Opening a thread for Rusta, whose performance may also be useful to follow for those interested in Tokmanni and Puuilo – in Tokmanni’s case, particularly through Dollarstore. Like its competitors, Rusta also intends to grow by expanding its store network. Time will tell which of these companies will ultimately be the most successful. Without further ado, let’s dive into the Rusta case.

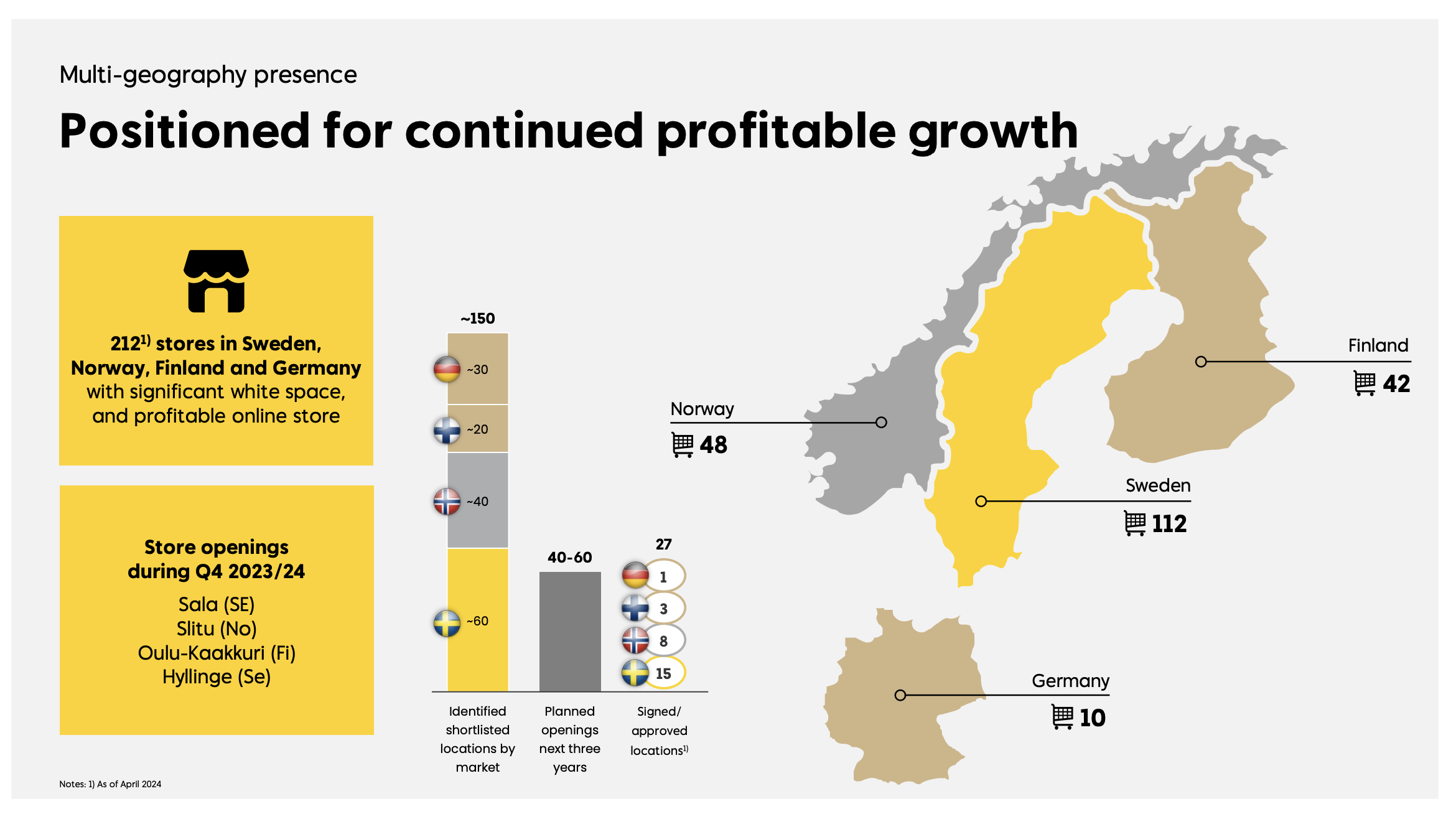

Rusta is a Swedish international discount retail chain founded in Uppsala in 1986, which listed on the Stockholm Stock Exchange in the fall of 2023. At the time of writing, it has over 200 stores in Sweden, Norway, Finland, and Germany, complemented by online stores in Sweden and Finland.

