Based on a tip from another investor, I’ve been looking at Eniro as a potential turnaround company emerging from a crisis. There are interesting elements of continuity and scalability in the business model. Unfortunately, Redeye’s coverage just ended, but I’ve been rubbing my eyes looking at these valuation multiples—I should start digging deeper:

Well, I guess I have to put my favorite on the table: Irisity. There has been plenty of turbulence along the way, but I still believe things will start to take off.

In short, the company makes AI-powered surveillance camera software—meaning the cameras monitor and the AI triggers an alarm if anything unusual happens. I see two growing trends here—security and AI—so go ahead and check it out!

Storytel got a good boost from the COVID-19 stay-at-home trend, and the stock price rose very high along with the rest of the market euphoria. Since then, the bubble burst, and for over a year, the valuation has been crawling at more moderate levels. The previous ambitious growth strategy has, under new management, shifted to emphasizing profitable growth, and the results in that regard have been convincing. The share price has indeed started to recover with this turnaround, but it is still well below even the original 2018 listing price. The price curve from the COVID years follows the First North Stockholm curve of the opening message, but perhaps on an even larger scale

My own thought has been to invest in this until at least the 2030s and see how far the audiobook market develops. Audiobook penetration outside the Nordic countries is still surprisingly low, and I see potential for significant growth here as those markets mature. Storytel’s strategy has long relied on local languages. Moats are being built by acquiring publishers and creating original content. Large players like Amazon’s Audible and newcomer Spotify are formidable competitors, but their focus is on English-language content, at least for now. Consequently, an acquisition is also a possible scenario. Private equity firm EQT is involved with a large stake, and as an active owner, they can influence various arrangements. There are several smaller audiobook companies in the Nordics, whose consolidation we will quite likely see.

Good opening. I’ve been keeping an eye on a turnaround in this sector myself. Genovis, Physitrack, and Calliditas are in my own portfolio. There are already threads for the first two here, so no more on those.

Calliditas is very interesting for two reasons:

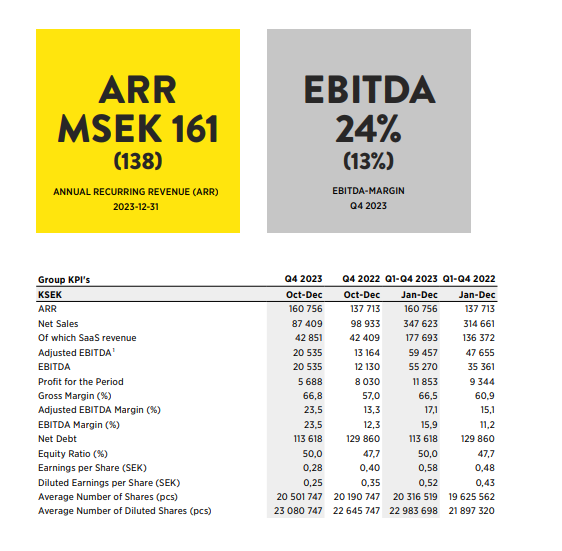

Q4 report tomorrow

the business

Develops drugs for rare diseases. A drug developed for kidney problems just received full approval in the US and China. Sales have started well. New drugs are already far along in the pipeline. Earnings are clearly turning positive, the CEO has a large stake…

From the office, at least @Verneri_Pulkkinen owns this firm. If I recall correctly, Mikael has also had these types of wholesalers in his portfolio before (Yleiselektroniikka?).

There are some mentions in the Foreign serial acquirers thread, although the discussion focuses heavily on quarterly reports. In my opinion, it’s still going “under the radar”. 525 retail shareholders.

Interesting thread, most of my portfolio consists of Swedish (at least former) small-caps

Swedencare: A company manufacturing supplements and other health-related products for pets. The German company Symrise will eventually buy this out; they already own ~40%. In my opinion, very competent management.

Genovis: Enzymes etc. for biopharma development. Redeye has good material on this, and there is a dedicated thread on the forum as well. Significant upside scenarios and a potential acquisition target.

Plejd: Smart home components, started with lighting control and is gradually expanding its portfolio. Excellent product, I use it for lights in my own home as well. Electricians like to install them because they are very reliable and easy. In my experience, Shelly, for example, isn’t even close in terms of reliability.

