Over at Inderes.se, you can find an interview in Swedish by @Isa_Hudd with CEO Johannes Lind-Widestam! ![]() In the video, we hear how the company’s 2023 went, delve into the Q4 report, review the market situation, and take a look at the outlook.

In the video, we hear how the company’s 2023 went, delve into the Q4 report, review the market situation, and take a look at the outlook. ![]()

9 Likes

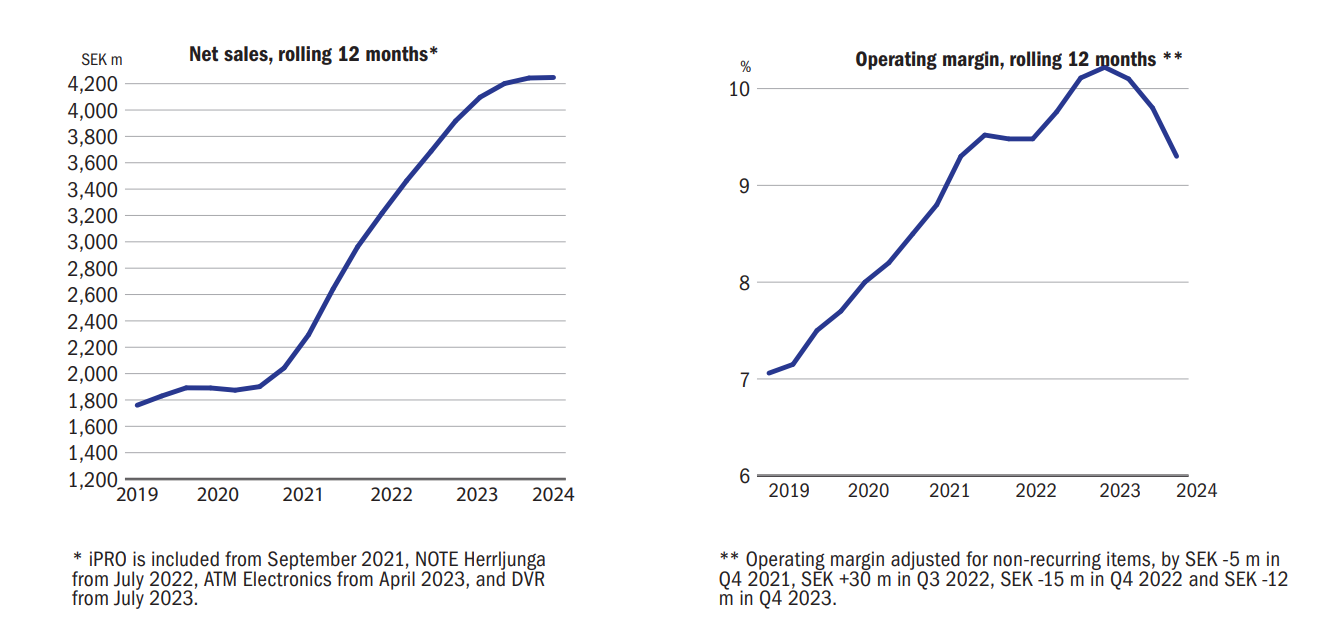

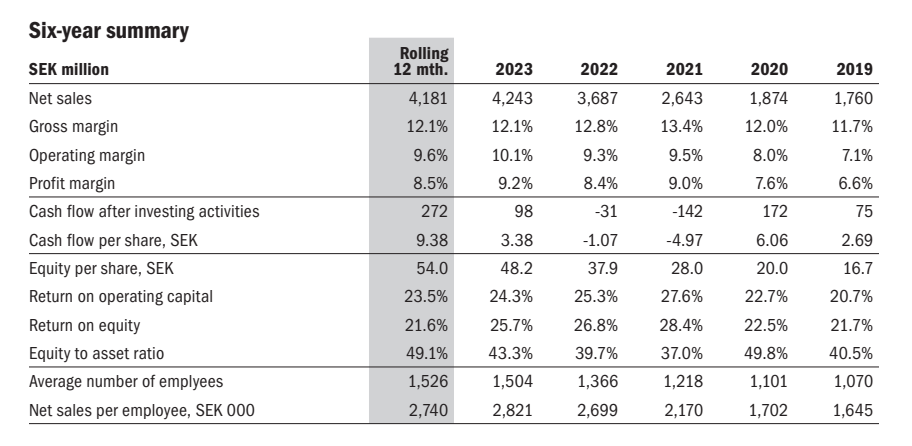

NOTE had a really sluggish start to the year.

At the same time, guidance was lowered regarding revenue, and the operating profit guidance was refined from 10% to 9.5-10.5%.

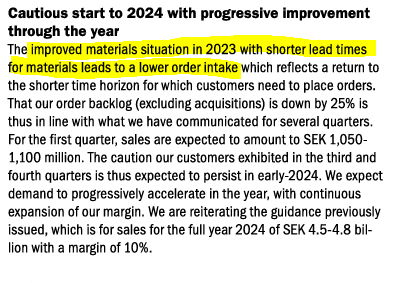

The order backlog does not inspire confidence, even though it is explained, as expected, as being due to the improved component situation resulting in no need to place orders so far in advance.

Our order backlog (excluding acquisitions) was down by 18% year on year. This is consistent with what we have been communicating for some time; that an improved situation on materials

with shorter lead-times will feed through to lower order intake, reflecting a return to the shorter horizons customers need to place orders. However, we do think some of the lower order

backlog can be attributed to the more cautious market situation, which had some impact on our guidance. For the second quarter, we anticipate sales of SEK 1,025–1,075 million. We now anticipate the cautious start to the year that we’ve witnessed in the first quarter continuing some way into the second quarter. We still expect progressive improvement in the year with full-year 2024 sales of SEK 4.3-4.7 billion and an operating margin of 9.5-10.5%. In our previous Interim Report, our estimate for the full-year 2024 was SEK 4.5-4.8 billion and a margin of 10%.

I have to say, compared to what Johannes was chatting about at the Redeye EMS evening a few months ago, the situation has certainly darkened quite a bit. Back then, they were still very confident that the downturn in the EMS sector wouldn’t really be visible at NOTE. If and when the year becomes difficult, it will be interesting to see if NOTE manages to protect its profitability as well as Incap, which used a very heavy hand to lay off people from its Indian factory when there was no work.

