I hadn’t even thought to check Glassdoor. It certainly looks weak based on that, but I believe that the large layoffs in 2022 also heavily influence the numbers, which, based on comments, were handled poorly. When reading a bit more comments, the negative side largely mirrors Lemonade’s “micromanagement,” “processes constantly changing,” “no proper onboarding,” “a lot of calls” (apparently on the claims side). Additionally, one ROOT comment mentioned that claims data is recorded in Google Sheets instead of a claims system, which sounded very peculiar. Based on that, there seems to be huge potential for improvement in their systems, if one is looking for a silver lining.

I would argue that in both ROOT and Lemonade, the employee headcount is heavily weighted towards claims processing, which is not very glamorous, especially if one has to take 30-50 customer calls per day (I have experience). In car accidents, there is often an immediate situation, making it common to call the insurance company instead of submitting an online claim. ROOT practically only does car insurance, although they have already started expanding into home insurance (Renters insurance in an app | Root Insurance). For Lemonade, car insurance is still small, and home and pet insurance make up the clear majority. In these types of insurance, online claim notifications are much more common, which is considerably more pleasant for a claims handler.

These are my thoughts on the Glassdoor reviews, but as stated, ROOT certainly has a lot to improve in that area.

If one starts to compare ROOT and Lemonade more closely, I believe that purely from a customer acquisition perspective, Lemonade has a better strategy in offering a wide range of insurance products, especially in insurance types (home and pets) where customer retention is better compared to car insurance. It also helps with cross-selling, e.g., in car insurance, where Lemonade also uses telematics. A home insurance customer can be offered a test period with telematics, after which they receive an offer for car insurance. However, I find it peculiar that they, as such a small player, have also expanded into Europe.

