested by the Regional State Administrative Agency for Northern Finland to the environmental and water management permit application for the Suomussalmi talc project. The supplements concern, among other things, the assessment of the project’s impacts and technical solutions.

The key supplements included more detailed information on the methods used in the treatment of operational wastewaters and an assessment of the achievable residual concentrations for key pollutants. In addition, the cumulative impacts of the Kivikangas quarry, the current overburden area, and the planned talc production were assessed, as well as solutions related to combining the overburden areas.

The permit authority will continue processing the application.

The company’s goal is to enable a modern, carbon-neutral, and traceable talc production facility at the current factory site of the Suomussalmi soapstone quarry and factory.

Tulikivi, a manufacturer of heat-retaining fireplaces based in Juuka, North Karelia, has continued active business operations in Russia during the years 2023–2025. The value of exports is approximately 2.5 million euros.

Yle’s information is based on Russian and international customs data.

In 2022, Tulikivi announced it would wind down its Russian operations immediately after the start of Russia’s war of aggression.

Despite the decision, soapstone, ceramic stone, fireplaces made from them, and parts for fireplaces and sauna heaters have been exported to Russia.

Ilmarinen is Tulikivi’s largest institutional owner. The company states it is holding discussions with the companies it owns to promote responsibility.

Deviations from the company’s responsible investment principles are not accepted, such as those related to sanctions against Russia.

– We do not accept the enabling of Russian trade through the circumvention of sanctions, responds Karoliina Lindroos, Head of Responsible Investment, to Yle.

Efforts are made to end misconduct through engagement.

– If engagement does not yield results, we will divest from the investment where possible, Lindroos states.

It brings to mind another case where an authority threatened to throw not only the management but also the employees in prison if operations didn’t continue. It might have been social media exaggeration, but it’s probably better to clarify the situation first and make a fuss later.

This isn’t activity subject to sanctions, meaning no laws have been broken, but voluntary withdrawal is still highly recommended.

Tulikivi has been looking into the situation for 3.5 years, but nothing has happened. It’s good that a noise is being made.

I’m a bit surprised that this comes as a surprise to Tulikivi’s largest owners. The Russian business hasn’t been hidden in any way; instead, information about the continuation of operations can be found directly in the annual reports. It’s just that no one has been interested.