Let’s open a thread for this too, as it might be of interest if the price is right.

“Stockbroker Nordnet has made an official decision to list on the Stockholm Stock Exchange. It anticipates the listing to take place before the end of this year. In the listing, shares will be offered to investors in Sweden, Norway, Denmark, and Finland.”

Wikipedia says the following about the company: “Nordnet AB is a Swedish stock and fund broker and online bank founded in 1996, offering services in the Nordic countries. In 2017, Nordnet had a total of 669,300 active customer accounts, of which 302,700 were in Sweden, 183,800 in Finland, 97,900 in Norway, and 84,900 in Denmark. Nordnet’s current owner is NNB Intressenter, which in turn is owned by the investment fund Nordic Capital Fund and the Öhman Group.”

At least I would be interested if the price isn’t totally maxed out.

-Similarly, for Finland, the Equity Savings Account (OST - osakesäästötili) has potentially increased active trading. This could, of course, have an impact in the longer term as well.

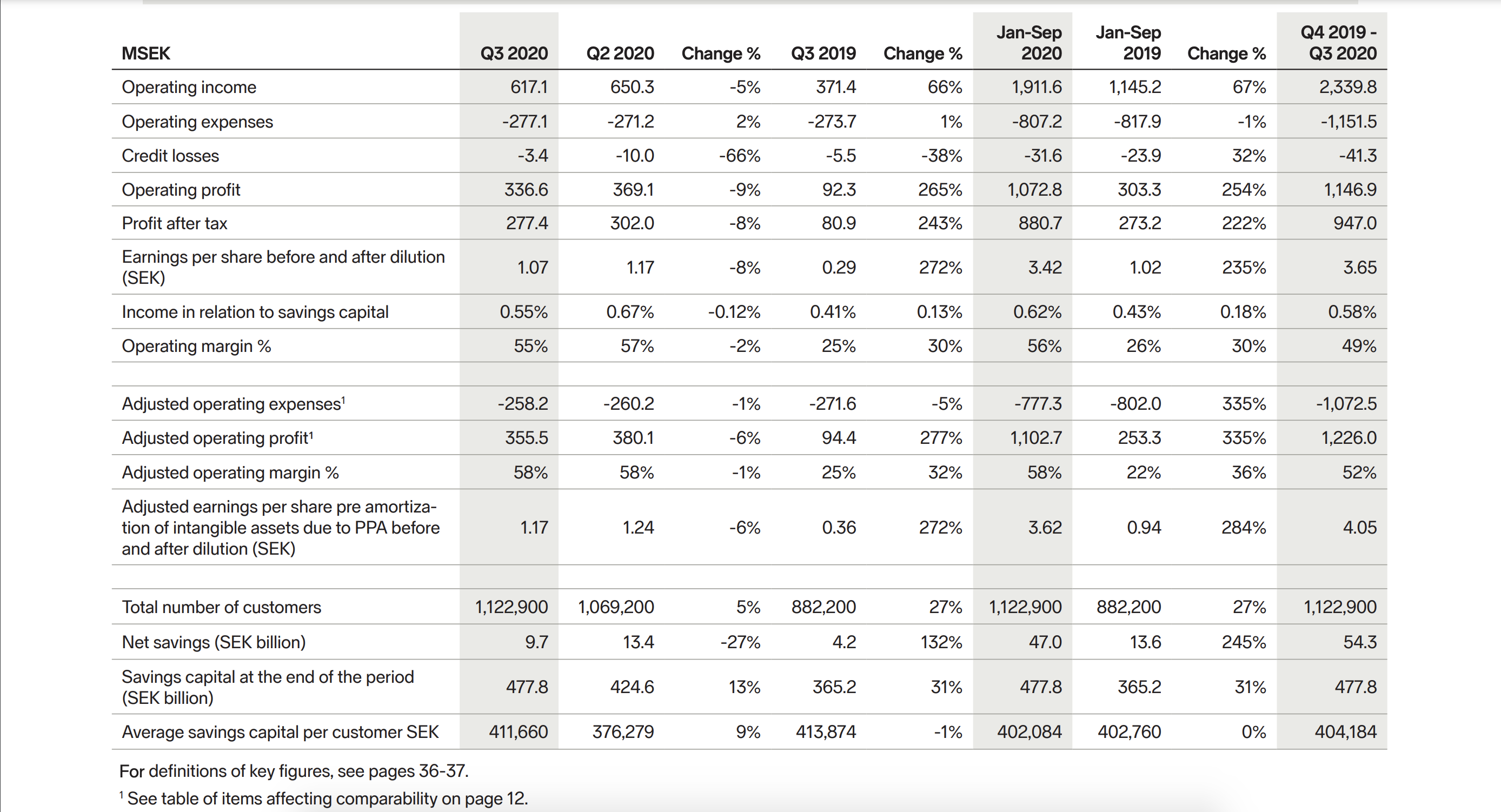

Numbers: Financial results in brief, January-December 2019

Operating income increased by 20 percent, amounting to SEK 1 573,4 million (1 310,4).

Operating profit increased by 167 percent to SEK 377.4 million (141.2).

Profit after tax for the period increased by 187 percent to SEK 339.5 million (118.1).

The number of new customers increased by 19 percent to 913,600 (765,200) customers.

As I understand it, Avanza is also listed on the stock exchange (yep: Ihre Datenschutzeinstellungen). How do you think Nordnet’s listing will affect its operations? Will transaction prices increase even more? Will portfolios become paid?

