Voiko tosiaan olla niin, että Inderesin foorumilla ei ole ainoatakaan sijoittamisen psykologiaan keskittyvää ketjua? En ainakaan haulla löytänyt.

Siivotaanpas tämä foorumin häpeätahra saman tien pois ja aloitetaan suuri sijoittajapyskologia-keskustelu!

Lähden nyt kirjoittelemaan aiheesta ihan lonkalta ja katsotaan mihin päädytään. Aloitetaan vaikka määritelmästä (wikipedia):

Psykologia (vanha nimitys sielutiede) on tieteenala, joka tutkii ihmisen mielen sisäisiä tapahtumia kuten tunteita, muistia, ajattelua ja käyttäytymistä. Laajemmin psykologian harjoittamisessa on kyse mielentapahtumien ja käyttäytymisen lainalaisuuksiin liittyvän tiedon soveltamisesta ongelmanratkaisussa.

Sijoittajapsykologiasta ei löytynyt näköjään oikein mitään järkevää määritelmää. Eri lähteissä aihetta oli kyllä jotenkin koitettu määritellä – joskus hyvin, joskus vähän vähemmän hyvin – mutta määritelmät ja kirjoitukset näyttivät keskittyvän pääasiassa käyttäytymistaloustieteeseen ja erilaisiin vinoumiin. Mielestäni yksittäisiä vinoumia tarkastellen saa kyllä käsityksen yhdestä sijoittajapsykologian osa-alueesta, mutta suurin osa sijoittajapsykologian hienouksista jää käsittelemättä.

Mutta ei hätää. Kaiketi ihan hyvän määritelmän saisi jo pelkästään muokkaamalla tuota edellistä psykologian määritelmää.

Sijoittajapsykologia on ala, joka tutkii ihmisen mielen sisäisiä tapahtumia kuten tunteita, muistia, ajattelua ja käyttäytymistä sijoittamisessa.

Mennään vaikka tällä.

Voi olla, että lähden nyt sukeltamaan aiheeseen mielestäsi hieman liian kaukaa, mutta olen vakaasti sitä mieltä, että sijoittajapsykologiassakin on ensin hyvä laittaa oma pesä kuntoon. Ja omalla pesällä tarkoitan tässä yhteydessä esimerkiksi itsetuntemusta, omia psykologisia piirteitä ja ominaisuuksia sekä ylipäätään ymmärrystä psykologisten tekijöiden vaikutuksesta ihan kaikkeen.

Mennään heti esimerkkeihin, niin saadaan vähän paremmin otetta. Aloitetaan vaikkapa uskomuksista:

Millaisia uskomuksia sinulla on sijoittajana? Kenties seuraavanlaisia:

- ”En kestäisi, jos häviäisin rahaa.”

- ”Minä olen taitavampi sijoittaja kuin muut.”

- ”Minulla pitää olla uusi auto.”

Mitä luulet, onko näistä esimerkkiuskomuksista hyötyä sijoittamisessa? Tunnistatko ylipäätään toimintaasi ohjaavat uskomukset? Voisitko jatkossa kenties paremmin huomata ne ja niiden vaikutukset tunteisiisi, ajatuksiisi ja käyttäytymiseesi, sekä mahdollisesti korvata ne paremmilla uskomuksilla?

Tai hei. Nyt tuli mieleen hyvä. Tapojen voima ja ihmiselle ominainen uomakipittäjyys:

Millaisia tapoja sinulla on sijoittajana? Kenties seuraavanlaisia:

- Käytät paljon aikaa klikkiuutisten lukemiseen (vaikka voisit käyttää saman ajan esim. analyysien tai osavuosikatsausten lukemiseen)

- Myyt voittajaosakkeesi heti kun ne ovat nousseet (vaikka voisit antaa voittojen rullata, jos kerran liiketoiminnan tulevaisuus on valoisa)

- Menet jatkuvasti katsomaan kurssi- ja tuottokäyriä (vaikka voisit käyttää saman ajan esim. analyysien tai osavuosikatsausten lukemiseen)

Todennäköisesti sinulla on sijoittamisen lisäksi muillakin elämän osa-alueilla hyvinvointia heikentäviä tapoja. Päivitä nekin. Vähän sporttia arkeen, aikaisemmin nukkumaan ja päivittäin terveellinen päivällinen yhdessä vaimon ja lasten kanssa. Ja lopeta se kännykän räplääminen. Lue mieluummin vaikka kirjaa (juu, tiedän, kuulostaa keski-ikäiseltä ja tylsältä). Jos muuten haluaa lukea tavoista lisää, niin sekä Charles Duhiggin että James Clearin teokset ovat ihan timanttia.

