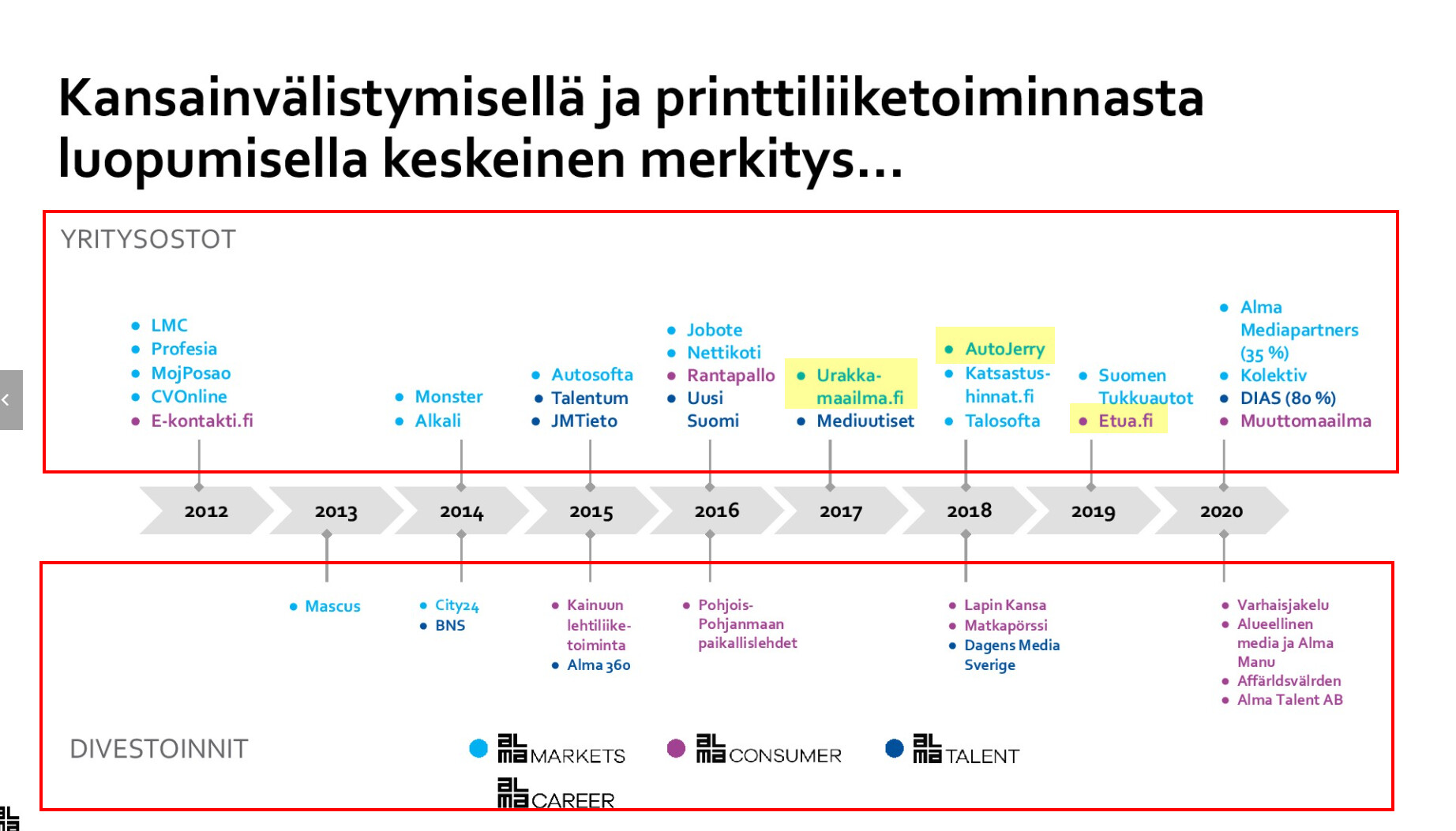

There isn’t much discussion about Alma Media on the forum. However, a lot has happened recently, and the company has been in constant change since the financial crisis. On its website, the company describes itself as “Alma Media is a strongly renewing multi-channel media company” with operations in 10 European countries. Alma Media has a reputation for paying stable dividends and generating good returns on capital. Early this year, the company sold its regional media and printing business to Sanoma, receiving 115 million euros in cash.

One question mark has been how to profitably invest the funds received from this sale, among others. Recently, however, interesting new developments have emerged, e.g., a little over 20% stake in Bolt Works (purchase price not disclosed):

https://www.almamedia.fi/sijoittajat/raportit-ja-esitykset/tiedotteet/tiedote/17-12-2020-alma-career-osakkaaksi-henkilöstöpalvelualan-teknologiayritys-bolt-group-iin

The full redemption of Alma Mediapartners from minority shareholders (including well-known brands such as Etuovi.com, Vuokraovi.com, and Autotalli.com) for 53 million euros:

And most recently, increasing the stake from five percent to just over 80% in DIAS Oy, specializing in digital real estate transactions, for 14.3 million euros and a possible additional purchase price:

Kai Telanne has been the company’s CEO since 2005. I believe Telanne has been very convincing in all interviews and events, realistically presenting the company’s market situation and transformation process over the years. In retrospect, it can be said that he has spoken sense, and Alma Media has indeed carried out the moves Telanne has promised. Telanne is currently 56 years old and will likely continue the transformation process for another 4-6 years, so I expect the determined journey to continue under good leadership.

Are there any investors on the forum who closely follow Alma Media? @Petri_Gostowski highlighted Alma Media as a success story during the coronavirus year in his section. If the company performs this well even in a difficult year, what kind of performance is possible with market tailwinds? What are your thoughts on the recent news, and what risks do you see in the development?

I myself am seriously considering additional investments in the company early next year. Alma Media may not be in the big spotlights, but I believe the company is currently developing a massive digital brand portfolio that is highly profitable, somewhat scalable, and further enhances the company’s ability to transform in the future in line with market developments.