the environmental permit will be submitted during Q2 (this is my interpretation as the CEO said the matter was more about weeks than months),

the company will start investing in the sauna business, where acquisitions are possible in the future.

I wouldn’t really rely on acquisitions, as there’s a lot to do and many opportunities regarding organic growth as well. It’s a good thing that the sauna business is seen as a growth target within the company.

If you want to see happy Easter faces, I recommend going to Nordic Talc’s LinkedIn pages, where you can find a post after a successful foaming experiment.

According to a press release, Tulikivi Oyj submitted the environmental and water permit application for the Suomussalmi talc reserves utilization project to the Regional State Administrative Agency of Northern Finland on May 9, 2025.

The permit application was submitted in accordance with the schedule previously announced by Heikki Vauhkonen, “rather in weeks than in months”.

The next news will likely be the reporting of studies on the utilization of the byproduct.

As I understand it, Harvia also had problems in Europe/Nordic countries, so this was probably quite expected on the sauna products side. Even in construction, there isn’t any real boom yet.

Electricity has also been cheap considering the season, at least in Finland.

Add to this the still increasing uncertainty of customs matters in Q2. Just what we needed.

Yes, Tulikivi has so much to gain in the sauna sector that its numbers must be better than Harvia’s, which has more to lose than to gain in market share.

From the interim report, one could conclude that the sauna segment performed relatively well, but there is a lot of room for improvement in sales.

Positive points included the order backlog growth of 200,000 euros from a year ago to 7.8 M€, and the order backlog growth from 2.8 M€ at the turn of the year to 4.3 M€. Based on these figures, the revenue dip is temporary.

The submission of the environmental permit application on schedule is crucial.

Perhaps a somewhat simplistic conclusion, or else the sales network must be scaled back, with significant reductions in every country.

Even though I haven’t been to business school, I doubt this is the way.

Thomas has prepared a recent company report on Tulikivi.

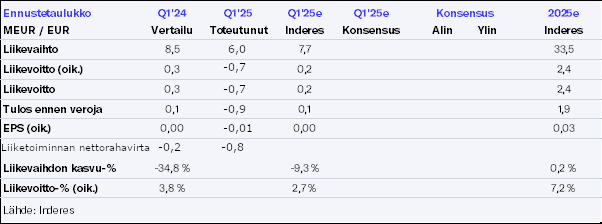

Tulikivi’s Q1 figures fell short of our estimates, but the continued growth in order flow balanced the overall picture of the report. The guidance for the current year leaves a significant amount to catch up on in the latter half of the year, although the gap will be closed with a significantly stronger order book than in the previous year. Our forecast changes remained small, as a result, we reiterate our target price of 0.42 euros and a sell recommendation.

If there’s an interview with the CEO, Jukka7 suggests that Heikki could be asked directly about this: How much/to what extent sales have been generated through new resellers, and how likely it is that sales through new resellers have not, in turn, reduced sales through the old sales network?

I simply don’t believe that Tulikivi’s products are so well-known abroad that buyers already know in advance that they are going to buy Tulikivi fireplaces and search online for the nearest point of sale. I believe that a significant portion of buyers make their decision in the store, and if there is no Tulikivi product available, the purchase decision will be directed towards a product from a completely different manufacturer.

There are significantly fewer points of sale for sauna heaters abroad than for fireplaces. One could even say that, regarding sauna heaters, points of sale are very few and far between.

We have initially started with semi-annual interviews, so it’s worth suggesting interview questions just before the Q2 report!

I don’t believe that new resellers would have come at the expense of previous ones. However, with resellers, it takes quite a long time until sales start rolling with a new brand (if they do), so new sales points only generate significant revenue with a delay. Distribution points are also not brothers among themselves, as the key figure simplifies them a bit too much, when a sales point is a sales point regardless of its size. The ramp-up of new resellers is also hampered by the weak fireplace market in both the Nordic countries and Germany.

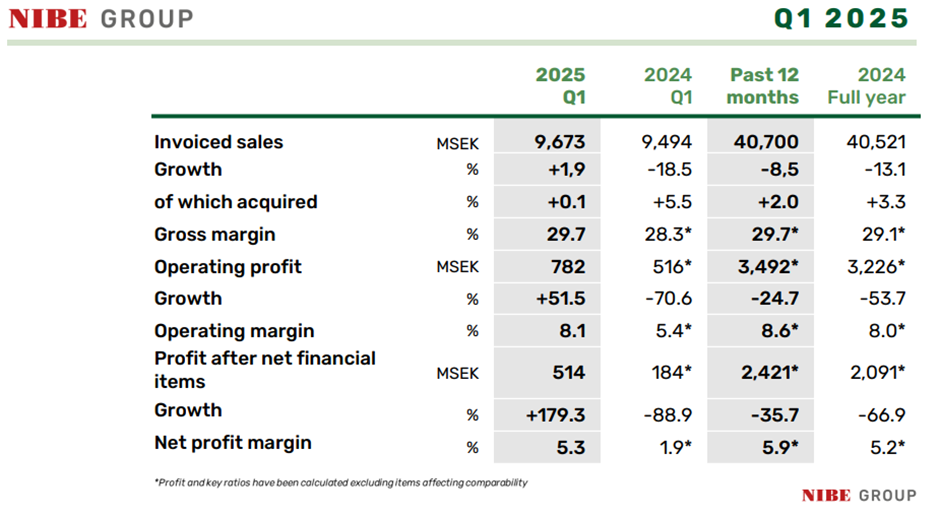

NIBE published its Q1 report yesterday, which already showed cautious signs of cyclical recovery. Revenue saw a cautious 2% growth, and operating profit was up 52%.

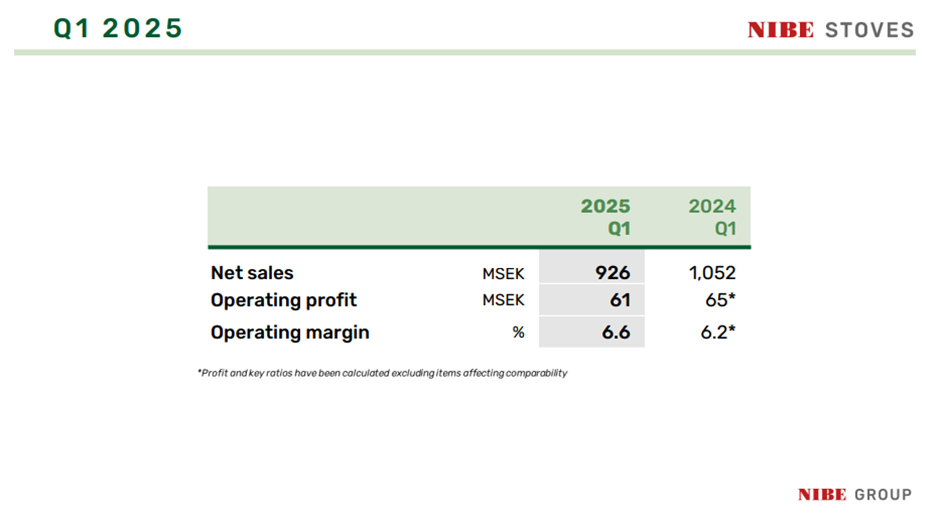

From Tulikivi’s perspective, a more relevant comparison than the group level, the Stoves segment, lagged behind the group’s development, with revenue down 12%, although relative profitability improved slightly.

NIBE also signaled, like Tulikivi, that the fireplace market is returning to more traditional seasonal fluctuations. According to the company, demand in Europe has weakened, but underlying demand in North America has developed positively. The company states that oversized inventory levels of fireplace distributors in Europe have been melted down, which could support the future margin development of the entire industry. Sweden, Norway, Denmark, and Germany are highlighted as particularly weak markets.

NIBE’s comments, in my view, reinforce the thesis that Tulikivi’s weakened performance is market-driven, as even a player like NIBE is facing difficulties. Unfortunately, based on NIBE’s comments, a sudden recovery is unlikely in Tulikivi’s key markets, so to achieve growth, one must swim against the market current.

Jotul just published its Q1 figures, which, along with NIBE’s previously mentioned comments, support the thesis that the fireplace market has bottomed out. Revenue saw slight growth, but the result was still deeply in the red despite the favorable development.

Based on management’s comments, there are cautious signs of demand recovery, and high inventory levels of fireplaces are no longer an issue for new orders. New orders grew by 5% in Q1. The company’s factory deliveries grew by 38%, although this was supported not only by demand growth but also by increasing inventory levels at the retailer level. In addition, the company secured its financing early in the year, which supports business continuity.

Here are Thomas’s preliminary comments as Tulikivi publishes its Q2 results on Friday.

The company entered the current year from a more challenging position than in previous years, with a reduced order book, but the outlook is balanced by new sales turning to growth. After a nearly two-year period of declining revenue, we expect Tulikivi to have turned its revenue back to growth. The guidance, which points to growing revenue and comparable operating profit, requires strengthening demand throughout the year, as a result of which the order flow during the review period plays a particularly interesting role.

Good point @Jopinaattori!

An interview is coming up regarding Q2, so you can send your questions here! Naturally, I cannot promise that all questions will be included in the interview.

The company reiterated its guidance, which means that sales will grow in the latter half of the year compared to H1 and Q2, meaning that Q3 and Q4 revenue must be over €9.35M. Since growth is predicted, revenue must clearly be over €9.35M per quarter. As we are already in mid-August, the company evidently has a good understanding that sales have continued to develop positively.

The talc project appears to be progressing as planned

Next, we await Heikki’s interview, which will hopefully provide further insight into the company’s operations.