The tweet asks – will Spotify become a money printer? Or will it be hacked empty before then? ![]()

https://x.com/QualityInvest5/status/2002815998400028772

The tweet asks – will Spotify become a money printer? Or will it be hacked empty before then? ![]()

https://x.com/QualityInvest5/status/2002815998400028772

Spotify is now raising the price of Premium in Estonia, Latvia, and the United States starting from the beginning of February. ![]()

The streaming platform said its Premium plan will rise from $11.99 to $12.99 per month in the United States, Estonia, and Latvia. The change, which represents an increase of around 8.3%, will take effect from subscribers’ billing dates in February.

Christoffer Jennel has published a pre-earnings report on Spotify, which will release its Q4 results on February 10. ![]()

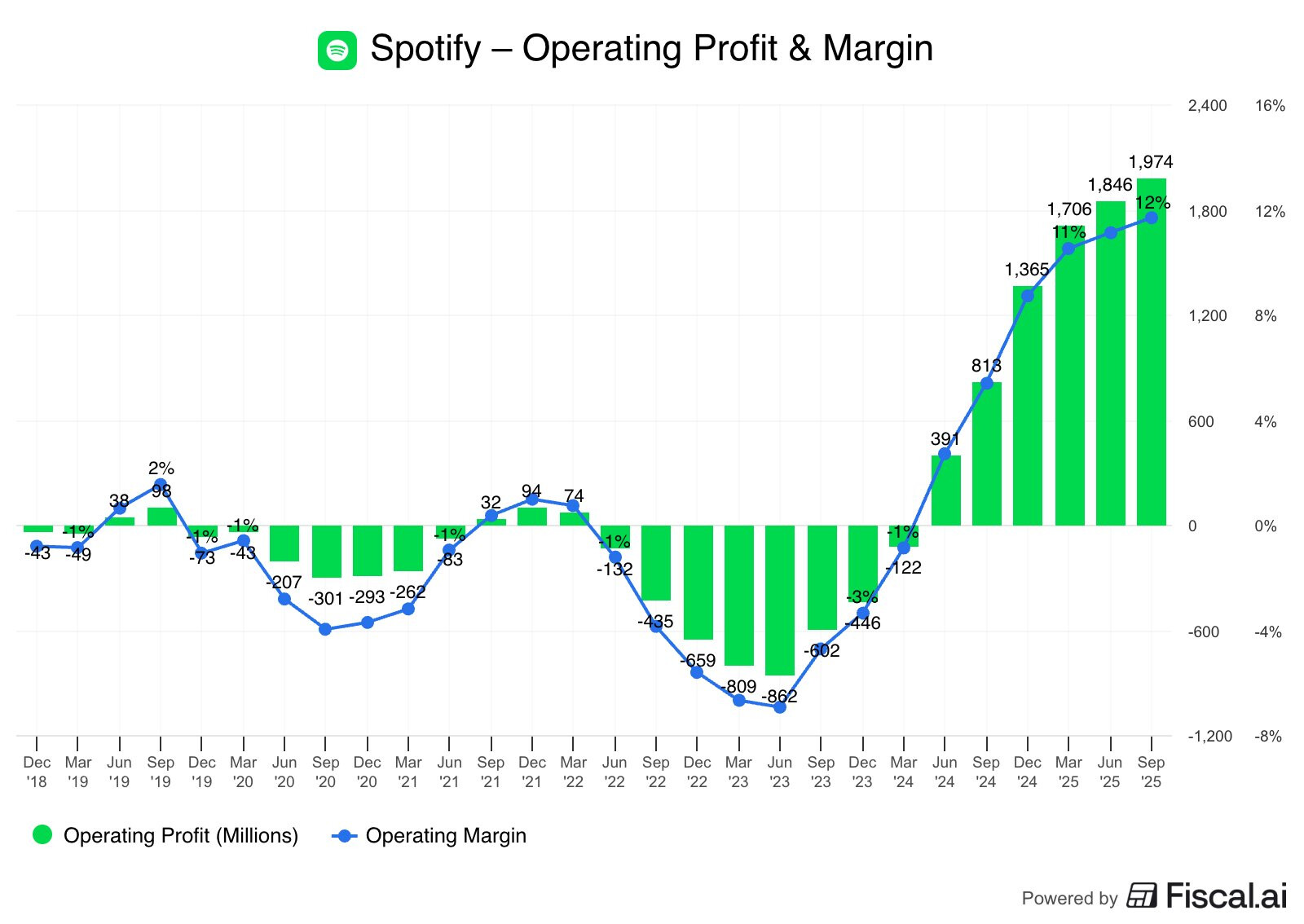

Spotify reports its Q4 results on Tuesday, February 10, before the market open. We do not expect major surprises regarding revenue and user metrics. However, we expect operating profit to exceed guidance, due to lower social costs resulting from the weakness in the share price during Q4. Following the recent price hike in the US and previous international increases, we expect investors to focus on management’s comments regarding churn, subscriber growth, and the broader pricing strategy leading up to 2026. In our view, the decline in the share price has significantly improved the valuation profile, and Spotify is now trading below our acceptable valuation ranges (EV/FCFF 26’: 23x, EV/EBIT: 28x, EV/GP: 12x). As the company’s fundamentals remain intact in our view, we are now more positive about the stock and see attractive risk-adjusted upside from current levels. We are therefore upgrading our recommendation to Accumulate (prev. Reduce), but lowering our target price to $590 (prev. $655) to reflect what we believe are lower justified valuation multiples due to the contraction of peer multiples.

