I opened a new thread for this Swedish company that is surely familiar to almost everyone, at least through its brands, since no previous thread could be found.

As a quick background, the company operates in the field of outdoor and hiking apparel with its timeless brands, the most famous of which is Fjällräven. The portfolio also includes Hanwag, Tierra, and Royal Robbins. The company also includes Partioaitta and its foreign equivalent stores. The stores also sell many products from other brands, but the primary focus is strongly on their own brands.

Historically, the company has an excellent track record of growth and strong profitability due to its great pricing power.

In the longer term, the company’s profitability has mainly been eroded by the inefficiency and high cost structure of brick-and-mortar stores, while wholesale and direct-to-consumer sales have performed excellently.

Today, the company’s 2023 financial year figures were released, and they were grim reading. Interim-report-2023-12-31 (1).pdf (3.1 MB)

Profitability dropped significantly, and the last quarter even went well into the red. The share price also reacted as expected. Personally, the weakness in the USA particularly surprised me, given the previous strong trend. Reasons for the weakness were explained in the report by weather conditions and the fact that they did not participate in Black Friday and Cyber Monday campaigning, as well as the weak financial situation of retailers and the general inventory situation. A “COVID hangover” was also mentioned. Have other Inderes members delved into Fenix’s operations and opportunities? In my opinion, the company has excellent long-term opportunities to consolidate the market, and especially now, possibly at the bottom of the cycle, to make acquisitions at attractive valuations and create future growth.

Thanks for starting this thread!

I’m familiar with the company, mainly regarding the acquisition of Partioaitta’s stores in the Helsinki metropolitan area over 10 years ago. I know the brands from personal use and I’m aware of the distribution companies. Especially Globetrotter, which operates in Germany, is quite a significant player. From a Finnish perspective, Fenix’s flagship brands are high-quality gear.

The result for the last quarter really seems to have dropped like a camping axe into a spring. Quite a lot of the weak performance seems to be explained by one-off write-downs and investments in streamlining operations. Hopefully, they will also deliver on their promises.

I believe in the company’s positive growth prospects and development, even as the nature rush of the COVID era levels off a bit.

This could be considered for the portfolio at these levels to some extent, if for no other reason than for the love of the game. It’s nicer to go shopping for outdoor gear and clothing when you can buy “your own company’s” products

This turned out to be more of an emotional outpouring than a financial analysis, but so be it…

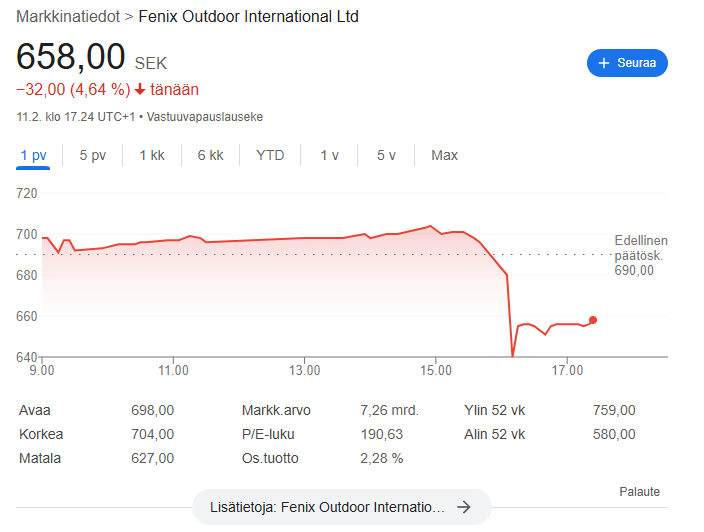

Many people’s faith in the company is currently more than tested. The Fjällräven brand is still carrying the company, but even its ability to defend the company’s performance is now under strain. EBITDA collapsed by almost half, and difficulties in the US intensified. According to the Chairman, Q2 is the most sensitive quarter, but now that H1 is wrapped up, the result stands at -€0.05, whereas a year ago, when it was already difficult, we were at least €0.83 in the black. Sure, there have been some organizational changes regarding distribution channels, but in the big picture, the situation looks particularly bad, even though excessively high inventory levels should gradually be cleared. The strength of B2C sales was positive, but unfortunately, it wasn’t enough to compensate for the rest of the operations. A surprisingly small drop in the share price, only 18% from yesterday to the time of writing, likely due to low trading volume. The €585 million market cap seems unjustified based on my own calculations, which is why I put my own shares on the sell side.

There needs to be a clear change in Fenix’s story soon; otherwise, we are inevitably on the same path as Rapala.

Of course, it must be admitted that the market is not easy and sales are solidly higher than the pre-COVID era, when there was plenty of front-loaded purchasing by consumers—after all, even our quality company Harvia hasn’t found a path to organic growth in Finland since those times. Also, Fenix products last for years, and you don’t need to update a good backpack very often.

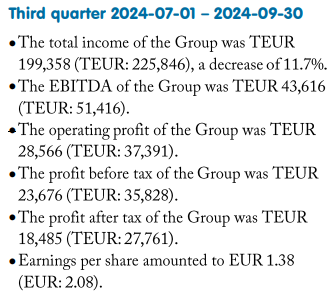

Revenue decreased by 11.7% from the comparison period and EPS by 34%. However, EPS was quite comfortably positive, 1.38 EUR compared to the negative EPS of the previous quarter:

Brief comments from the Chairman of the Board, translated freely:

Price pressures, warm weather, and pressures on supply chains caused by the Middle East are weighing in.

There isn’t much positive to say about sales, but at least there is growth in some markets, e.g., Canada.

Inventory levels were reduced and gross margin was increased.

A slight change in the air, where brick-and-mortar stores performed better than digital.

Brand segment growth slowed by 20.8%. The main reason was North American sales, and some unprofitable stores have been closed. As a result, however, costs are falling and margins are improving.

Global Sales segment sales dropped by about 17% and gross margin fell due to a changed sales mix. Expenses improved (decreased?) according to plans.

Frilufts segment sales fell only 2.3%, mainly due to digital sales in Germany.

Q4 looks okay based on the first few weeks.

Moving forward, there are plenty of challenges, mainly due to supply chains and freight costs. ESG and CSR laws (regulation) also make the business environment unpredictable.

The preorder book for next spring looks more positive than for this year. Autumn and winter orders for next year also look more positive.

Costs are starting to be better controlled.

The balance sheet is strong and enables acquisitions if opportunities arise.

Next year’s outlook is positive, and the current volatile market may be ending and the market may be normalizing.

Personal thoughts:

I took a tracking position at the beginning of September; the share price has dropped about 6% since then, and I personally expected worse.

A turn back to earnings growth is unlikely to happen in Q4; I would expect it next year.

I might add to this in the near future, depending on how the share price continues from here. With last year’s earnings, P/E ~19; with the 2022 peak earnings, P/E ~9.7. I don’t think we’ll be returning to that 2022 peak earnings level for a while, but 3 EUR and a growing EPS doesn’t sound impossible for the coming years, so the valuation feels quite neutral. Currently, the share price reaction to the results is neutral, so apparently, it met market expectations: