These comments are certainly pleasant to read. The Lemonade bears on the forum clearly know the insurance industry well.

First, I state: If one could read the potential of the best future companies from 10K reports or income statements, as these experts do, there would not be a single accountant practicing their profession in the world. They would all be investors, even multi-millionaires.

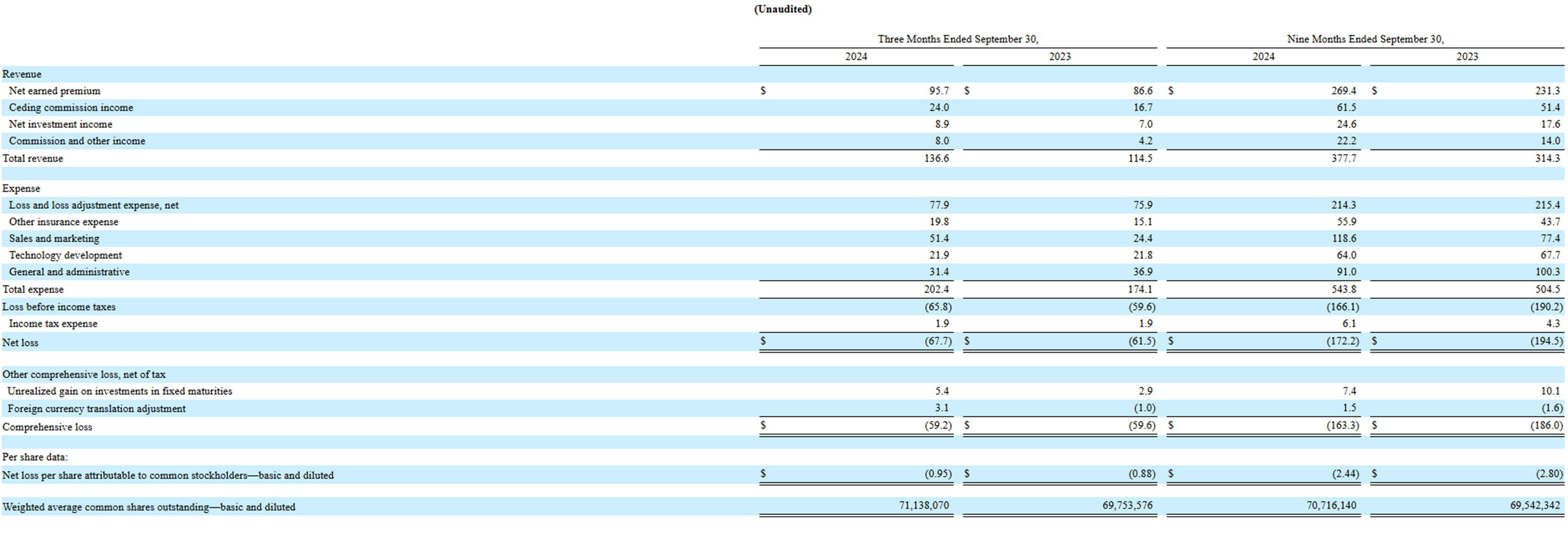

Yes, the Combined Ratio is in the gutter. Yes, the company is making a lot of losses. Yes, the company’s expenses are far too high compared to current revenues. Yes, the company’s book value has been constantly decreasing – of course, because they are making losses.

But what happens when we fast forward a few years in this story? What happens when expenses barely grow at all? What happens when auto insurance gains momentum and the company finally starts receiving so-called big money alongside Renters and Pet insurance? What happens when the book value starts to grow? Slowly at first, then quickly? What happens when customer acquisition costs are paid back to GC in 2-3 years and GC exits the equation?

One commenter, apparently an insurance industry employee, stated here that “Lemonade is chuckled at in our workplace when the company comes up.”

Do you chuckle in the same way that Amazon was chuckled at in 1997?

Or how Microsoft’s Ballmer chuckled at the iPhone in 2007?

Or perhaps like Blockbuster chuckled at Netflix in 2000?

Or how hotel bosses laughed at Airbnb in 2017?

GM’s boss laughed at Tesla.

There are many other examples.

Next, you will surely state that “the insurance industry does not work like your examples, e.g., due to capital restrictions.” Until it does, because the company invents creative arrangements for this, such as Synthetic Agents.

What unites all these examples of mine? None of these products or services were created by industry veterans. They all faced belittlement and truly bloated and overwhelming balance sheets. They were all told that “competitors can easily kill the disruptor’s business with their balance sheets, and if there was anything special about them, they would have already been bought out.”

Why didn’t Blockbuster buy Netflix? Why didn’t Yahoo buy Facebook for “peanuts” when the opportunity was offered? How could Kodak, with its massive balance sheet, drive so thoroughly into a wall?

The reason is obvious: The leadership of these companies consists of individuals who do not share the same vision and understanding of where the world is going as the founders of the disruptors. Old dinosaurs are forced every quarter to maximize dividend yields for their owners. Owners who are not interested in innovation, but in everything remaining the same. These leaders receive tens of millions in annual income for not taking risks, because risks quickly reduce EPS. The difference is obvious when one looks at, for example, what Mark Zuckerberg did at the helm of Meta. He invested massively in the future in 2022. The industry’s best analysts declared the company’s story to be nearing its end. And what’s more.

In the US, a large portion of insurance is still sold by insurance brokers, and companies’ business models are built around using brokers. What do you think, do these brokers have the enthusiasm to innovate their industry towards automation and AI? When a company is developed to meet the needs of the modern world, it won’t succeed unless the company’s personnel offer a DNA match for development. Innovation is shunned and its progress is hindered.

And what do you think, do Gen Z and young millennials want to interact with insurance brokers by phone or email? They don’t even want to call their friends or family members? If these giants cannot offer a seamless digital experience, they are doomed as insurance providers, not quickly due to their massive balance sheets, but gradually.

“But they can drive Lemonade out of the game by lowering prices and even making losses,” some have sometimes said. Firstly, selling insurance intentionally at a loss is, to my understanding, illegal at least in the US? Secondly, and even more importantly, it is crucial to understand that the younger generation will not switch to their father’s or grandfather’s insurance company, even if it offers a cheaper product, if the brand does not appeal or the user experience is clunky and old-fashioned.

Ajit Jain of Berkshire Hathaway, responsible for Geico’s business, stated at BH’s 2023 annual meeting that Geico has 600 different systems that do not communicate with each other.

And he continued: "We’re trying to compress them to no more than 15, 16 systems that all talk to each other. That’s a monumental challenge, and because of that, even though we have made improvements in telematics, we still have a long way to go because of technology.”

“Because of that, and because of the whole issue more broadly in terms of matching rate to risk, GEICO is still a work in progress.”

Such problems are not solved with “AI.” The advantage for a player like Lemonade, which has built its entire existence on AI and automation, is obvious. And what’s more, on ITS OWN system. They are not dependent on a third party. I believe that large insurance giants buy these services externally.

It is also good to note that from 2022-2024, we experienced the wildest inflation of our generation. This has not made Lemonade’s journey easier, and they bit off too big a chunk in the aforementioned operating environment in the field of home insurance.

Large insurance giants have made losses on their insurance business in recent years. This is certainly due to the inflation situation. Profits have been made through investment activities. For Geico, this happened in 2022. For State Farm, at least in 2022-2023.

Whether Lemonade succeeds remains to be seen, but from an investment perspective, I recommend gentlemen/ladies to look at much more than just the income statement and book value in companies. Otherwise, you might miss out on the best investment stories.

Of course, if the investment strategy is safer and based, for example, on stable dividend payers, then that’s another matter.