North Media Oy released its Q4 results about two weeks ago, and now that exam week has started, I have some time to digest and update these results. My two cents:

The year 2022 went pretty much as expected, but the guidance was perhaps a slight disappointment for the stock market, at least initially.

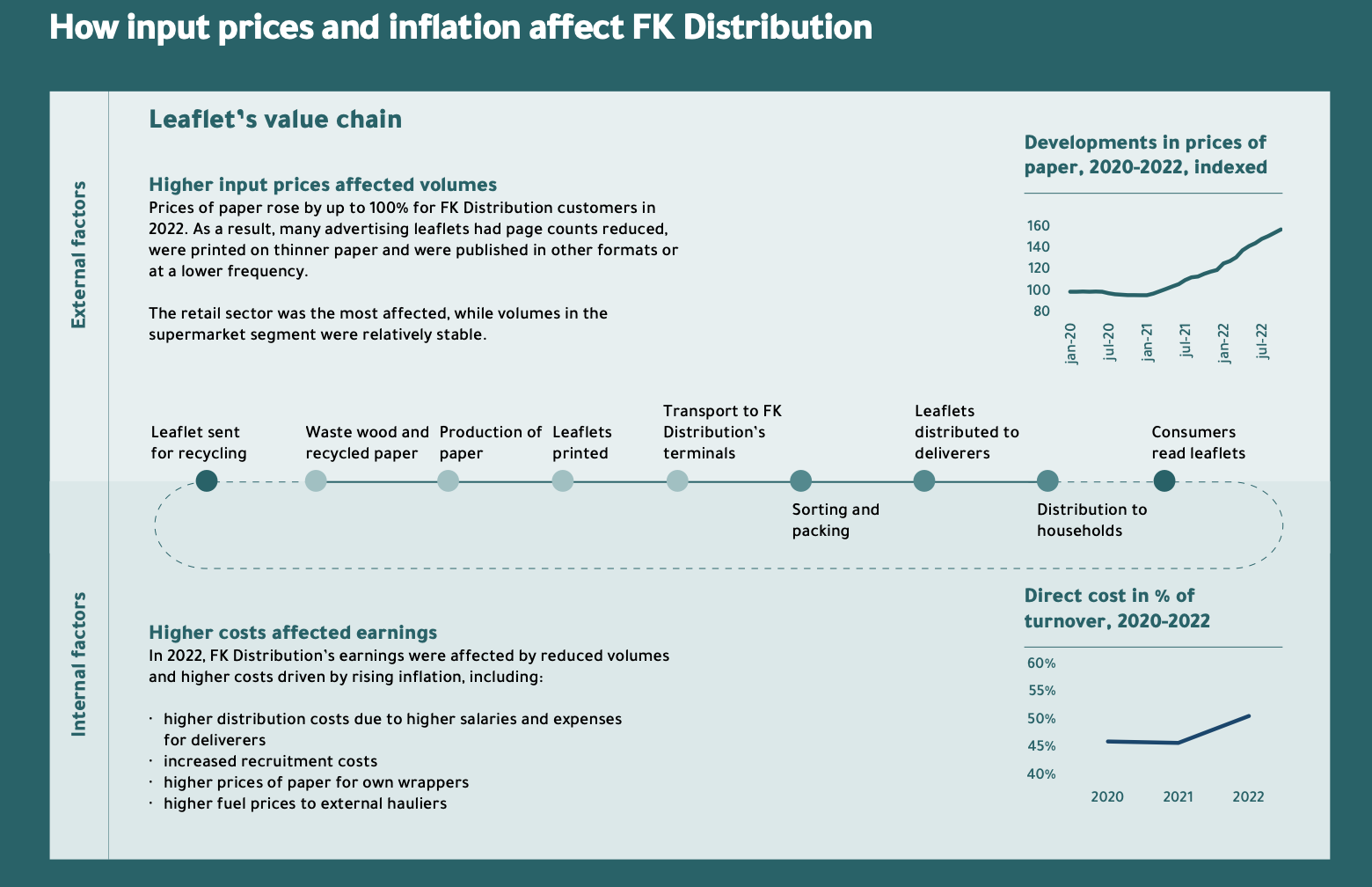

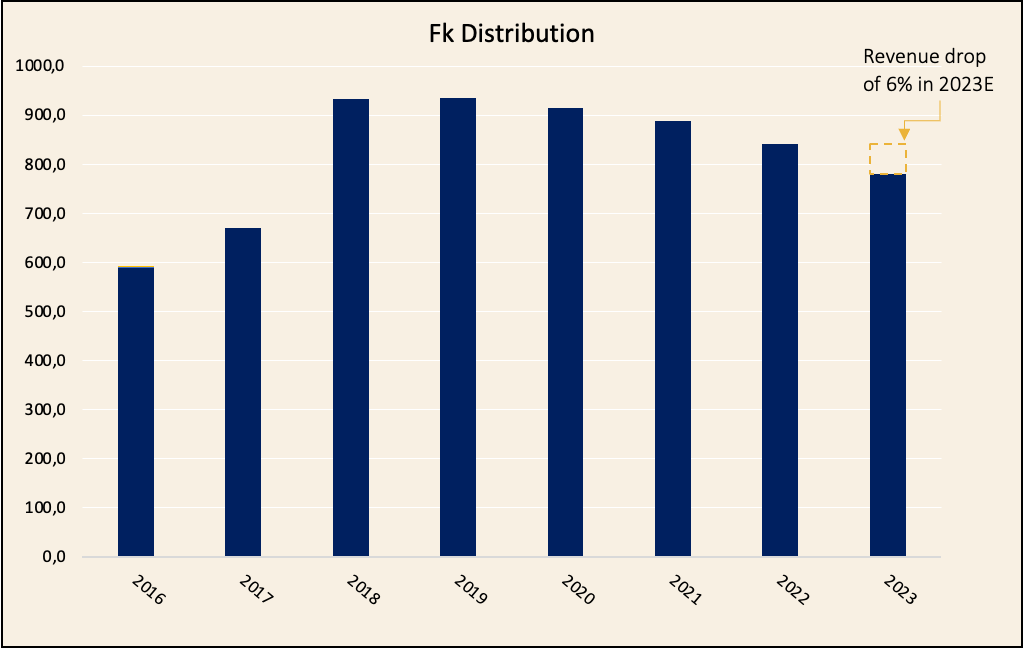

Fk Distribution

Revenue dropped by 6% for the full year according to the company, due to the price of paper rising by nearly 100%, which led customers to reduce ad distribution. The company reports that companies advertising consumer durables in particular reduced their ad distribution, while grocery stores maintained roughly the same level. Consumers, however, are looking for deals as purchasing power is under pressure. Some seasonal product sellers stopped ad distribution entirely.

- Price increases also affected the volume of local newspapers.

- A 2% price increase was implemented, but it was not enough to offset the rise in costs.

- Revenue from packaging services for Deutsche Post is growing slowly.

- The number of consumers registered for the NoAds program remained stable at 36%.

- Things happened in the political field, and 140m DKK was allocated to local newspapers through a new media agreement, which slightly reduces doubts about the entire business being at risk.

- In 2022, Fk Distribution launched a data-driven solution, providing advertisers with information on which areas would have interest in a specific product.

How does inflation show in costs?

2023

Fk Distribution reports on its strategic steps, which have remained unchanged even though the 2023–2024 guidance was lowered. Fk aims to develop its digital advertising platform (minetillbud) and offer this new data-driven advertising solution to advertisers to offset the chronically declining revenue caused by the fact that physical papers are read less year by year.

In the Q&A, it was asked why the result is dropping so “much” even though you say the need for ads is greater than ever as consumers look for deals.

A: The 2021 operating profit was, so to speak, too large, and such a margin should not be expected in the future. In '22, prices were not raised, which led to a margin drop from 28% to 22%. Now prices have been raised by 9.2%, but the margin drop to around 19% reflects poor visibility and declining distribution volumes.

