I’ll start a thread for this small iGaming company with a short intro, as I’ve dug into the available materials a bit after my own purchase. It’s always better when the digging is done by broader shoulders.

Overview

EMB Mission Bound AB is a Swedish iGaming sector company that provides digital content, platform solutions, and white-label services to operators. The company develops and publishes video slots, aggregates third-party games, and offers payment system and user interface solutions.

In 2025, the company was rebranded from Embark Group AB to EMB Mission Bound AB. The change is driven by a strategic shift: from being primarily a developer of game content and individual products to a broader technology player. EMB thus aims to position itself as a technology and platform company in the iGaming ecosystem, not just a content provider.

Financial Development

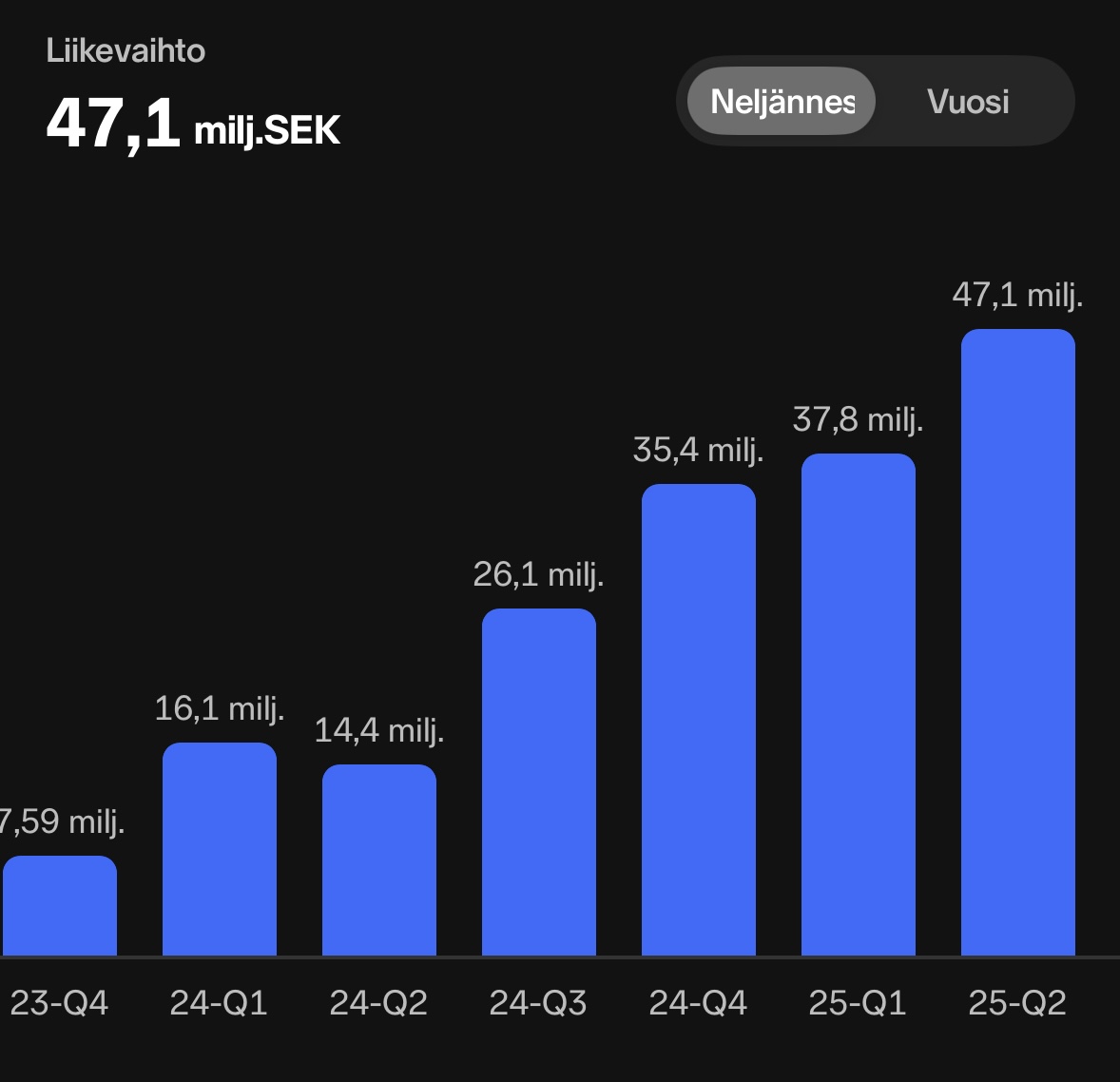

Revenue has been growing rapidly since Q2/2024. From Q2/2024 to Q2/2025, revenue grew by a robust 227%.

