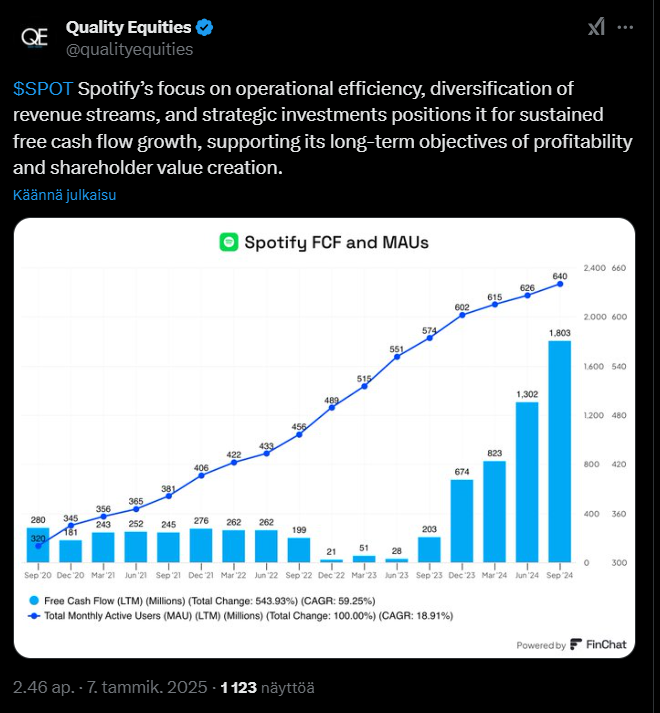

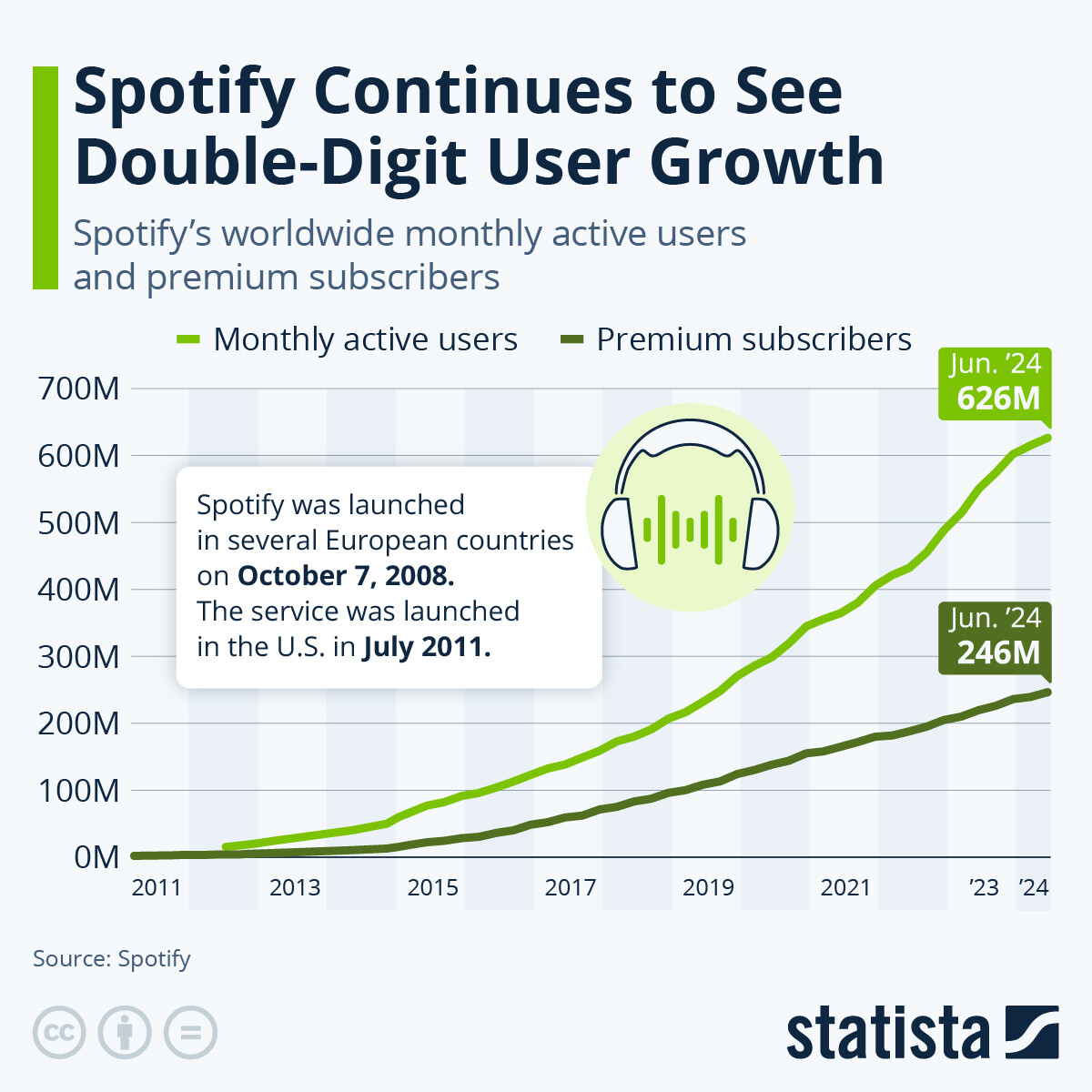

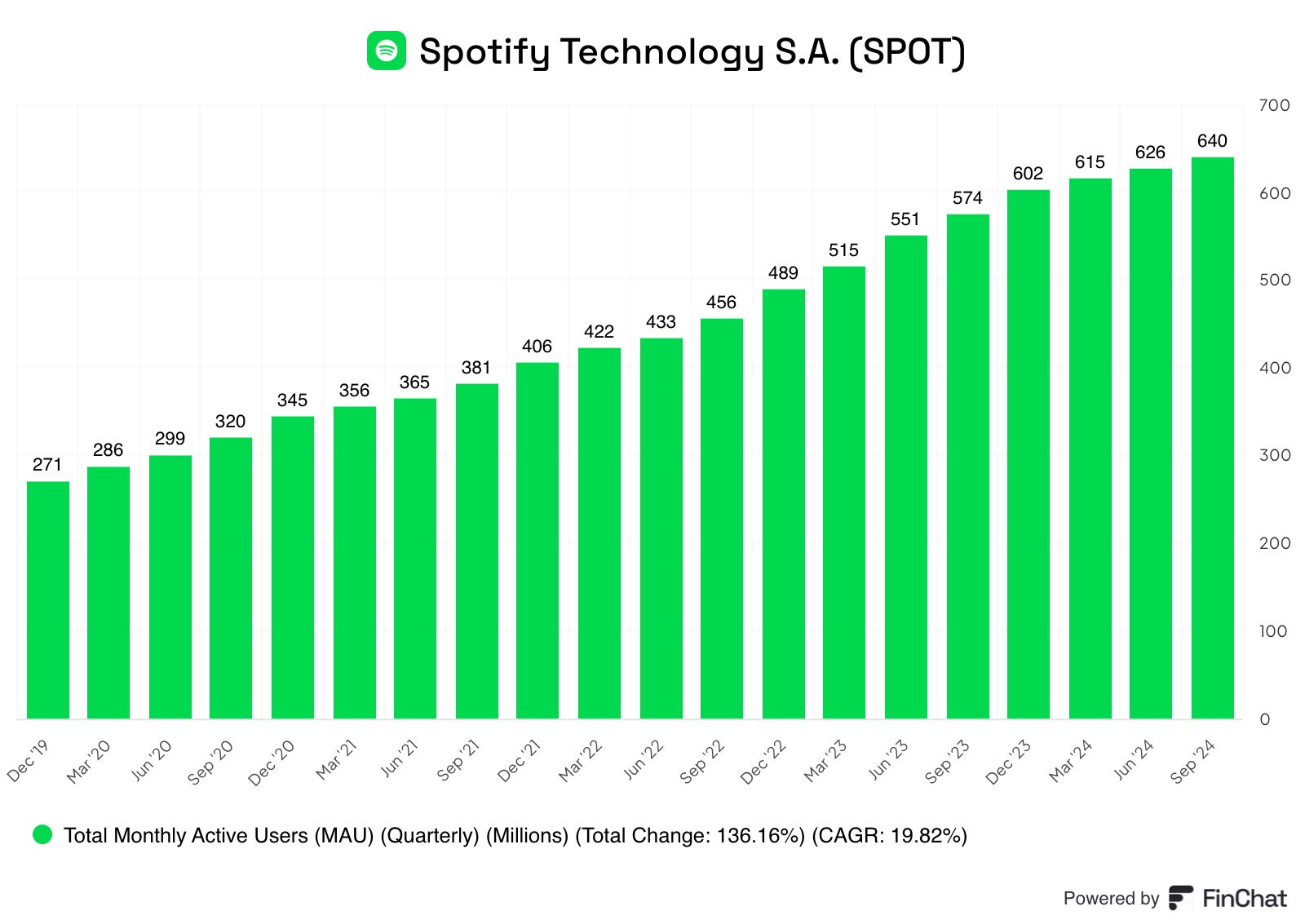

Spotify is a Swedish audio streaming service and media service provider, founded by Daniel Ek and Martin Lorentzon in 2006. It is one of the largest music streaming service providers in the world, with over 626 million monthly active users, of whom 246 million are paying subscribers (2024/6).

What kind of service

Spotify offers digital, copyright-protected audio content, and most users can find almost all the music they could wish for there. Spotify is available for free with ads, but additional features such as offline listening and ad-free listening are only available through a paid subscription. Users can search for music by artist, album, or genre, and create, edit, and share playlists.

2024: 100 million songs, 6 million podcast episodes, 350,000 audiobooks

Global availability

Spotify is available in most of Europe, as well as in Africa, the Americas, Asia, and Oceania, across a total of 184 markets. The majority of users and subscribers are from the United States and Europe, which together account for approximately 53% of users and 67% of revenue. Spotify is not present in mainland China, where the market is dominated by QQ Music. The service is available on most devices.

Royalty payments and such

Spotify pays royalties based on the number of artist streams relative to total listens. The company distributes approximately 70% of its total revenue to rights holders, most often record labels, who then pay artists based on individual agreements. While some musicians have criticized Spotify’s royalty structure and its impact on album sales, others appreciate the service as a legitimate alternative to piracy and for compensating artists for each listen.

Generally

Spotify is a huge player in the world of music and podcast streaming. The company has succeeded in continuous growth and is able to offer a wide range of content globally.

What an investor considers

Spotify is very popular, has a huge user base, and is still growing with plenty of additional potential to acquire new customers. According to many, the company has boldly invested significant sums in technology, which, especially in the long run, is expected to offer competitive advantages and deepen its moat.

