Here are Aapeli’s comments on Sanoma’s Capital Markets Day.

Sanoma held a Capital Markets Day (CMD) on Tuesday. In the day’s presentations, the company provided more background on its updated financial targets and presented an overview of its business operations. The recording of the CMD can be viewed here.

Juho Toratti has also written about Sanoma and its CMD.

Subheadings:

Sanoma’s Capital Markets Day

Growth expected to be driven by the learning business

Media Finland market seen stabilizing – growth from gambling advertising

New financial targets

Sanoma pays annually growing dividends

Sanoma’s stock falling on CMD day

Investor’s perspective

Sanoma’s expectations rise, but valuation declines

NOTE.

IR Window is a channel for corporate partners of SalkunRakentaja and Sijoittaja.fi for background and analytical articles, as well as other interesting investor information. The article is part of a commercial collaboration with the company. The article does not contain investment recommendations.

Sanoma Oyj estimates that the liberalization of the Finnish gambling market to a licensing system in 2027 will bring a significant earnings boost to the company. At its Capital Markets Day, Sanoma stated that it expects an increase of over 20 million euros in Sanoma Media Finland’s annual advertising sales, which would directly impact the company’s profitability.

Here are Petri’s comments on Sanoma rearranging its financing again.

With the new EUR 220 million loan agreement, the company will repay two old loans, which was in line with our expectations and, in our assessment, will reduce its net financing costs.

Many still perceive Sanoma as a media company, even though today its traditional newspapers and multimedia services account for a minority of the group’s business operations. The main focus is instead on the learning business.

Subheadings:

Sanoma’s financial targets

Sanoma Group’s dividend in 2026

Sanoma’s Q3 results

Sanoma’s share – An investor’s perspective

Sanoma’s growth accelerates in 2026

Sanoma’s forecasts and valuation metrics

Note.

IR-ikkuna is a channel for corporate partners of SalkunRakentaja and Sijoittaja.fi for background and analytical articles, as well as other interesting investor information. The article is part of a commercial collaboration with the company. The article does not contain investment recommendations.

Petri has likely updated Sanoma’s company report from Torstaikalle.

We have reviewed our forecasts following Sanoma’s Capital Markets Day and updated financial targets. Our forecasts were also well-aligned with the current targets, and the forecast changes we made were primarily focused on Media Finland’s medium-term forecasts, which are affected by the expected opening of the gambling advertising market presumably during 2027. In our view, the stock’s valuation is attractive relative to the earnings growth we forecast for the coming years, so we are raising our recommendation to the Buy level (prev. Accumulate) and reiterating our target price of EUR 11.3.

Quoted from the report:

The strongest earnings growth will be in 2026, when we expect Learning’s revenue growth and a clear improvement in profitability to raise its result to a new level. Even after the clear improvement in profitability, we expect Learning’s revenue growth to keep it in clear earnings growth. Regarding Media Finland, we expect a slight improvement in operational efficiency in its historical fashion, but we forecast clear growth in its earnings level in 2028, when gambling advertising brings high-margin growth throughout the year. Our 2028e forecast includes roughly EUR 16 million in growth in ad sales (incl. other advertising growth), so our forecast is conservative relative to the company’s target level. This is due to forecast risks currently related to market size and the company’s market position.

Here are Petri’s preview comments as Sanoma releases its Q4 report on Wednesday

In connection with the earnings report, the main focus will be on the guidance for the current year, which should provide support for forecasts expecting brisk earnings growth. Due to this and seasonality, the Q4 figures will play a secondary role on the earnings day.

And here are Petri’s quick comments on the results.

*Sanoma released its Q4 results this morning, which were operationally well in line with our expectations. The company is also raising its dividend in line with our forecast. In the report, the main focus was on the guidance for the current year, which was as strong as expected and points to clear earnings growth for the current year.

Petri managed to interview Sanoma’s CEO Rob Kolkman right after the Q4 results “appeared”

Topics:

00:00 Introduction

00:12 Key highlights for 2025

00:45 Development of the Learning business

01:54 M&A

03:10 Weakness in the advertising market

04:31 Changes in gambling legislation open up growth opportunities

05:55 Drivers behind the guidance

Petri has released a new company report following the Q4 results.