Humble Group: Sustainable FMCG, owns brands well-known in Finland such as Jalotofu and Humble’s bamboo toothbrushes. A total of about 50 companies in the sector under ownership. An interesting growth story and transformation from a sweetener manufacturer into a consumer goods company. I consider it a very potential acquisition target for someone like Orkla. The only one on my list that I have added to within the last year. Alta Fox’s report on Humble https://static1.squarespace.com/static/5aaacb57506fbe4636414126/t/651336f09fd2b91b8a91467f/1695758065852/Alta+Fox+HUMBLE+SS+Presentation+Sept+2023.pdf

USWE: In my opinion, the best running/MTB etc. hydration packs/vests in the industry. No bouncing, no swaying. Some challenges in the business after the Covid madness, but I still believe in the company.

Saxlund Group: various kinds of greentech, inflation hit profitability hard and the tail ends of projects are still showing. It should turn around once EUR/SEK returns to normal and the old projects are cleared Saxlund - Turnaround company from Sweden

My portfolio’s largest holding is Intellego Technologies, which released its Q4 2023 results a few days ago. It is one of the fastest-growing companies on the Stockholm Stock Exchange and is profitable. Cash flow was poor due to long payment terms for customers, stemming from new products/accounts. Cash flow is expected to improve in H1 2024.

Revenue is projected to grow from 180 mSEK to 300 mSEK this year, and EBIT from 80 mSEK to 110 mSEK.

ROE is 45% and the profit margin is 32%. There are many new customer accounts. Going forward, the sales performance of new products will be crucial.

Question for investors who have experience with Swedish stocks: How reliable are Swedish corporate leaders in their statements?

If at the bad extreme we have Canadian CEOs, who deceive as much as they can, and at the good extreme we have relatively reliable Finnish CEOs, where do the Swedes fall? Extra points if you can describe the situation for managers of Swedish small-cap companies. That is what the thread’s topic relates to most closely.

My motive is to avoid stepping on landmines during “overseas trips in the stock market,” and thus I’m trying to learn things in advance.

As thanks to those who answer, good vibes and a warm handshake!

The Swedes are closer to the American style. They are primarily the face of the company and promoters, so it’s worth taking their comments with a grain of salt, especially with small-cap companies. You can then reassess the situation if past talk materializes into numbers in the quarterly reports.

