Let’s open a thread about this. This is an interesting growth company I came across on a YouTube channel. Shift Technologies is an online car dealership that went public last year and raised approximately $300 million in funding through a SPAC arrangement.

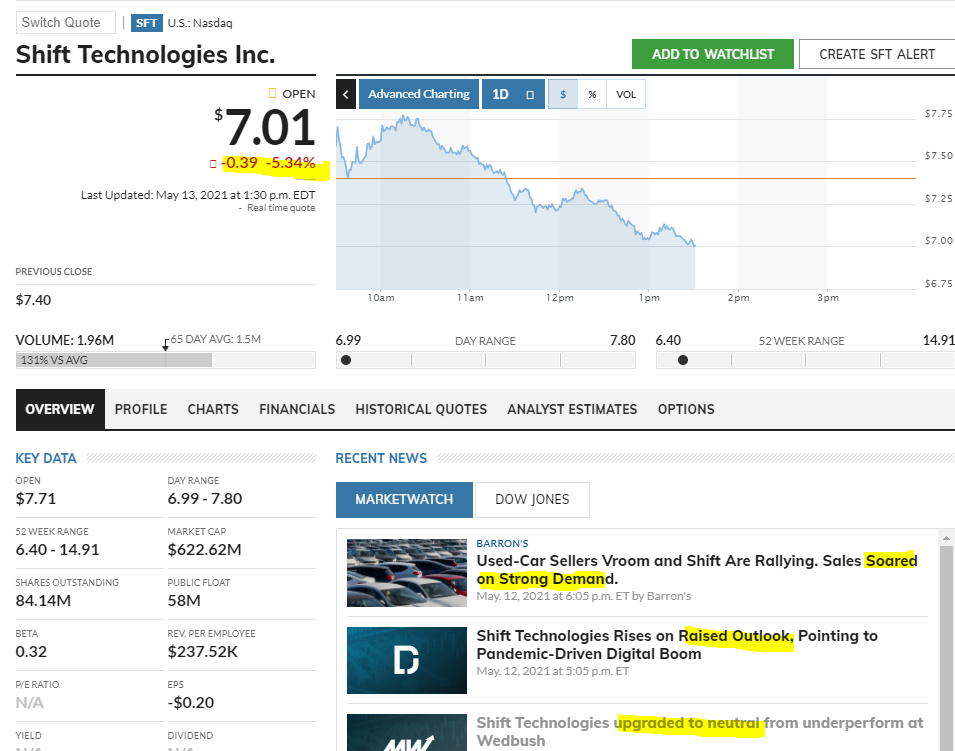

It’s an online used car dealership founded in 2013, operating in the United States, with about 3,000 cars in its selection and a market value of approx. $600 million. Its P/S ratio based on this year’s forecasts is only 1.35.

The US used car market is huge, about $840 billion. The share of online sales is still less than 1% of this market. The hundred largest car dealerships in the country account for less than 6% of the entire market. In addition, the US is the world’s second-largest online market after China, so there’s plenty of room for growth on its own continent.

The company is growing over 100% annually, but growth has come at a price, and last year the company made a loss of $59 million on revenues of $196 million. The company has raised approximately $220 million in funding over the years, with major investors including Lithia Motors and BMW iVentures.

In the last quarter of last year, they spent about $10 million on marketing, so their marketing budget alone is over 40 times larger compared to, for example, a Finnish car dealership.

The losses are huge for both Shift and its competitors.

But in the long run, investing in the US car dealership market has been very profitable, including Carmax, Autonation, Lithia Motors, Carvana, etc…

Competitors in online car sales include:

Carvana => Revenue: $5.5 billion P/S: 2.54

Vroom => Revenue: $1.3 billion P/S: 2.11

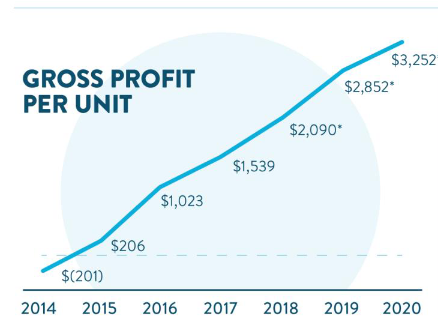

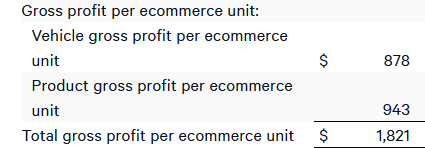

Figures from last year (2020):

- Revenue $195.7 million

- Net result (-$59.2 million)

- Cars sold 13,135 units

Forecast Q1 2021

- Revenue $90-95 million

- EBITDA ($33 million)-($35 million)

Forecast for 2021

- Revenue $450 million

- EBITDA margin >(25%)

- Cars sold 20,900 units

Based on the numbers, this is a very risky investment, but Carvana has also risen well despite making staggering losses in recent years. Shift still had $233 million in cash at the end of last year.

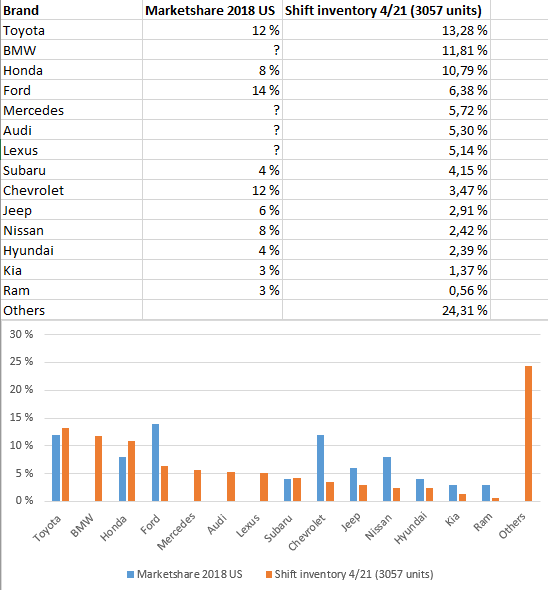

Growth seems to continue in the first quarter of the year, at least in terms of car inventory. The Q4 average was 850 units, and now over 3,000 units (Jan 1665 units, Feb 2089 units), so at least a record-breaking quarter in terms of revenue is coming.

Correct me if necessary.