Nyt moni varmaan jo miettii, että aika ohueksi katosi punainen lanka, kun mies puhuu päivällisistä ja linkkailee jotain sportti-hyvinvointi -valmentajan höpinöitä. Johtunee siitä, että olen vain itse niin tolkuttoman innoissani tästä aiheesta, että ehdin jo unohtaa teidän kanssasijoittajien toiveet. Ei se mitään, lähdetään kohta kerimään tätä takaisin sijoittamisen pariin. ![]()

Pari sanaa vielä itsetuntemuksesta ja oman arkielämän psykologiasta. Aiheesta on tehty ihan valtavasti hyviä kirjoja. Lue edes yksi. Ne tarjoavat lähes poikkeuksetta sellaisia oivalluksia, joista on hyötyä myös sijoittamisessa, jos nyt psykologian maailma ei muutoin kiinnosta. Pätevät ja asiantuntijavoimin kirjoitetut self-helpitkin ajavat usein asiansa, kunhan katsoo, ettei kenenkään puoskari-hampuusin kirjoja mene sokeasti uskomaan. Mutta psykologian parissa työskentelevät asiantuntijat ovat tuotteliasta väkeä ja esimerkiksi seuraavilla pääsee jo hyvään alkuun:

- Mielen voima -kirjasarja - Virolaisen veljekset

- Psyykkinen valmennus – Tossavainen & Peltonen

- Joustava mieli & Kohti arvoistasi – Arto Pietikäinen

Kun olet käyttänyt pari-kolme vuotta psykologisten self-helppien, avoimen yliopiston psykologian perusopintojen ja psykologisten podcastien tonkimiseen, onkin aika tutustua käyttäytymistaloustieteeseen. Ja mennään nyt äkkiä sen pariin, ennen kuin joku alkaa syyttää puoskaroinnista.

Käyttäytymistaloustiede:

Otetaan alkuun taas esimerkki ja otetaan se ihan sieltä helpoimmasta päästä:

Fear of missing out ( FOMO ) is the feeling of apprehension that one is either not in the know or missing out on information, events, experiences, or life decisions that could make one’s life better. FOMO is also associated with a fear of regret, which may lead to concerns that one might miss an opportunity for social interaction, a novel experience, a memorable event, or a profitable investment.

Otetaan perään vielä elävän elämän tapahtuma, joka kuvaa mielestäni fomottamista:

Joku tunnettu foorumilainen (myöhemmin TF) tekee uraa uurtavaa analyysiä pörssiin listatusta yhtiöstä ”Turska X”. Hän saattaa päättää analyysinsä avaamalla Turska X:lle jopa oman ketjun. Hän on löytänyt tästä yhtiöstä merkittävää potentiaalia ja ostanut itse osaketta salkkuunsa. TF kirjoittaa vielä ”Ostin/myin juuri äsken” -ketjuun pienen jutun Turska X:stä ja siitä, että on tehnyt merkittävän sijoituksen yhtiöön.

Se mitä tapahtuu tämän jälkeen, kuvaa mielestäni hyvin FOMO-ilmiötä.

Ensin keskusteluun saapuvat Kari ja Jari: ”Otettu pieni avauspositio Turska X:ää.” Sen jälkeen Seppo, Tero ja Minnakin saapuvat paikalle: ”Otin myös Turska X:ää. Hyvät perustelut TF:llä”. Tässä vaiheessa fomo voi olla vielä varsin pientä ja kyse on ehkä enemmänkin tunnetun sijoittajan peesailusta (joka lienee vähintäänkin sukua fomolle).

Nyt Turska X on kuitenkin saanut jo merkittävää huomiota Ostin/myin juuri äsken -ketjussa ja paikalle saapuvatkin karmit kaulassa ja ostohousut kahisten Matias, Markku, Mirkku, Kinkku, Timo, Kari ja Kerttu. He kertovat kovaan ääneen ostaneensa myös Turska X:ää (osa jopa koko salkun varallisuudella). Kari ja Kerttu, jopa kertovat viesteissään, että fomosta johtuen oli pakko ostaa. Tämä porukka on kaikkein suurimmassa vaarassa joutua fomon uhriksi. Lopulta voidaan olla tilanteessa, jossa yhtiöön sijoitti yhden iltapäivän aikana sata foorumilaista, joista vain yksi teki analyysin.

(Ja juu, sinä et tietenkään ollut yksi fomon uhreista, vaan pitkään valmisteltu ja ostosignaalin antanut analyysisi Turska X:stä vain sattumalta valmistui juuri tuona kyseisenä iltapäivänä.)

Kokeneemmat sijoittajat harvemmin lähtevät kaiken maailman hype-juttuihin mukaan ilman omaa analyysiä. Todennäköisesti se johtuu kokemuksen tuomasta rauhallisuudesta ja viisaudesta. Jotenkin en kuitenkaan jaksa uskoa, että kaikki kokeneet sijoittajat olisivat täysin immuuneja FOMO:n kaltaisille tunteille kaikissa tilanteissa. Ehkä he vain ovat parempia tunnistamaan sellaiset tunteet ja ajatukset, joita ei ole pakko uskoa ja lähteä seuraamaan.