Well, NOTE is certainly one of the highest-quality European EMS providers, so it should be possible for them to emerge from this slump in a relatively even better position, as long as the procurement and consumption party eventually returns.

Full report:

https://storage.mfn.se/5e467787-c778-4575-ae72-df2af861b134/interim-report-q1-2024.pdf

16 Likes

Is it really that bad? Maybe I just haven’t followed closely enough, but at least at the beginning of the year, there was talk of a recession in the news and comments, and to my eye, these figures don’t reflect that, so in that sense, things went well.

Regarding the order intake, this previous comment seems to apply:

4 Likes

Updating the thread with Note’s Q2’24 report.

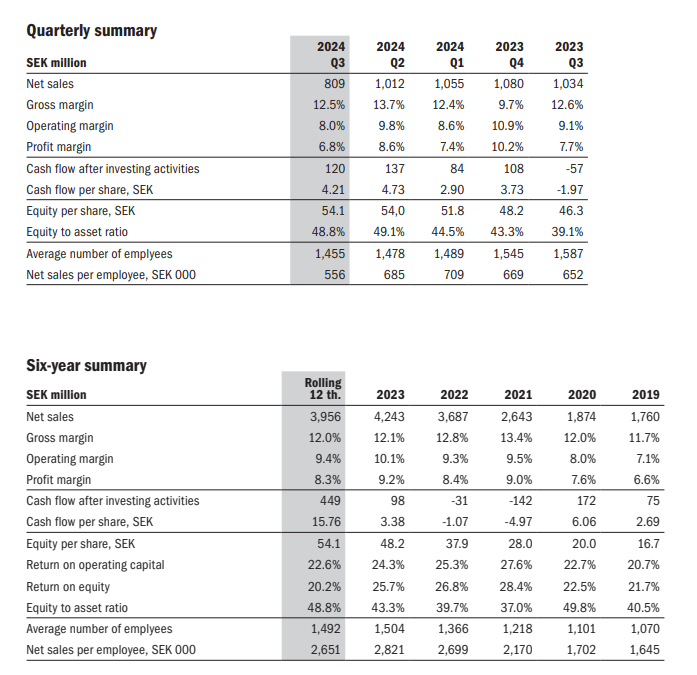

- Revenue 1012 MSEK (1078 MSEK). Organic growth -10%.

- Adjusted operating profit 97 MSEK (107 MSEK), or -9.4% year-on-year.

- Adjusted operating margin at the previous year’s level, i.e., 9.8%.

- Order backlog (excluding acquisitions) -18% year-on-year.

- Guidance was lowered for revenue to a range of 4100-4400 MSEK. Previous range was 4300-4700 MSEK. Profitability outlook remains unchanged at 9.5-10.5% in the guidance.

Highlights from the CEO’s review (not from a separate webcast)

-

Demand situation and inventories: The weaker economic cycle continues to affect demand, which has caused temporary delays in customer projects and inventory adjustments at the customer level. During the component shortage, many customers decided to increase their inventories, and it will now take a few quarters for these inventories to rebalance. As the market situation has soured, the inventory adjustment is taking longer than anticipated.

-

Market outlook in the longer term: Industry commentators expect the European EMS sector to grow at an average annual rate of about 7% until 2030. Annual fluctuations in demand can be strong, and this year is expected to be negative.

-

Visibility: There has been a return from the pandemic-era extended order horizons to shorter lead times due to improved component availability, and in some cases, delivery times have been even shorter than normal due to the more uncertain market situation.

11 Likes

Selling continues

2 Likes

I listened to NOTE’s latest earnings webcast at the end of last week (right after Incap’s equivalent). It wasn’t nearly as bleak as one might assume from the share price drop, the CEO’s share sales, and the negative profit warning.

However, I must add immediately that CEO Johannes’s commentary always seems to have a slight air of over-optimism, so it’s worth applying a small “safety margin filter” when listening to these NOTE events.

Nevertheless, in Johannes’s words, demand, the market situation, and the outlook for the coming years are much better than what can currently be reported in the form of figures. Regarding the acute situation, he said the end of Q1 was more difficult than the end of Q2, so perhaps the dip has already started to level out. About the coming years, he said he sees no reason why NOTE wouldn’t grow by double-digit percentages from 2025 onwards, doing exactly the same things as in previous years.

In addition to growth, he was confident that profitability will continue to improve. Regarding profitability, I must say that in my opinion, NOTE has protected it quite admirably in this otherwise weak situation.

A few of my other thoughts:

- Western production facilities are performing well, but China in particular is stalling. The Chinese unit was previously described as being “detached” from the company’s other production facilities, so perhaps it is even up for a quiet sale, as it reportedly doesn’t quite fit NOTE’s current situation (customers have moved from the Chinese factory to European factories in recent years).

- There are interesting discussions on the M&A front from time to time, but sellers apparently still have 2021-2022 valuations in mind, making it difficult to close deals.

- Some business shifted to future quarters right at the end of Q2.

- Investments continue as normal because the growth is definitely coming.

- Q3 will be weak due to the holiday season.

- Inventory will continue to decrease, resulting in further improvements to cash flow with a few months’ lag.

- The order backlog has shrunk significantly, but this is expected because in the current situation, customers don’t need to fear delays due to component shortages etc., which led to massive pre-ordering in 2020-2023 (and, as we know, led to bloated inventories across almost all industries).

- Paraphrased quote: “I don’t believe demand in 2024 is any weaker than in 2021-2023, but it seems some of the 2024 demand was already satisfied in previous years.”

The valuation is quite attractive compared to the numbers of the 2020s. Everyone has to consider for themselves whether the 2020s is even a valid comparison period for (Western) EMS companies, given the various tailwinds (and, of course, headwinds) that have been present.