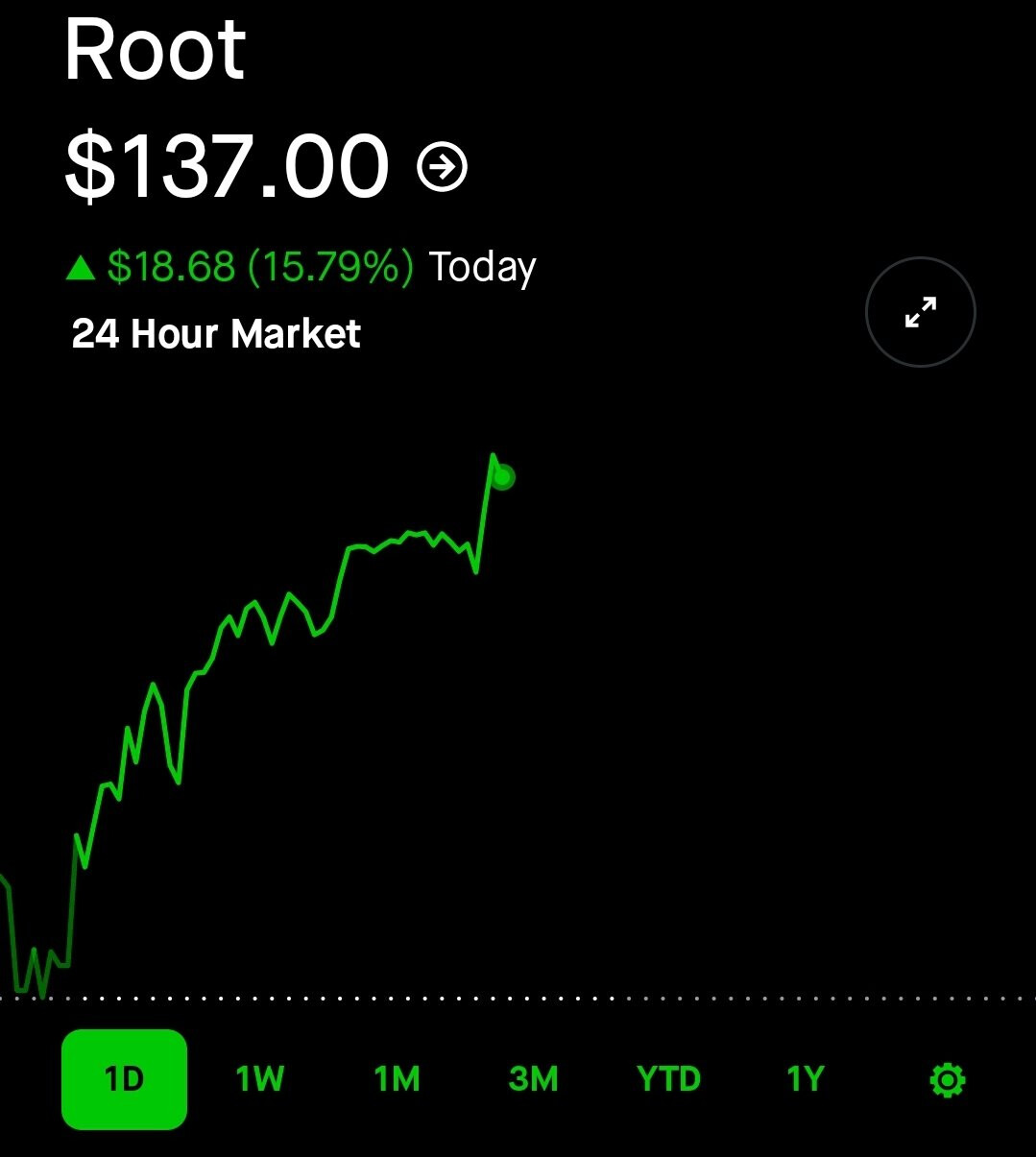

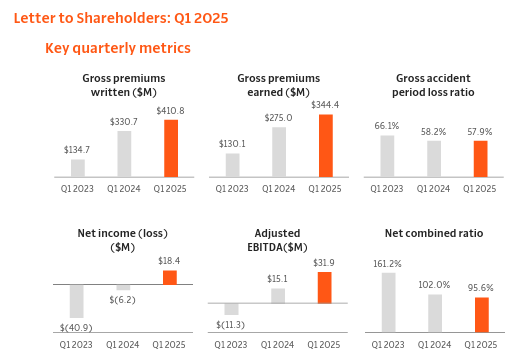

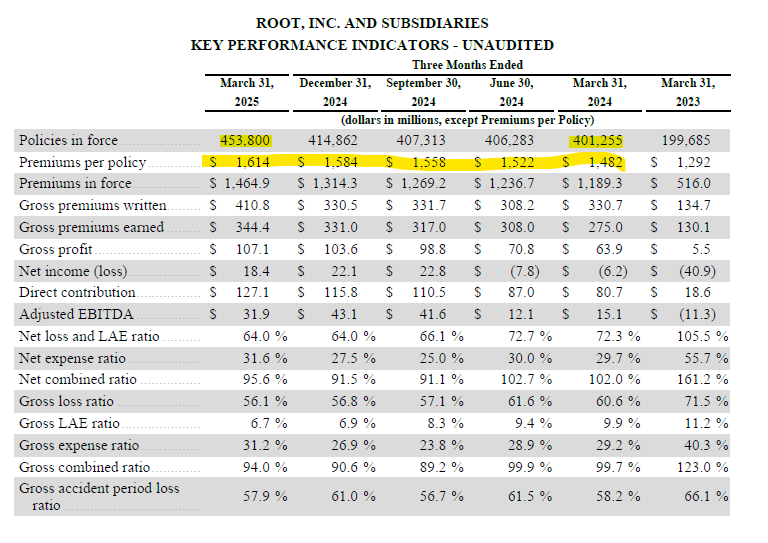

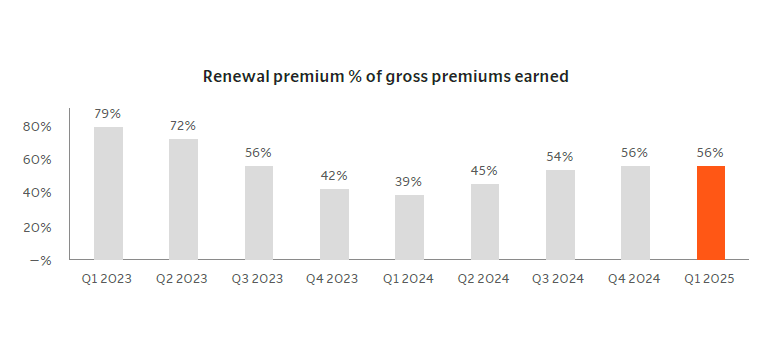

ROOT’s customer acquisition slowed significantly in Q2, but new geographical openings and sales channels will hopefully support growth in H2. Otherwise, the stock might be in for a rough ride, as management has already promised that costs will increase significantly in H2, which could cause earnings to fall back into loss. Management’s strategy for customer acquisition seems to be focusing on the partnership channel (Carvana, brokers/agents, etc.), which I believe is much weaker than direct sales, because in the partner channel they have to onboard the customer before a test period. In the Q2 earnings report, they mentioned that they cut marketing investments specifically from direct sales because the competitive situation is tight. Hopefully, the new pricing model improves the customer experience in that partnership channel; below is an excerpt from the Q2 earnings report:

“This included the launch of our new pricing model in several states, with early indicators showing that this model is substantially improving our risk selection, increasing estimated customer lifetime values by 20% on average.”

Lemonade (H1/-25: 35% relative to revenue excluding investment income) also spends significantly more money on sales and marketing compared to ROOT (H1/-25: 12.4% relative to revenue excluding investment income). This is also reflected in the results. Additionally, Lemonade has a 10-percentage point weaker Loss ratio (75% vs. ROOT’s 65%).

ROOT also has clear room for improvement on the investment income side. I don’t fully understand why they are holding such a large cash reserve (40% of the balance sheet) unproductively in an account. For Lemonade, the corresponding share is 20%.

An interesting H2 is coming.