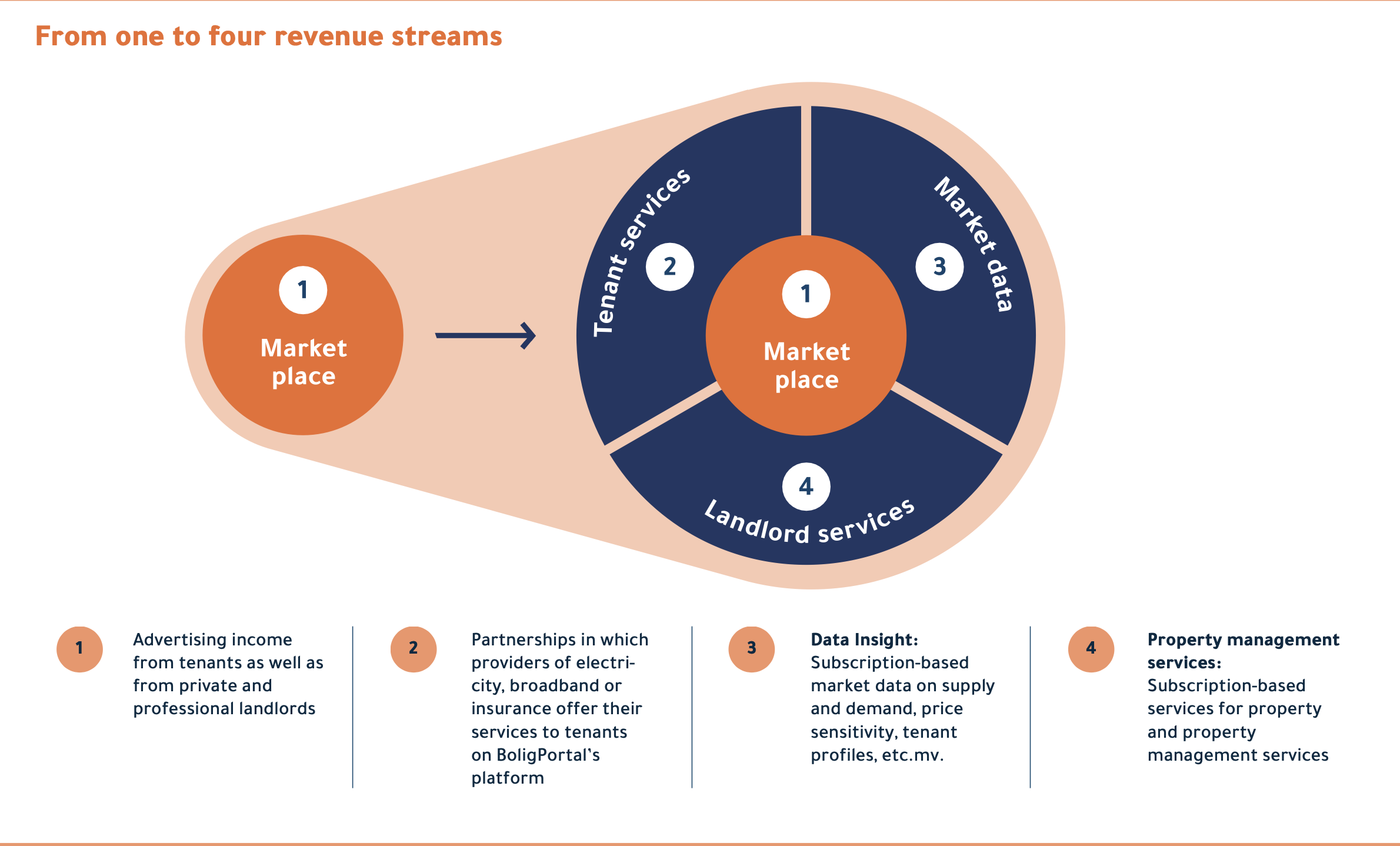

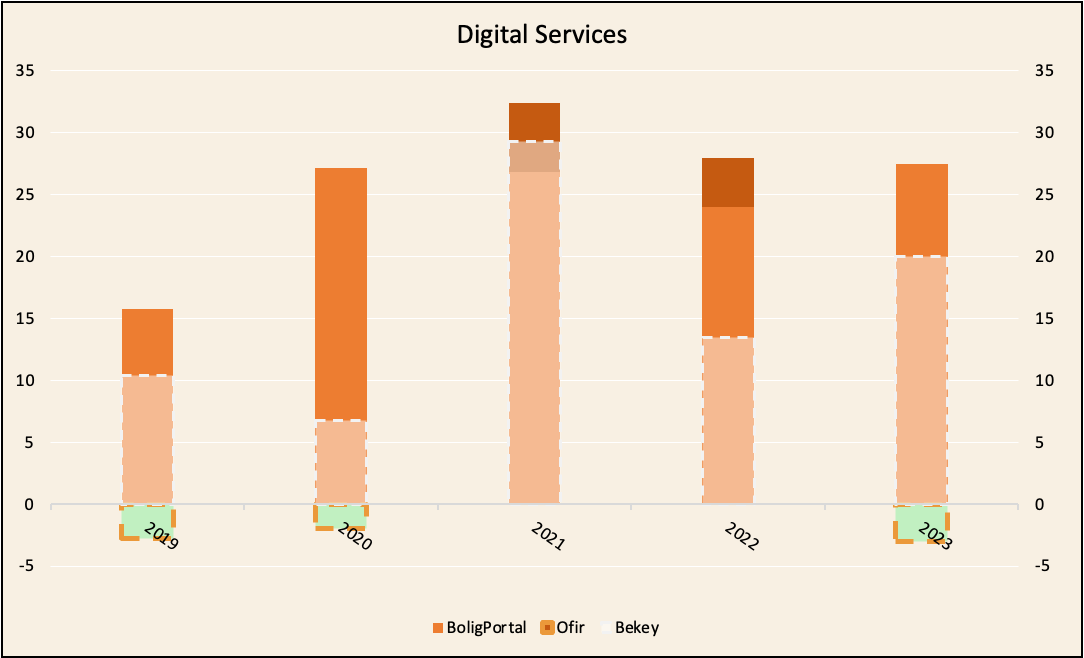

BoligPortal

The crown jewel of the entire company continued its strong performance. The full-year EBIT was 26%, and adjusted for costs from the Boligmanager acquisition, the EBIT was approximately 30%. Revenue grew by 11%.

The company is developing this marketplace for landlords and tenants, and reports that sales of new services grew by 140%, now accounting for 9% of revenue. Below is an image of this business.

Looks like smart business, at least here on PowerPoint.

2023

The company believes the core business will grow only marginally in '23, as people are not as willing to move in a high-inflation environment. However, the company guides for over 10% growth, meaning these new products are expected to generate good growth. From an investor’s perspective, it’s very positive that growth opportunities are being found.

Ofir

Revenue grew by 11%

EBIT 7%

Growth comes from the business of selling job advertisements. Public sector revenue grew due to price increases in addition to sales, but private sector revenue is reported to have grown only through sales growth.

The market peak last year was seen after Q1, and a sharp decline began after Q3, when volume dropped by 10.8%.

2023

Based on the Danish central bank’s estimate, job advertisements are expected to decrease by 10–12% next year. Ofir sees revenue dropping <10%, and EBIT will go slightly into the red. The data platform is being developed, and public sector jobs are being filled, as demand for these is expected to remain this year as well.

Below is an image of Ofir’s 2023 goals:

Bekey