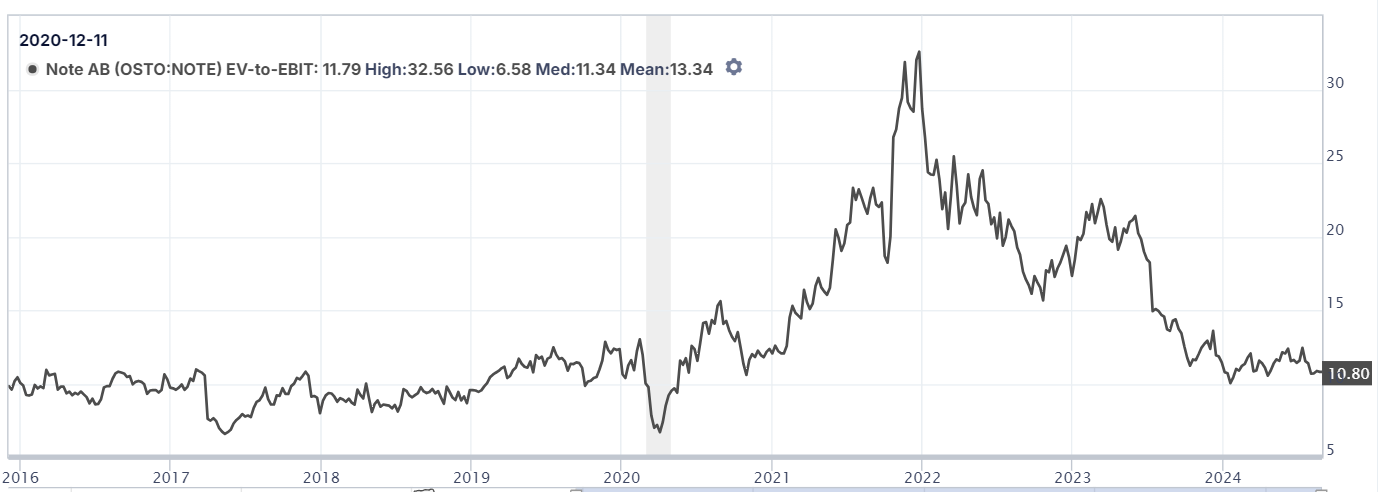

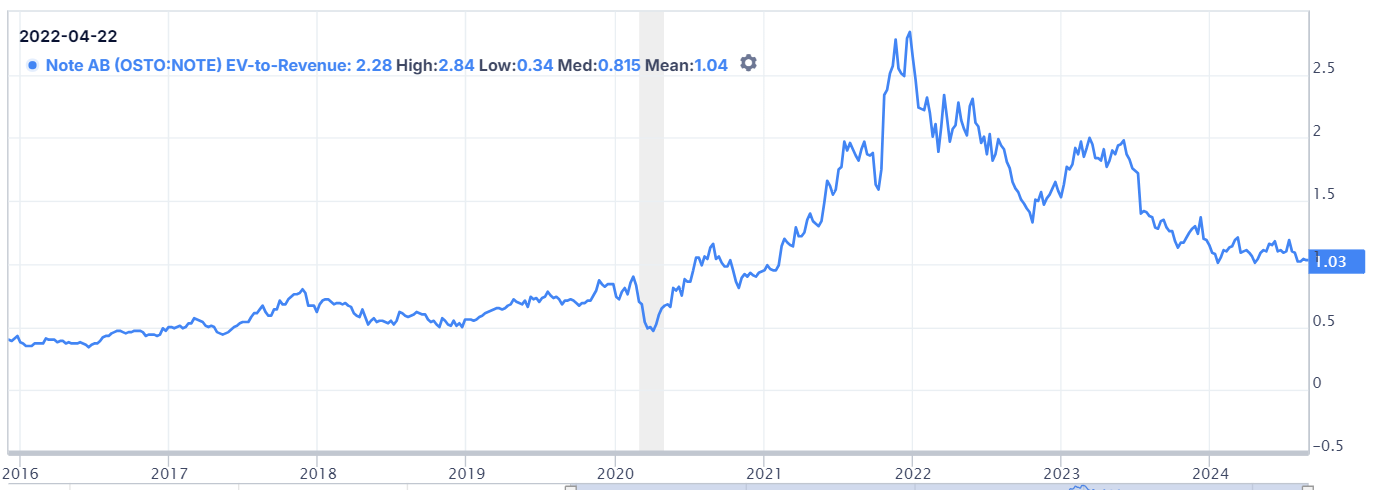

Looking at the current guidance, a quick calculation gives me a 2024e EV/EBIT multiple of 8.2 - 9.6 (top end of guidance - bottom end of guidance). EV/S on either side of 1. Doesn’t this already sound downright cheap?

Pair that with an optimistic 2025e scenario, where they reach the midpoint of the 2024 guidance and achieve 10 percent growth with an 11% EBIT margin in 2025. In that case, the 2025e EV/EBIT would be 7.3 and EV/S 0.8.

I’m almost tempted to buy NOTE shares.

Finally, a question for @Antti_Viljakainen and @Tommi_Saarinen; what are your thoughts on the valuation multiples of Western EMS firms over the last 10 years? And how do you relate the situation to the present day and future years? (Your answers regarding individual companies can, of course, be found in your reports, but if we could get some informal reflections on these companies as a group?)

