Then I threw some numbers into Excel.

Q1 Average|Q2 Average|Q3 Average|Q4 Average| [2015-2019][million €]

Revenue |6.06|7.82|7.2|8.72|

Group profit before taxes |-1.4|-0.14|-0.12|-0.36|

Order backlog|4.58|3.86|3.72|3.18|

Q1/20|Q2/20|Q3/20|Q4/20 [million €]

Revenue|5.7|7.4|6.9|?|

Group profit before taxes|-0.7|0.3||0.4|?|

Order backlog|4.4|3.3|4.0|?|

From these, it can be seen that revenue and order backlog have remained pretty much unchanged, but a pretty big chunk has appeared in the profit.

Prices have reportedly been raised and some savings have been made. This explains at least partly.

A hell of a lot of debt too, but the new products actually look good.

Speaking of debt… in the video, Harri Vauhkonen says that debt has been paid down by 12 million over 5 years and now the debt is 15 million.

I’m quite a novice at investing. A real investor wouldn’t dare to bring up Tulikivi (a Finnish ceramics company) seriously. It’s often used as an example of a bad company.

Could wiser people tell me what I’m not understanding at all, or are these possibly the first steps of a turnaround…

The lockdowns in Germany do worry me a bit. Half of the revenue comes from exports, and a significant portion from Germany.

It’s great that you made a separate thread for this. Prejudice kills too many good trades, at least for me. Additionally, a profitable year for Tulikivi is an achievement worth a thread in itself.

Even if the most likely scenario plays out and it turns out to be a bad company, this thread can still be useful. Avoiding bad trades is at least as valuable as making good ones.

You could, however, take a screenshot of the Excel file with the snipping tool or share it via Google Sheets.

I was looking at the same guy’s thread on vauva.fi when I was Googling, but I’m a different person.

It was hard to find any intelligent discussion about the company, though.

I also thought about bringing up the hype surrounding this company here. Especially the user Předák on Shareville, repeatedly with apparently unsubstantiated stories. The good thing is that expectations for the company are so low that no one has lost much money with this since 2015. A few tens of percent at most.

In itself, the opening of the thread cannot connect one person to another. Besides, the language used by this poster differs negatively from how the puff piece I saw was written.

Well, Inderes, however, differs from the aforementioned places in its moderation, so if a troll is found here, they won’t be found for long.

