This time there are two people in the episode, Teemu and Heikki. In the episode, Alma Media and Sanoma face off.

Topics:

00:00 Intro 01:35 Sanoma 03:14 Alma Media 07:34 Business and outlook 14:23 Valuations 17:40 Which one do Heikki and Teemu choose for their competition portfolios?

@Petri_Gostowski is providing us with some reading material in honor of Ascension Day.

In our view, the overall picture of Sanoma’s Q1 report is relatively neutral, as the slight beat of our forecasts was, in our estimation, partly due to timing factors in the Learning business. Against this background, we have not made any material changes to our forecasts. The company’s efficiency program is progressing on schedule and thus the overall picture of the expected pace of earnings improvement remains unchanged.

Hi, here I’m talking with David Klett, CEO of Klett Gruppe, one of Sanoma Learning’s European competitors. On the learning side, they only compete in the Netherlands and Finland (Studeo), though.

A publishing peer would be WSOY or Otava, but they aren’t listed. Additionally, the balance sheet includes early childhood education.

Perhaps this might be relevant in the sense that this Klett family company + the family’s consigliere-type family office puts the profits it generates primarily into growth rather than dividends.

David Klett Perfecting family business #negotiator 255

Dr. David Klett reveals well-honed system used by 40+ members of the German Klett family to manage the international book publishing, education and childcare company Klett Gruppe.

00:00 Intro: Secret to family office survival, “death” of publishing, love of Kaurismäki movies in Finland

00:50 Why family businesses are very important and why all ownership cannot be institutional

01:24 Klett Gruppe, 127 years publishing, education, kindergartens from Germany

02:02 Internationalisation and growth. Comparison to Sanoma of Finland

03.28 Four to six generations of family company, 40something members from 3 to 86 year old

04.06 Comparison to “asuntosakeyhtiö” (housing cooperative) apartment ownership structure in Finland, lack of capital in Finland

05:10 The Klett solution to ownership complexity is carefully layered corporate governance

07:30 Silicon chip industry in Asia. Finnish Harry Potter (WSOY) share the Thai artwork (Nanmeebooks)

08:47 Overcoming challenges, “Families are not built to decide stuff”

09:57 The Family Council of 5 takes care of the family

11:56 Board of Directors / Supervisory Board

13:00 Management Board

13:40 Checks for nepotism vs. family ownership education

16:09 Top level executive qualifications are very strict

19:50 Time limits for positions

21:20 Managing the international subsidiaries under four silos

22:07 Paradox of survival. Managing acquisitions and exits. Studeo. SAP’s failed acquisition of Qualtrix of USA

25:30 Selling to Private equity is not for Klett Gruppe which aims for long-term ownership

28:18 Family office does not need to hold financial assets. Living off dividends is not encouraged

30:40 Tackling political risk. Problems of high inheritance tax in Finland

34:00 Finnish pension system replaces private ownership capital

35:05 Good ownership skills are more important than inheriting wealth

36:49 #negotiator insider episode: Kaurismäki movies, high quality chainsaws and the secret ingredient of family office survival

Lately, I’ve been buying several small batches of Sanoma. The latest one today. The stock doesn’t seem to interest the members of this forum very much. On the other hand, going through this thread, I noticed similar wondering already two years ago, when there could be a couple of months’ gap between messages. Well, the ticker doesn’t seem to interest many others either; trading days often pass with low volume as the share price slowly drifts down.

The textbook business probably isn’t quite as hot an industry among investors as AI plays. Regarding the media side, quite a few people probably hope the whole business would be dumped the hell out into its own company.

Personally, what interests me most in Sanoma, in a “for the love of the game” spirit, is the media business, even though it’s obviously clear that its importance in revenue and especially operating profit will decrease even further. Still, I wonder if we might see major moves from Sanoma in that field as well, in the same spirit as the acquisitions of regional newspapers from Alma years ago. Although instead of newspapers, the target would be MTV and the seller Telia. The idea feels crazy at first glance, of course, when talking about a company that makes around twenty million in losses annually—year after year. But the idea, of course, would be to reduce competition and adapt operations to fit the modern world. One could imagine that such a deal would also be beneficial in strengthening the position of the streaming service.

Just some thoughts like these. Not very groundbreaking, but at least I managed to bump the thread.

I follow the situation closely, and unfortunately, this deal would not pass the competition authorities. There was a similar case in France when two major channels, which are very comparable in terms of market position to MTV and Nelonen, attempted a merger, but it was blocked:

Jorma Sairanen, who has served as the head of programming for both Maikkari and Nelonen, was at least of a very different opinion regarding the attitude of the competition authorities (paywall):

Of course, that is just Sairanen’s opinion, and he is a top professional in programming acquisition, not law.