Christoffer’s comprehensive quick comments on Spotify’s Q4 results. ![]()

Spotify’s Q4 report showed strong operational performance, and profitability exceeded our forecasts. User growth also exceeded our forecasts, primarily due to the strong development of ad-supported users. Although Q1 revenue guidance fell slightly short of expectations due to currency headwinds, the subscriber outlook remained unchanged. More importantly, the profitability outlook was significantly stronger than expected, supported by better-than-expected operational efficiency and the impact of smaller-than-expected renewed licensing agreements throughout 2025. Consensus seems to be focusing on the profitability and user growth beats, and shares rose by about 10% in the pre-market after several weeks of decline. Following the report, we see primarily upward pressure on our profitability forecasts.

@christoffer.jennel has published a Q4 update on Spotify. It’s an interesting report, I recommend checking it out. The valuation is certainly not cheap yet, but it likely won’t be for a long time. The company has taken quite a hit in the software sector’s AI crash, even though it’s harder to see such a clear disruption threat for the company imo. Of course, the share price had been rallying for a while, making a correction quite welcome.

Here is a link to the English report, which is free to read.

Spotify is investing in AI, such as ChatGPT integrations and personalized playlists, to retain its users in fierce competition with Apple, Amazon, and YouTube.

The goal is to improve music discovery and engage more users.

According to experts, AI can be a decisive advantage as music selections become more similar and easier to copy.

Key Points

- A new ChatGPT integration with Spotify and a “Prompted Playlists” feature are signals from the music streamer that investing in AI may be the best defense from threats including AI commodification of music and Apple, YouTube and Amazon competition for subscribers.

- Spotify, which has seen its stock price slump over the past year, says its interactive DJ, introduced in 2023, now has roughly 90 million subscribers and has racked up four billion hours of user time spent.

- “The catalogs at Amazon, Apple and YouTube are similar — nearly identical songs — to Spotify, just like Bing and Edge are nearly identical to Google,” says Michael Pachter, Wedbush Securities senior advisor.

https://www.cnbc.com/2026/03/22/spotify-apple-amazon-streaming-music-ai.html

Christoffer Jennel has written preliminary comments on Spotify, which will publish its Q1 report on Tuesday, April 28. ![]()

We expect the company to demonstrate continued operational development characterized by stable user growth and strong profitability improvement. While reported revenue growth still faces significant currency headwinds, we anticipate the underlying business to remain strong, supported by recent pricing actions in the US and a continued focus on AI-powered operational efficiencies. Our Q1 expectations are largely in line with the company’s guidance, although we have raised our EBIT forecast due to the impact of the negative share price development (-17%) in Q1 on social security contributions. Following the recent strengthening of the share price, some of the upside we saw has already materialized. Spotify is currently trading at the lower end of our acceptable valuation ranges (EV/FCFF 26’: 24x, EV/EBIT: 28x, EV/GP: 12x), which still leaves upside potential for the stock. However, due to the recent share price increase, we are lowering our recommendation to “add” (previously “buy”), leaving our target price unchanged at USD 595.

Spotify and Peloton are launching an extensive partnership by making over 1,400 diverse fitness classes available to Premium subscribers globally.

Through this move, Spotify is expanding into physical wellness, while Peloton seeks international growth by moving from hardware toward scalable digital content, leveraging Spotify’s network of hundreds of millions of users.

Key Points

- Spotify is partnering with Peloton to launch a fitness category with more than 1,400 classes available for Premium users globally.

- This is Spotify’s first push into wellness as it looks to boost engagement and unlock new monetization beyond music and podcasts.

- Peloton, meanwhile, is aiming to expand its international reach as it pushes beyond a hardware-centric model.

https://www.cnbc.com/2026/04/27/spotify-peloton-fitness-content-hub.html

Here are Christoffer Jennel’s quick comments on Spotify’s Q1 results. ![]()

Spotify’s Q1 report met our expectations in terms of both revenue and profitability, showing continued operational progress. However, Q2 guidance was mixed. While gross margin and Monthly Active Users (MAU) slightly exceeded our expectations, the operating profit guidance of 630 MEUR was approximately 10% below our forecast, suggesting significantly higher operating expenses than we had modeled. Consensus seems to focus on the Q2 operating profit miss and a modest 1 million subscriber miss compared to consensus, with the stock down about 12% in pre-market trading. Following the report, we see moderate downward revisions to our short-term profitability forecasts, while our long-term view remains unchanged.

And here is the company report, Christoffer style ![]()

Spotify’s Q1 results were in line with our expectations, showing that operational momentum continues. However, the Q2 guidance was mixed. Although gross margin and user metrics (MAU) slightly exceeded our expectations, the operating profit guidance was weak and below our forecasts, reflecting an increase in operating expenses related to elevated marketing, cloud, and AI investments. Crucially, however, management stated that these elevated investment levels are expected to continue for only the next one or two quarters before moderating, while reiterating that the full-year operating margin will still grow y/y. As such, we consider the impact to be temporary rather than structural, leaving our medium-term thesis intact. In our view, the post-earnings market reaction therefore appears excessive and overly short-sighted, creating an attractive opportunity for long-term investors to capitalize on short-term noise at attractive valuation multiples. We are upgrading our recommendation to Buy (prev. Accumulate) while lowering our target price to $570 (prev. $595) due to lowered forecasts.