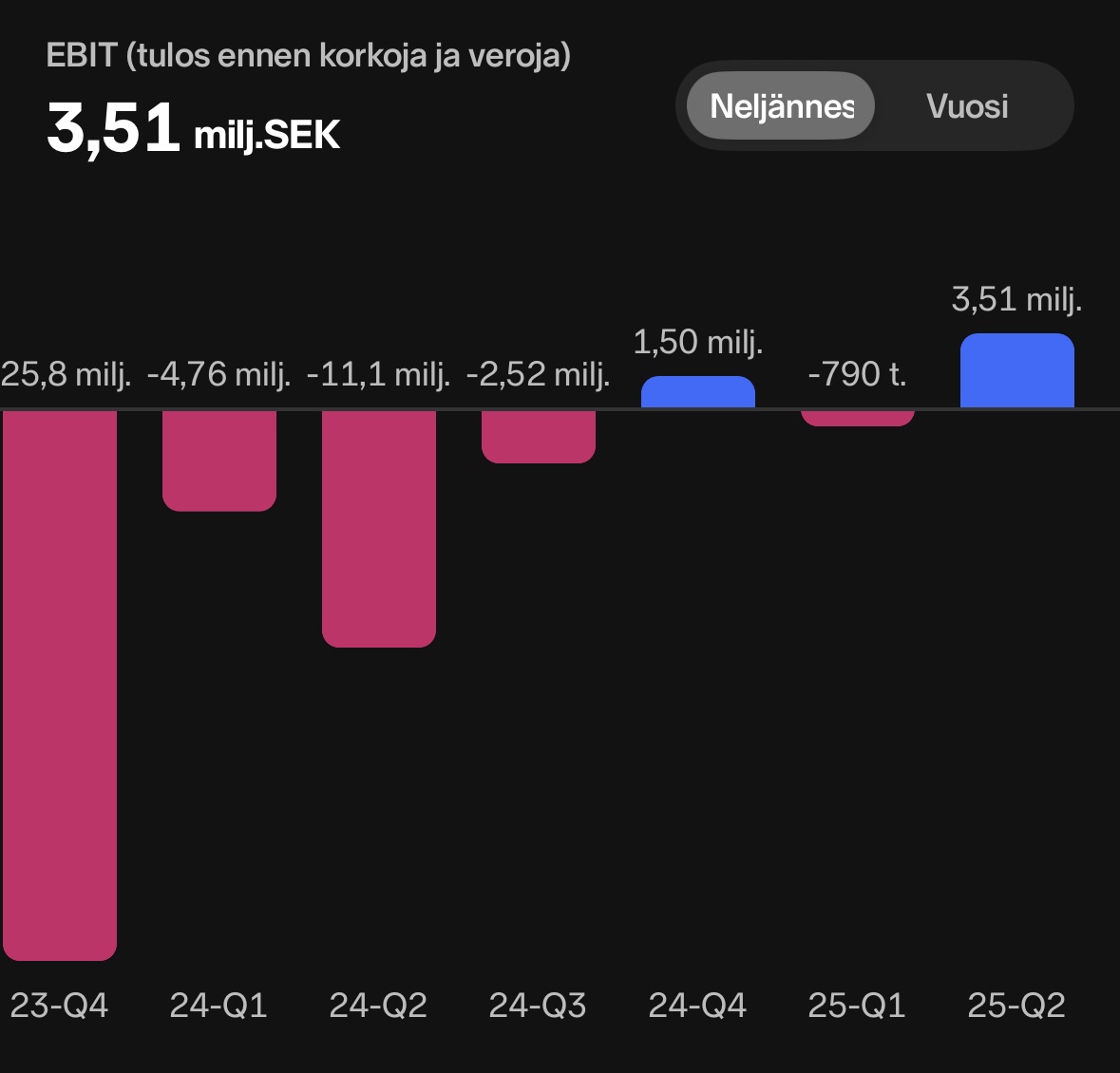

Q2/2025 was the third consecutive quarter with positive free cash flow. The balance sheet is debt-free. The turnaround towards profitability is currently underway. The company is currently undergoing an organizational restructuring, which incurred one-off costs in Q2 and is expected to affect the third quarter as well.

Drivers and Recent Events:

The new EMB RGS platform was launched in February 2025. It brings improved scalability, reliability, and modularity. The new RGS platform can also be offered to external game studios, enabling the expansion of revenue streams. Through the acquisition of Confetti Group, EMB expands its IP portfolio and development capabilities.

Risks and Considerations

Although the EBITDA result turned positive, the company does not yet have a long history of profitable operations.

Approximately 75 percent of revenue comes from the two largest customers, meaning that although the products and platform are widely available in the market, revenue relies on a narrow customer base. On the other hand, this also indicates significant revenue potential in new customer acquisition if current growth percentages have been achieved largely from two customers.