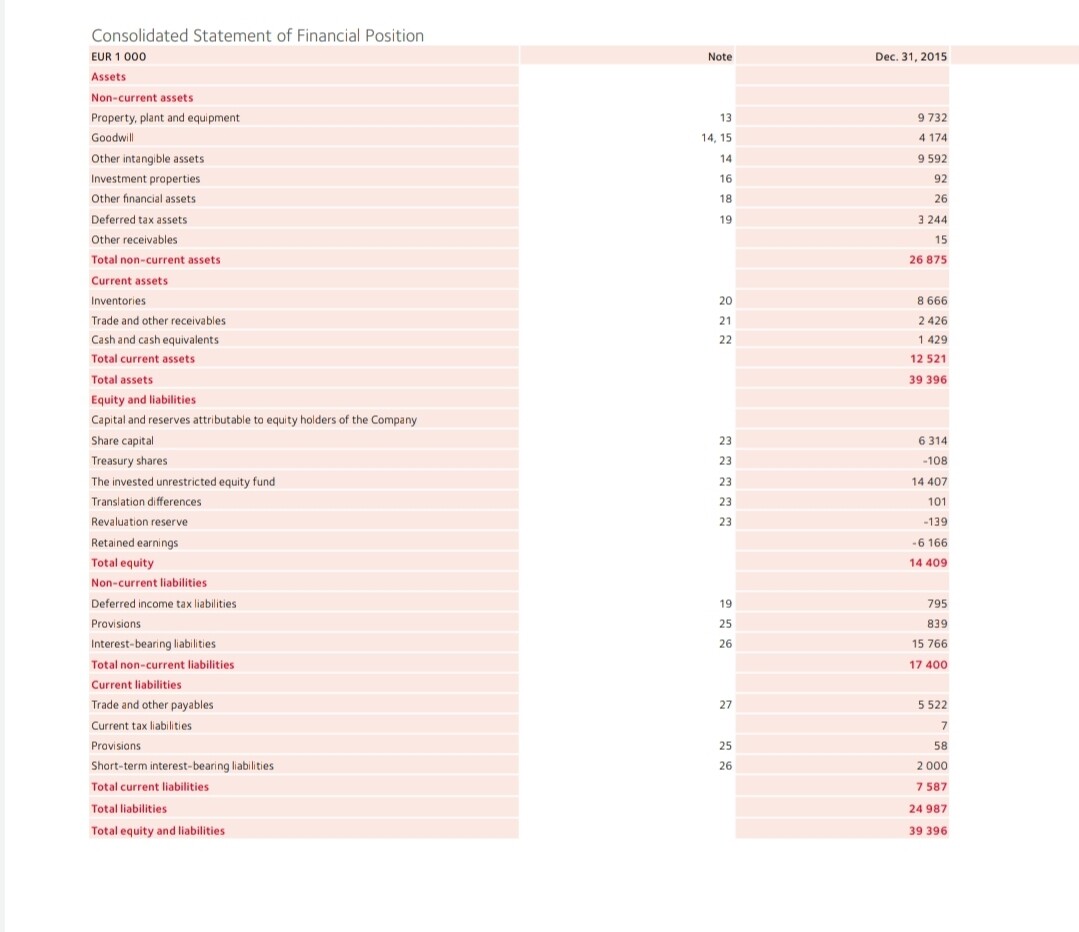

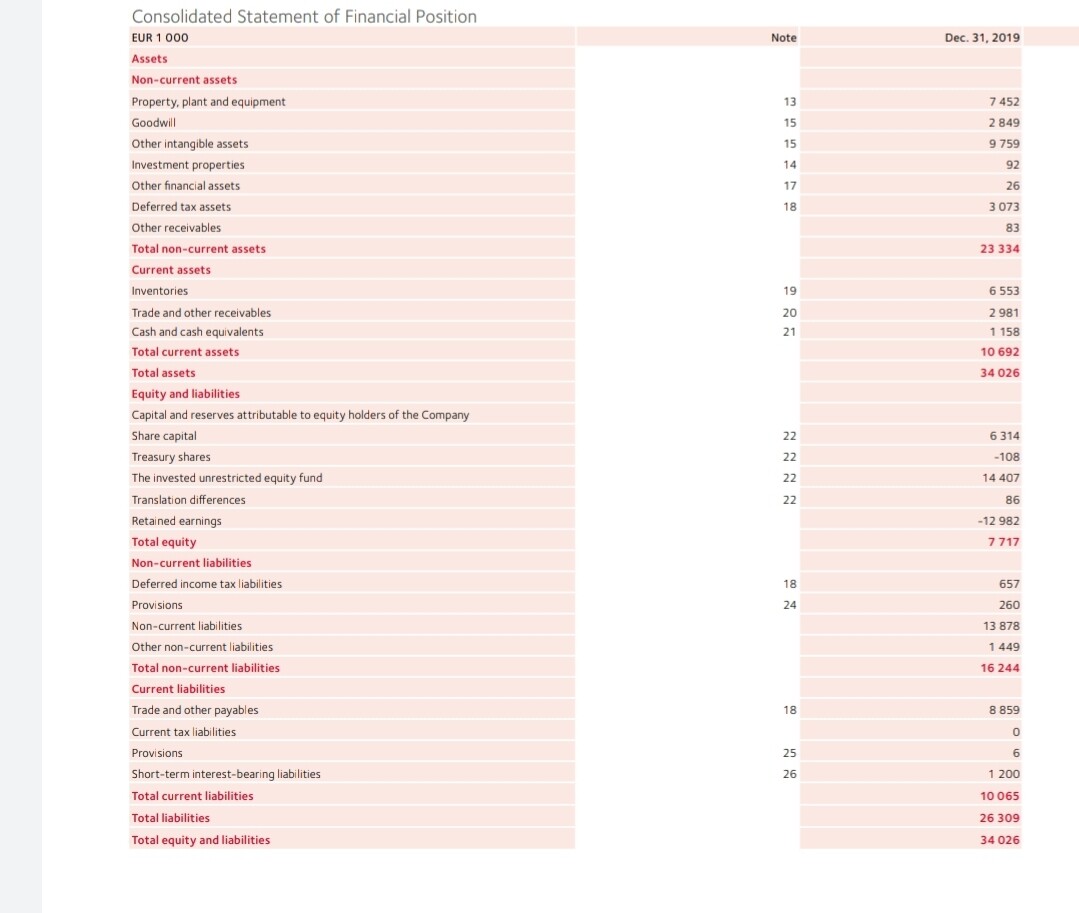

How does a company that makes a loss year after year reduce its debt so much? Or is the most important part just left out, i.e., the debt has indeed been reduced by 12 million, but at the same time, new debt of 15 million has been taken on, and now the debt is 3 million more? Now, it’s easy to get the impression that 5 years ago the debt was €27M and now it would be €15M.

