I finally jumped in with a small initial investment – I would have liked to buy around the recent lows but my cash situation didn’t allow it. The intention is to gradually add more once the next quarterly reports come out and I see how things develop.

The biggest reasons for the acquisition were that the numbers look relatively promising and the valuation has moderated considerably.

Additionally, I’ve been doing a bit of a “Lynchian” approach, researching product reviews and talking to acquaintances who have bought these products. These discussions further strengthened my impression that the price-quality ratio of the products is almost incredibly good, and that alone will surely get them far. I’ve been disappointed lately with the quality of many larger, and more expensive, brands like Northface and Fjällräven, especially in clothing, so I believe RevolutionRace still has plenty of room to grow and gain market share.

How on earth can one be disappointed with Fjällräven’s quality? At least based on my own experience with gear and clothing acquired for hiking, they are more durable and exceptionally well-designed garments that haven’t changed at all over years of use. I understand if one is disappointed with the price, but cheap and good rarely come in the same package. I don’t blame Revolution for having any flaws, as I have no experience with them.

Yep - I’ve been a little surprised by this myself. The “Fjäll” equipment (including tents and a couple of backpacks) is truly top-notch, and they’ve also invested in environmental friendliness, which I give them a plus for.

In terms of clothing, I’ve had a couple of experiences recently where the quality might not have been at the level of previous years - though, of course, I might have simply gotten a lemon.

For example, my hiking pants started to fall apart in a few places after only a couple of years of use (and we’re definitely not talking about heavy use). When we’re talking about prices that are 2-3 times those of comparable Revolution products (which also get a lot of praise for their quality), I think that for the “average outdoors person,” these will sell well in core markets, probably at the expense of more expensive brands - especially outside of those loyal to Fjällräven and similar brands.

EDIT: I’m not suggesting here that any specific other brand is bad. But is RevolutionRace’s price-quality ratio good enough that I believe they can achieve sales growth in a competitive market? Absolutely.