And of course, those acquisition targets can also be split up. It seems clear that there isn’t exactly a queue of buyers for Maikkari, and Telia likely doesn’t want to remain the owner for long. Similarly, it seems clear that if a commercial channel is required to have, for example, its own news content (read: expensive production), Sanoma is likely the only player with the possibility to produce content with decent quality and at a realistic cost level.

Petri’s preview as Sanoma releases its Q2 report on Wednesday.

Sanoma will release its Q2 report on Wednesday at approximately 08:30. Due to the strong seasonality of the Learning business, the second quarter is typically the company’s second-best quarter of the year in terms of performance. Q2’24 earnings forecasts are roughly on par with the comparison period, and the company is also expected to reiterate its guidance for the current year.

Sanoma released its Q2 report this morning, which was slightly better than expected across the board. Sanoma also reiterated its guidance for the current year, as expected. Sanoma’s results briefing starting at 11:00 can be followed on inderesTV via this link.

This new composition by Peter Tsaykovski is quite good:

I would have refined the dramatic arc a bit, in the sense that the target price could have been raised slightly as the grand finale. But we’ll roll with this.

I’m putting my spare cash into Sanoma because of their digital learning materials.

They are user-friendly and, best of all, teachers—who are notoriously slow to change—have grown accustomed to using them. In my experience, they are used willingly and extensively.

And Sanoma receives fair compensation for them.

As this pattern repeats across Europe, I definitely want to be part of this.

The only concern is the stock’s practically non-existent trading volume. It seems the major shareholders don’t really sell their positions, so even buying or selling a modest amount has a significant impact on the share price.

Couldn’t that also be seen as an opportunity? As you mentioned, because of the non-existent trading volume, the price sometimes makes sharp moves that are nice to take advantage of in trading. Just set a low-ball limit order nice and low and give the order a longer validity period.

This long-pending lawsuit has now come to a conclusion – everything related to it has been recorded and paid, so it has no impact on forecasts. Of course, a different outcome would have been more desirable, as it involved a significant sum.

Sanoma will release its Q3 report on Thursday, and here are Petri’s preview comments regarding it.

Due to the strong seasonality of the learning business, the third quarter is the most important quarter of the year for the company in terms of earnings. Q3’24 earnings forecasts are below the comparison period, reflecting the timing of curriculum reforms. Consensus estimates for the current year are at the upper end of the provided earnings guidance, so a revision of the earnings guidance range would not be surprising.

Here is the company report on Sanoma made by Petri after Q3.

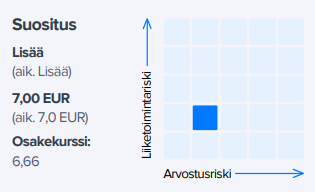

Sanoma announced Q3 figures on Wednesday that were better than our expectations, with the profitability of both segments exceeding our forecasts. Although the most significant earnings improvement from the learning business efficiency program will have to wait until 2026, decreased investments, among other things, have already strengthened cash flow and show that the program is taking hold. This strengthens confidence in the earnings improvement program, as the greatest benefits are naturally ahead when the learning business returns to growth in 2026. Relative to this, the stock is moderately priced, so we reiterate our Accumulate recommendation and raise our target price to EUR 8.0 as the earnings improvement progresses on the expected track (prev. EUR 7.0).

Quoted from the report:

Operating cash flow has strengthened

At the end of Q3, Sanoma’s operating cash flow strengthened to EUR 104 million (Q1-Q3’23 EUR 66 million), and after organic investments and IFRS16 repayments, free cash flow was EUR 53 million (end of Q3’23 EUR 46 million). Consequently, the company’s net debt at the end of Q3 was EUR 616 million (excl. EUR 150 million hybrid), and the leverage calculated from it (Q3’24 2.4x LTM adj. EBITDA) is clearly at the target level of < 3x. Thus, the balance sheet position already enables small bolt-on acquisitions in the short term.

Here are Petri’s pre-analysis in the form of a company report.

Reflecting the strong seasonality of the learning business, Sanoma’s Q4 figures hold no major surprises. Attention is mainly focused on the current year’s guidance, for which, in our opinion, the risks are skewed downwards based on consensus estimates. With the share price increase, the stock’s valuation is, in our opinion, neutral on a 12-month horizon. Considering this and the risk associated with consensus estimates, we take a more cautious stance on the stock, although we still see good return potential in the stock over a slightly longer horizon.