Jos haluaa ottaa sijoittajapsykologiasta vain välttämättömät osat, kannattanee keskittyä käyttäytymistaloustieteeseen:

Käyttäytymistaloustiede tai behavioraalinen taloustiede on taloustieteen tutkimussuunta, jossa tutkitaan psykologisten, sosiaalisten, kognitiivisten sekä tunneperäisten tekijöiden vaikutusta ihmisten ja instituutioiden taloudelliseen päätöksentekoon sekä niiden seurauksia markkinoihin ja resurssien jakoon.

Behavioraalinen rahoitus (engl. Behavioral finance ) on siihen läheisesti liittyvä tutkimusala, joka pyrkii tarjoamaan psykologisia ja kognitiivisia selityksiä erilaisiin rahoitusmarkkinoilla esiintyviin anomalioihin. Behavioraalisen rahoituksen tutkimusasetelma pyrkii huomioimaan sen, ettei ihminen kykene tietokoneen tavoin toistamaan täysin rationaalista päätöksentekoa. Vastoin rahoituksen akateemisen tutkimuksen valtavirtanäkemystä, markkinoiden tehokkuuden koulukuntaa, behavioristinen rahoitus näkee, että sijoittajien järkevistä pyrkimyksistä huolimatta heidän rationaalisuutensa on parhaimmillaankin rajallista.

Käytännössä käyttäytymistaloustiede keskittyy esimerkiksi erilaisiin kognitiivisiin harhoihin ja vinoutumiin. Heitän nyt ihan lonkalta muutaman esimerkin:

Tappiokammo (loss aversion) = Tappiot sattuvat enemmän kuin voitot antavat tyydytystä. Voi johtaa esimerkiksi tappioiden ja epäonnistumisten välttelyyn, ja sitä kautta lamauttaa päätöksenteon. Voisi ajatella, että tappiokammo johtaa myös esimerkiksi defensiiviseen päätöksentekoon:

https://twitter.com/Salkku_Mauri/status/1470085081616338945?s=20

https://twitter.com/Salkku_Mauri/status/1470085083738611712?s=20

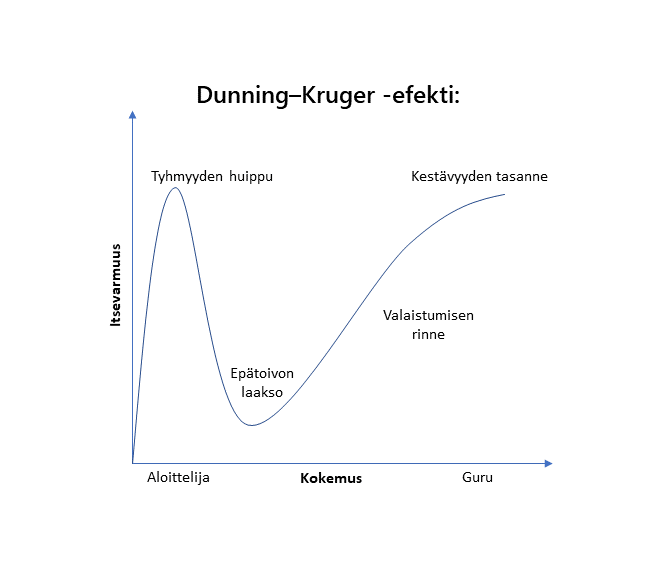

Ylivertaisuusvinouma on kognitiivinen vinouma, jossa yksilö yliarvioi itsensä jossakin suhteessa kuten vaikkapa jonkin taidon hallinnassa. Lisäksi tyypillisesti mitä huonompi yksilö on kyseisessä taidossa sitä enemmän hän yliarvioi osaamistaan. Tämän voi katsoa johtuvan siitä, että kun yksilö ei hallitse taidon suorittamista, ei hän osaa myöskään arvioida osaamistasoa.

Jos haluat perehtyä tarkemmin käyttäytymistaloustieteeseen, niin lue ainakin seuraavat:

- Ajattelu nopeasti ja hitaasti - Kahneman

- Väärin käyttäytyminen - Thaler

- Signaali ja kohina - Silver

- Riskitietoisuus - Gigerenzer

- Petos ja itsepetos ihmiselämässä - Trivers

Erityisesti Thalerin kirjassa on esimerkkejä ihan sijoittamisestakin, mutta toisaalta kaikki tarjoavat sijoittajalle hyviä esimerkkejä. Kun vain opit kunkin vinouman logiikan, voit varsin näppärästi lähteä soveltamaan niitä sijoittamisen maailmaan, vaikka esimerkit kirjoitta olisivatkin terveydenhuollosta, vedonlyönnistä, urheilusta tai parisuhteesta.

Ylipäätään Terra Cognitan kirjat on lähes aina sairaan kovia, ja antavat hyvää ajattelemisen aihetta laajemminkin talouteen, yhteiskuntaan ja käyttäytymiseen.

Paljon jäi vielä sanomatta, mutta mennään nyt alkuun vaikka tällaisella avauksella. Ja muista, että sijoittaminen on X prosenttia sijoittamista ja Y prosenttia psykologiaa, ja Y > X. Prosentit saat päättää itse.

![]()

")

")

")