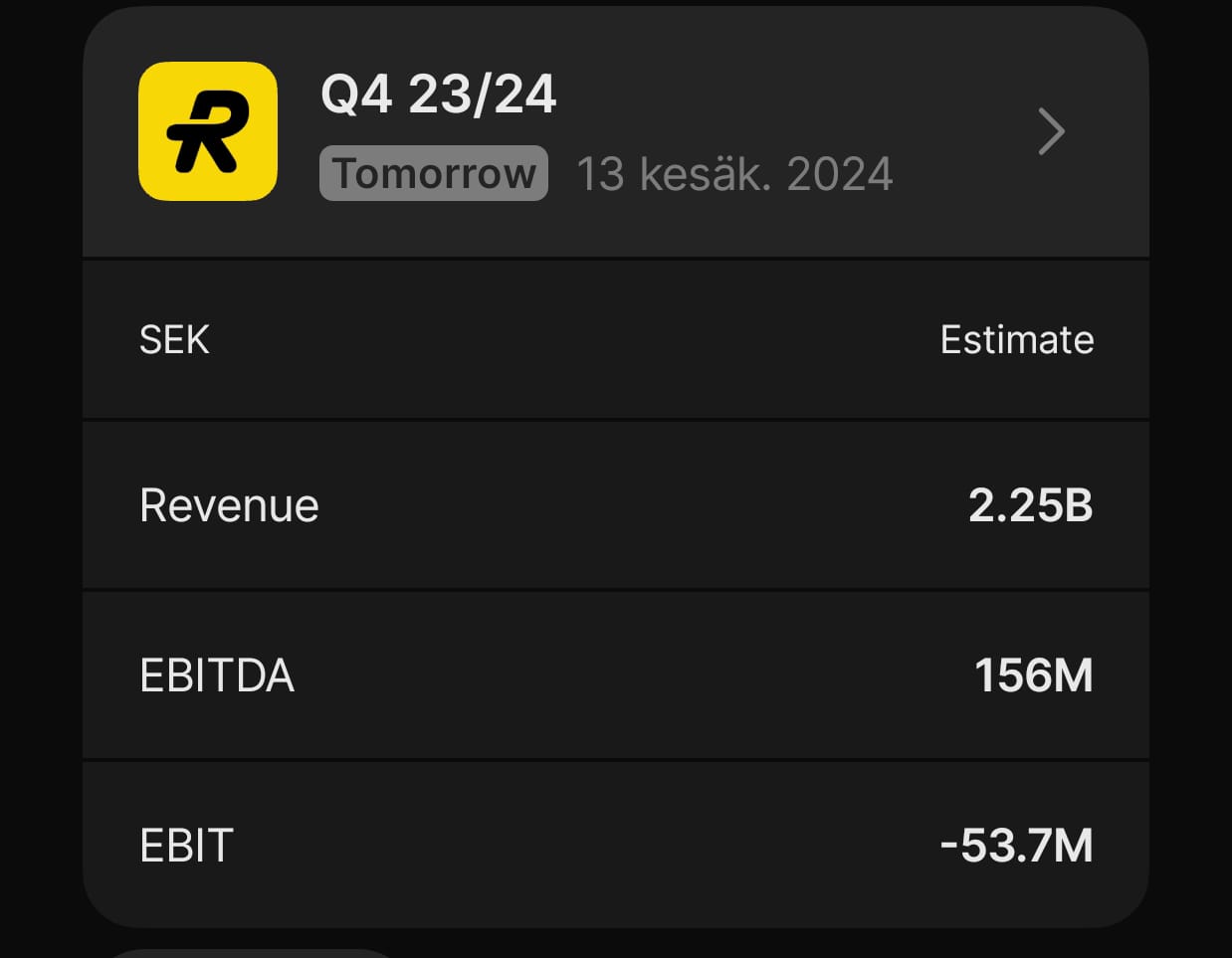

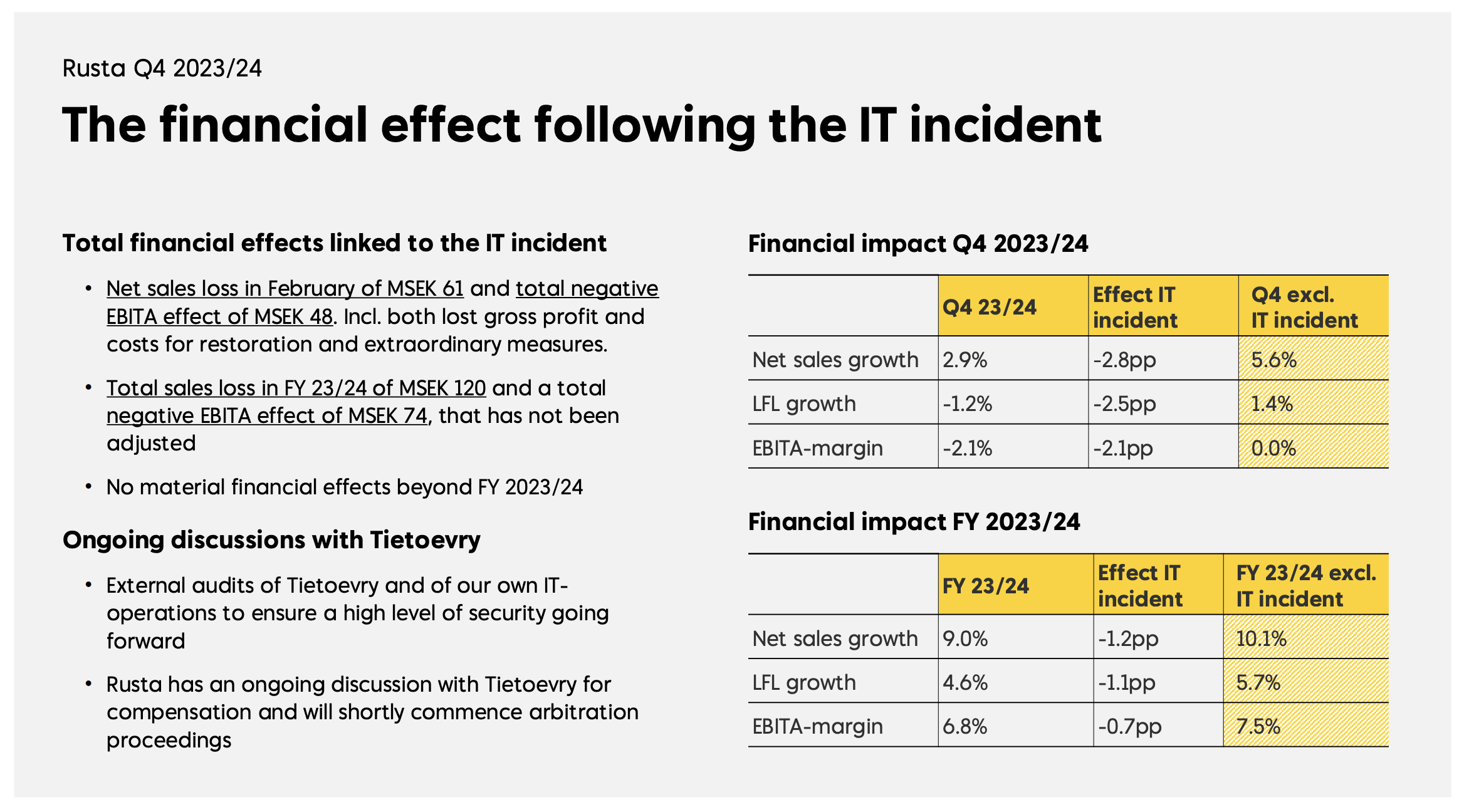

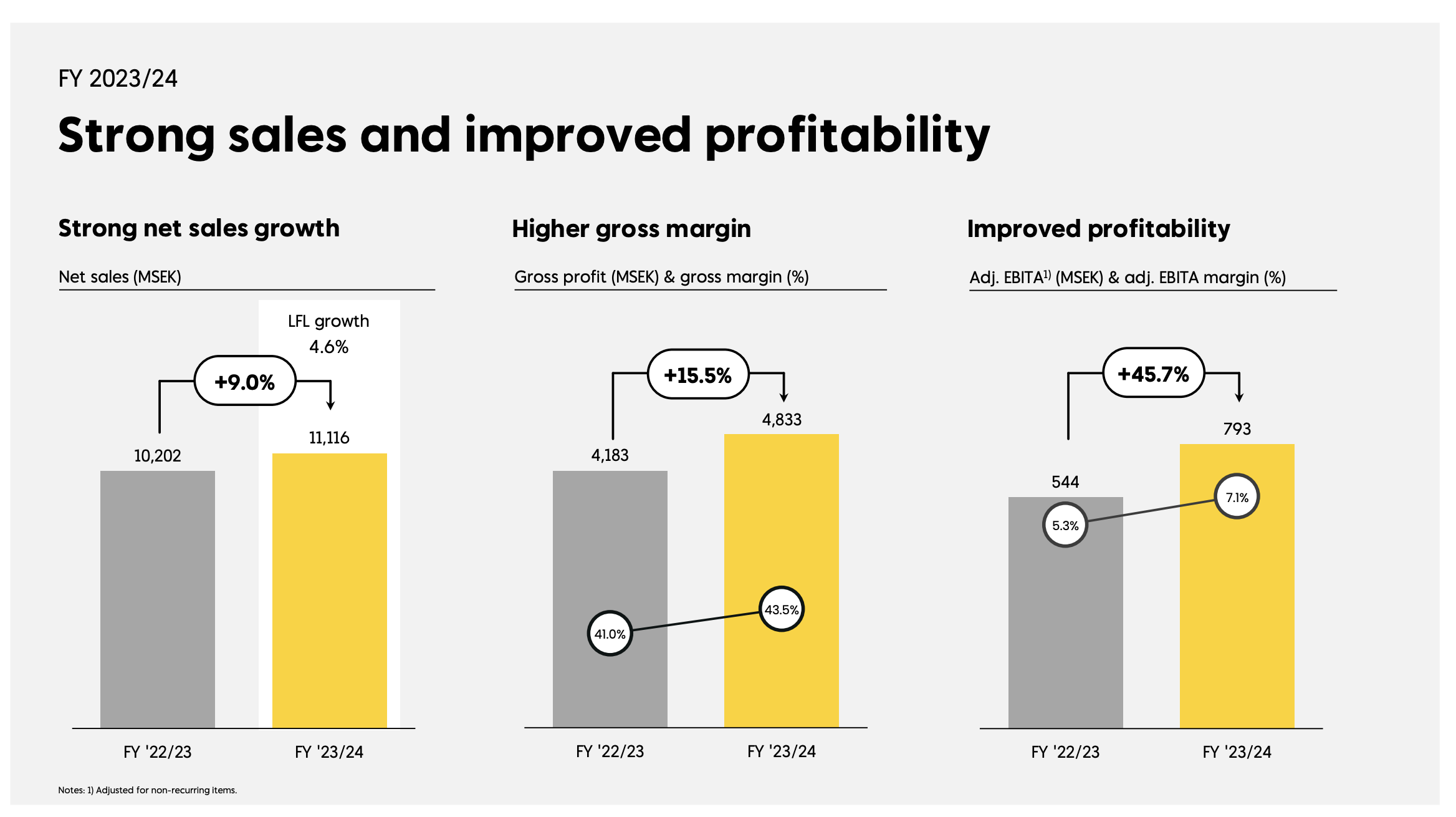

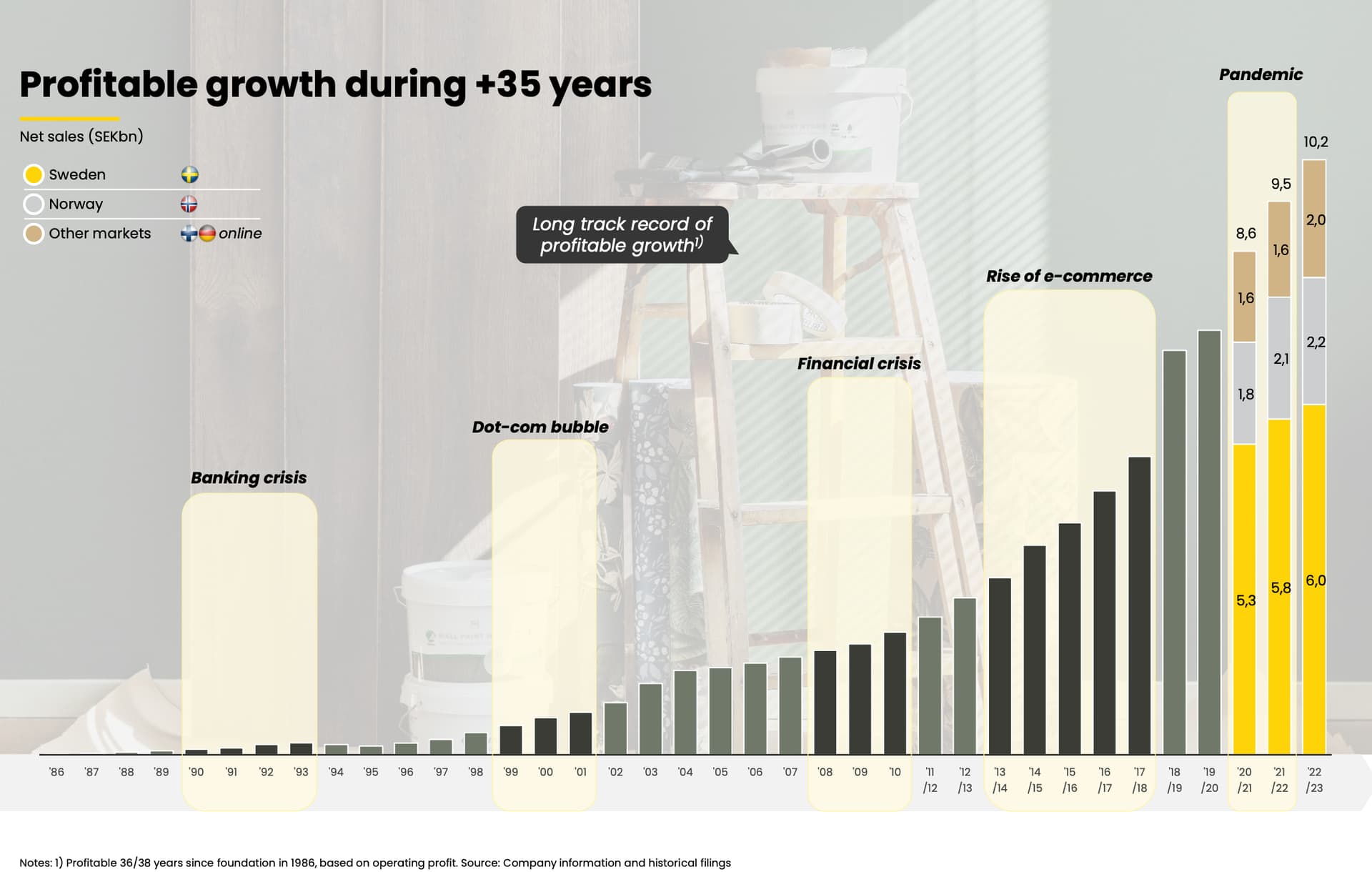

The majority of Rusta’s revenue comes from brick-and-mortar stores, as e-commerce accounted for only 1.6% of revenue in the 2022/23 financial year (10,202 MSEK). During the same period, Rusta’s adjusted operating profit (“adjusted EBITA”) was 5.3% and return on equity (ROE) was 20.5%. These figures will be updated very soon, as Rusta will report the results of its non-calendar financial year later this week.

Rusta has over 5 million loyalty members (“Club Rusta”), whose purchases accounted for nearly 80% of total sales in the previous financial year. Rusta’s main product categories are Home & Interior, Garden, DIY, Leisure, and Beauty & Care. Over 50% of the customer base is female, whereas for most competitors, the customer distribution is male-dominated.

