I listened to NOTE’s Q3 results while out for a run over the weekend. Quite a lot has happened at NOTE over the past few months. Guidance has been revised a couple of times, the CEO has sold shares, there has been investment in a new Swedish factory, and I think there was a release about share buybacks (maybe routine; I haven’t checked whether they have actually bought any or not).

In light of that, the earnings call was quite calm. Johannes felt that the situation, demand, and potential are better than what the Q3 report was able to convey in terms of numbers. He remained convinced that growth will eventually come and that there is demand for their partnership. Customers have not canceled deals; they have only delayed orders.

(At this point, I have to note that regardless of the industry or company, everyone seems to be expecting that growth in the coming years will just fall from the sky when the time is right. I understand that falling interest rates etc. support demand, but there has been quite a lot of this “growth will come in due time” talk in Q3 calls.)

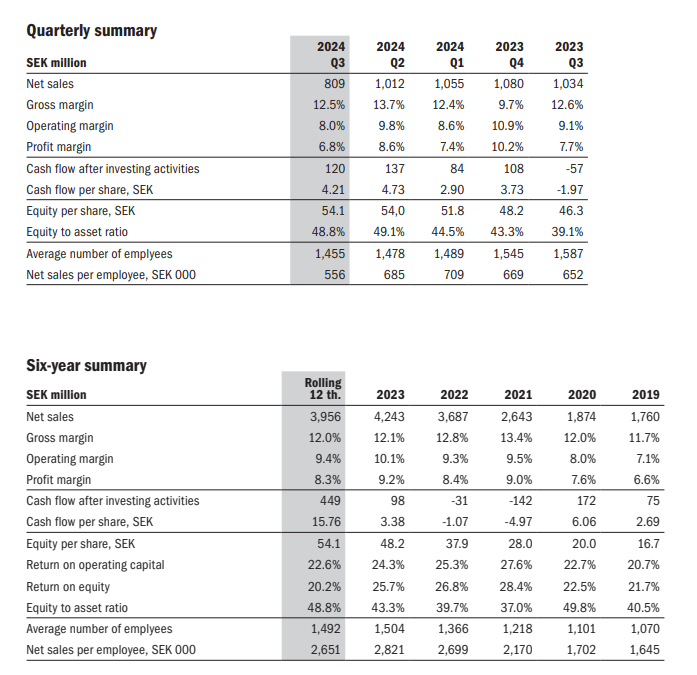

Johannes was downright proud of the profitability. And why wouldn’t he be, when they can achieve a respectable EBIT margin of over 8 percent on declining revenue. It’s not an Incap-level figure, but it deserves a small pat on the back.

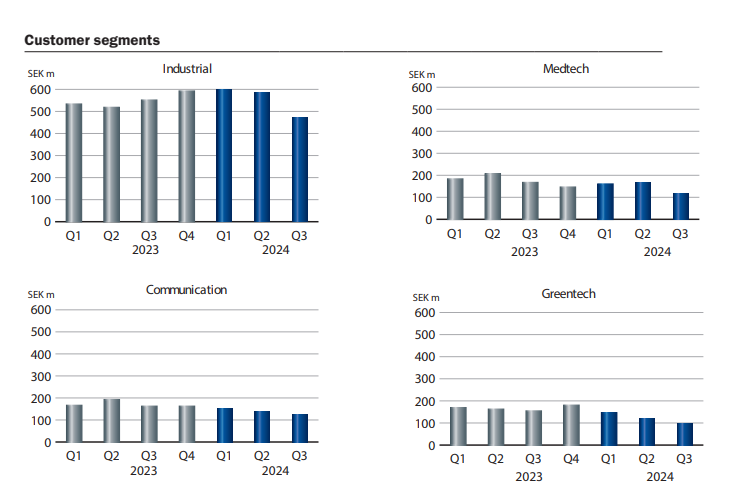

All segments are leaking:

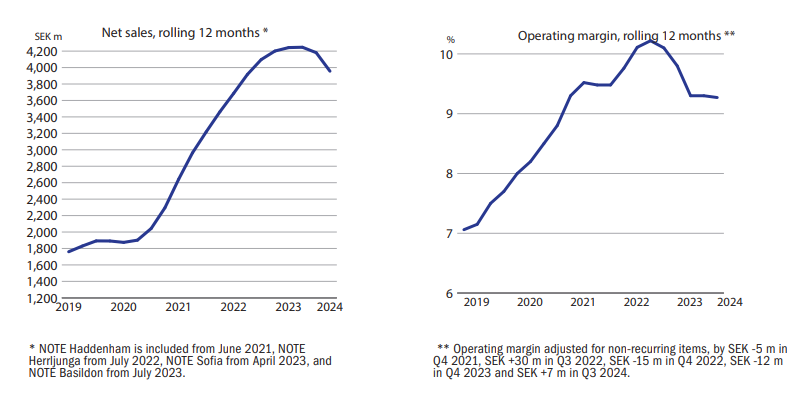

In the big picture, the direction is right, but 2024 will be a transition year, and 2025 will be a struggle to reach 2023 levels.

If we stay roughly within the 2024 guidance, EV/EBIT will likely hover somewhere between 10–13, and P/E around 13–16. On top of that, if 2025 brings about ten percent more revenue with profitability (EBIT) at 10%, then 2025e EV/EBIT drops below ten and P/E is just over ten.

In the Q&A section, someone asked why they even provide guidance when their forecasts can’t seem to hit the mark. Johannes was convinced that guidance can still provide added value to owners and investors, but if the misses continue, they may consider stopping guidance altogether.

In summary: NOTE is clearly going through a more difficult period. A new growth phase and recovering profitability are expected in 2025. The potential is there. However, I expect that even if the bottom has been reached, the turn back to growth may be slower and bumpier than we might currently want to believe. In the long run, I still see NOTE as one of the winners in the EMS industry, and it will likely gradually grow into one of Europe’s leading EMS houses (if it cannot already be cautiously considered as such).