Sanoma’s operating result was well in line with our estimates in Q4, and the dividend proposal also matched our forecast. The earnings guidance provided for the current year also fell exactly within our expected range. The company’s earnings growth outlook for the coming years is very good, in relation to which the stock’s valuation is moderate. Thus, we reiterate our Buy rating for the stock. Reflecting minor forecast changes, we revise our target price to EUR 11.5 (prev. EUR 11.3). Sanoma’s CEO’s Q4 interview (Eng.) can be viewed at this link.

Quoted from the report:

Free cash flow has strengthened

Sanoma’s cash flow from operations strengthened to EUR 199 million in 2025, which, after normal capital expenditures, lease liability payments, and hybrid loan interest, corresponds to a free cash flow of EUR 117 million. As a result, the company’s net debt settled at EUR 486 million, which corresponds to 1.8x the adjusted EBITDA for the previous 12 months. Thus, within its financial position, the company is well-positioned for the proposed dividend increase to EUR 0.42 and the refinancing of the hybrid loan taking place in March. Even after these actions, and thanks to the accumulation of cash flow that continues to strengthen with earnings growth, the company estimates it has approximately EUR 300 million in headroom for acquisitions. The financial position already enables the company to make even a large acquisition.

Here is Juho Torati’s analysis of Sanoma after the Q4 results.

Sanoma’s growth drivers through 2026 remain unchanged, however. Sales of Learning’s educational materials are expected to grow in its largest market areas—Poland, Spain, and the Netherlands—driven by curriculum reforms. In Media Finland, digital subscription sales are expected to continue growing faster than the decline in print media, and advertising sales are expected to remain stable. Sanoma also enters the year in a very stable financial position, having successfully improved its profitability and strengthened its balance sheet in 2025, in line with its strategy.

Note:

IR Monitoring is a channel for the corporate partners of SalkunRakentaja and Sijoittaja.fi for background and analytical articles, as well as other interesting investor information. The article is part of a commercial collaboration with the company. The article does not contain investment recommendations.

Sanoma Powers Growth with Learning – In Conversation with CEO Rob Kolkman

Sanoma held a CMD at the end of last year and announced its new financial targets. During the 2026–2030 strategy period, the company aims for growth driven by its Learning business. The opening of Finland’s gambling market to competition will expand the advertising market, and Sanoma aims to capture its share. What does gambling advertising look like from a responsibility perspective? President and CEO Rob Kolkman is interviewed by Mikko Jylhä.

Petri and Mikael chatted about the state of the media industry.

Topics:

00:00 Introduction

00:11 Q4 earnings season for media companies

01:08 Differences in companies’ revenue structures

02:53 Situation and drivers of the Finnish media market

05:03 Deregulation of the gambling market in Finland

06:26 Efficiency gains enabled by AI

08:36 Companies ready for acquisitions

12:51 Otava has increased its stake in Alma Media

14:57 The situation with the unlocking of value in Ilkka

16:27 Valuation outlook for media companies

20:11 Why is Sanoma’s share not pricing in the forecasted earnings growth?

Sanoma has acquired Mr. Chadd, a Dutch tutoring platform, from its founder and other shareholders. Mr. Chadd complements Sanoma’s personalized learning offering for schools beyond its core of printed and digital learning materials by providing integrated digital learning support in line with the Dutch primary and secondary education curriculum. Mr. Chadd’s platform combines AI-based guidance with academically trained coaches, thereby strengthening the link between homework support and classroom work. The acquisition supports Sanoma’s strategy to grow its K12 (primary and secondary education) learning business by, among other things, expanding the product portfolio in existing operating countries and shaping the development of K12 education towards personalized learning.

Mr. Chadd’s net sales were approximately EUR 1 million in 2025. The platform has already been used by more than 140,000 secondary and vocational education students. Mr. Chadd’s founder will continue to work for Sanoma Learning following the acquisition.

Petri has released a new comprehensive report on Sanoma, and like other extensive reports, it is available for everyone to read.

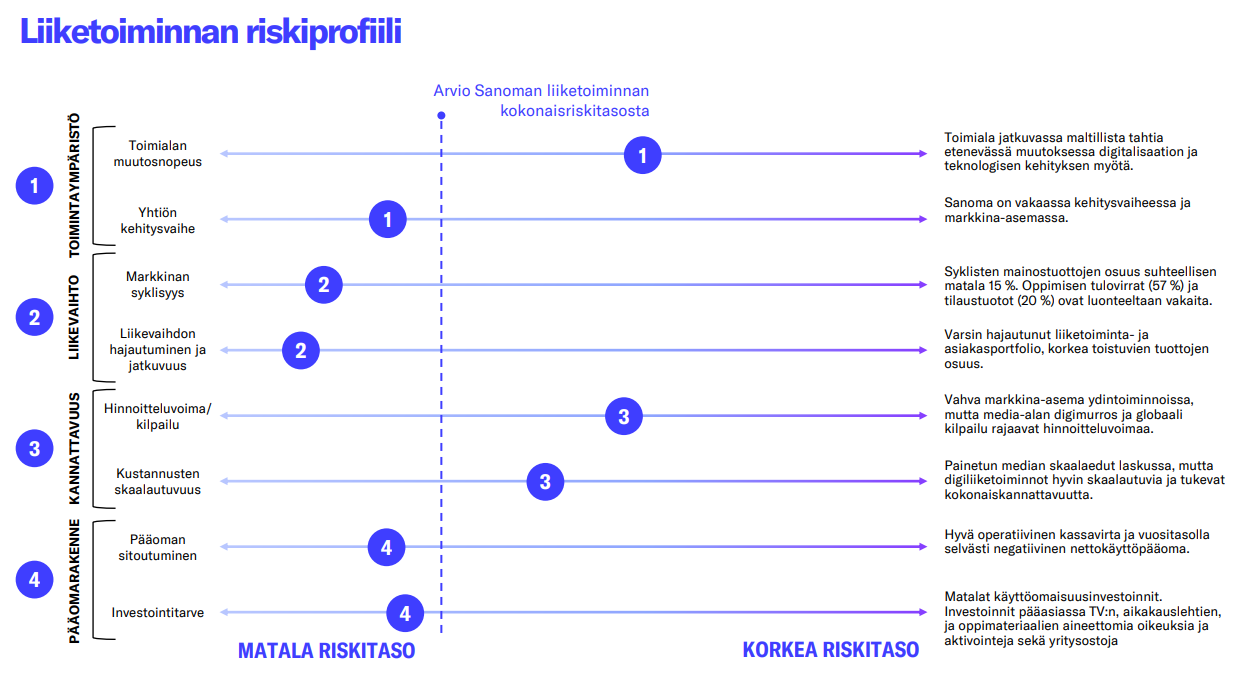

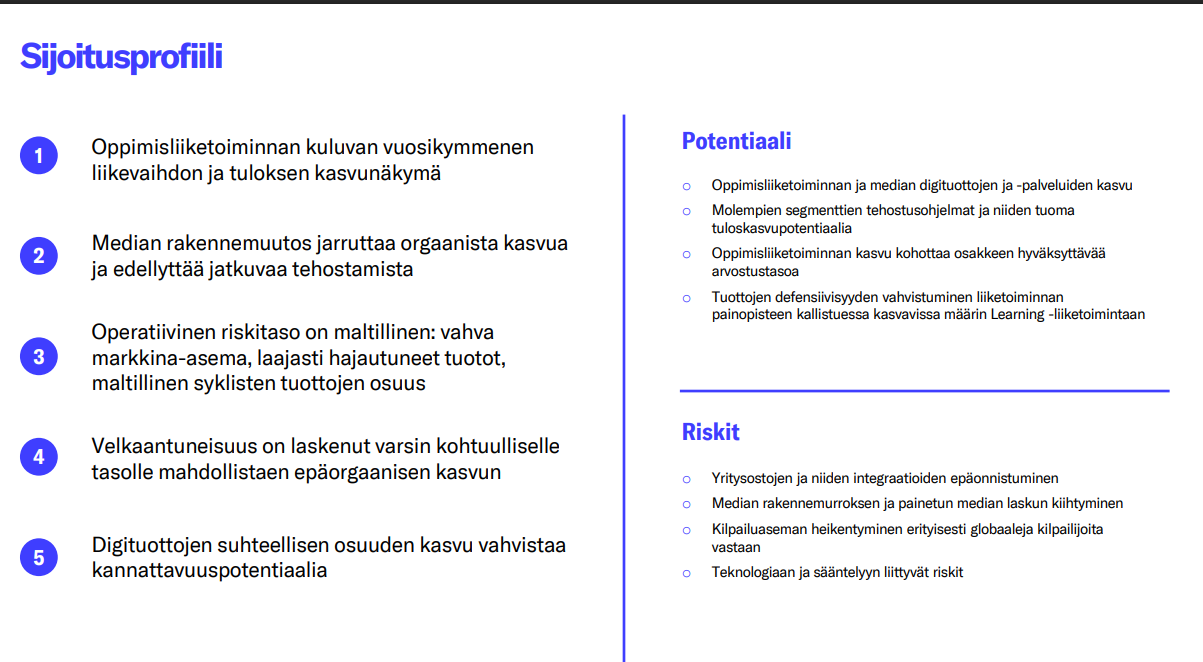

Sanoma’s earnings growth outlook for the coming years is very good, as curriculum reforms are being implemented in the major operating countries of the learning business, which has a strong market position in the European educational materials market, and the segment’s efficiency has increased through operational streamlining. Relative to our estimated earnings growth, the stock is valued quite moderately, which, combined with Sanoma’s moderate risk level, creates a very attractive risk-reward ratio. Thus, we reiterate our Buy recommendation for Sanoma and our target price of 11.5 euros.

Quoted from the report:

Long-term earnings forecasts In our forecasts, Sanoma’s long-term revenue growth is set at 2%. This reflects a 2-5% growing learning business and a stably developing media business. After the profitability improvement in the coming years, we expect a somewhat stable profitability development in the long term in both segments.

Miksu and Petri chatted about Sanoma regarding the extensive report.

Topics:

00:00 Introduction

00:13 Accelerating earnings growth expected

01:13 Learning – predictable and defensive

03:56 M&A strategy

06:00 Media business and advertising market

10:02 Future of the businesses

14:04 Market not pricing in the forecasted earnings growth

Here are Petri’s comments on Sanoma’s recent acquisition.

