What the heck is driving this down? After the earnings report, it was up almost +10%, and now those gains have been skied away, along with the interest. The future looks good, it’s a strong dividend payer + low valuation currently. Of course, print media might lose market share to electronic media, but I still can’t understand these movements.

Oh well, guess I’ll have to buy more. What are others’ thoughts on Sanoma?

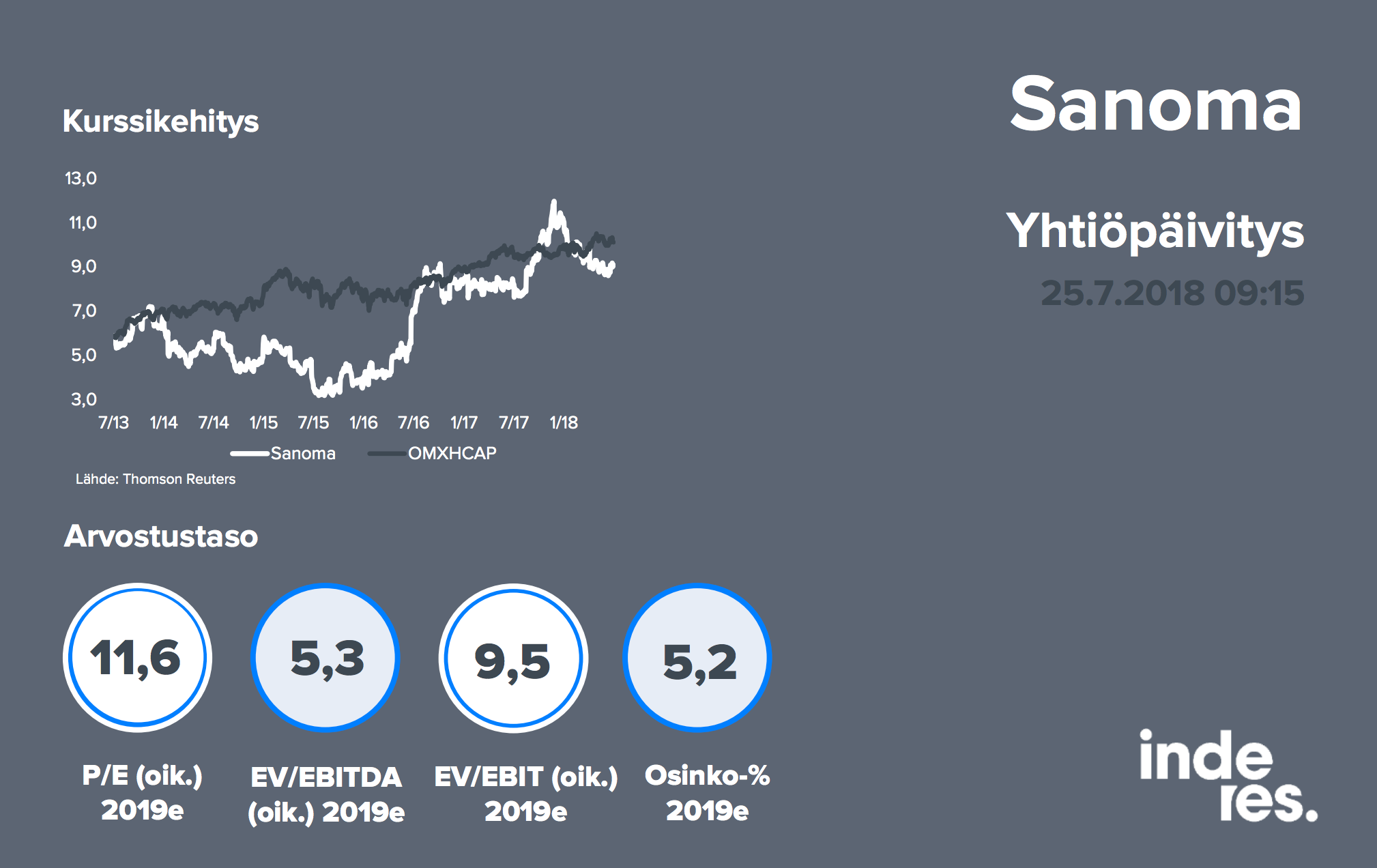

Well, based on Aho’s forecasts, it doesn’t look expensive for next year (2019e). Where do you think Sanoma will be in 3 or 4 years?

