I listened to NOTE’s latest earnings webcast at the end of last week (right after Incap’s equivalent). It wasn’t nearly as bleak as one might assume from the share price drop, the CEO’s share sales, and the negative profit warning.

However, I must add immediately that CEO Johannes’s commentary always seems to have a slight air of over-optimism, so it’s worth applying a small “safety margin filter” when listening to these NOTE events.

Nevertheless, in Johannes’s words, demand, the market situation, and the outlook for the coming years are much better than what can currently be reported in the form of figures. Regarding the acute situation, he said the end of Q1 was more difficult than the end of Q2, so perhaps the dip has already started to level out. About the coming years, he said he sees no reason why NOTE wouldn’t grow by double-digit percentages from 2025 onwards, doing exactly the same things as in previous years.

In addition to growth, he was confident that profitability will continue to improve. Regarding profitability, I must say that in my opinion, NOTE has protected it quite admirably in this otherwise weak situation.

A few of my other thoughts:

- Western production facilities are performing well, but China in particular is stalling. The Chinese unit was previously described as being “detached” from the company’s other production facilities, so perhaps it is even up for a quiet sale, as it reportedly doesn’t quite fit NOTE’s current situation (customers have moved from the Chinese factory to European factories in recent years).

- There are interesting discussions on the M&A front from time to time, but sellers apparently still have 2021-2022 valuations in mind, making it difficult to close deals.

- Some business shifted to future quarters right at the end of Q2.

- Investments continue as normal because the growth is definitely coming.

- Q3 will be weak due to the holiday season.

- Inventory will continue to decrease, resulting in further improvements to cash flow with a few months’ lag.

- The order backlog has shrunk significantly, but this is expected because in the current situation, customers don’t need to fear delays due to component shortages etc., which led to massive pre-ordering in 2020-2023 (and, as we know, led to bloated inventories across almost all industries).

- Paraphrased quote: “I don’t believe demand in 2024 is any weaker than in 2021-2023, but it seems some of the 2024 demand was already satisfied in previous years.”

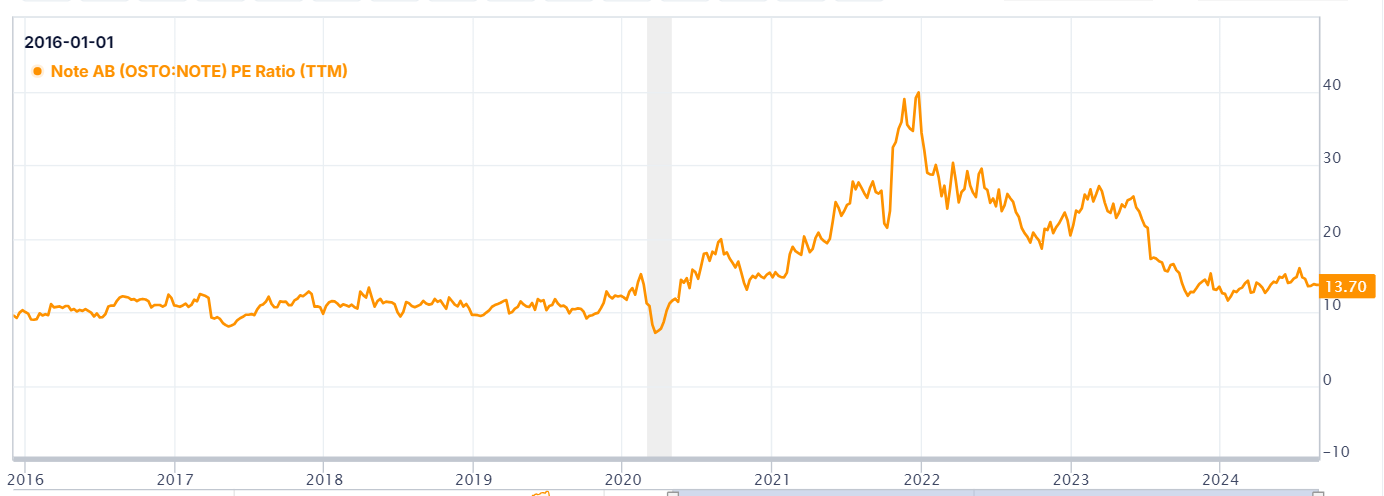

The valuation is quite attractive compared to the numbers of the 2020s. Everyone has to consider for themselves whether the 2020s is even a valid comparison period for (Western) EMS companies, given the various tailwinds (and, of course, headwinds) that have been present.

