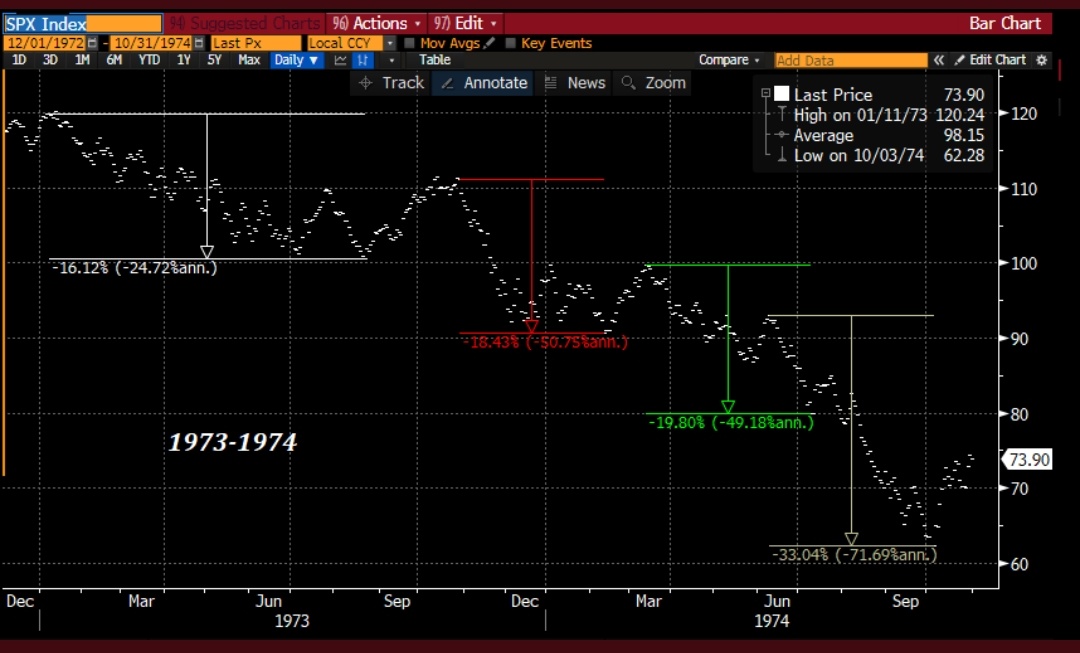

During such downturns, one starts to ponder the psychology of investing and their own reaction to a shrinking portfolio. As the plunge steepens, the thought constantly creeps in: should I sell my OST holdings, watch from the sidelines for a bit, and then buy back cheaper later? This is illogical, as the return potential of stocks whose story/investment case has remained practically unchanged (e.g., Qt, Harvia, Remedy) continuously increases as their prices fall.

My strategy is to buy quality companies for long-term holding in both my OST (equity savings account) and AOT (regular investment account), and for OST, try to lighten up when “we rise too much” and buy more/back when prices drop due to reasons unrelated to the company. From the Covid-19 dip until today, this strategy has worked quite well, but now tighter monetary policy, inflation, and the seeming shift in sentiment generally over a slightly longer term pose additional challenges.

I have been investing regularly in stocks every month since 2010, and in recent years, I have been adding nearly €1000/month of new money to my portfolio. I will likely remain a net buyer for the next 15 years. Although, for example, @Verneri_Pulkkinen emphasizes in his videos that a net buyer should actually hope for a market downturn to buy cheaply, it’s not very comforting to be able to inject that €1000 of new money into the market when the portfolio simultaneously drops by €30,000.

Because of this, it would be important to be able to increase my cash position as described above, and I did manage to accumulate some cash in my OST from the “stump-Santa rally” at the end of December. However, I notice that I often start buying too early, and now most of my cash is back in play.

As the downturn continues, I must either watch my portfolio continue to shrink or sell against my strategy during the fall, even though the return expectations of stocks are constantly growing. My portfolio mainly consists of companies from Inderes’ model portfolio and those familiar from the forum, and the diversification is quite good, with no single stock having too much weight (1. Harvia, 2. Qt).

An intelligent investor would surely be inclined to accept a temporary decline and buy more stocks with the cash added to the portfolio. If, for example, Qt were to drop to around €80 from here, I would surely blame myself for not selling at €105 and buying back at €80, but on the other hand, it would be more regrettable if it recovered to €130-140 levels and my OST position had been sold at the bottom. Timing buying and selling is proven to be extremely difficult, and perhaps generally one should accept their own inability and understand that no one is perfect in investing, and one could always have bought/sold at a better moment.

Anyone else having similar thoughts in the midst of this slide?