The same Predak troll also lived on the Kauppalehti forum for a long time, under numerous different usernames. The delivery is very different from the starter of this thread, but I wouldn’t be surprised if the original troll soon finds his way here too (tomorrow this thread will probably be found quite high up with a Tulikivi Google search).

The business cash flow before investments has been positive for the last 5 years, ranging from 0.8 million to 2 million. Perhaps debt repayment has been slowed down this year, which is reflected in the income statement.

Vauhkonen’s comment on debt completely surprised me, at least. My impression was entirely different. I don’t know if I should believe it.

I put Tulikivi in the top 3 risers for next year, but I don’t dare invest my own money at this point.

A few points:

investments are still being reduced; continuous tightening and years of slow strangulation easily cause good people to leave for other jobs.

short-term debts/assets feel too risky, especially since inventory has probably not been written down for a long time (even though marketability could be questionable).

the coronavirus has brought one nostril to the surface, but is it enough to bring the company to new prosperity?

the talc deposit has been talked about for a long time; of course, the mining industry is slow, but what is its true realization value?

Pros/why I bother to read the interim report at all

the stoves and even the fireplaces are, in my opinion, good-looking.

exports account for half of the turnover; will it grow in the future?

stone as a raw material and interior design element is fascinating; it could have the potential for a great Finnish stock market story

Predak has trolled the image of Tulikivi for a large part of small investors, so it is partly hated in that sense.

I checked the debt amounts from the 2015 and 2019 annual reports: they seemed to have increased by a couple of million.

Edit: here are the figures for others to review, current liabilities = short-term liabilities and non-current liabilities = long-term liabilities:

2015:

1-12/2019 Net Gearing, % 200.1

1-09/2020 Net Gearing, % 189.5

The pace of net gearing reduction isn’t exactly breathtaking yet

At a quick glance, Tulikivi’s most interesting part is the talc mine, which is potentially more valuable than the rest of the company combined. Unfortunately, the core business has been quite dismal so far, and I would personally demand stronger evidence before daring to say it would even be worth the current debts.

However, that mine will start producing limestone (kalkkia) at the earliest in 2024, so it’s not worth leaning on too much

Yes, I listened to that stock market evening clip, and the CEO directly states that it’s good to know about the debt, which was about 27 million euros some five years ago and is now about 15 million euros… roughly at the 1:20:00 mark. wtf

I’d be interested to know how valuable a talc mine like that can be. With my limited knowledge, left over from Talvivaara and Sosi, I’d estimate around 30 million dollars. Even though I tried to use conservative values and roundings at every turn, it still feels quite optimistic…

Yeah, let’s see if it was a short trade since I bought it yesterday xD The reasoning was profitability as a backup to buy time for the mine issue to resolve within a couple of years. So, it’s artificial respiration until it’s resolved whether there’s jam or rotten cod in the jar…

Edit: I somewhat mirrored this as Benjamin Graham’s cigarette butt. Considering that the talc mine has not been valued on the balance sheet in any way, as it doesn’t have any bookable value yet.

It’s hard to say how much a million in EBIT warms when you have over twenty times that in debt and ten times that in short-term debt.

Not all liabilities are interest-bearing debt, of course, but there’s so much of it that it won’t even clear 5-6% interest with exceptional results. And who would give this at a lower rate?

Oh, but that’s “comparable operating profit,” so it might have been adjusted in some way. Oh well.

But at least my hat’s off, I didn’t expect even this much.

Yeah, that’s right, as I said, a cigarette butt that needs artificial respiration. And I didn’t expect anywhere near this much myself either. I thought it would hover somewhere between 0 profit and 400k (euro) for the next couple of years while loans are rearranged for longer payment terms into the distant future.

At the same time, however, there’s still the talc option to pay off the loan and thereby reduce loan servicing costs.

This is trash. Just gotta see if there’s any mayonnaise left on the Big Mac wrapper to lick off