Expanding the store network as a key growth driver

Virtually all stores in Rusta’s Swedish and Norwegian networks are profitable, while 85% of the stores in the Finnish and German networks were profitable in the 2022/23 financial year. In addition to growth, it is essential for Rusta to improve the profitability of its Finnish and German store networks to be closer to Swedish levels. More on this later.

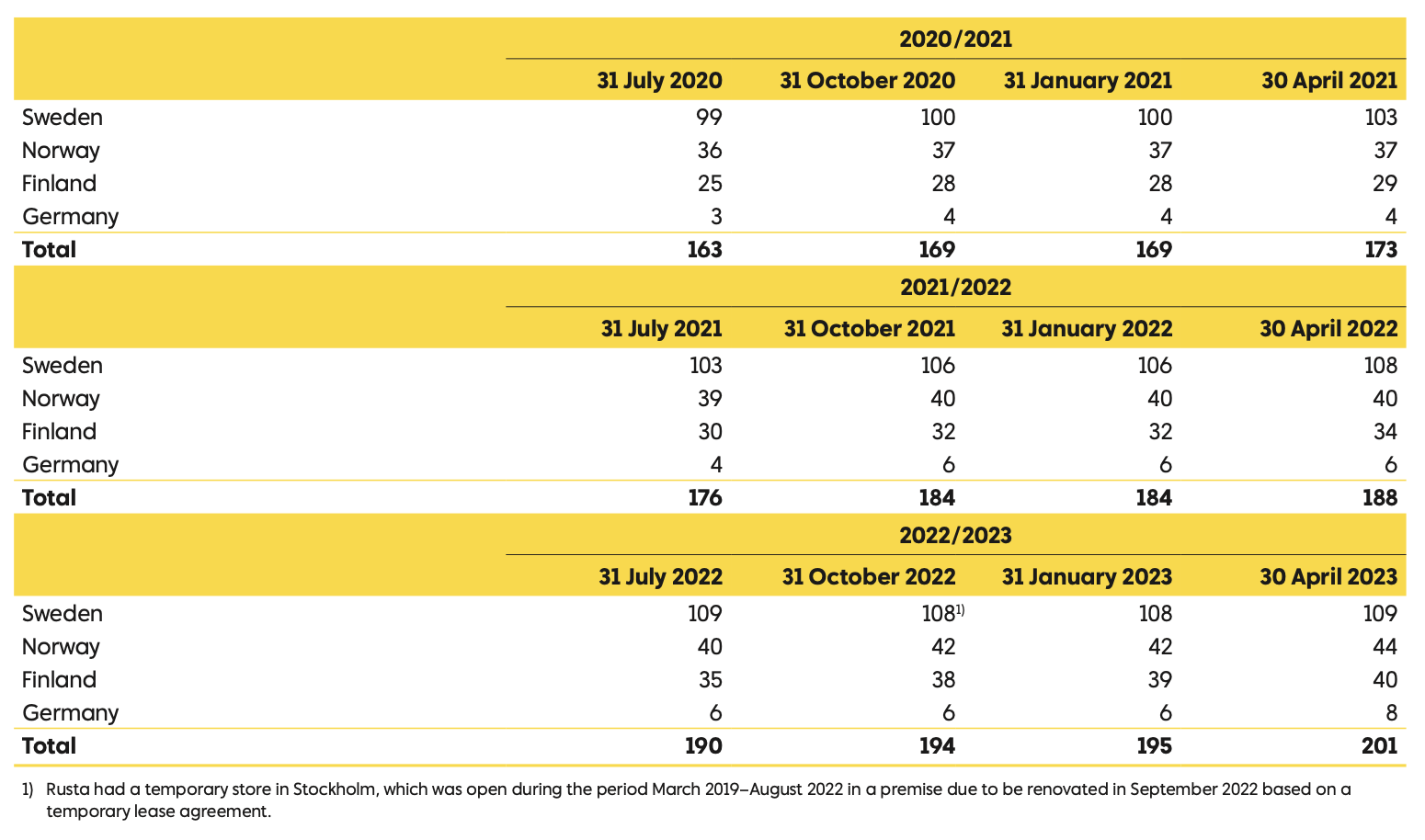

Expanding the store network is a central part of the strategy for many companies focused on discount retail, and this is also the case for Rusta. Rusta has opened an average of more than 10 new stores per year in recent years, and the pace of expansion is expected to remain rapid between 2024 and 2026, with 40–60 store openings planned. Time will tell how many they eventually reach, but as of January 2024, Rusta had signed agreements for 25 locations (14 in Sweden, 8 in Norway, 2 in Finland, and 1 in Germany).

