Now that we’ve gained momentum, let’s start a thread for this as well.

Hippo Insurance operates in the insurance sector, focusing on home insurance. Hippo focuses on a fast and easy insurance process and can provide a home insurance quote in minutes. Home insurance policies are tailored to customers’ individual needs, and coverage is often better than with traditional providers, for example, regarding home electronics. Hippo utilizes smart devices and home sensor systems to reduce risks. For example, customers are offered leak detectors or other similar home security devices that help prevent damages and reduce the insurance company’s risks.

I would also like to point out that the company has approximately 545M USD in cash, and its market value is approximately 665M USD. If the company’s statements about turning net income positive prove true, there is significant upside potential here.

Let me also add that after Q3, the company sold a significant portion of its ownership in First Connect Insurance Service to Centana Growth Partners for 48 million, and that purchase price includes the possibility of an additional 12 million if targets are met.

Regarding the proceeds from this, the company commented in a letter to shareholders as follows

" The proceeds from the transaction further strengthen our cash position, and we have taken this as an nopportunity to repurchase and retire some of our own shares"

Q4 Revenue up 58% YoY to $102 million; FY2024 Revenue up 77% to $372 million

Pro-forma for the First Connect transaction, Consolidated TGP up 16% YoY, driven by Insurance-as-a-Service (“Iaas”) which grew 22%

Continued Improvement of HHIP Loss Ratio

HHIP Q4 gross Loss Ratio improved 3pp YoY to 50%, with HHIP non-PCS loss ratio at 43%, and HHIP PCS loss ratio at 7%

HHIP FY2024 Gross Loss Ratio improved 28pp to 73%

HHIP Net Loss Ratio improved 46pp YoY to 60%

Significant Step Forward on our Path to Profitability

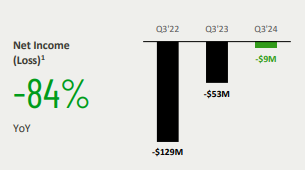

Q4 Net Income attributable to Hippo of positive $44 million, vs. Net Loss of $42 million in Q4 of last year; Gain on Sale of First Connect contributed $46m

Q4 adjusted EBITDA of positive $8.5 million vs. Adjusted EBITDA loss of $22 million in Q4 of last year

Q1 revenue up 30% YoY to $110m

IaaS revenue grew 91% YoY driven by higher gross earned premium and higher premium retention

HHIP revenue grew by 12% YoY driven by higher premium retention offset by lower gross earned premium

Loss Ratios Higher YoY, driven by the LA wildfires

HHIP Gross Loss Ratio of 121%, a 41pp increase YoY; LA wildfires contributed 56pp

HHIP non-PCS loss ratio of 53%, a 6pp improvement YoY

HHIP PCS loss ratio of 68%, LA wildfires contributed 56pp

Consolidated Net Loss Ratio of 106%, LA wildfires contributed 51pp

Improving Operating Leverage

Investments in operational efficiencies continued to pay off as fixed expenses (S&M, T&D, and G&A) declined by $7m while revenue increased by $25m YoY, resulting in an 18pp decrease YoY in these costs as a percentage of revenue, from 48% of revenue in Q1’24 to 30% in Q1’25

Underlying improvement in profitability masked by impact of LA wildfires

Q1 Net Loss attributable to Hippo increased YoY by $12m to $48m; LA wildfires contributed $45m2

Q1 adjusted EBITDA loss increased $21m to $41m; LA wildfires contributed $45m2

Financial Strength

Cash and investments, excluding restricted cash, decreased $42m QoQ to $528m; decrease was mostly related to losses from LA wildfires

Spinnaker surplus of $198m

Signed an agreement to raise a $50m surplus note; pending regulatory approval, expected to close in Q2’25

Gross Written Premium up 16% YoY to $299m, driven by organic growth in existing and new hybrid fronting programs launched

Revenue grew 31% YoY to $117m, driven by an increase in gross earned premium and higher premium retention

A Step-Change in Net Loss Ratio

Consolidated Net Loss Ratio of 47%, a 46pp improvement YoY, powered by underwriting and rate actions, better claims operations, and favorable reserve releases

HHIP net loss ratio of 55%, a 58pp YoY improvement, driven by better gross loss ratio

HHIP non-PCS loss ratio of 42%, a 28pp improvement YoY; PCS loss ratio at 13%, a 30pp improvement YoY, boosted 7pp by favorable reserve releases Continued Operating Leverage Improvement

Fixed expenses (S&M, T&D, G&A) declined by $6m YoY as revenue increased by $28m, reflecting continued improvement in operational efficiencies

These costs decreased as a percentage of revenue by 16pp YoY from 46% in Q2’24 to 30% in Q2’25

Significant Gain in Profitability Metrics

Net Income attributable to Hippo of $1m compared to Net Loss of $40m in Q2 of last year

Adjusted Net Income of $17m compared to Adjusted Net Loss of $20m in Q2 of last year

Financial Strength

Cash and investments, excluding restricted cash, increased $76m QoQ to $604m; increase was mostly related to the issuance of a $50m surplus note

Spinnaker surplus of $223m, up from $202m a year ago