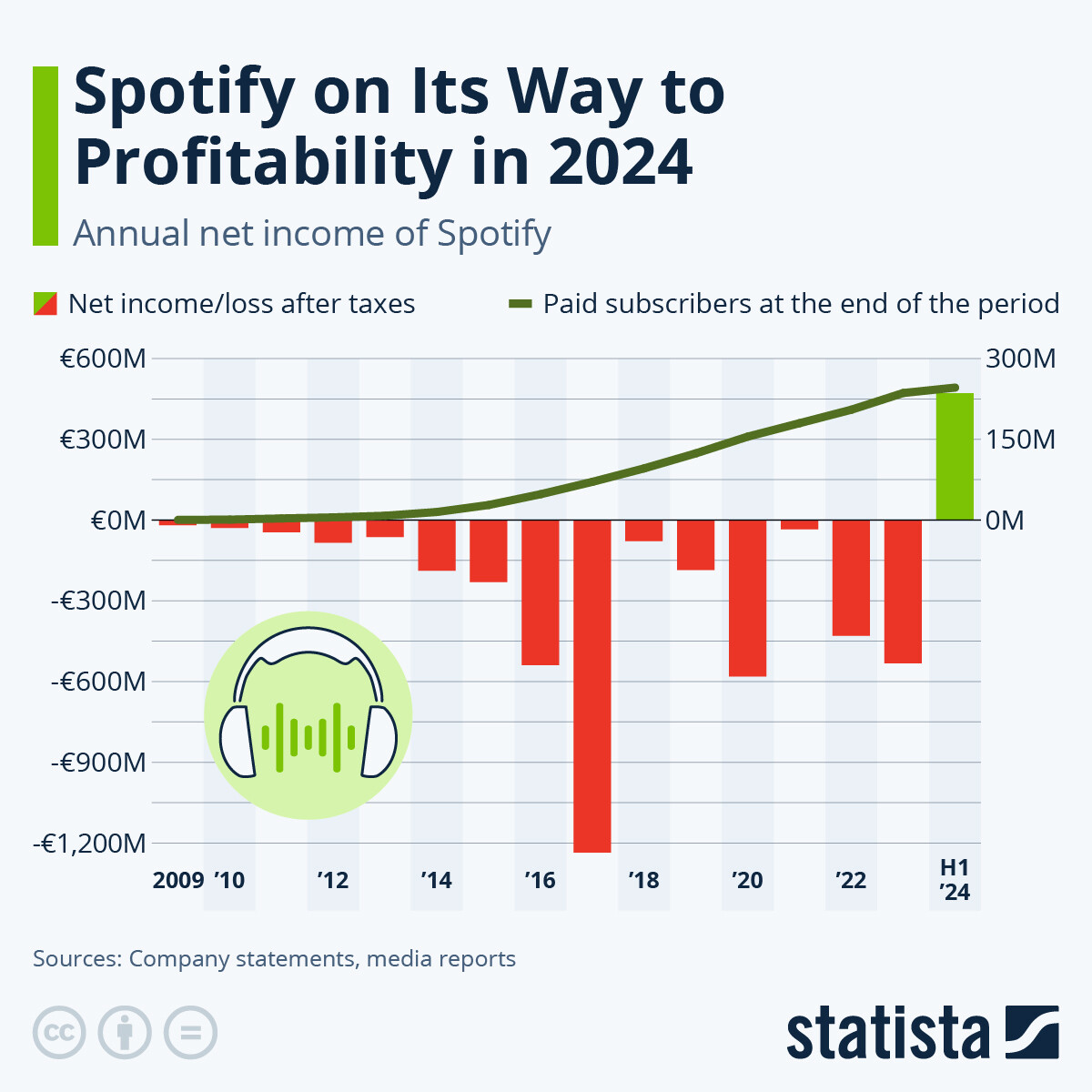

There are many competitors in the market, and some of them have the money to invest and develop if they get enthusiastic. Making a profit has not always been easy for Spotify.

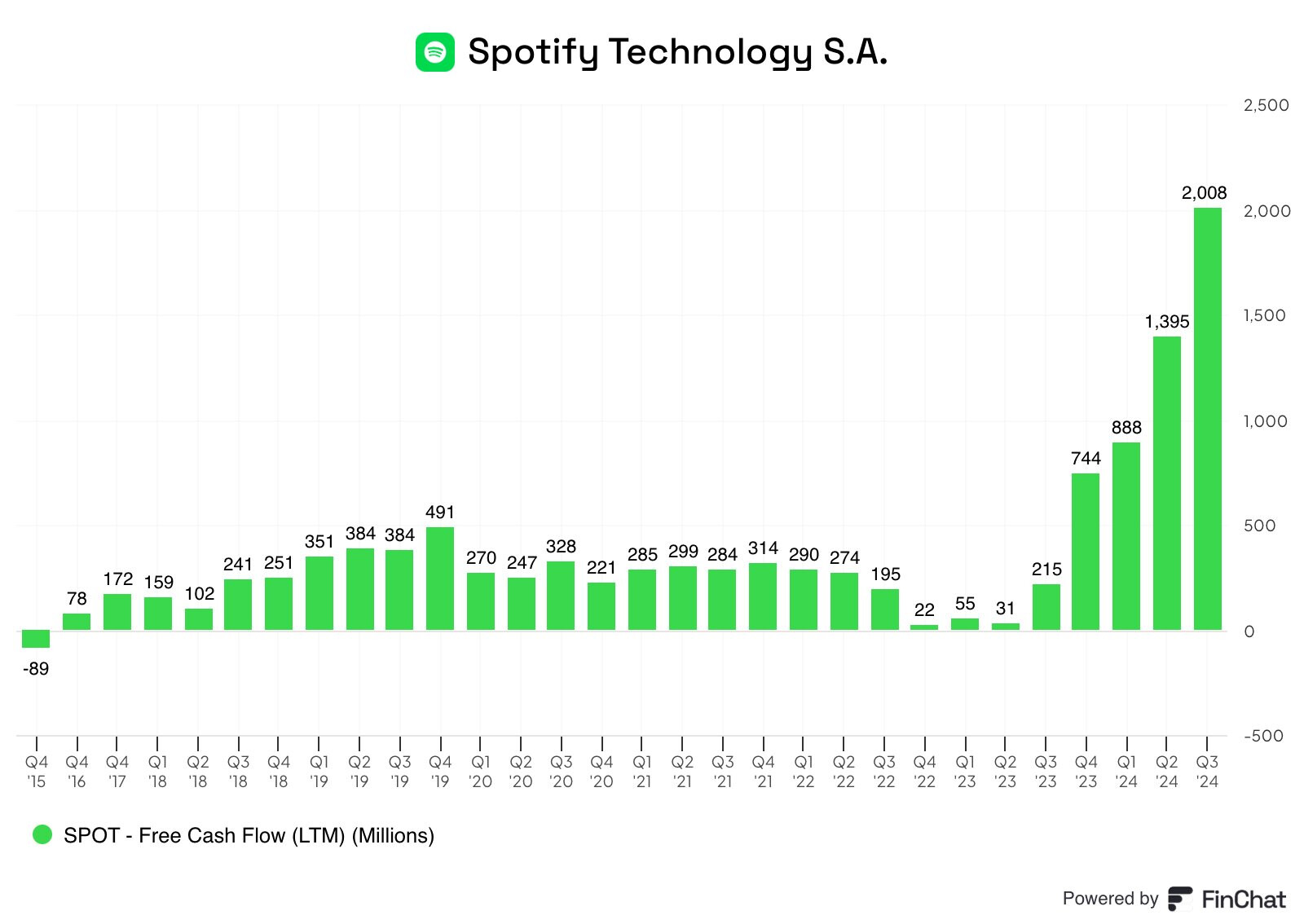

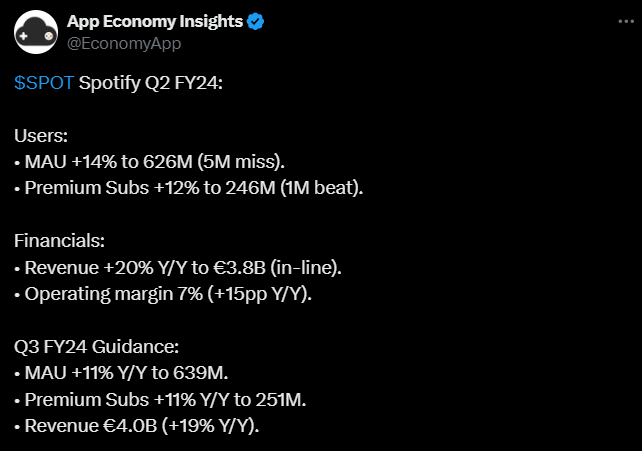

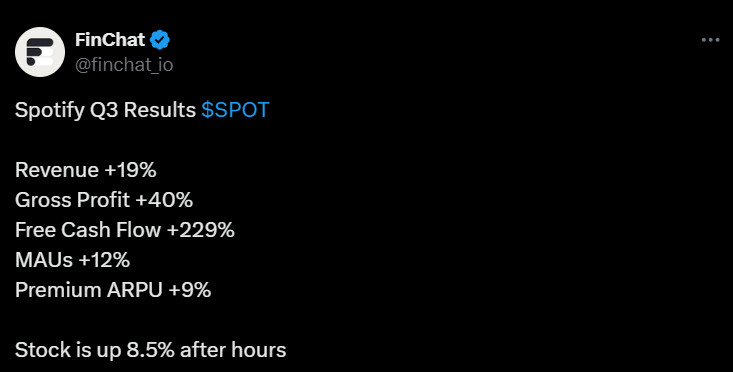

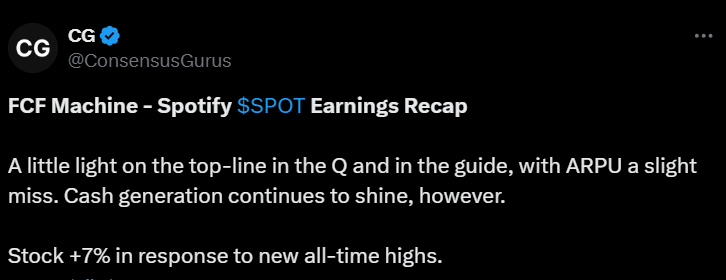

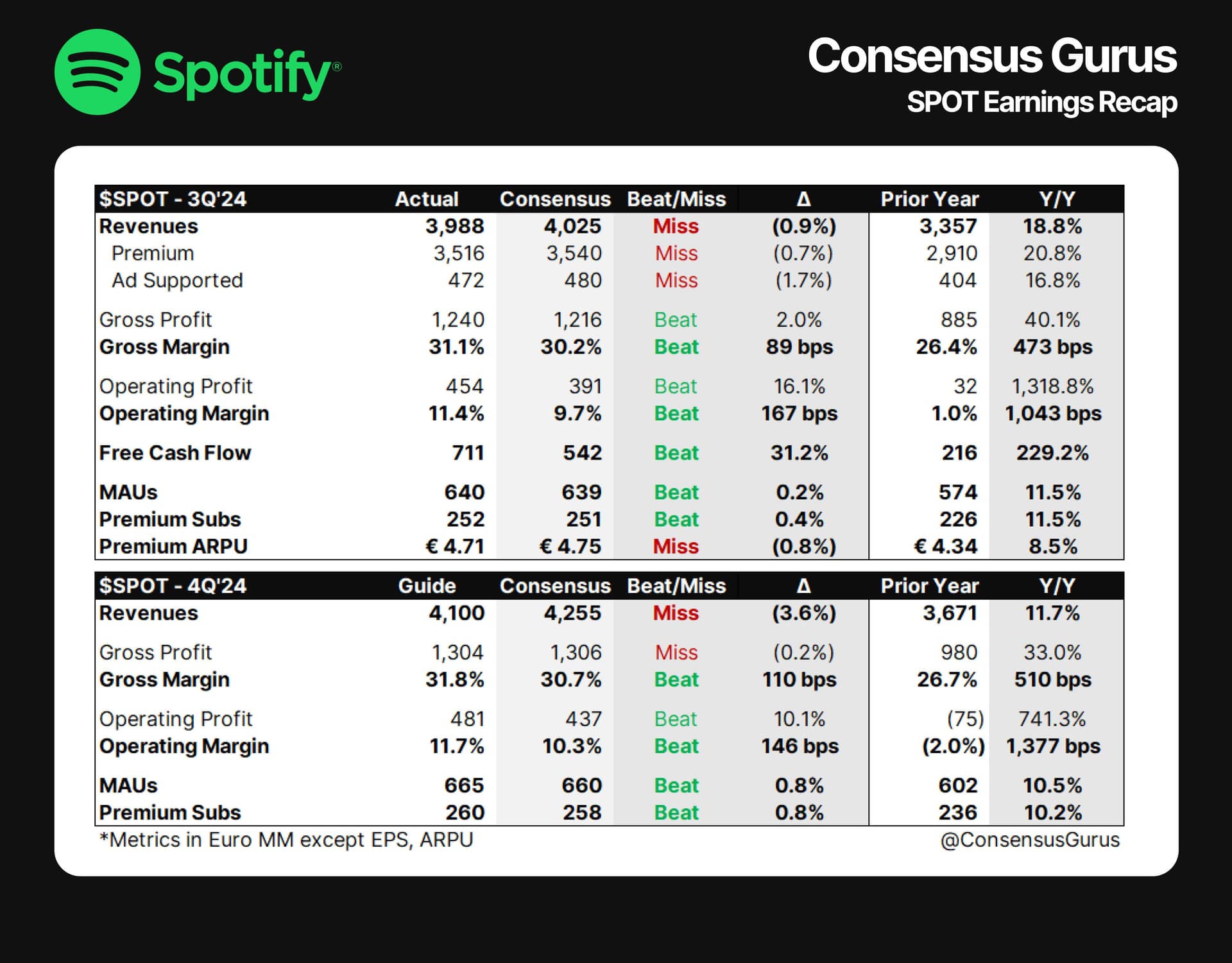

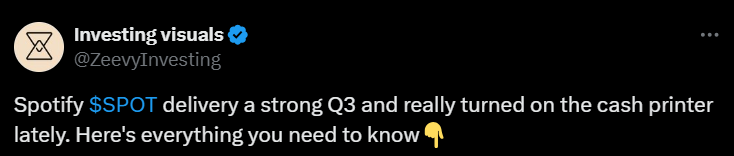

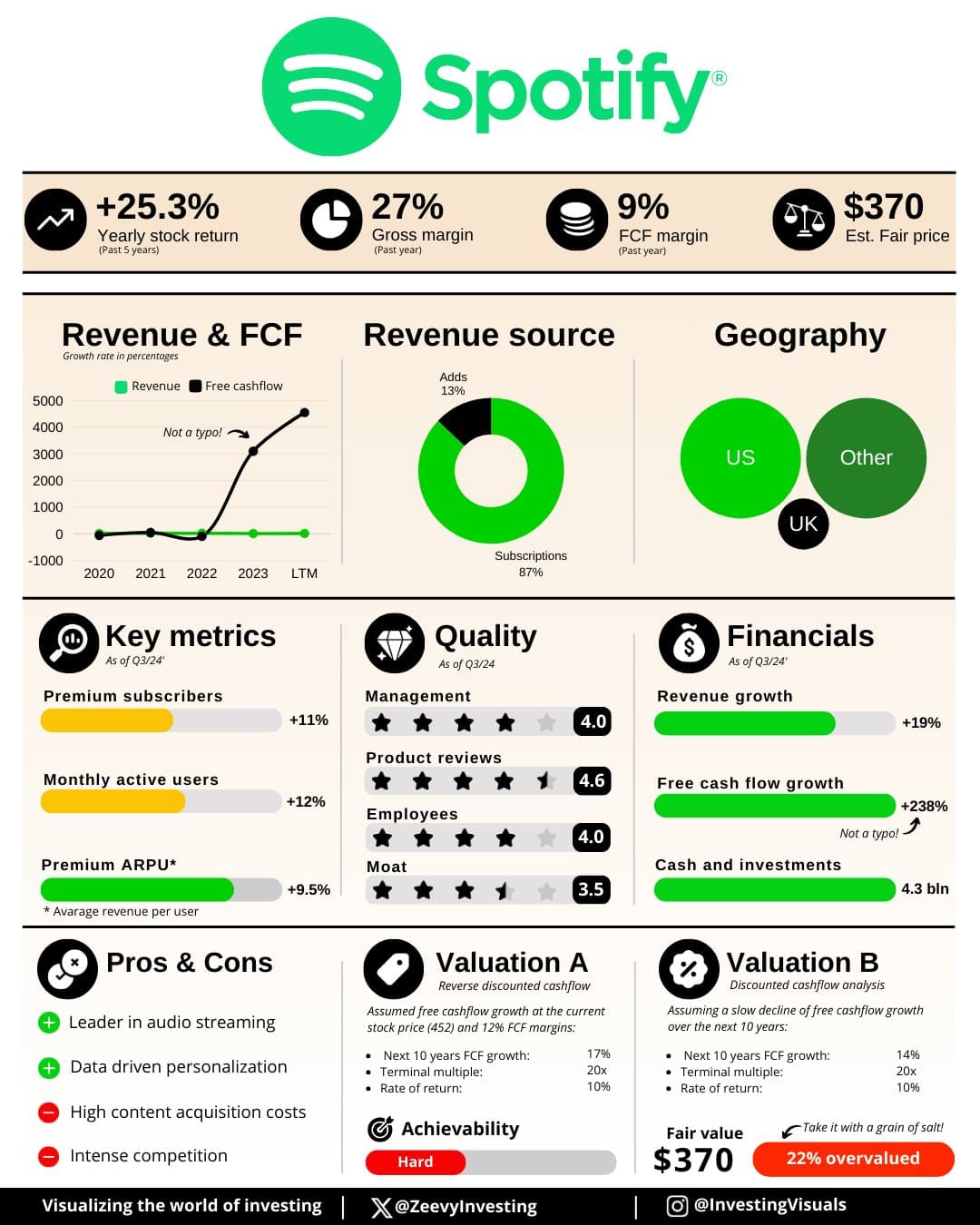

and about that Q2, which was strong:

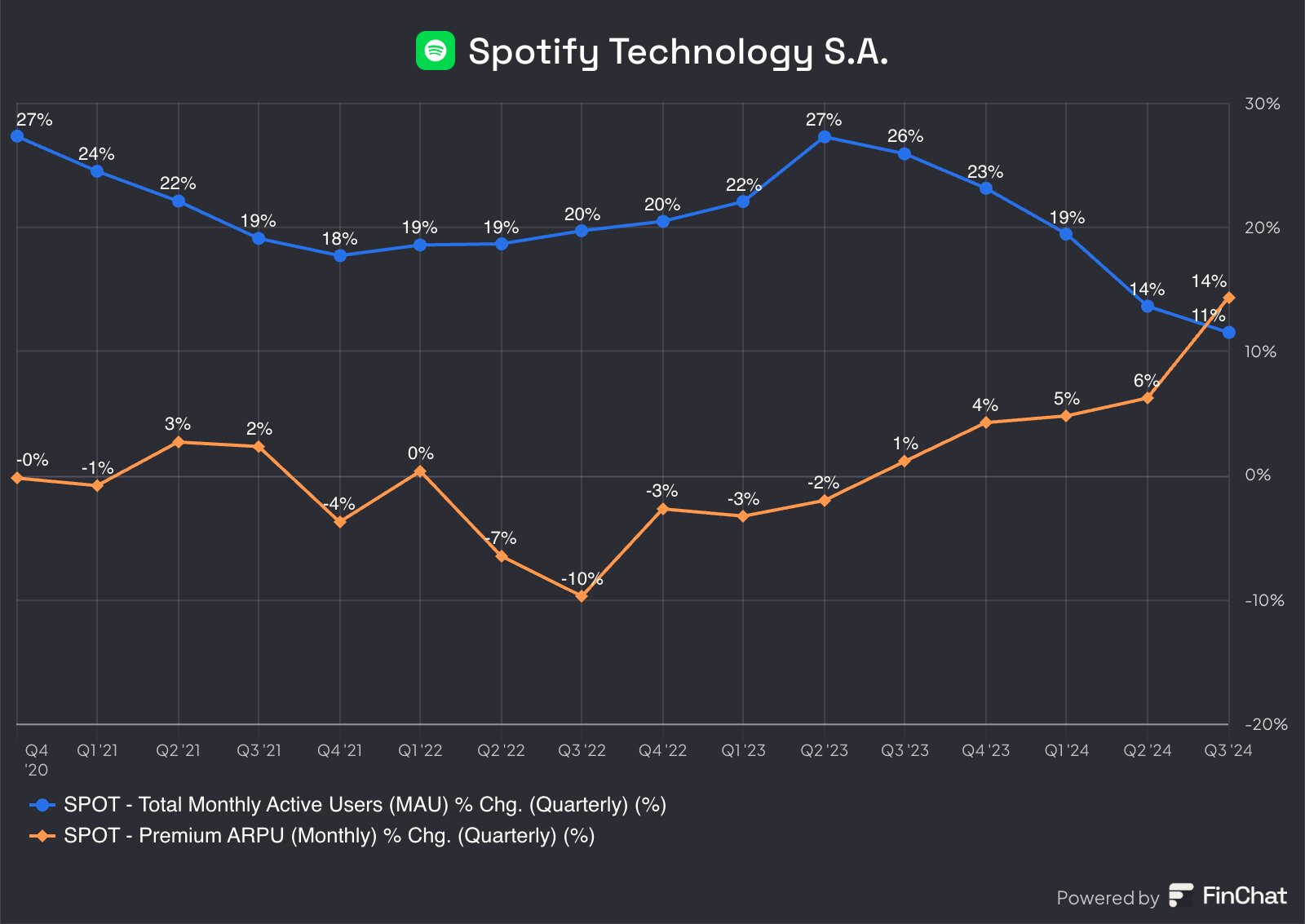

Spotify has exceeded analysts’ expectations for second-quarter subscriber numbers. The company has successfully grown its paying users by 12% year-over-year and has thus surpassed market forecasts.

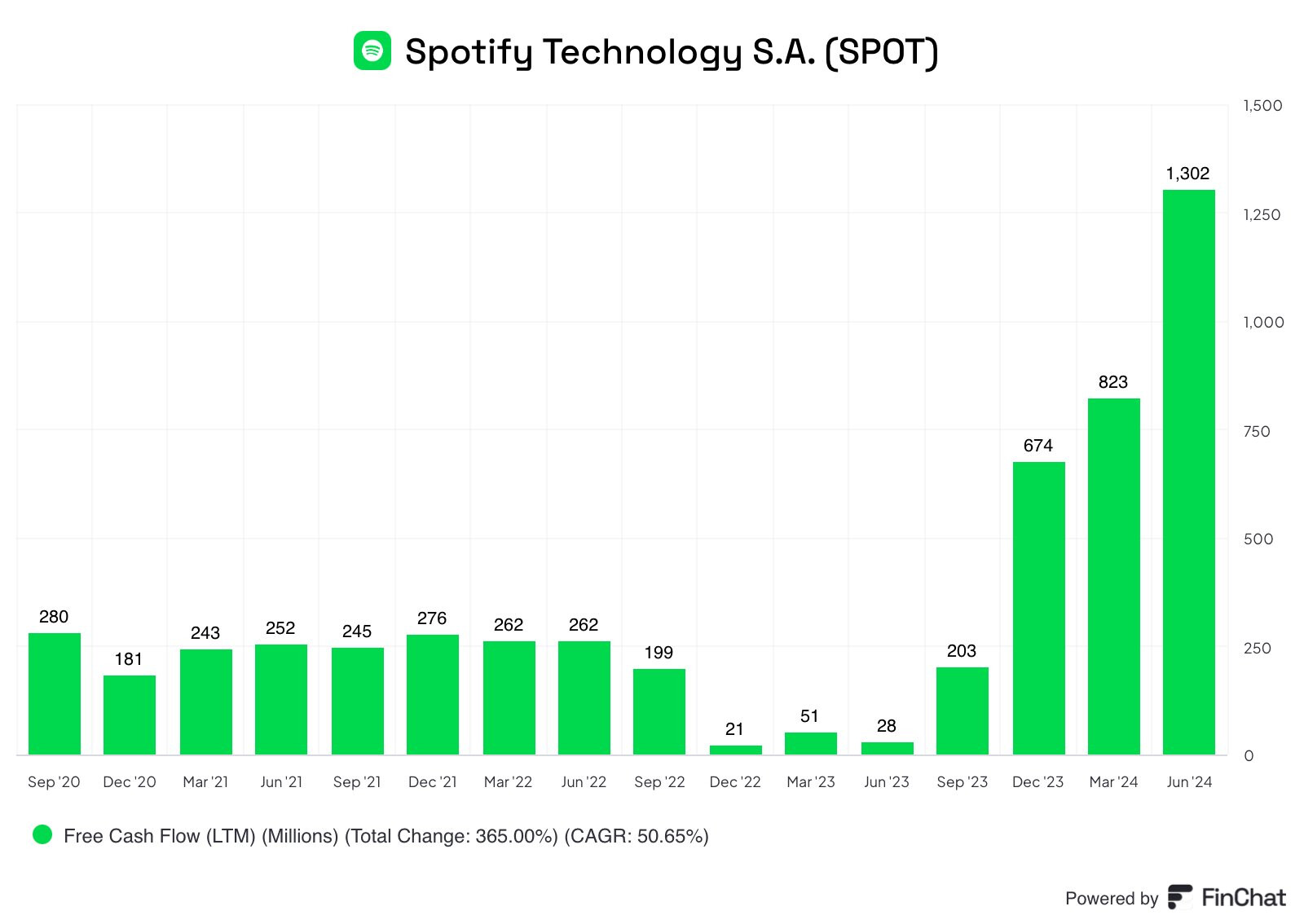

The successes in the figures are due, among other things, to how Spotify has effectively reduced costs over the past year to improve profitability. Additionally, the company has raised monthly fees for the second time this year.