According to the company’s own estimate, there are approximately 150 potential store locations in its current markets (Sweden ~60, Norway ~40, Finland ~20, and Germany ~30). Currently, about half of the network of over 200 stores is located in Sweden, with 40–50 stores in Norway and Finland respectively. There are about a dozen stores in Germany.

On average, opening a new Rusta store has historically cost about 4 MSEK (excluding inventory), and the store has typically paid for itself (“average payback period”) in less than a year—specifically 10–11 months. In Rusta’s IPO prospectus, the average payback period is defined as the investment related to establishing the store (including store interior but excluding working capital) relative to the store’s contribution margin.

I could not find exact information on the age of the store network, but based on my own conclusions, about 30% of the stores in the current network could be less than 5 years old, and these presumably have the highest ramp-up potential for sales.

Summary

Store network growth

Financial targets

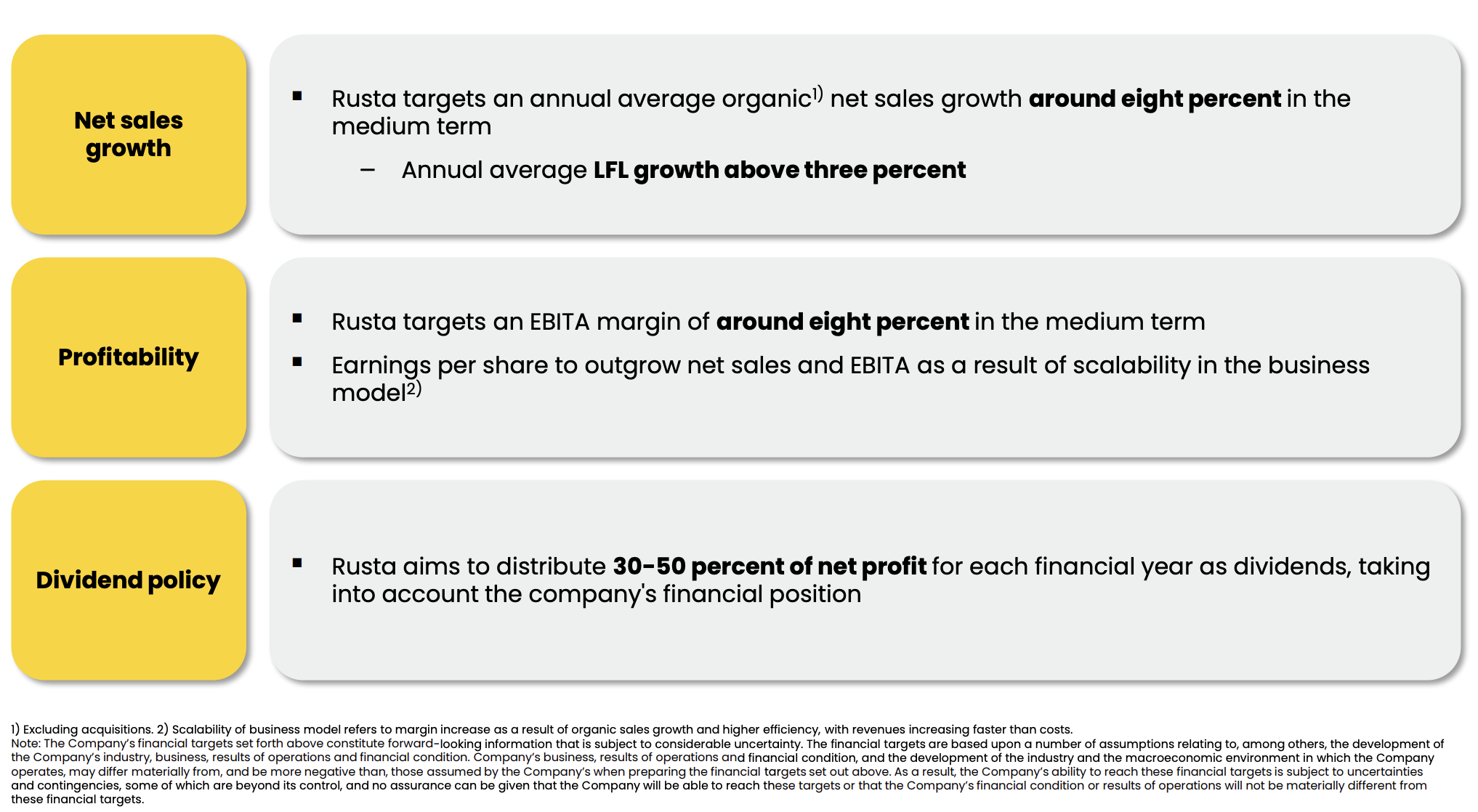

Rusta aims to grow its revenue by an average of about 8% per year (CAGR ~13% 2019–2023) without acquisitions. A significant part of the growth is built on network expansion, as the underlying target for like-for-like (LFL) sales growth is over 3 percent per year.

The profitability target is an 8% EBITA margin (~5% 2022/23). In Sweden and Norway, Rusta already achieves significantly higher profitability than this. Therefore, efficiency must be improved most in Finland and Germany to prove the scalability of international growth.

A significant portion of the profit is reinvested into business growth, as according to the targets, 30–50% of Rusta’s net profit should be distributed as dividends.

The market in brief

A good overview of the Nordic discount retail market and its competitive landscape can be found in the market overview of Rusta’s IPO prospectus (pages 43–54). According to Rusta’s estimate, the size of its relevant market was 67 billion SEK (Sweden 29, Norway 20, Finland 18) in 2022. The share of discount retail in the total retail market was less than 4% in all countries, while in the USA, for example, it was estimated to be at least 9%.