Bekey failed to move the business forward as desired again this year. Revenue grew by 4 percent, and the result was -57% of revenue. The Homecare Dk segment is the largest segment, accounting for 83% of revenue. In this segment, 3 new contracts were signed and 12 contracts were renewed. Recurring revenue 65%.

A new CEO was hired in November; we’ll see if this makes a difference!

I personally like the Bekey product, and it sounds like this kind of solution is needed in modern society. Bekey’s NetKey is a cloud-based key management solution where you can either grant access to a key or remove it.

Bekey also has a mobile app connected to the NetKey cloud service, where these doors can be opened and you can determine who gets a key or who doesn’t! This solution is used to a great extent by healthcare personnel when visiting their clients.

Strategic Priorities

In Bekey’s situation, the important thing is just to get the solution scaled so they can start making a profit. So far, it has just been burning a lot of cash. For Bekey, winning municipalities as customers is crucial.

Q&A

They were asked when this crap will be divested.

A: We see potential here and are not divesting. It was also asked if there is a specific deadline for when it needs to become profitable or be divested, but there is no such thing; they are developing and spending money because they see potential here.

The dividend was cut from 5 → 4 DKK, why?

A: We want to keep plenty of cash in the coffers for new growth opportunities and to enable an attractive dividend yield in the long run.

The company does have money, and in my opinion, more isn’t specifically needed for new growth investments. I suspect the reason behind this is that the main owner wants to maintain and grow that stock portfolio.

The big picture of the company’s development with 2023E figures.