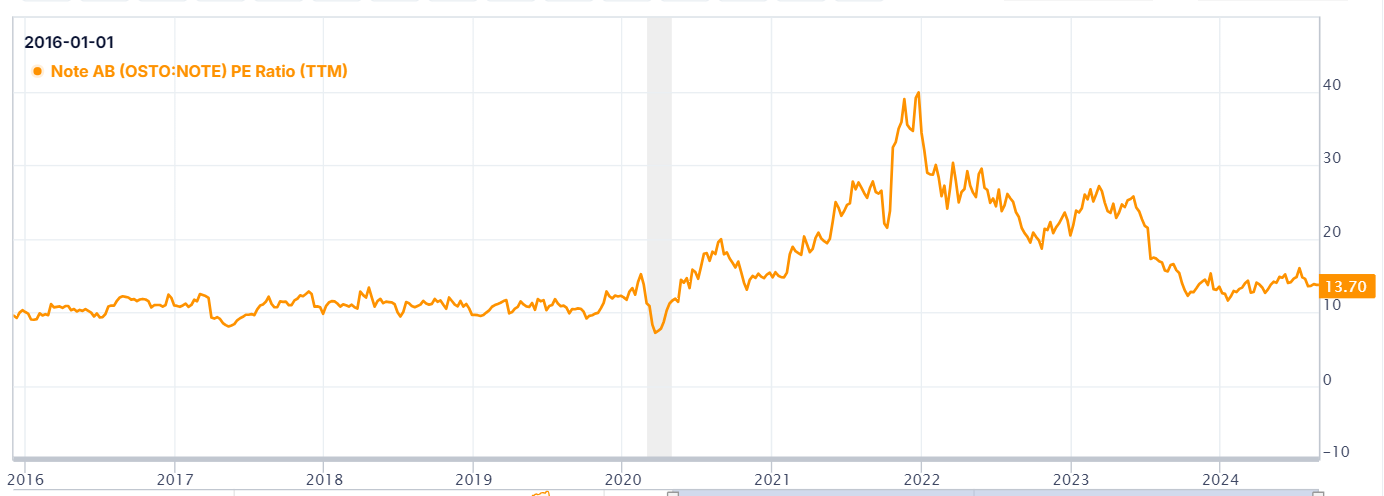

In the 2010s, multiples were miserable across the board. P/Es and EV/EBITs were chronically under 10, regardless of business development. Then, in the early 2020s, we probably hit some kind of valuation ceiling for EMS companies, when all the good Western EMS firms had multiples solidly in the double digits and usually started with something other than a one.

10 Likes

Hi!

Some informal reflection:

Compared to the realized return on capital, organic growth, and M&A opportunities, I consider those historical valuation multiples to be low. In my opinion, this is also reflected in the long-term stock returns of the companies, which have been amazing, especially for Note, Incap, and Kitron.

I’ve been mulling over the following possible explanations:

- The market has constantly priced in a high risk that hasn’t happened to materialize.

- Growth and profitability have consistently surprised to the upside, meaning the market has continuously priced in slowing growth and/or weakening profitability.

In my view, the risk level doesn’t justify such low multiples and high required rates of return. Factors that come to mind as increasing the investor’s required return:

- Poor visibility into the end product and thus the demand drivers, which makes understanding and forecasting the business difficult.

- The resilience of an electronics contract manufacturer in a sharper recession is a question mark.

Your screenshots also match my perception that current valuations are slightly above the longer-term average, but not significantly (adjusting for the post-Covid boom).

How does the present differ from the past? The short-term organic growth outlook is more challenging looking at those 12-month revenue growth forecasts. Incap’s growth is based on a weak comparison period and an acquisition, and I assume Hanza’s growth also includes an acquisition.

Source: Bloomberg

There are still plenty of M&A opportunities in the market, but there are also many listed contract manufacturers operating with an active M&A strategy, which should limit the value creation potential of acquisitions. On the other hand, this has been true for some time, yet good acquisition targets still seem to have been found.

Profitability levels fluctuate with volume, and if organic growth continues at the 0–5% level, I don’t expect major changes in profitability compared to history.

Thus, the sector’s multiples still seem attractive to me, considering the drivers supporting long-term demand. I recall the reasons for the chronically low valuation levels being speculated upon in extensive reports, and the industry’s poor reputation has been one factor that has come up.

Compared to Elcoteq, which went bankrupt in the 2000s, the customer structures of Nordic contract manufacturers are clearly more diversified, which limits the companies’ risk profiles. Additionally, these companies focus more on industrial electronics (Elcoteq was consumer electronics). Perhaps the Elcoteq case, among others, has left some scars on investors.

Antti is on vacation this week and he knows the sector significantly more deeply than I do. He will certainly be happy to comment on the topic when he returns. ![]()

25 Likes

To continue Tommi’s good reflection and to chew on the question posed by @Mauri, this analysis could be expanded to cover European countries more broadly. I chose one Swiss, one British, one French, and one German company (whose shares were just delisted from the stock exchange); all, however, are electronics contract manufacturers with a turnover of 200 million plus. Compared to the Nordic selection, the performance of all these has been anemic, to say the least.

Source: Refinitiv and the undersigned’s spreadsheet program

What if the markets are pricing high risk into Nordic contract manufacturers because the same business isn’t yielding results on the continent, and they don’t believe the northern dimension can indefinitely resist the industry dynamics? Globally, there aren’t many larger EMS companies with operating profit margins above 5%.

All of the companies have grown through acquisitions over the last five years, and organic growth in the near future (and past) is negative. However, all selected companies have also invested in new equipment (I included my personal favorite financial ratio in the table: operating cash flow divided by investments, as well as the ratio of operating cash flow to acquisitions). Every company has invested more in itself during the period than money has come in, so all the companies are also heavily indebted. Additionally, all except Cicor have also gone to the owners’ pockets to dig for additional funding.

In our Nordic flock, investments have been more moderate and yet growth has been better. I wonder why this is? Are our companies simply better managed? If we look at another of my favorite ratios, Sales-to-Capital (which in this case also includes working capital and acquisition prices), our European friends have all nonetheless generated more than one euro in sales for every new euro invested—with the aggressively growing KATEK reaching nearly two. For the Nordic peers, this figure would be nearly the same at 1.5 for all (except Scanfil, which is slightly higher due to fewer acquisitions during the review period). From this, one could conclude that there cannot be very large differences in sales prices to customers for similar services, which means the better profitability of Nordic companies likely stems from better cost management—but how could they all manage that across the board?

I don’t have any answers to give here, only more questions at most. In my opinion, comparing to contract manufacturers more broadly gives a much more pessimistic view of the industry than what we have been used to in our part of the world in recent years. If the industry as a whole is poor, and an outside investor doesn’t really have the opportunity to compare individual players’ customers with each other, it is relatively justified to price risk properly into the required rate of return. After all, this has already been realized in terms of valuation for many companies, and there are no dividends or buybacks to make up for it.

14 Likes

4 Likes

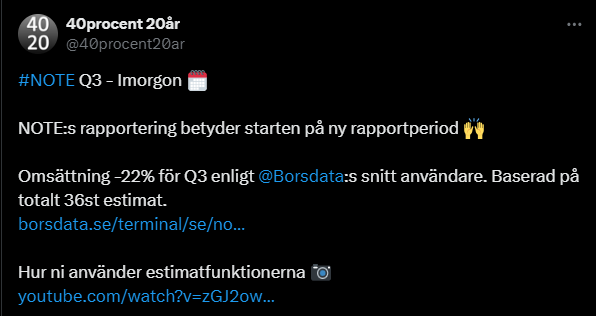

NOTE’s Q3 interim report will be published tomorrow.