https://x.com/EconomyApp/status/1815750580457099458

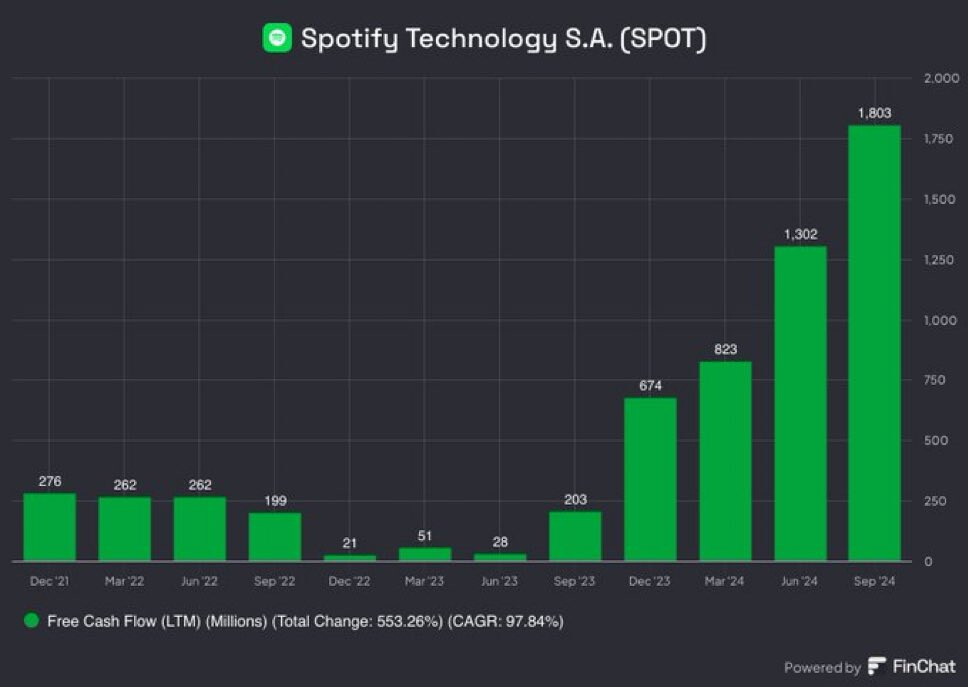

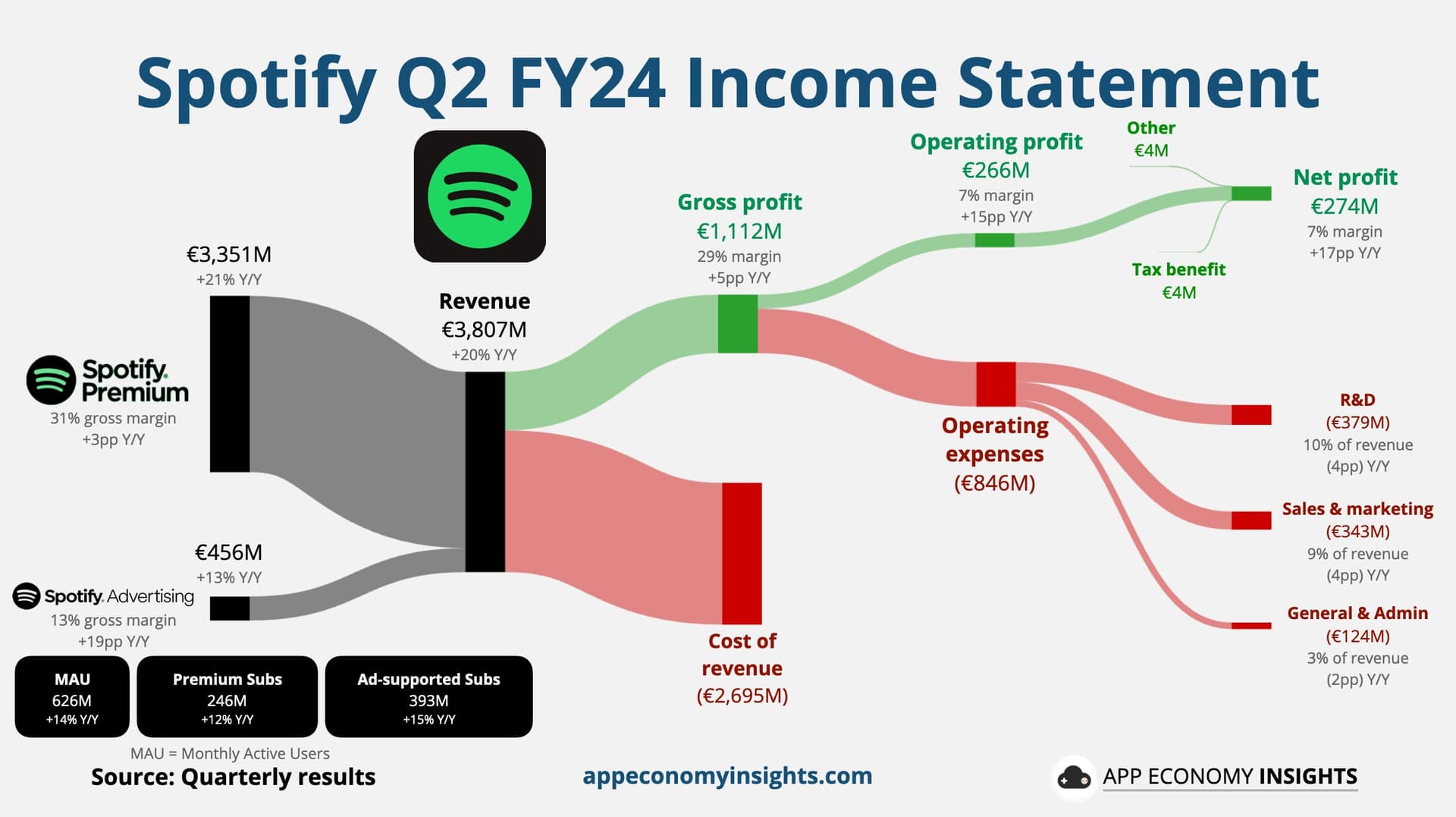

Then a few more figures.

And here’s much more, Spotify’s Q2 materials.

| inderesPodi 210")