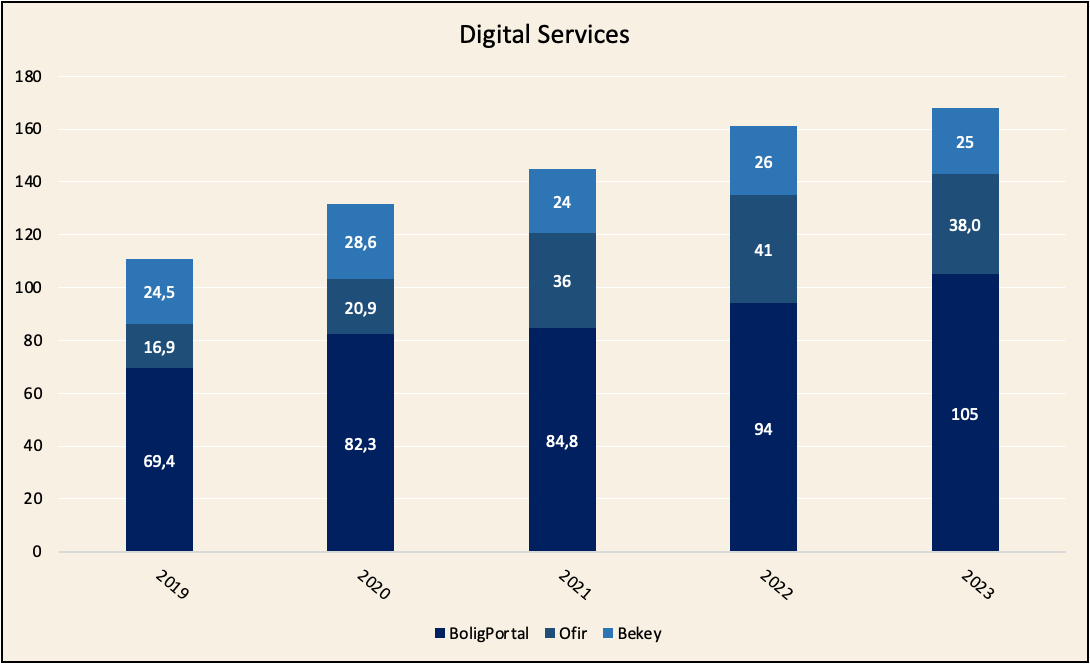

Digital Services growth:

By business unit:

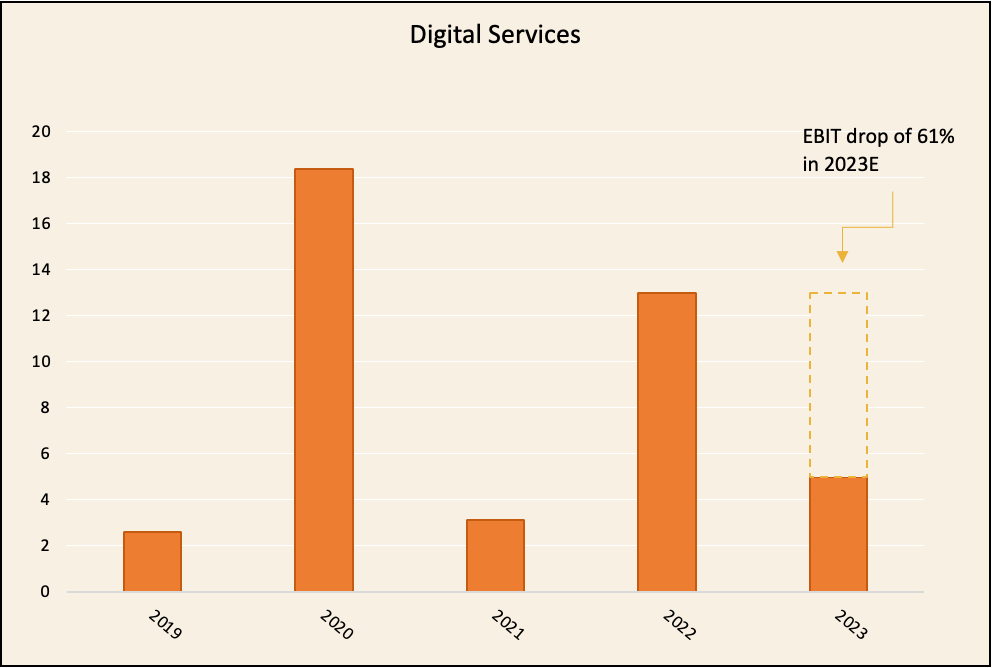

Profitability development:

From this, you can see how “beautifully” Bekey eats into DS’s profitability; Ofir’s profitability fluctuates a bit, but it’s not yet significant when looking at the big picture.

Fk Distribution

Profitability development

| Multiples | ||||

|---|---|---|---|---|

| Mcap (mDKK) | 1,253 kr | |||

| Total Debt (Mortgage) | 115.5 | |||

| Liquid assets (Cash & stocks) (31.1.23) | 827 | |||

| EV | 542 kr | |||

| Invested Capital | 331.1 | |||

| Book Value | 1058 | |||

| EV/IC | 1.64 | |||

| ROIC | 48.6 % | |||

| 2023E | ||||

| EV/EBIT | 3.6 | |||

| EV/FCF | 4.2 | |||

| P/FCF | 9.6 | |||

| P/B (31.12.2022) | 1.18 | |||

| P/cash (31.12.2022) | 1.5 |