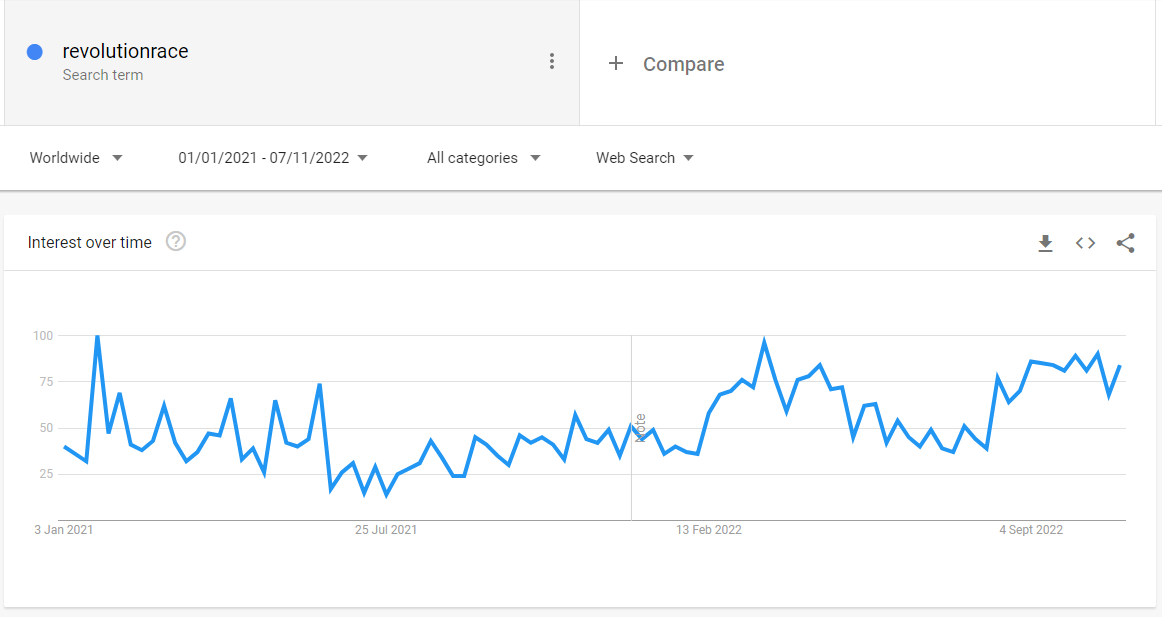

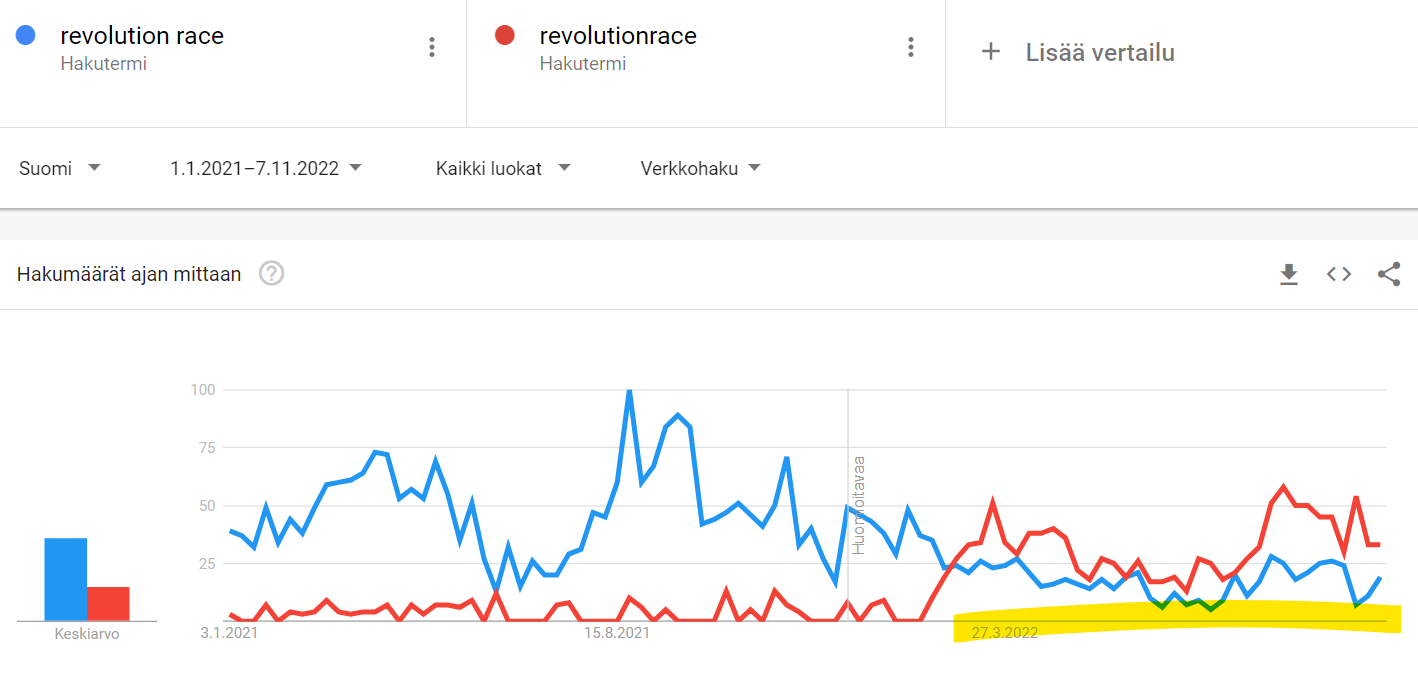

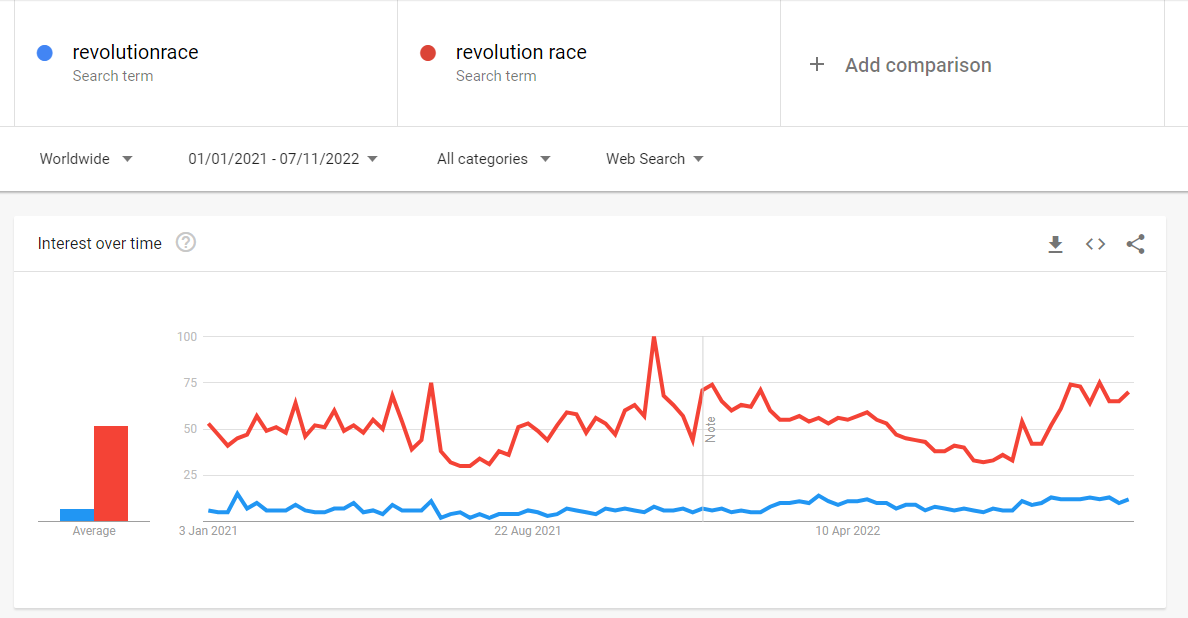

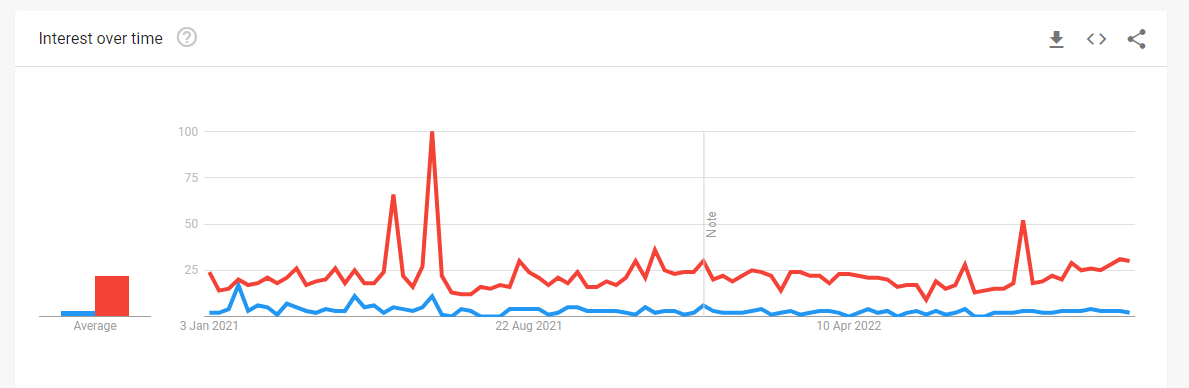

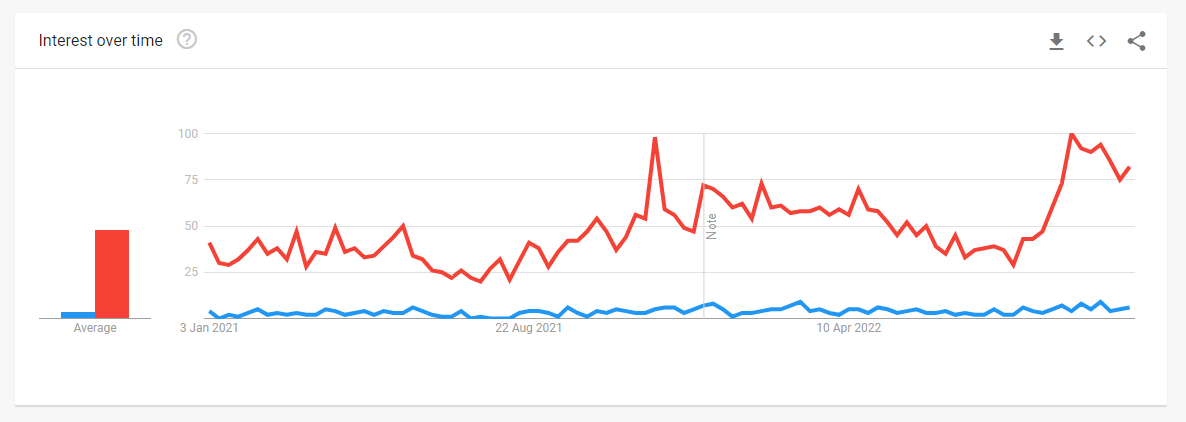

I’ve been following RevolutionRace’s search volumes on Google Trends, which I believe gives good indications of the e-commerce operator’s attractiveness and search volumes. According to the trend, RevolutionRace’s search volumes have also grown significantly in Q3 vs last year:

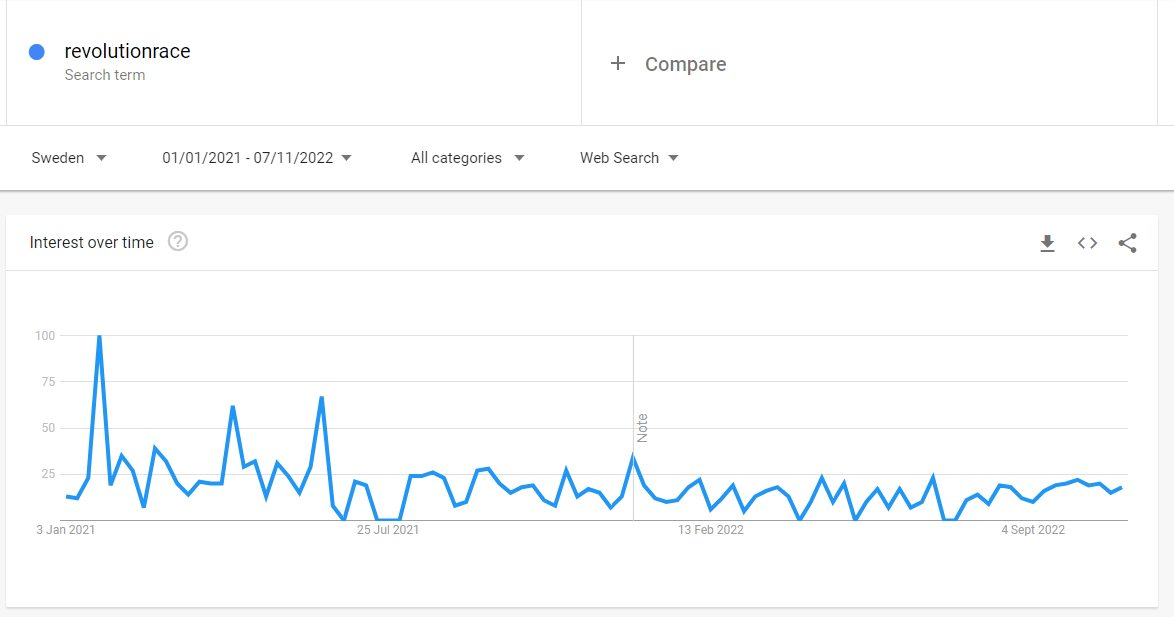

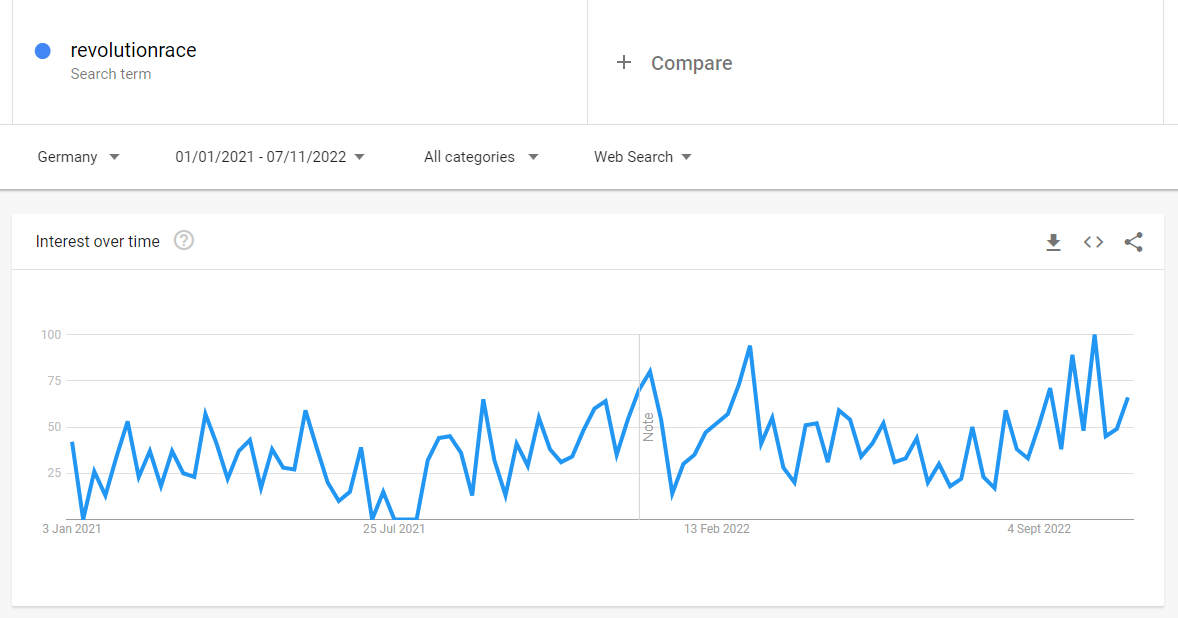

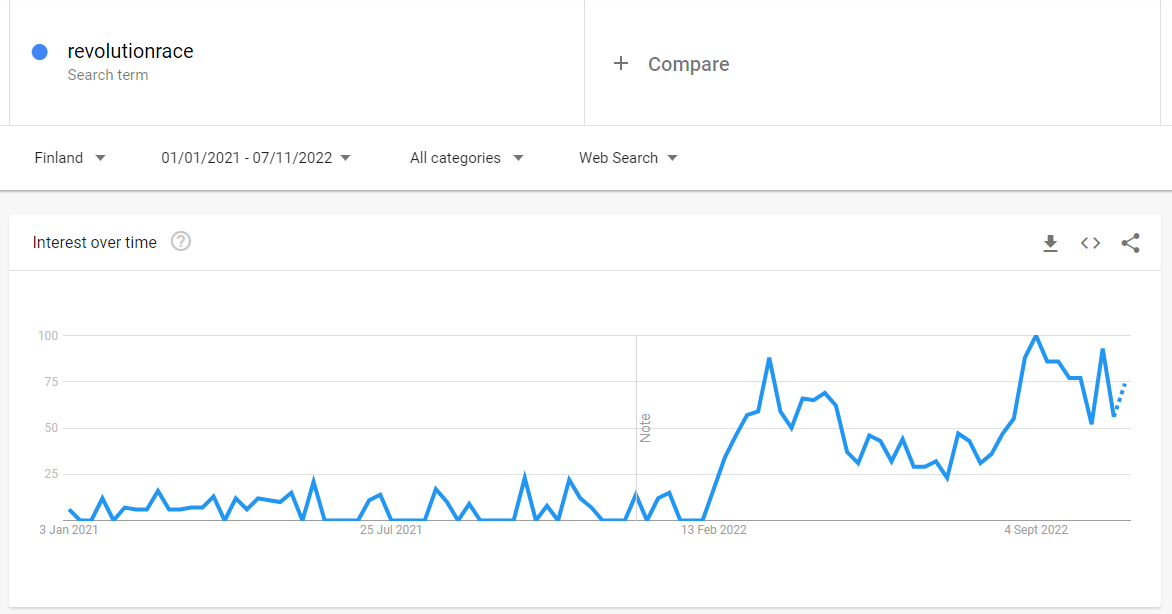

Google Trends provides interesting graphs. It’s hard to say how to interpret them, as the search term “revolutionrace” is on the rise in Finland this year, but “revolution race” is declining:

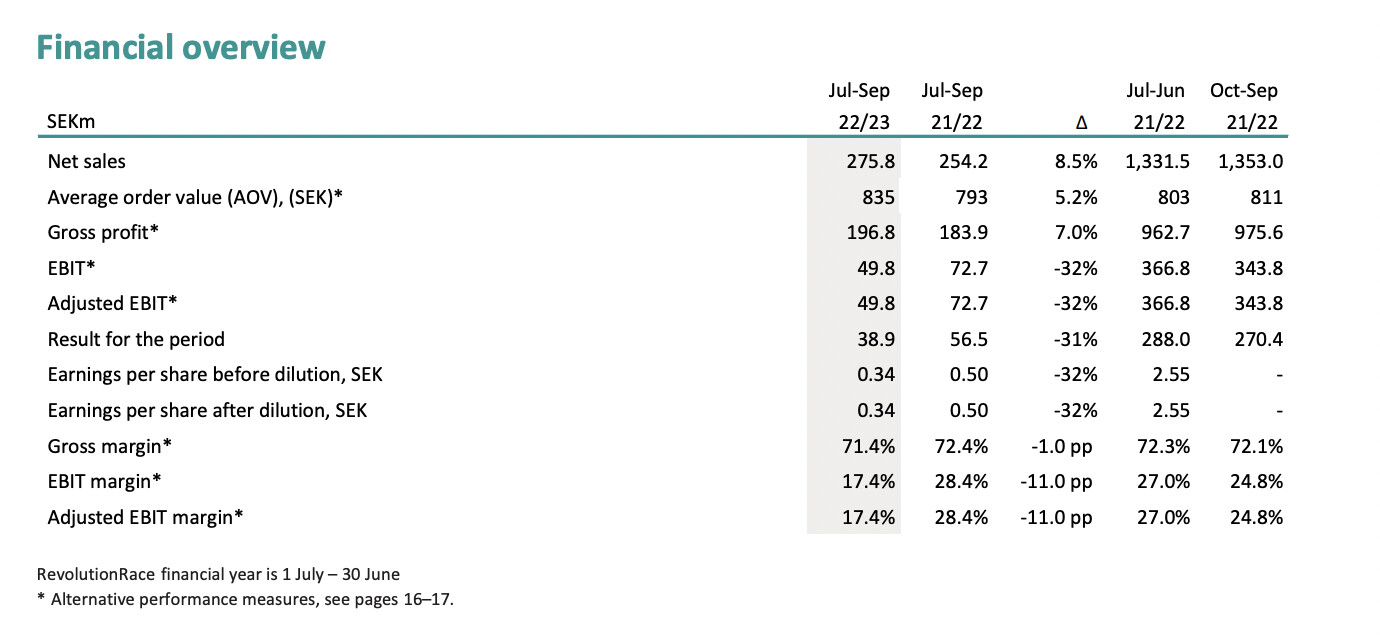

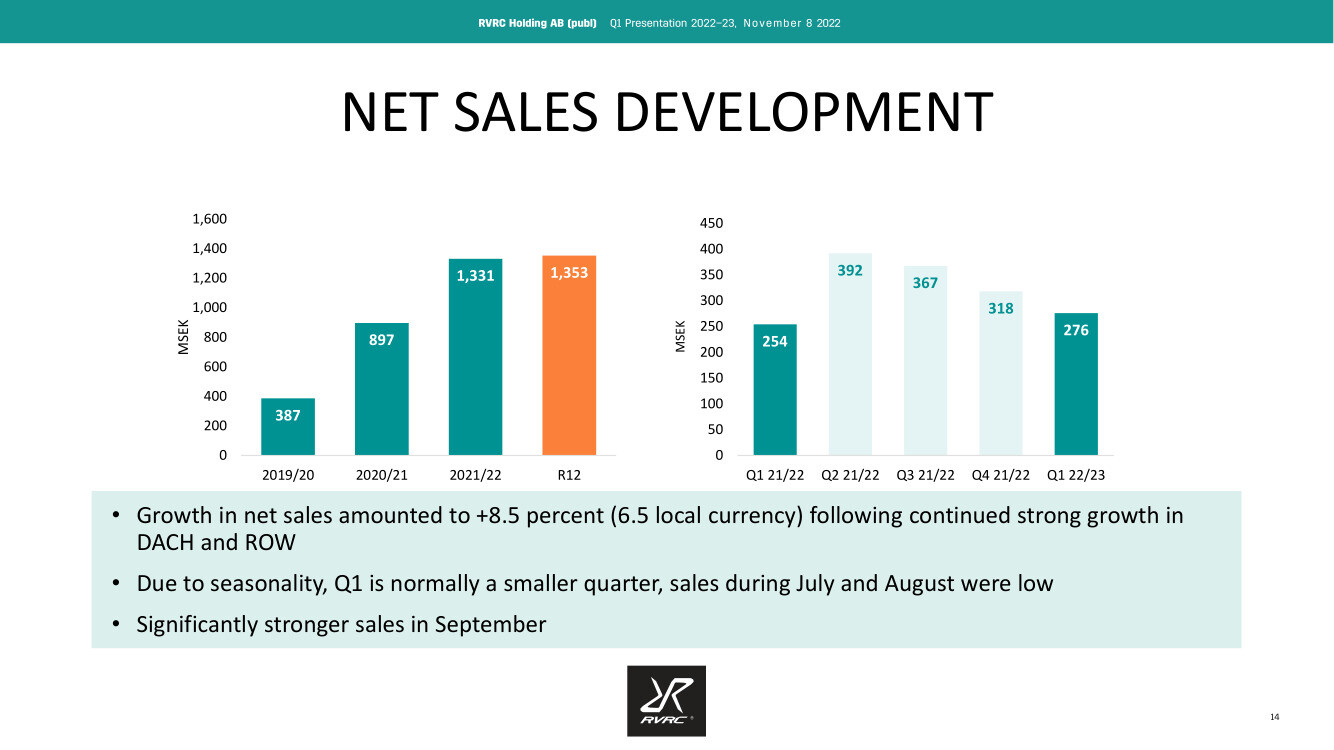

Following the weak sales in July and August, we saw a

clearly improved sales trend in September and October,

which was more in line with our plan. During September,

when sales volumes were higher than July and August, the

underlying EBIT margin was also in line with the long-term

profitability target.

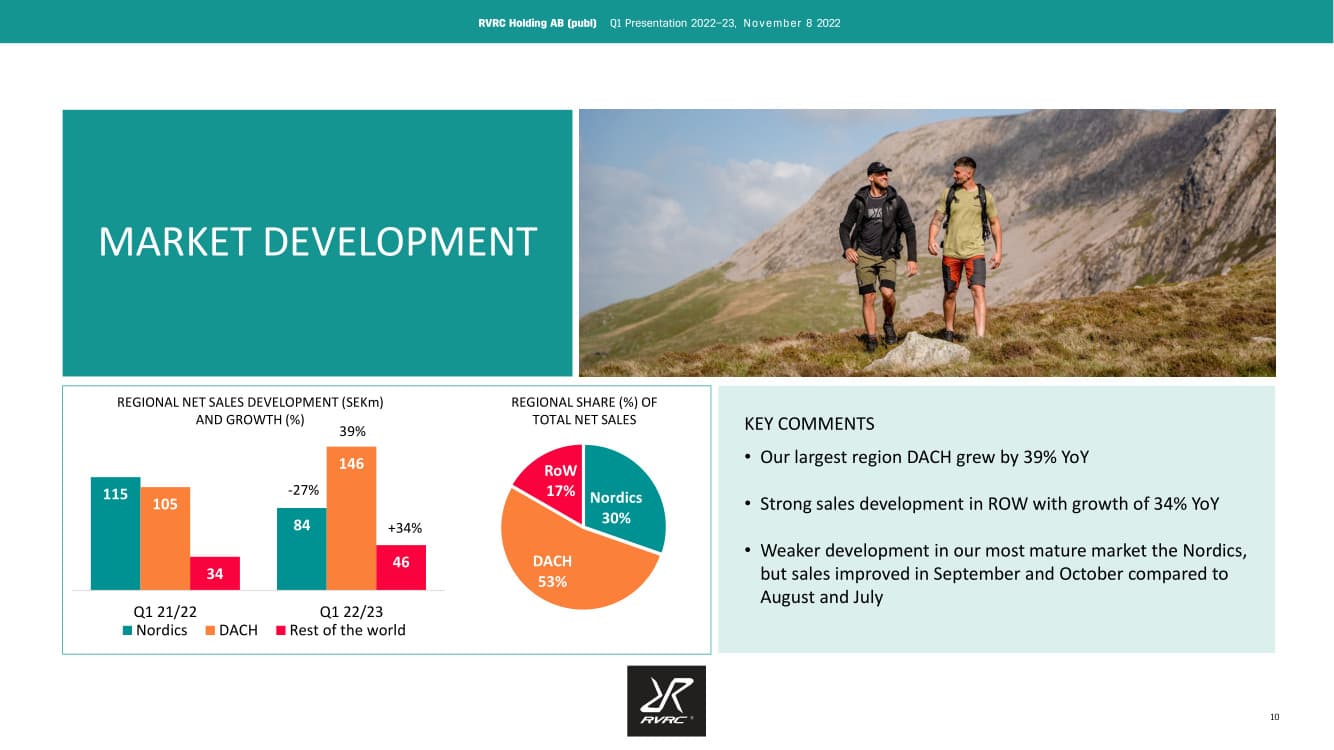

Online sales of outdoor gear are surprisingly sensitive. Within a weak quarter, I believe there are both super successes and failures. In the Nordics, with their poor purchasing power, consumers have clearly cut back on spending, and sales dropped by as much as 29 percent. At the same time, German-speaking Europe grew by an impressive 39 percent, and the rest of the world by 34 percent. The DACH region already accounts for over half of sales. It has been communicated earlier that sales, for example, to Germany are more profitable than to the Nordics due to lower VAT.