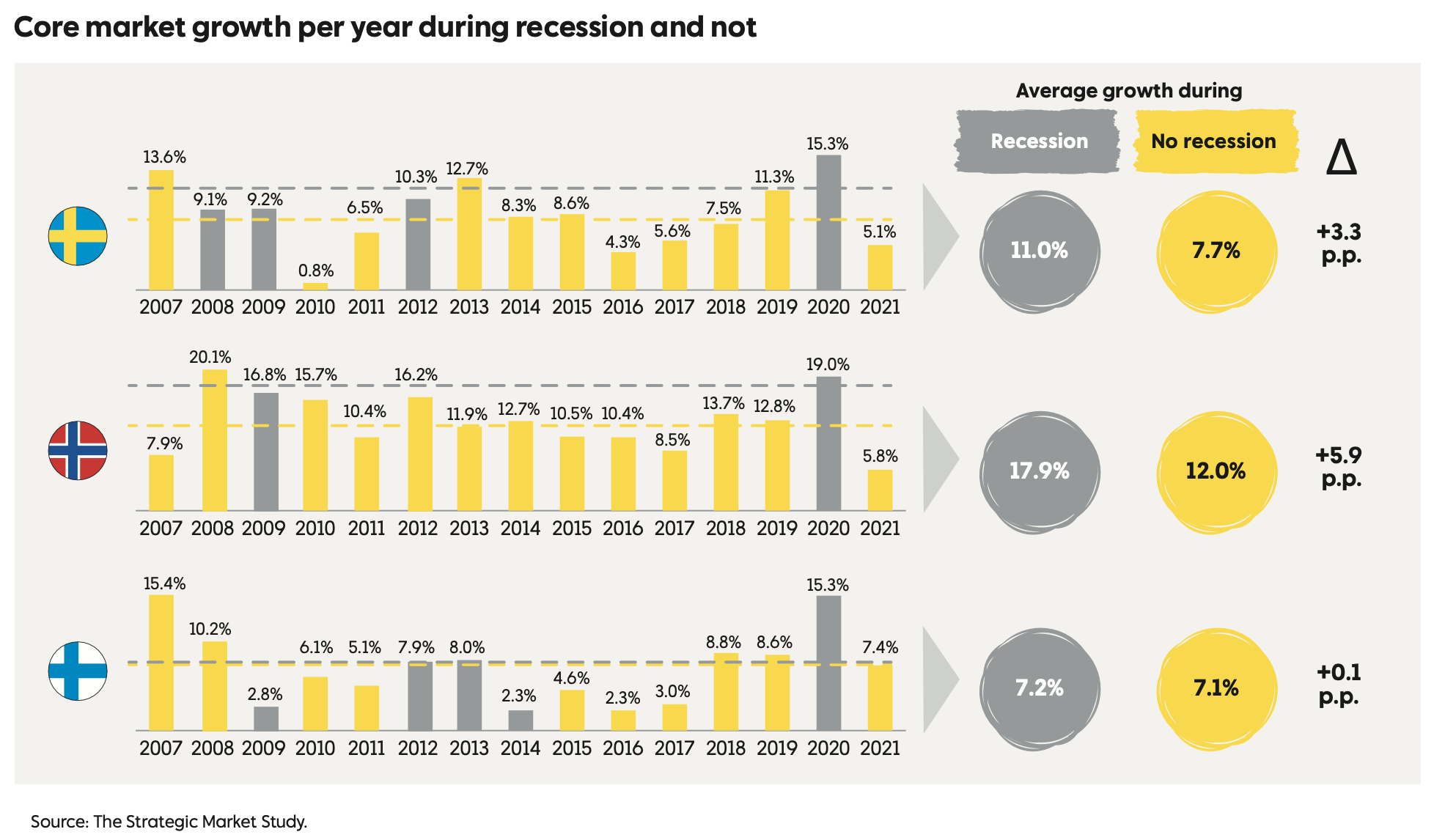

Between 2018 and 2022, the discount retail market grew by a total of 8.9% in Sweden, Norway, and Finland according to Rusta’s estimate, driven partly by strong pandemic years. Despite this, the market overview predicted that growth would continue at a rate of about 8% per year, explained by, among other things, the uncertain economic situation supporting discount retail and increasing price consciousness among consumers.