The Vicens Vives acquisition complements Sanoma’s learning business offering in the Spanish market, where it has a strong foothold thanks to the Santillana acquisitions. Thus, we estimate that this small bolt-on acquisition offers synergy potential and, given the moderate purchase price, we see it as a good capital allocation target. All in all, we believe the acquisition is fully in line with the company’s growth strategy and the valuation of the deal is quite reasonable.

Here are Pete’s pre-match thoughts as Sanoma prepares to release its Q1 report on Thursday.

We forecast the company’s revenue and operational result to be at the same level as the comparison period. The company has guided for operational profit growth for the current year, and with forecasts sitting at the midpoint of the guidance range, expectations are in line with the guidance.

And here are Petri’s quick comments on the Q1 result

Sanoma released its Q1 results this morning, which were slightly better than expected in terms of profitability during the seasonally loss-making first quarter. The company reiterated its guidance for the current year, so we do not anticipate significant upward pressure on our forecasts or the consensus estimates, which are at the midpoint of the guidance range, with the exception of the recent acquisition. Sanoma’s Q1 earnings call starting at 15:00 can be followed via this link.

Petri interviewed Sanoma’s Rob Kolkman regarding Q1

Topics:

00:00 Introduction

00:09 Q1 Highlights

02:06 Profitability improved in Media Finland

03:14 Advertising market remains weak

04:29 Vicens Vives acquisition

05:32 Synergies in acquisitions

06:38 Acquisition philosophy

07:56 The Spanish market is not concentrated