If/when the share of juicy digital revenues grows, this could develop into an even stronger and more stable cash cow. Currently, the secular decline of print media is obviously weighing on the top line; we should look “under the surface.”

Sanoma’s goal, in accordance with the new dividend policy, is to distribute a growing dividend, which is 40–60 percent of annual business cash flow minus capital expenditures.

So I expect Sanoma to have something small in mind if they intend to distribute a growing dividend

Elections are approaching, and several parties’ education policy programs include a provision for free secondary education. Could this open up an opportunity for Sanoma to bring the Iddink format to Finland as well?

Was it like that last time, that we were nervous around Q1? This should be a pretty stable stock in terms of performance, right? I already took out about 10% and bought some back, I guess I have to grab the position back when the price drops soon?

Especially when that digital education deal might be finalized in the latter half. Digital digital…

The NY Times is experimenting with this kind of “emotional targeting” model for ads. They already consider it a success and it also better protects users’ personal data.

Waiting for Sanoma’s opening. Just recently, there was a statement from Inderes that even though digital marketing at Sanoma is slightly increasing, it won’t compensate for the big hit coming from the decline in print advertising. This holds true with the current trend and in the short term, but if they look at what others are doing around the world, they might very well get new advertising revenue from such initiatives, which are specifically wanted for digital newspapers and not, for example, Facebook. I personally now prefer reading Helsingin Sanomat (Hesari) from the app rather than print, and a few ads there have been relevant. My intention is to hold until, for example, the printed Hesari is no longer available (if I live that long).

Based on the numbers, it just tilted quite a bit towards performance-based. If one believes that the acquired money will lead to a better acquisition, then it could be quite good. However, I’m not at all familiar with Sanoma’s business.

I read in the news that Sanoma will use the money to pay off its debts, but it was mentioned that the deal opens up possibilities for M&A (Mergers and Acquisitions) worth 400 million euros, meaning that much new debt will be taken, apparently with better terms than the current ones? Perhaps getting rid of print newspapers was wise, but it won’t materialize until something new and sensible to buy has been found and integrated. So, for me, it’s a bit 50/50 how to approach this.

I’m just getting into this as I’m on a business trip… I would think, however, that they would have already thought about further investment targets for the money, and presumably they want to invest in digital business, especially in school materials?

Probably quite logical, I can’t say about the price, but at least the stock was rising while the index was in the red, so probably quite good :)?

I’m just listening to Susan’s presentation. Sounds good! Selling a less profitable business and buying a more scalable, more profitable, growing business instead?

Sanoma is one of my favorites for 2020, even if it’s not a huge stake. I expected growth in revenue and profit, now I expect at least a fair relative improvement in profitability and that they will continue to build up learning. Presumably, valuation multiples can rise.

Susanin’s comments at least suggest that several potential targets are in sight. Learn has, however, brought good profit with less business momentum compared to that legacy.

Sanoma has now become a much more interesting acquisition target. It was pretty clearly said on the cast that they are shopping around, if not quite at the checkout, then at least browsing the shelves.

The stock movements after the Dutch deal were interesting.

Some would probably have liked to keep the Dutch operations, as their nature was known.

If one trusts the management now, one must assume that they have calculated that the money received can be invested more profitably than before, creating shareholder value.

I would argue that if the Dutch operations had been kept, revenue and profit would have increased, and valuation multiples would have risen.

#Sanoma announced new segment-specific growth and profitability targets. For Learning, the targets are slightly better than our forecasts, and for Media Finland, they are in line with our forecasts. The company will host an analyst day on 18.12., live on InderesTV: https://t.co/FyS9iepMimpic.twitter.com/L4vnBXDeyl