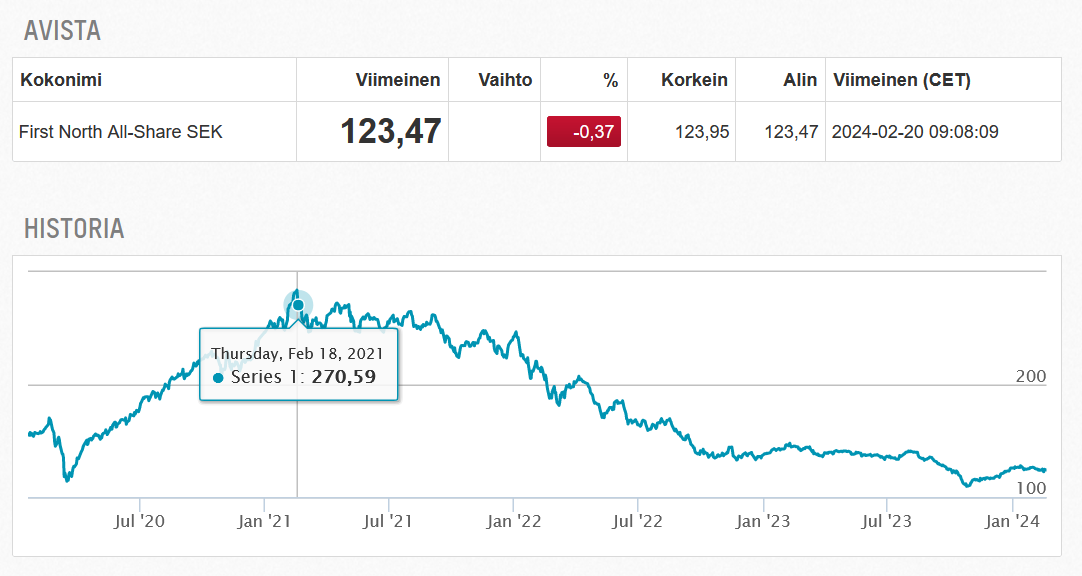

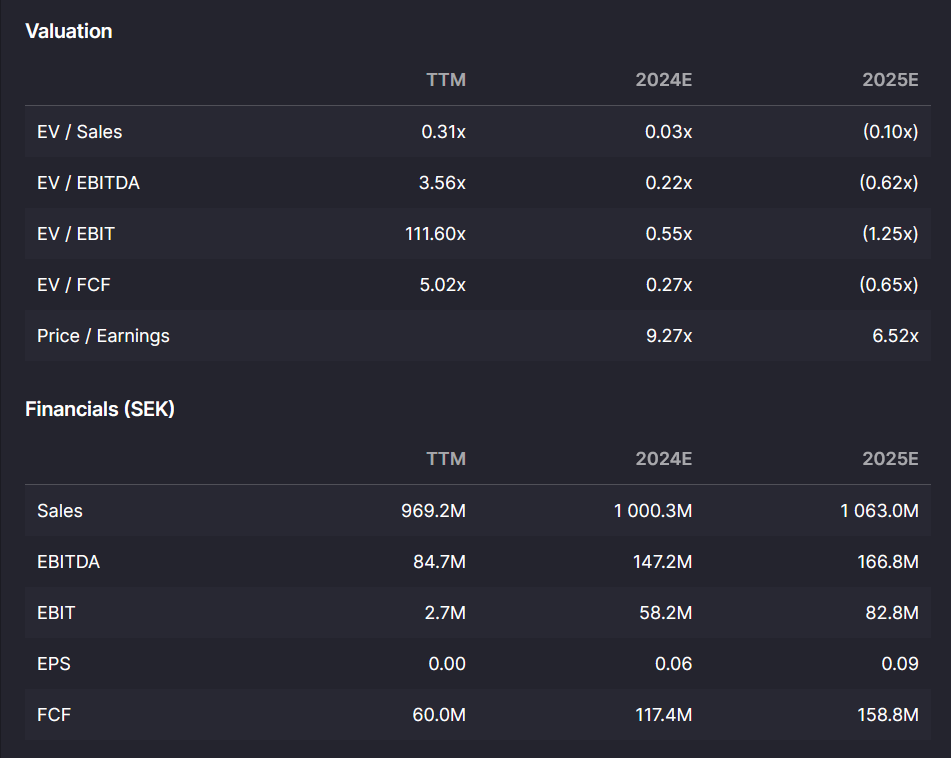

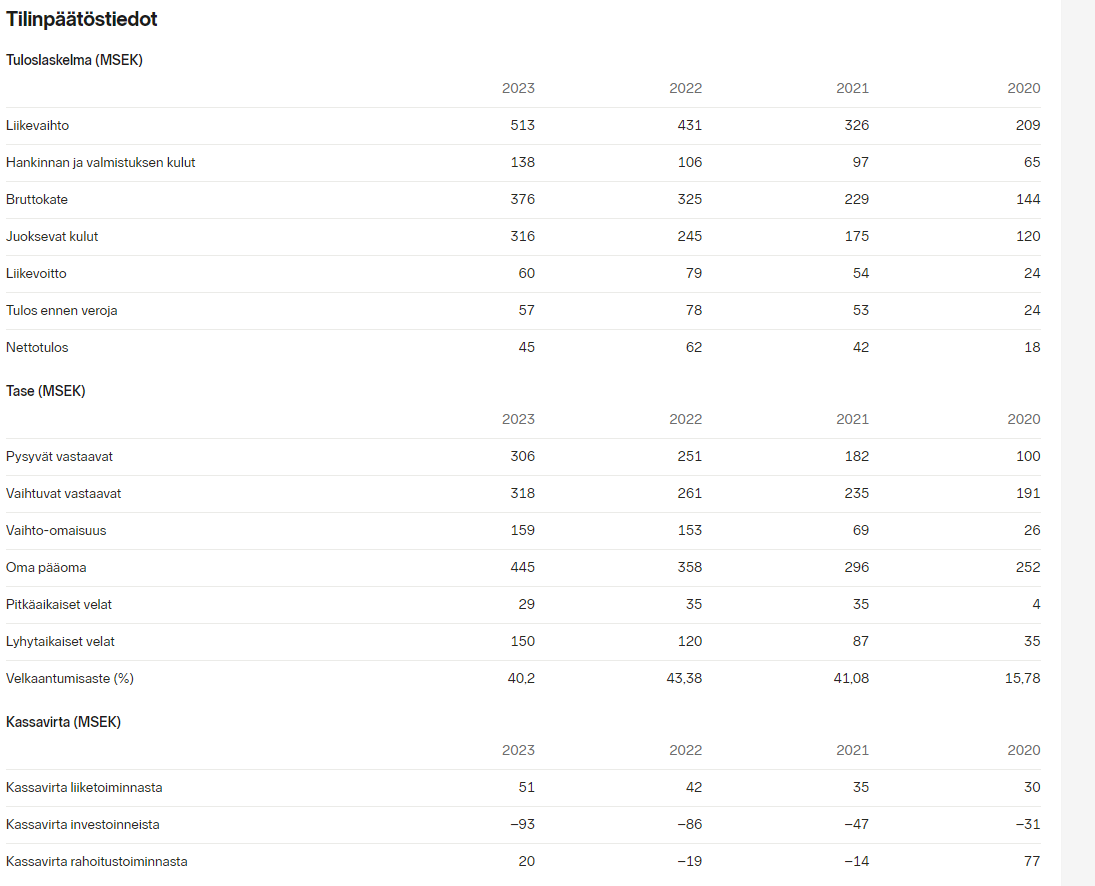

I had to start somewhere to kick off my Stockholm exploration game. I bought a small opening position in Eniro. This was mainly an entry to force myself to get to know the company. Before anyone follows me, a few warnings:

I haven’t done a proper analysis of my own, just a superficial review of the figures and the latest interim report (the balance sheet should be examined more closely before the multiples can be trusted) The idea for the purchase came from a discussion group (pretty smart people, though) The company has a terrible track record spanning nearly two decades, and there are likely a few disappointed owners on board (the share cost 350,000.00 SEK in 2006 and is now 0.56 SEK ) There are some ownership disputes in its history, with a related court case still pending Verneri mentioned at the office that the company is investing in AI, referring to news shared by a Shareville user

Why I bought anyway:

Valuation multiples are mind-blowingly low (even if you take a small margin of safety on Redeye’s 0.55x EV/EBIT forecast )

The business model is interesting, recurring billing and potential for quite good profitability (cf. Fonecta in Finland EBITDA 23 %)

At a quick glance, no signs of a company in crisis, the balance sheet is fine, and it’s generating cash flow

.. but based on this, I’m starting to look into this company; if others have views on Eniro, please do share At the same time, I’m adding other companies you’ve tipped (and of course the Swedish ones coming under Inderes analysis) to my Inderes account watchlist.

My first thought was that they are operating in a dying industry (comparable to phone books). Operations have been turned profitable, but where is the growth? The share price suggests that the market is mostly expecting cash flows to dry up and the business to shut down. Is AI a silver bullet? If they have some data assets besides phone and address information, then some business could be generated from there, maybe.

How about Investor AB? It’s churning out quite good results and you get many top Swedish companies at the same time?

I’ve been slowly poking around the Stockholm Stock Exchange lately. Mostly for learning purposes – and who knows, maybe I’ll find a hidden gem to pick for my portfolio.

I didn’t start with any screening; instead, I’ve been going through everything alphabetically on a surface level. Of course, I try not to waste too much time, so I don’t spend long reading about companies where I already know my competence wouldn’t be enough to ever make an investment decision. This means loss-making small drug developers and such.

I’ve gone through over a hundred names and I’m only at the B’s (started from A)! So there’s plenty of wading left to do…

I’ve written a few-sentence characterization for each company at this stage, color-coding the most interesting ones, those requiring further research, etc.

Here are a few leads to throw out there:

ADDvise: a health tech serial acquirer/consolidator (cf. Addlife, Thermo Fisher). EV/EBIT ~10x TTM and about 8x 2024 (RedEye’s forecasts). Market cap in euros is under 200 million, with the US being the most important market. An attractive sector as such, and the business model has huge potential at its best, but after listening to a couple of earnings calls, I’m not quite sure yet. Is this “platform” now enough for management to start financing operations through internal cash flow? So far, share issues have been used for expansion. It’s a bit off-putting if the dilution of current owners continues at these valuations.

Balco Group: a balcony builder/renovator. Quite a niche sector, which the company has also been consolidating. In January, they acquired the Finnish Riikku Group, which is a fairly big mouthful (approx. €40m in revenue compared to just over €100m for Balco Group in 2023). The valuation could be quite interesting, but I’ll leave guessing the normalized earnings level to those interested. This also gives exposure to the construction sector, if you’re into masochism.

Betsson: there’s already a thread on the forum for this, and it certainly can’t be called a small-cap company as per this thread’s title. I’ll highlight it anyway because the valuation reeks of disgust and fear, considering the company’s track record and quality as measured by numbers. The gambling sector doesn’t seem to be in high favor right now, and the regulation bogeyman is lurking around every corner.

A couple of months ago, a company called Opter Ab showed up on my screener.

A small Swedish SaaS company that provides solutions for Nordic transport companies. Listed in 2021, it has grown commendably and succeeded in international expansion. Currently, growth is being sought especially in Finland, but new market entries are likely on the way. Management is the largest owner.

This looks interesting and I’m putting it under the microscope! I need to investigate what kind of interface solutions they’ve implemented. If it’s primarily EDIFACT or other legacy traffic without sensible API solutions, that’s a red flag. There are many such challenges in this industry.