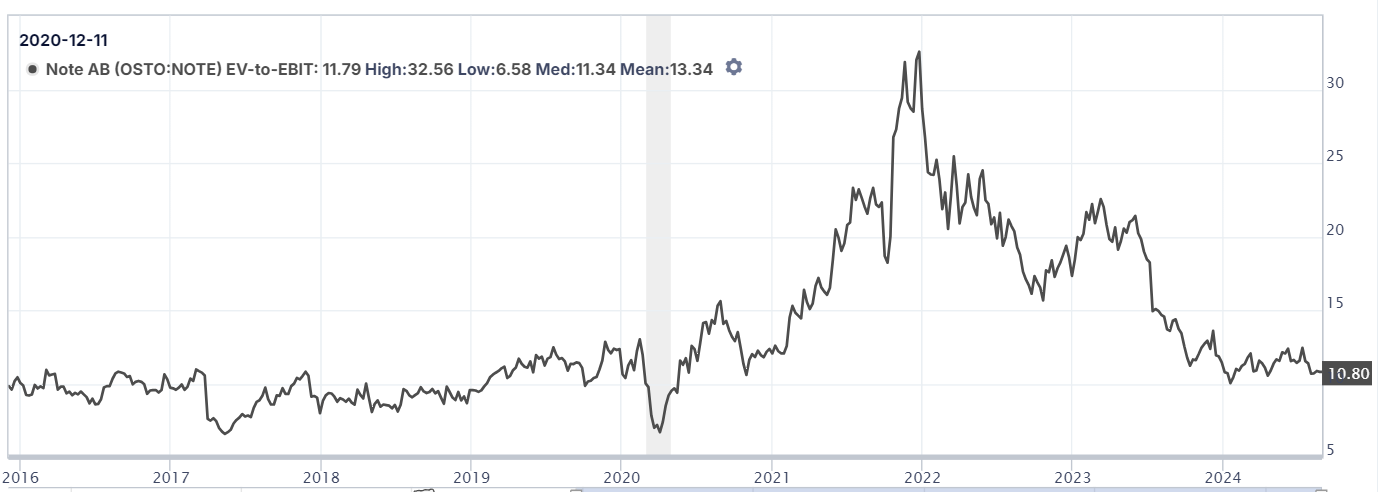

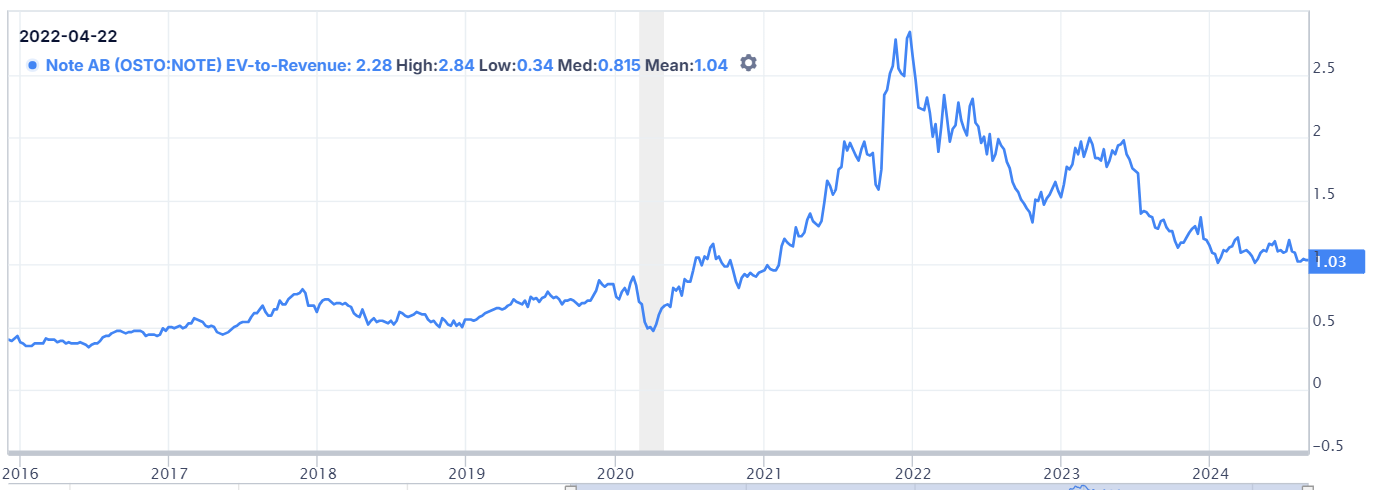

Looking at the current guidance, a quick calculation gives me a 2024e EV/EBIT multiple of 8.2 - 9.6 (top end of guidance - bottom end of guidance). EV/S on either side of 1. Doesn’t this already sound downright cheap?

Pair that with an optimistic 2025e scenario, where they reach the midpoint of the 2024 guidance and achieve 10 percent growth with an 11% EBIT margin in 2025. In that case, the 2025e EV/EBIT would be 7.3 and EV/S 0.8.

I’m almost tempted to buy NOTE shares.

Finally, a question for @Antti_Viljakainen and @Tommi_Saarinen; what are your thoughts on the valuation multiples of Western EMS firms over the last 10 years? And how do you relate the situation to the present day and future years? (Your answers regarding individual companies can, of course, be found in your reports, but if we could get some informal reflections on these companies as a group?)

In the 2010s, multiples were miserable across the board. P/Es and EV/EBITs were chronically under 10, regardless of business development. Then, in the early 2020s, we probably hit some kind of valuation ceiling for EMS companies, when all the good Western EMS firms had multiples solidly in the double digits and usually started with something other than a one.