Pricing

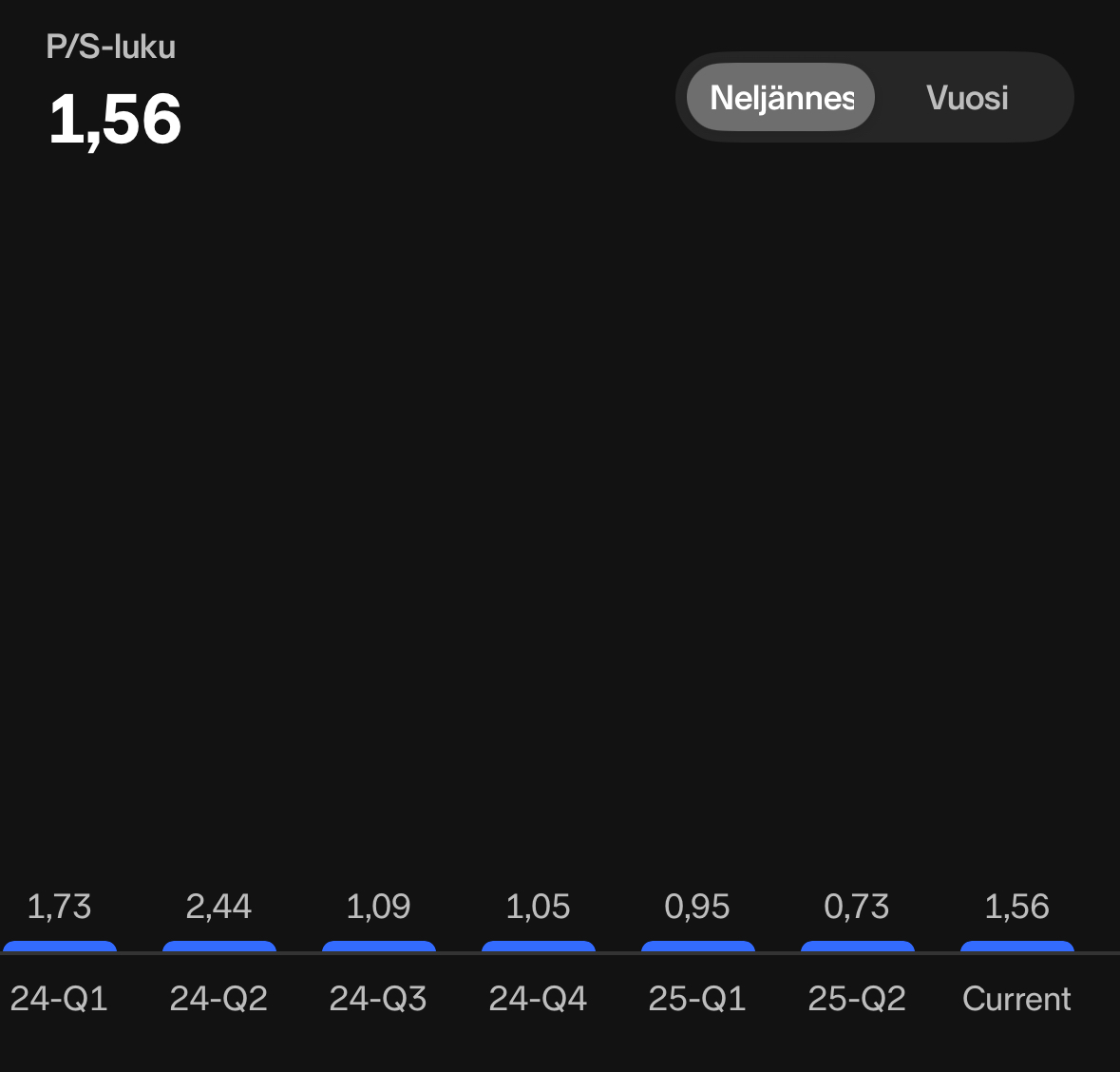

The current market capitalization is SEK 284 million, meaning it is still a very small player.

Below are screenshots from Nordnet related to the stock’s valuation.

Analyst Group’s Q2/2025 updated base case is 2.04 SEK.

My Own Thoughts

The investment case looks promising, but it largely depends on how long the current growth rate can be maintained. My own idea is to follow the case primarily through revenue development in the coming quarters. A scalable business rewards if growth continues.

There are 116 owners in Nordnet, so this largely flies under the radar of small investors for now. The company also doesn’t make a fuss about itself to investors, which partly makes it harder to follow. The industry is also unsexy and the company’s business difficult to understand, which may explain the lack of interest from small investors.