- Revenue is projected to decrease by 22 percent in Q3, according to the average estimates of Börsdata users (approx. 36 estimates).

https://x.com/40procent20ar/status/1845539521175113947

3 Likes

@Isa_Hudd interviewed NOTE’s CEO in Swedish. If you don’t know Swedish, you can get some help from YouTube’s auto-translations (though they aren’t that good :D), but even those who don’t speak Swedish can get something out of it. ![]()

Johannes Lind-Widestam, CEO of NOTE, doesn’t dodge any questions as he summarizes the company’s third quarter. Everything from negative sales growth to profit warnings and personal share sales is put through the wringer! The plan forward is as clear as the rest of the communication: growth is the goal!

https://www.inderes.se/videos/note-q324-2024-ar-ett-mellanar

Contents:

00:00 Introduction

00:27 “A lost year regarding sales”: profit warning and postponed financial targets

01:50 Continued decline in China, Nordic upturn and expansion

03:00 Overcapacity risks? On historical downturns and production peaks vs the current situation

05:50 The industry’s underlying growth and trends

07:49 Potential M&As: supply exists, unwilling to overpay

09:50 Communications - it will happen, the only question is when

11:50 The “problem child” Greentech

14:00 On growth going forward

14:59 Comments on incentive programs + sales of personal shares in NOTE

This video can only be found on the Inderes Nordic channel, which also features English-language videos. ![]()

EDIT:

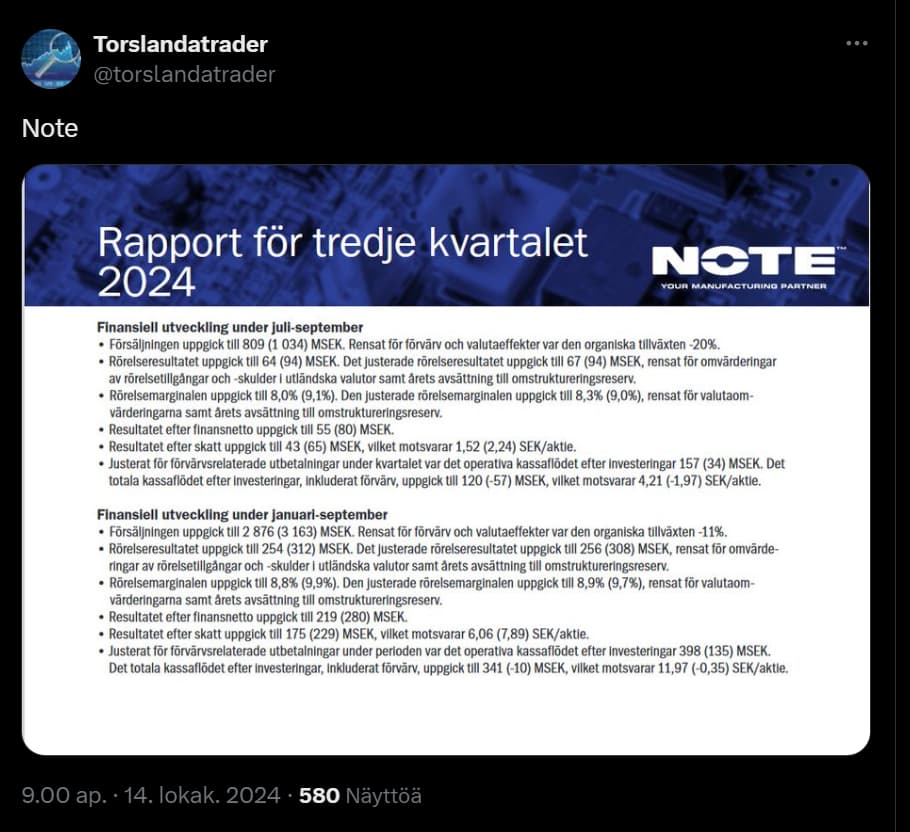

Below is a tweet about Note’s result, with a 2/5 translation below. ![]()