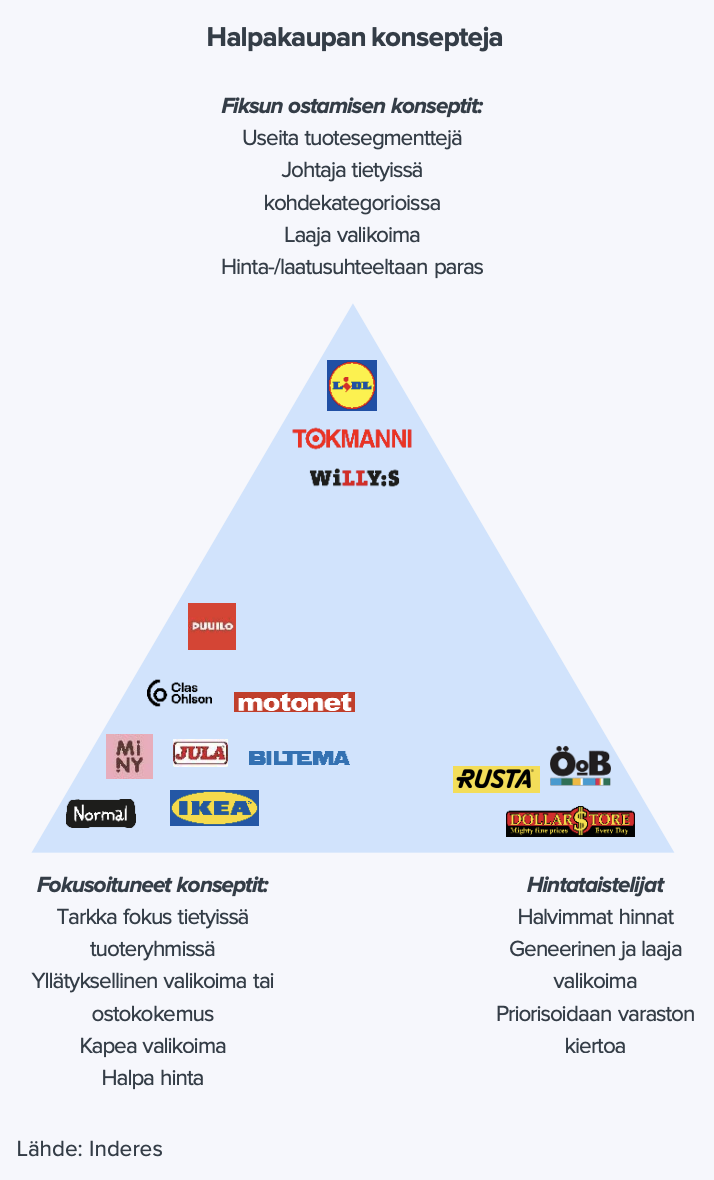

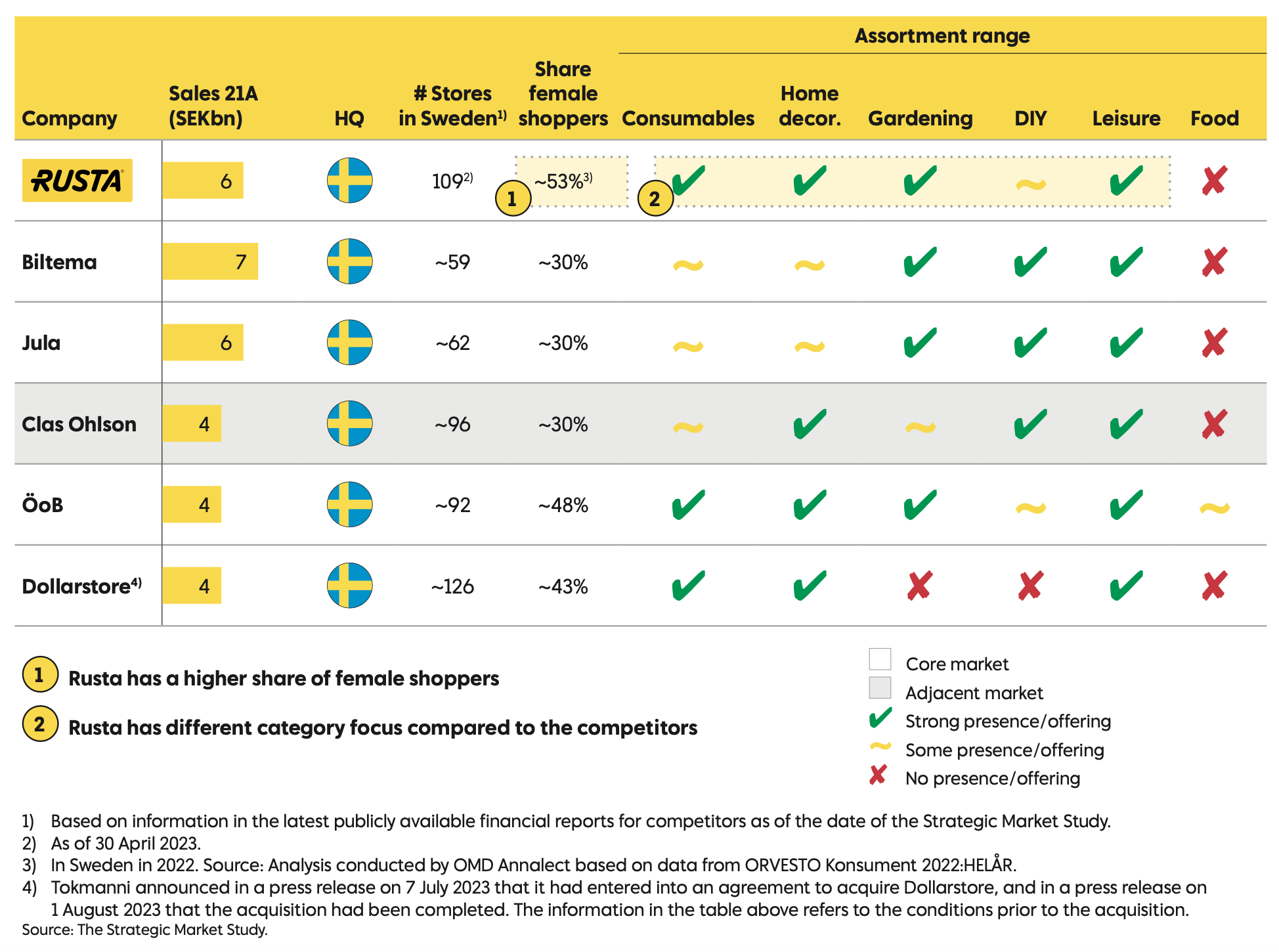

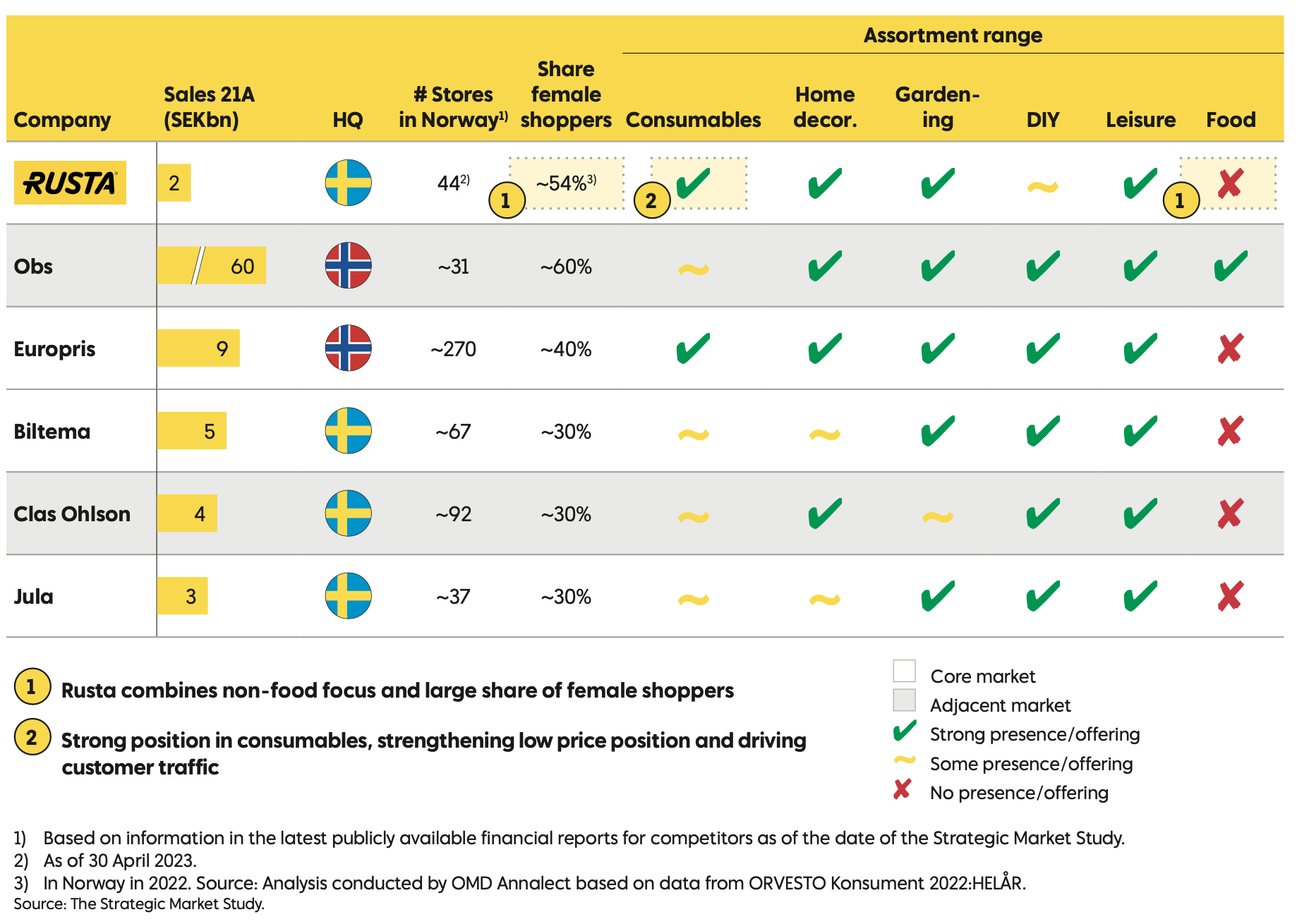

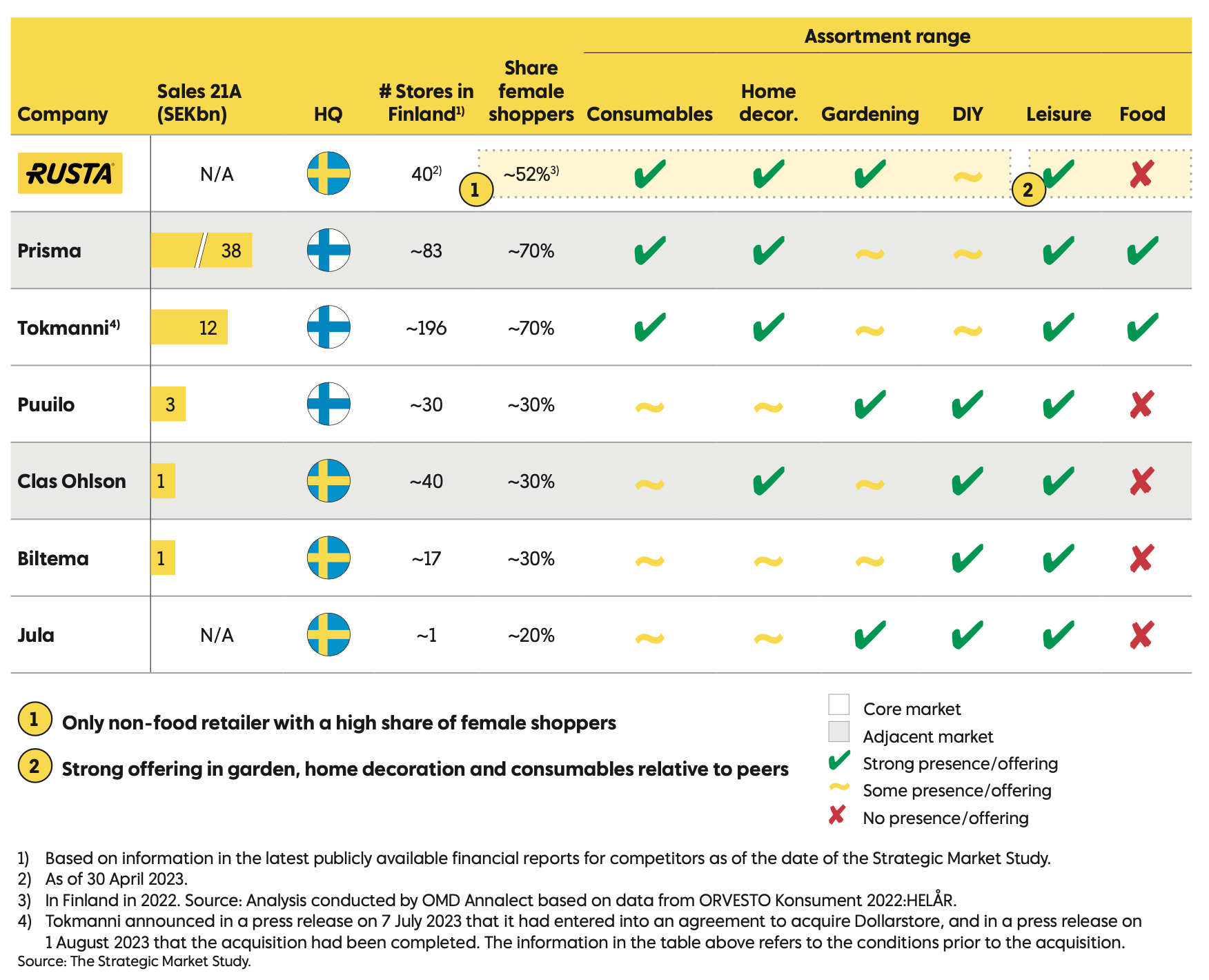

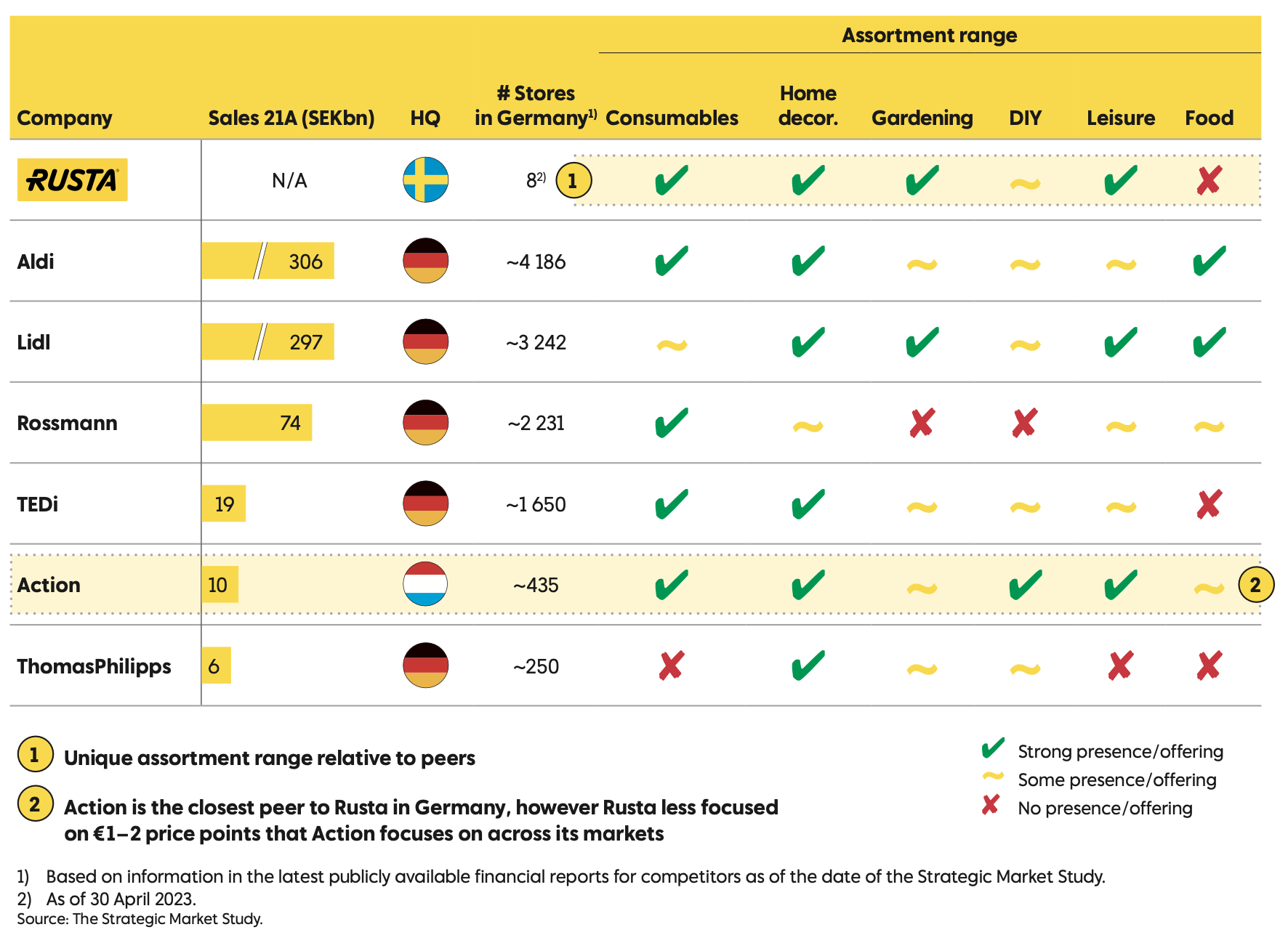

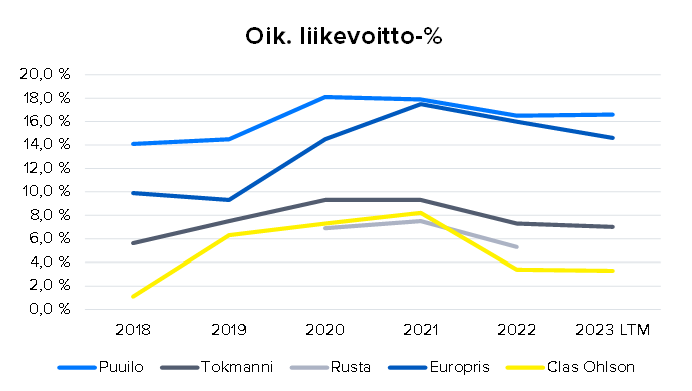

In the competitive landscape, Rusta competes in all markets (excl. Germany) with Biltema, Clas Ohlson, and Jula. In addition to these, key local competitors include DollarStore and ÖoB in Sweden, Europris in Norway, and Tokmanni and Puuilo in Finland. Ikea is naturally a competitor for Rusta in all countries in the interior category. The summary below (click to open) gives a good idea of which categories Rusta differentiates itself in relative to its main competitors.