However, profitability had taken a severe hit. Apparently, sales growth has been achieved through more aggressive marketing than before, and of course, also through discount sales that continued throughout the quarter.

Based on the number of reviews, the youth collection has not taken off as I would have expected. Instead, people are not yet willing to compromise on dog clothing, and these have been reviewed at a furious pace. Hopefully, customers are adding other items to their shopping carts, as those pet fleeces are quite affordable.

Now we are facing a really tough quarter, and it is certainly encouraging that sales have been good in October. Perhaps Central Europe will continue its momentum and generate growth. The importance of the Nordics is already smaller. There is a slight fear that the sluggish sales in the Nordics are due not only to a decrease in purchasing power but also to brand burnout.

I’m left with slightly mixed feelings about this; here are my thoughts:

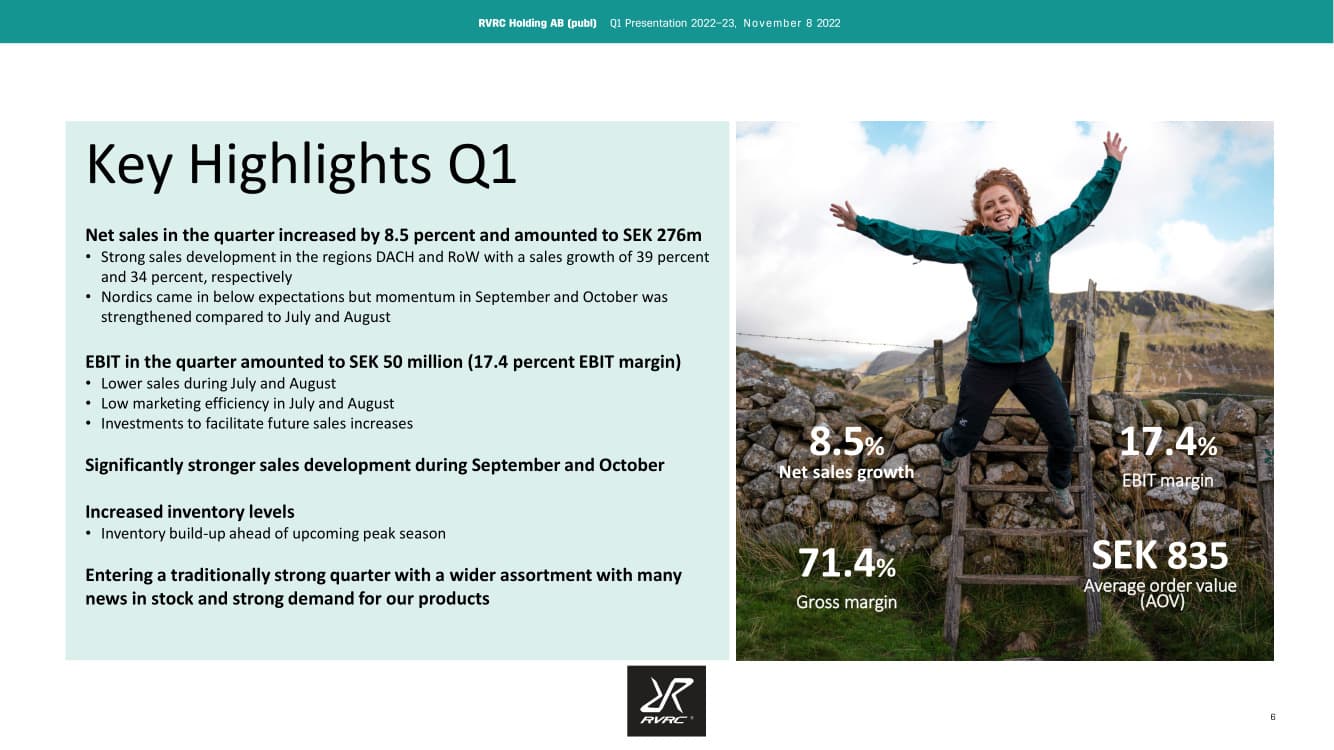

On one hand, sales grew from a year ago, and the average purchase size also increased nicely (+5%), but at the same time, EBIT dropped quite sharply. It’s also a plus that DACH and rest of the world sales grew.

The underperformance in Nordics sales is regrettable.

The company has relatively little history so far, making it a bit difficult to assess the seasonality of sales. Sales (and EBIT) have now decreased for four consecutive quarters, even though sales grew compared to the year-ago period.

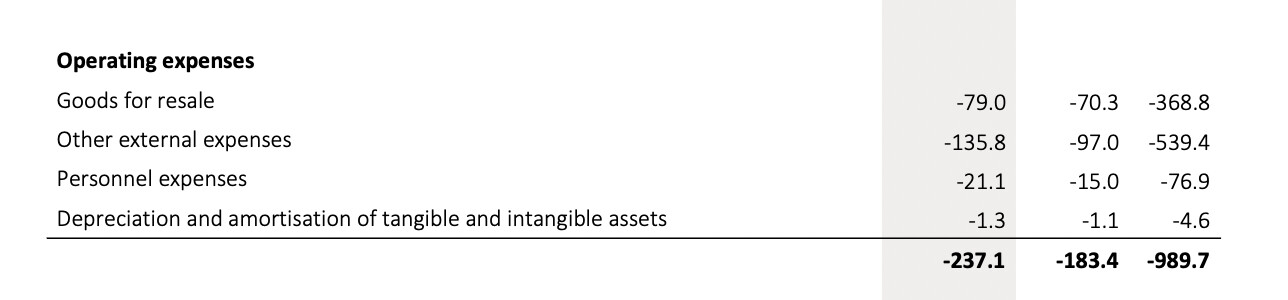

Of course, personnel has also increased by about 30% from a year ago (although salary costs didn’t grow massively), and rising logistics costs have probably also eroded this, but overall, costs have increased most in the “other external expenses” category. This probably includes logistics costs, but perhaps marketing also falls under this, meaning perhaps too much was invested there relative to how much it yielded.

Discounts weren’t directly mentioned there, but based on previous discussions, etc., they have probably been used a bit too aggressively.

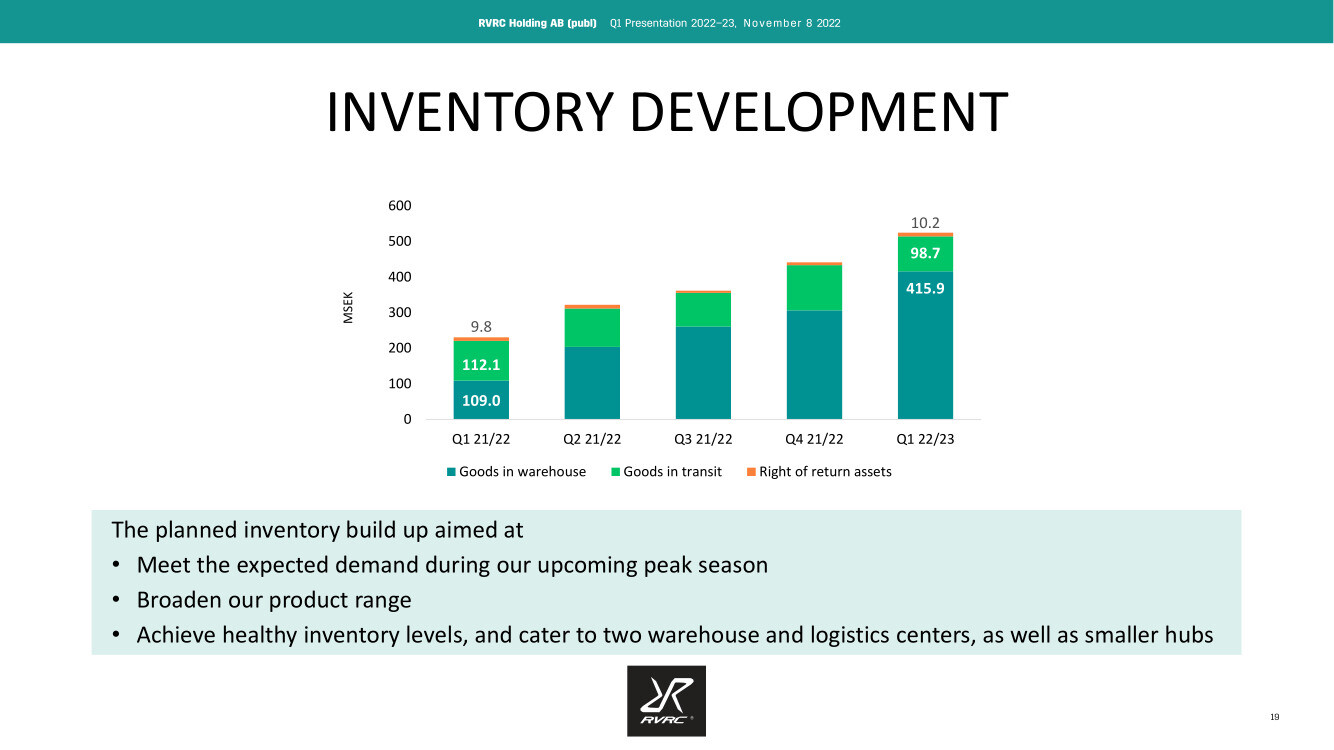

However, it was commented that things are improving and inventory has been increased. We’ll see how things progress, but it will be interesting to see the market reaction today.

Also, the cash balance has diminished quite rapidly in a year, by about 50%! Of course, the majority of that is probably tied up in inventory, and a substantial credit line has been agreed with banks, so the situation is not catastrophic yet, but this still needs to be monitored.

Picked from page 6 of the report (my bolding):

Financial position

Net debt amounted to SEK 24.9 (-47.4) million, mainly driven by cash flow from financing activities. Cash and cash equivalents amounted to SEK 142.1 (281.7) million. The interest-bearing debt of SEK 167.0 (234.3) consist of lease liabilities of SEK 7.7 (5.8) million and liabilities to credit institutions of SEK 159.3 (228.5) million in the form of a utilized bank overdraft which is within the framework of the group’s credit facility. The group’s total credit facility amounts to approximately SEK 600 million.

The conference call convinced investors quite well, and the sharp morning decline has eased into a gentle upward slope. The call also answered the issues raised by @PeeJii very well. It was also strongly emphasized that after a sluggish summer, performance has been “more in line” from September onwards, both in terms of profitability and sales.

The quality of calls has improved a lot, but Flik still has room for sales here.

November and December seem to be RevolutionRace’s best sales months. Hopefully, the ads are now targeted correctly, and consumers have enough faith in their own finances.

Philipp Lahm as a prominent brand ambassador for the German market. I don’t know what his image has been like since his career ended? Is he, for example, outdoorsy in some way?

At a quick glance, the results look a bit weaker and cash is starting to run low, as there is quite a lot of inventory. The ratio of current assets to current liabilities is a bit worrying (Assets approx. 130M and liabilities 314M). Generally speaking, the sportswear business is not exactly a gold mine in the long run, as it ties up a relatively large amount of capital in inventory, and products from the previous season often tend to get left in stock and then have to be sold at a discount. My own experience is, of course, more from the retail side, rather than the clothing manufacturer/brand owner side.

I have some experience with the company in that we ordered a couple of pairs of pants for my wife and oldest daughter. They all ended up being returned, though, as the fits were somehow strange.

At an earnings level of 2 SEK/share, the P/E would be around 16, so it’s not particularly expensive if they stay on the growth path and manage to maintain/improve their margins.

Cash flowed nicely into the coffers in the past quarter, and inventory levels have been reduced. Cash was decreased by paid dividends and taxes. Sales growth was good, but profitability weakened. More investment in marketing has been required to drive sales growth, but it seems the accuracy of sales-boosting marketing has improved since the late summer quarter, and business has been brisk. The CEO pointed out that sales had increased particularly in Austria, Switzerland, the Netherlands, Denmark, and Poland. These are quite good markets for growth. The share of brand marketing has increased compared to before.

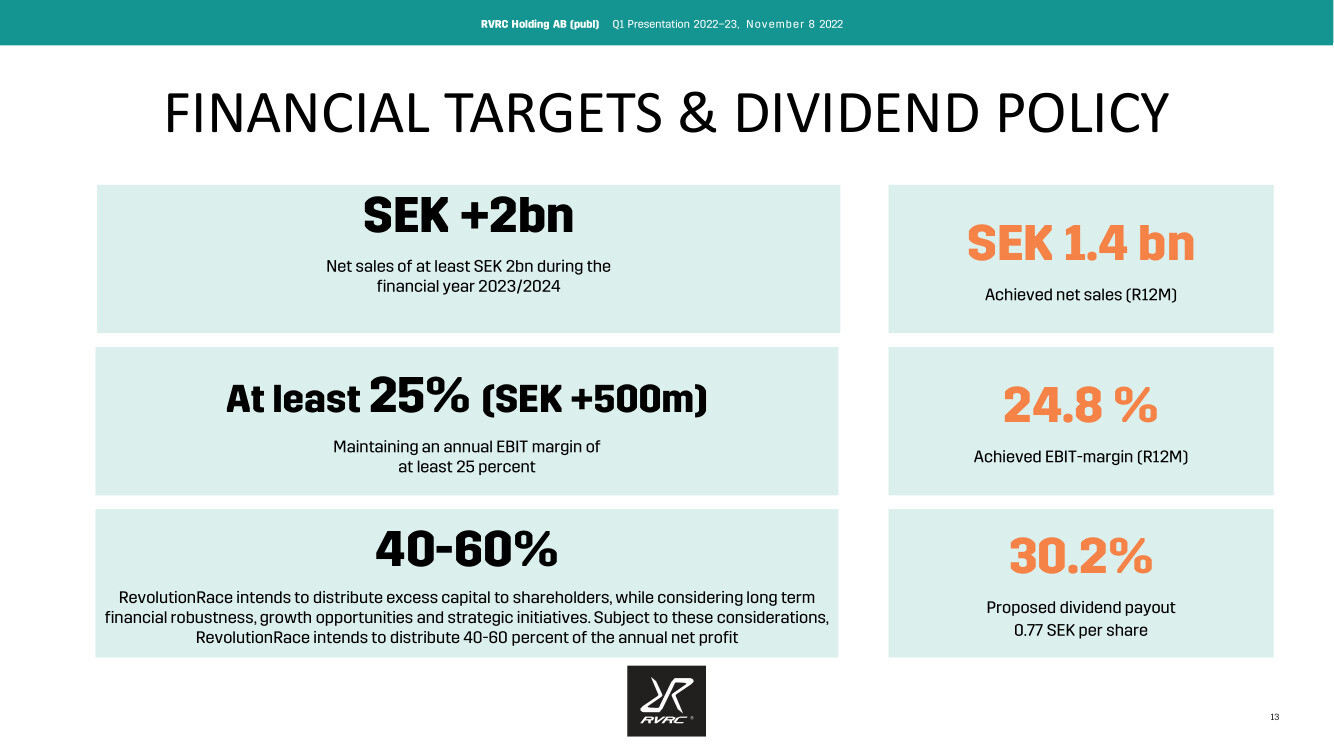

In line with its strategy, RR pays out 40–60 percent of its earnings as dividends, which is a good amount for a growth company. Inventory management is surely a delicate operation when there are many items for sale; they are multiplied first by gender, then various sizes, different colors, and furthermore three different warehouses, so there is inevitably a lot of inventory on the balance sheet. At first glance, the outlet situation looks a bit concerning to a shareholder, but when you filter for gear that fits you, for example, quite little is left. https://www.revolutionrace.fi/campaigns/40-selected-items

The company reported that sales this year have started with more moderate growth rates than the previous quarter, but they are well on track toward the July 1, 2023 – June 30, 2024 fiscal year target, i.e., 2 billion SEK in sales. The rolling 12-month figure is now 1.47 billion. However, market turbulence is to be expected in the future as well. The profitability target might be a more challenging goal, even though it has been exceeded before. Especially if moving toward founder Pernilla’s vision where RevolutionRace climbs toward export success similar to H&M, Ikea, Volvo, and Spotify. There is still a way to go to reach these peers.

Hi, and greetings from Stockholm ! I can’t promise anything 100%, but I might have a chance for a quick interview with RR’s CEO tomorrow.

If it happens (please don’t shoot me if it doesn’t.. ): any requests for what I should ask ?

Wow, that would be great if it works out! I’m at least interested in how RR believes it will reach its ambitious growth targets in the current changed market environment. Will we see new product category launches or new online stores (countries)?

Revolution has 500,000 Instagram followers and a huge number of product reviews on its website. RR has emphasized the importance of influencer marketing on many occasions, but it is already a significant influencer itself. Has RR planned to leverage its community, for example, through a service where the community could recommend nice hiking destinations to each other or otherwise share outdoor tips?

@Isa_Hudd, during the last announcement, I noticed that the cash position is starting to look a bit tight. Of course, it depends a lot on the figures to be released where we stand now, but I would like to hear some thoughts on how management views the adequacy of the cash reserves.