https://x.com/torslandatrader/status/1845706280712749330

5 Likes

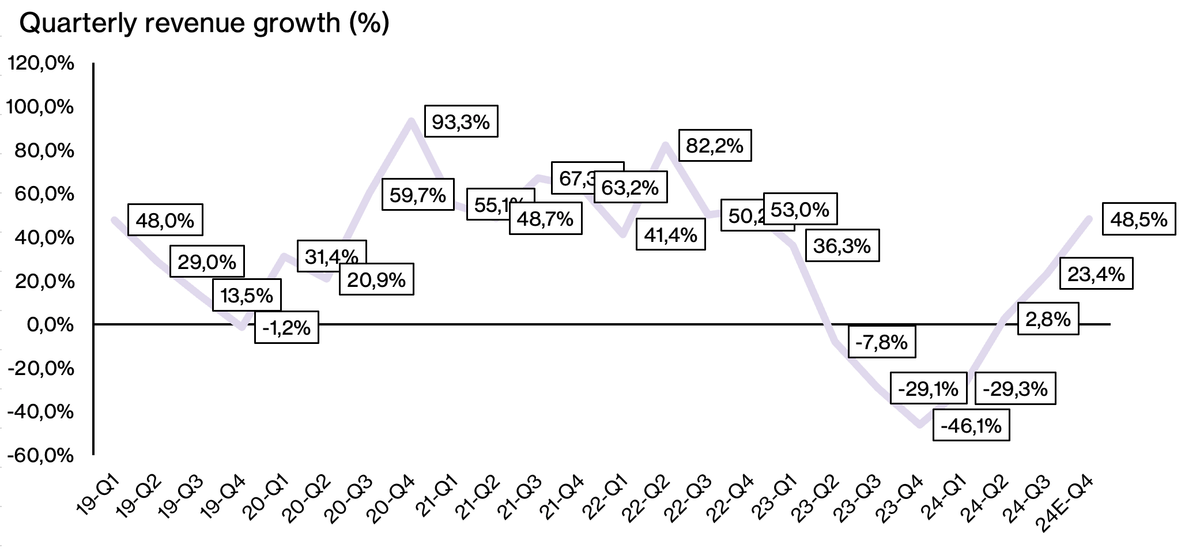

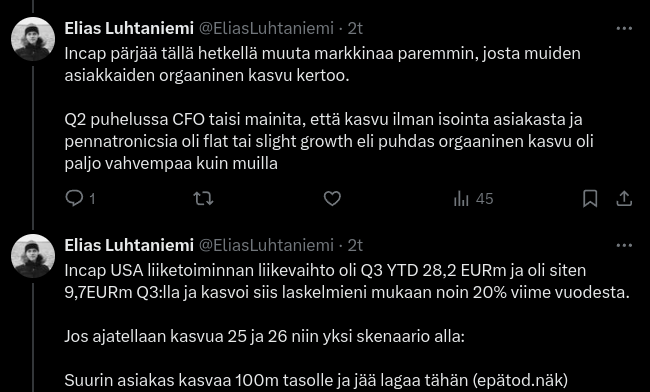

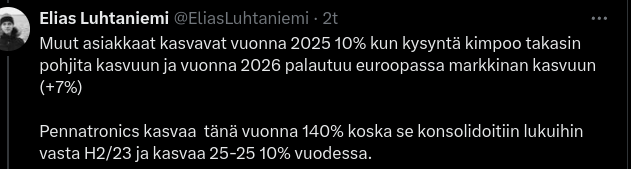

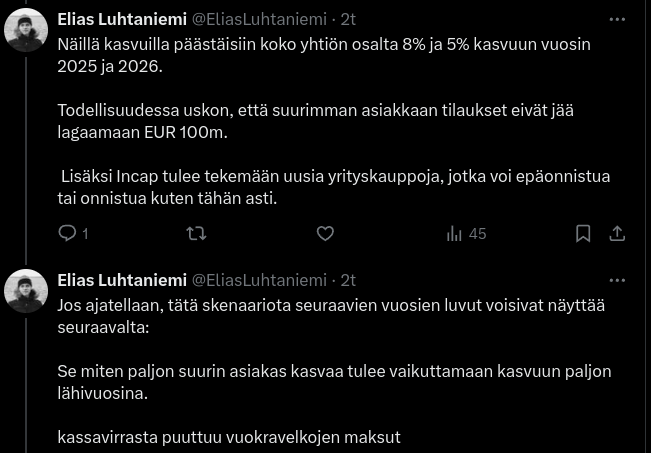

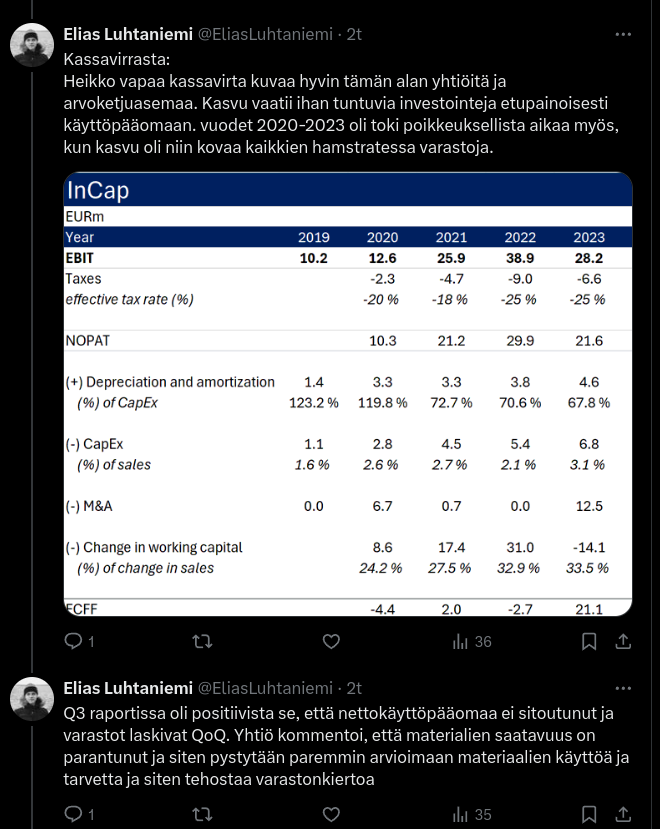

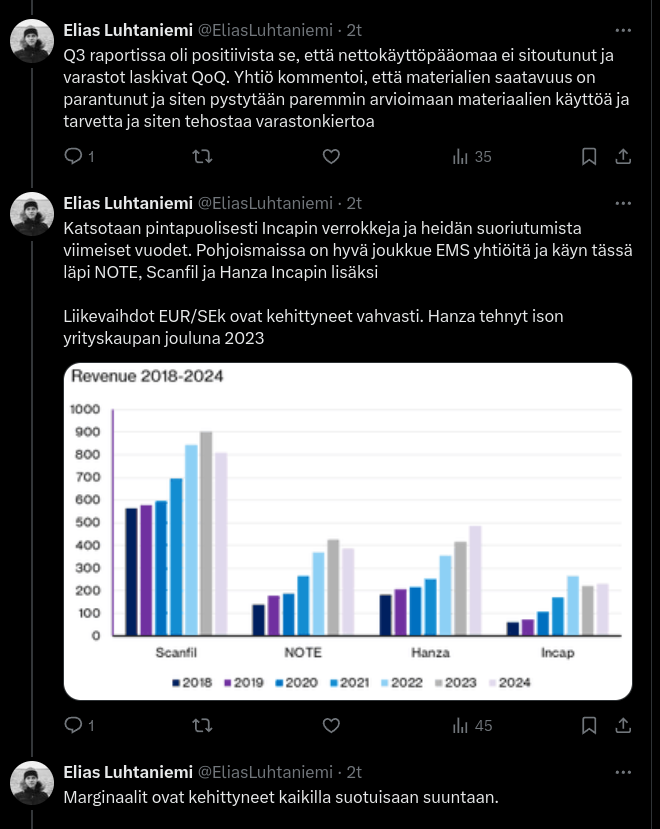

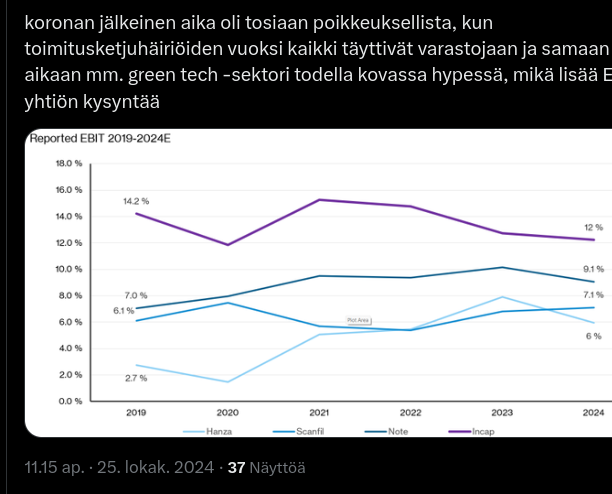

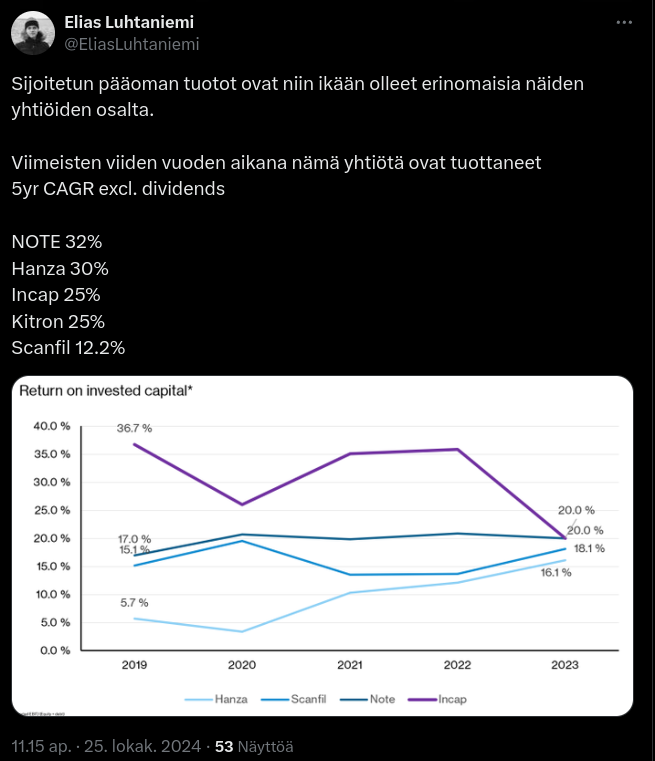

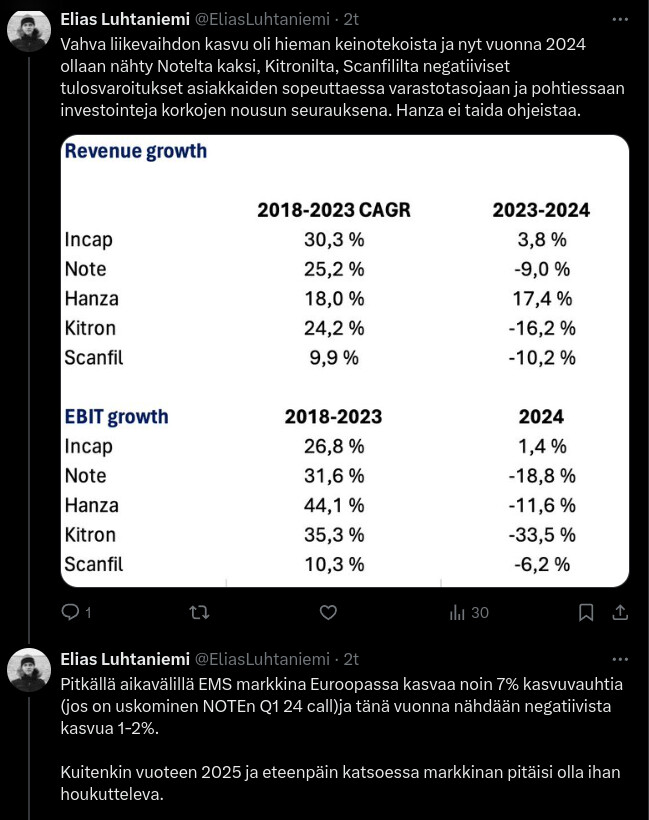

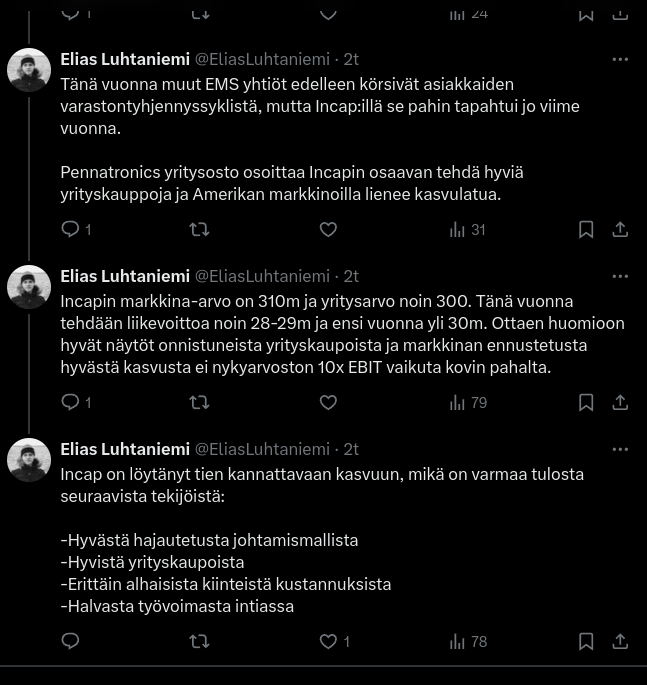

This was already in the Incap thread; of course, this tweet thread was mostly about them, but there’s also information on other companies in the industry here. @Elias_L has done a great job! ![]()

https://x.com/EliasLuhtaniemi/status/1849726314670063666

Rest of the tweet thread, but easier to read on X

6 Likes

I listened to NOTE’s Q3 results while out for a run over the weekend. Quite a lot has happened at NOTE over the past few months. Guidance has been revised a couple of times, the CEO has sold shares, there has been investment in a new Swedish factory, and I think there was a release about share buybacks (maybe routine; I haven’t checked whether they have actually bought any or not).

In light of that, the earnings call was quite calm. Johannes felt that the situation, demand, and potential are better than what the Q3 report was able to convey in terms of numbers. He remained convinced that growth will eventually come and that there is demand for their partnership. Customers have not canceled deals; they have only delayed orders.

(At this point, I have to note that regardless of the industry or company, everyone seems to be expecting that growth in the coming years will just fall from the sky when the time is right. I understand that falling interest rates etc. support demand, but there has been quite a lot of this “growth will come in due time” talk in Q3 calls.)

Johannes was downright proud of the profitability. And why wouldn’t he be, when they can achieve a respectable EBIT margin of over 8 percent on declining revenue. It’s not an Incap-level figure, but it deserves a small pat on the back.

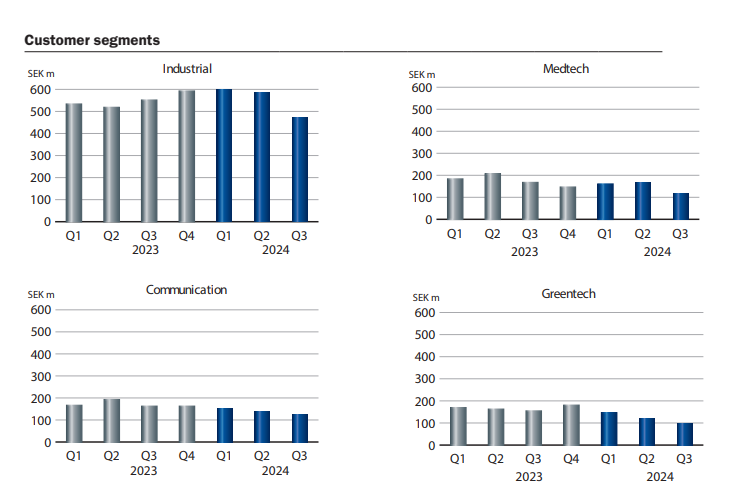

All segments are leaking:

In the big picture, the direction is right, but 2024 will be a transition year, and 2025 will be a struggle to reach 2023 levels.

If we stay roughly within the 2024 guidance, EV/EBIT will likely hover somewhere between 10–13, and P/E around 13–16. On top of that, if 2025 brings about ten percent more revenue with profitability (EBIT) at 10%, then 2025e EV/EBIT drops below ten and P/E is just over ten.

In the Q&A section, someone asked why they even provide guidance when their forecasts can’t seem to hit the mark. Johannes was convinced that guidance can still provide added value to owners and investors, but if the misses continue, they may consider stopping guidance altogether.

In summary: NOTE is clearly going through a more difficult period. A new growth phase and recovering profitability are expected in 2025. The potential is there. However, I expect that even if the bottom has been reached, the turn back to growth may be slower and bumpier than we might currently want to believe. In the long run, I still see NOTE as one of the winners in the EMS industry, and it will likely gradually grow into one of Europe’s leading EMS houses (if it cannot already be cautiously considered as such).

12 Likes

NOTE acquires in the UK. 12 million GBP turnover and a strong foothold in the defense industry.

4 Likes

An interesting observation from NOTE’s Lind-Widestam in the webcast. They are apparently not currently looking for acquisitions in Germany, because the weak situation in the automotive sector has led to several contract manufacturers trying to find customers from other segments. This, in turn, intensifies competition, which then drives down prices and profitability.

I’m noting this comment here, but this is a phenomenon I have highlighted as happening in Finland, for example, in the IT services sector. When competition intensifies, companies start acquiring more sales by lowering prices → everyone’

4 Likes

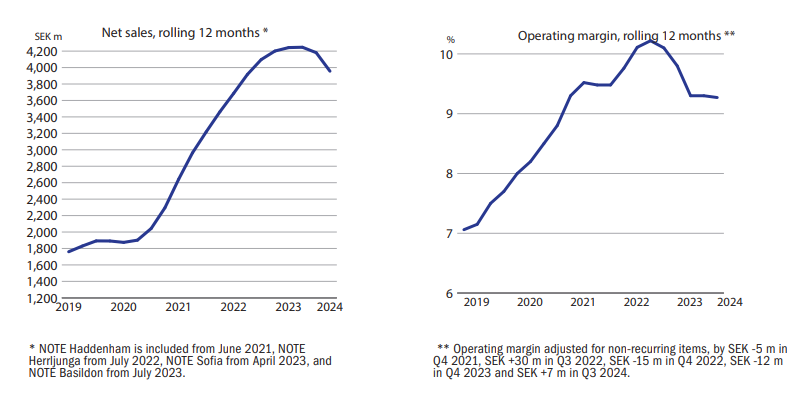

Recording the results for this quiet thread. Revenue was slightly over a billion kronor, profitability improved to 11%.

Financial performance in October-December

• Sales amounted to SEK 1,001 (1,025) million. Organic growth was -1%, currency adjusted.

• Operating profit was SEK 113 (98) million. Adjusted operating profit was SEK 114 (108) million, adjusted for revaluations of operating assets and liabilities in foreign currencies and acquisition costs.

• The operating margin amounted to 11.3% (9.5%). The adjusted operating margin was 11.4% (10.5%).

• Profit after financial items was SEK 109 (91) million.

• Profit after tax amounted to SEK 86 (73) million, corresponding to SEK 3.04 (2.55) per share.

• Adjusted for items affecting comparability, such as acquisition-related payments made and investments in the property in Torsby, Sweden, operating cash flow amounted to SEK 58 (140) million. Total cash flow after investments amounted to SEK -285 (124) million, or SEK -9.98 (4.35) per share.

Webcast

aaahhhhh

Dividend

• To maximise its financial freedom to act in the sector’s ongoing structural transformation, the Board of Directors is proposing that no dividend is paid for 2025.

8 Likes