Summary

Competitive landscape in Sweden

Competitive landscape in Norway

Competitive landscape in Finland

Competitive landscape in Germany

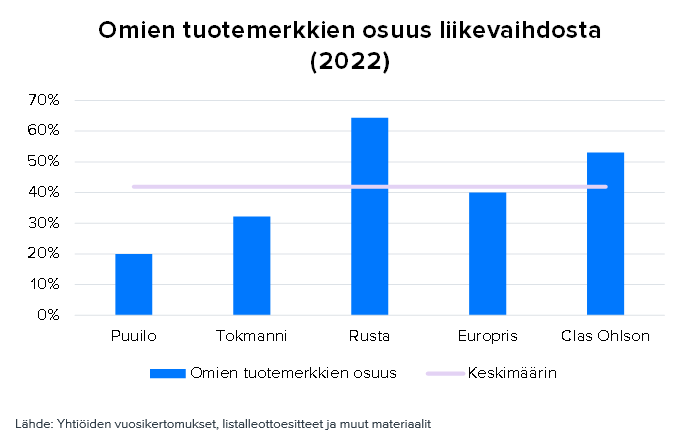

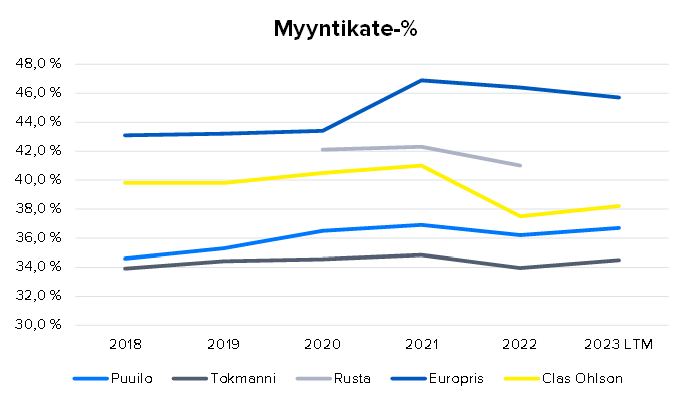

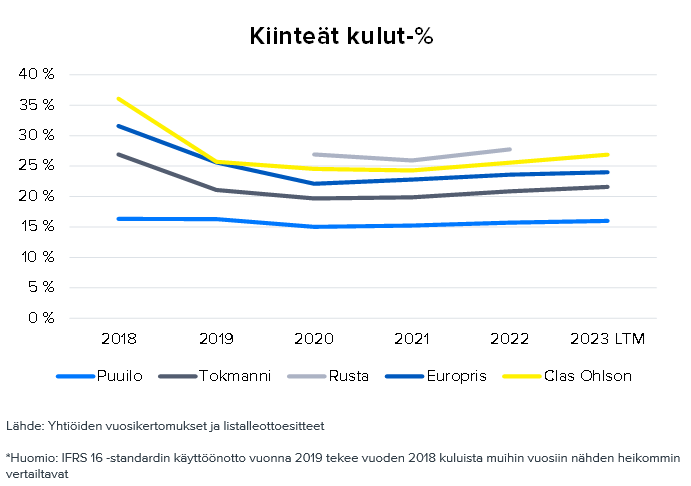

This information could be supplemented by the fact that the share of private labels in Rusta’s sales is clearly the largest among its peer group (over 60%), and its gross margin percentage (over 40%) is among the highest. Fixed costs as a percentage of sales are correspondingly at the highest level, partly due to the overhead required for international growth.

Summary

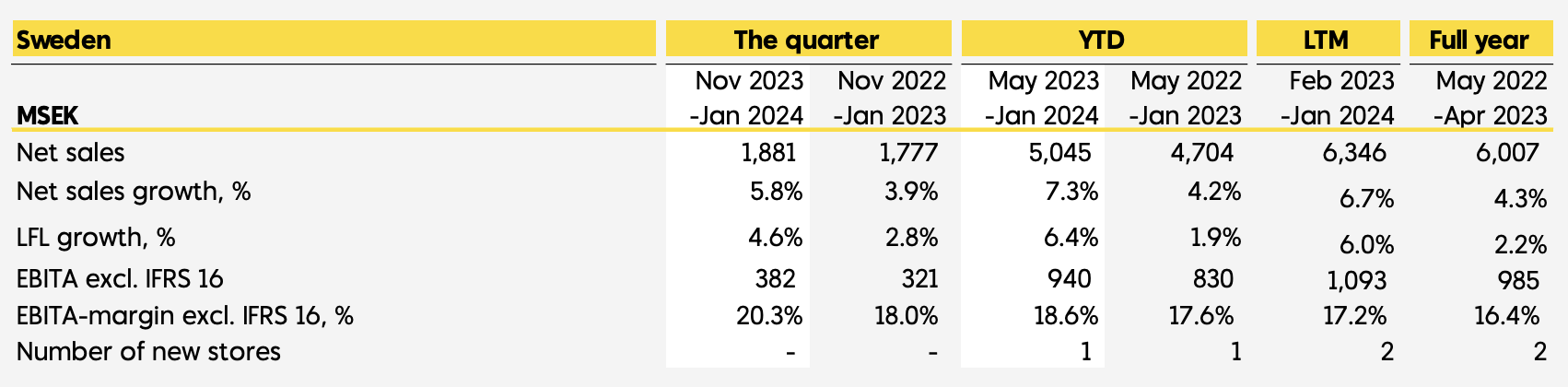

By far the most important market for Rusta, in terms of both revenue and the number of stores, is Sweden, which currently accounts for ~60% of sales and about half of the stores. Based on previous quarters, it is also clearly the most profitable market area for Rusta.

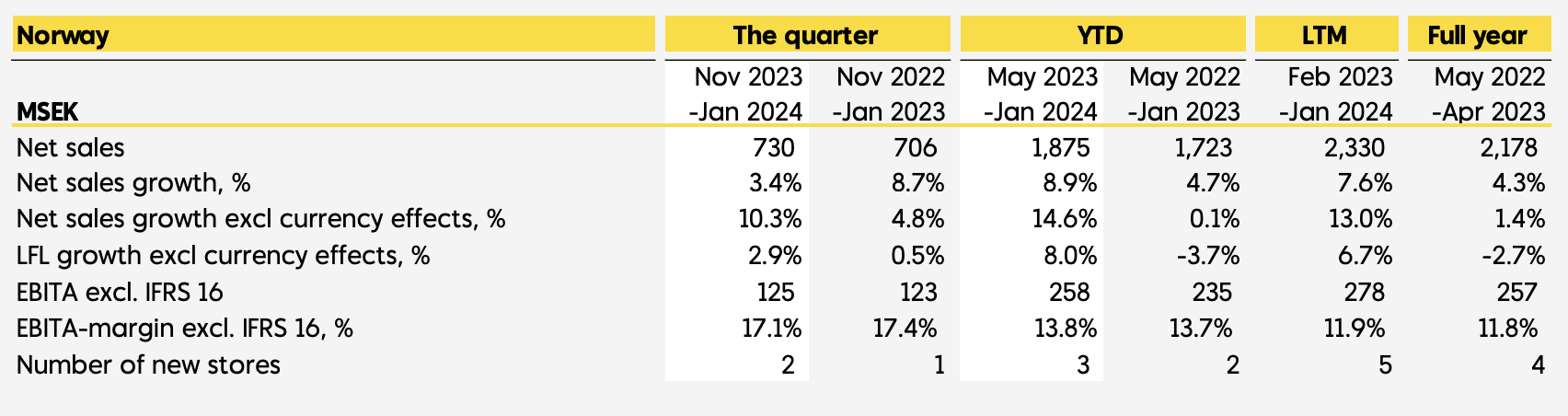

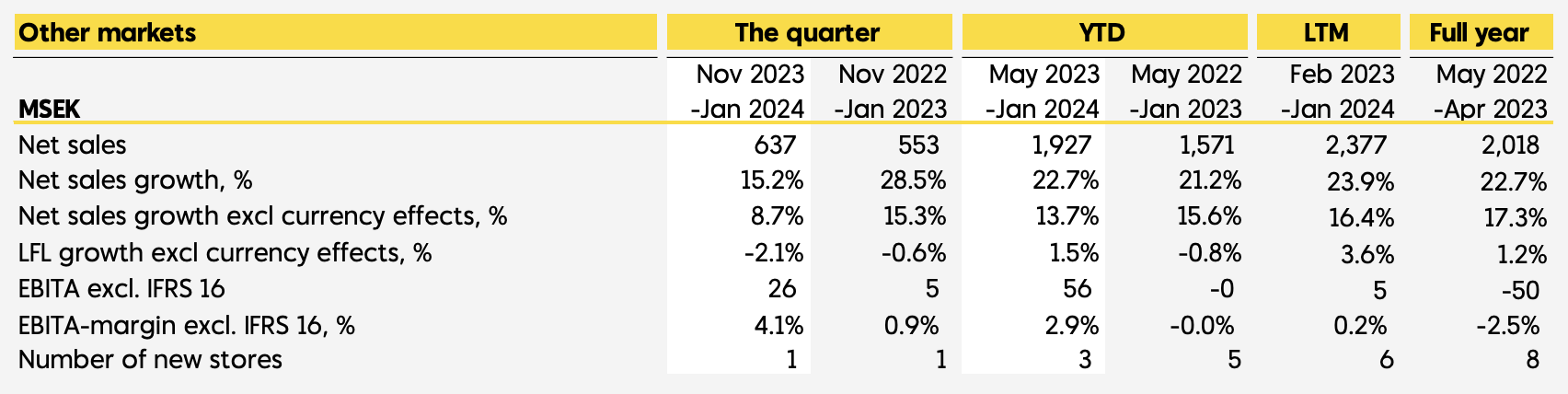

Since Rusta’s operations are divided into three segments (Sweden, Norway, and Other Markets), one can get a fairly good idea of market-specific development, even though “Other Markets” covers Germany and e-commerce in addition to Finland. The summary below shows the market/segment-specific figures for the previous 12 months and the financial year in more detail.

Summary

Sweden segment

Norway segment

Other Markets segment (Finland, Germany, Online)

Further resources

Since not much time has passed since the IPO at the time of writing, the most comprehensive information about Rusta can be found by reading its IPO prospectus. Below are also other relevant links related to Rusta.- IPO 2023 Prospectus

- Case: Profitability and cost structures of Nordic discount retailers

- Puuilo vs Rusta as an investment? | Kästi & Keskiväli

- Interim reports and info

- Company page on inderes.fi

Here is a brief summary of what the company is roughly about. More analysis will likely be added over time as I get to know the company better—for example, regarding returns on capital, leverage, risks, share valuation, management and ownership, and the breadth and differentiation of the product range. Finally, it should be noted that any errors, blunders, or misunderstandings are my own, and I do not own the stock at the time of writing.