Business

Nilörngruppen is a label manufacturer whose shares are listed on the Stockholm Stock Exchange. The company designs and manufactures garment labels in collaboration with fashion houses. Through labels, manufacturers can enhance the branding of their clothing. Labels represent a small luxury that elevates the perceived value of a garment purchase in the eyes of the consumer. Today, labels include identifiers through which manufacturers can send greetings to the consumer or provide, for example, washing instructions. These identifiers also facilitate e-commerce inventory management, as scanning a code reveals which product is in question.

The company was founded in 1977. Since 2009, the company has undergone a transformation process from a manufacturing-oriented company toward a service-focused group. The company has distribution units in Europe and the Far East, from which products are delivered to factories serving brand houses. The company has over 1,000 customers, of which the 10 largest cover 30% of revenue and the 20 largest cover 44% of revenue (in 2022).

The company’s main owner, with a 58.1% voting share, is the Swedish listed investment company Traction AB.

Profitability

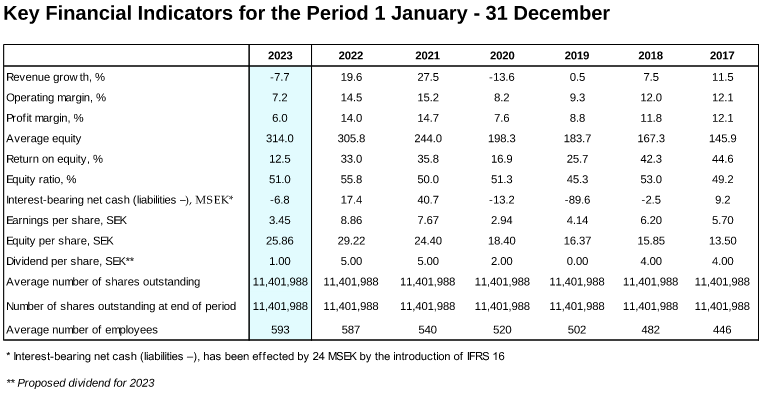

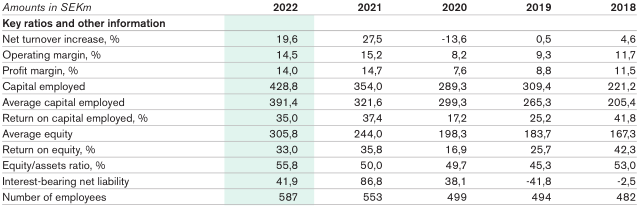

Nilörngruppen is a highly efficient and profitable group. The operating margin has averaged 11.6% over the last 10 years, and revenue has grown by 146% during the same period. Growth has been achieved through internal financing, and the share base has not been diluted. The company’s balance sheet is also net debt-free (as of 2023 Q1). The company’s Return on Assets (ROA) was 17.2% last year.

Risks

When considering the company’s risk profile, it is worth paying attention to the pandemic year 2020 in the accompanying table. Revenue decreased by -13.6%, but the operating margin fell only slightly to 8.2%. Thus, the company was able to adjust its costs and keep cash flow positive. However, the stock crashed severely on the market, losing about two-thirds of its market valuation.

I believe the company’s real risks relate to the necessity of the product if consumer buying behavior shifts toward recycling clothes at the expense of buying new garments. The company is cyclical, and purchasing clothes is something consumers can easily cut back on when the economic situation is tight. Furthermore, in the Business-to-Business sector, the company is dependent on the fashion houses’ own cost-saving measures and competitiveness. Recently, the decline in consumer confidence and the high inventory levels of garment manufacturers have led to a weakening of the company’s earnings development and a decline in the share price.

Valuation

The company has 11,401,998 shares outstanding. At a share price of 70 kronor, the market capitalization of the shares is 798 million kronor. Based on the latest quarterly report, the P/B ratio is 2.31. Net cash is 25.4 million kronor. The board has proposed a dividend of 5 kronor per share to the Annual General Meeting to be held in May.

Disclaimer:

Nilörngruppen shares currently account for approximately 5.8% of my stock portfolio’s value. This thread opening is not an investment recommendation; the information may be incorrect, and I encourage readers to conduct their own research on the company. The 2022 annual report can be read at this link.