E:

Well, at least Avanza has a free account, so Nordnet would shoot itself in both feet if it went paid:

Margins don’t seem to offer much room for improvement, so growth should practically come from revenue.

Finnish OST accounts are a small piece of the overall pie, so they’re unlikely to have a big impact on the bottom line.

The entire market is very price-sensitive, and customers easily move to follow the cheapest fees. Practically, a campaign from a larger bank could take a significant portion of NN’s customers and revenue with it. → Significant risk to the business.

The pricing of the entire case will certainly take into account the track record of the last three to four quarters, which will significantly increase valuation multiples. However, it’s hard to believe that this rocketing growth would continue in the same way, as the golden age of COVID (and portfolio liquidations and refills) is over for now. If the dividend distributed in spring 2021 falls below 5% (and no significant inorganic growth is on the horizon), then this certainly cannot be considered cheap.

On top of that, there are fee-free brokers like Freetrade, BUX, and Trade Republic that are expanding their operations across Europe. They will also eat into the market.

There haven’t been many IPOs lately, so it’s worth participating in this one just for the IPO hype. So, subscribe the maximum amount and sell when trading begins. I plan to first play through the IPO phase, meaning I’ll take as many shares from the offering as a “windbreaker investor” can get, and then sell them on the first trading day, depending on how much the price rises. If there’s no opportunity for a quick profit on the first trading day, then I’ll do a more detailed analysis of the stock’s valuation.

On average, IPOs provide a nice quick profit, so this listing should also be played “the traditional way.”

Three new companies have been added to the main list of Stokis in October alone, and so far, at a superficial glance, these have not been money-making machines:

@Markakorva, that depends entirely on the offering price of the listing, doesn’t it? At what prices were those three, for example, collecting money before trading began?

From a fundamental perspective, Nordnet seems quite decent. Investing is constantly growing in popularity, and even middle-class young people are putting their money into the market. This also means that more competition is bound to emerge, and I don’t think it will be long before “free” services gain popularity in the Nordic countries as well.

I don’t know. As I said, a superficial scratch of autumn events on our western neighbor’s stock market.

I doubt they were even publicly collected, at least not for all three. I just barked in my morning grumpiness when they directly recommended buying everything you can because it’s an IPO.

Apologies for the off-topic, but a little caution regarding recommendations, tack

So Nordnet is returning to the stock market after a few years’ break. I’m sure one can find the price at which Nordnet originally delisted from the stock exchange.

It’s an interesting listing in itself, and a bit different from a traditional commercial bank.

I had Nordnet in my portfolio for a while when it was last listed on the stock exchange. My thinking at the time was a Lynch-esque “it works well and attracts new customers like flies to a carcass”. However, in terms of returns, it was quite a disappointment back then; I believe I even sold the shares before the takeover bid, so that didn’t go well either.

I haven’t looked into the background in more detail yet, but I have a rather cautious feeling about this. Could the biggest growth of popular capitalism already be behind us? Customer service in Finland is actually quite poor, pricing is not very competitive, so we might lose out on profits in the future if a price war starts.

“The Offer values all shares in Nordnet at SEK 6,651m”

I don’t know if there were any more offers after that or if it went through at that price… Kauppalehti might have the answer, but I don’t have reading access

I’ve had pretty good experiences with customer service.

The price is probably a bit of a personal question. With Nordnet, you can get quite reasonable fees with private banking, and you even get Inderes included for free. As I understand it, the private banking threshold is the lowest, at least compared to traditional banks. Honestly, I haven’t really looked at these Mandatum services and such. And of course, Nordea’s private banking has been quite successful in comparisons: https://www.inderes.fi/fi/tiedotteet/nordealla-suomen-ja-pohjoismaiden-paras-private-banking

What caused difficulties with Nordnet during the Euro crisis and the corona drop was that the service was sometimes down due to “a large number of users.” In my opinion, that’s such a radical issue that I even considered switching services both times, but I didn’t end up doing it. Probably laziness.

Yeah, that’s how it was. Of course, you have to remember that the number of shares might be different now, so it’s worth comparing the valuation of the whole company when that information becomes available.

Markakorva, international research results have for decades provided clear evidence that IPOs, on average, offer quick profits by subscribing to the stock and selling it on the first trading day. This anomaly has existed for decades, so I don’t believe it would have disappeared this year.

On average, yes, but not always. A lot depends on the timing and the IPO valuation. So it’s good to use your own judgment and not blindly trust the IPO magic. For example, Bilot wasn’t a very effective quick profit target in the spring, thanks to the corona drop.

Yes, but the data must be understood and applied correctly. If an anomaly does not disappear with extensive knowledge, there is a reason for it.

The basis of the strategy is that at the time of an IPO, there are usually more buyers than sellers. In a desired IPO, you get fewer shares than you want. The price quickly rises. In a bad IPO, the subscriber gets the amount they subscribed for, and too many people want to get rid of them. In the absence of demand, the price collapses.

As a strategy, subscribing to a large number of shares so that you get the desired amount in a good IPO is bad because if you hit a miss, you get many times the shares, and the damage is significant. Correspondingly, the return on shares received for a hit is good, but the volume is small. Therefore, the average does not describe the effectiveness of the strategy with very large subscriptions, and scalability is poor.

Unless one can better sense good IPOs than usual, going blindly after an anomaly is dangerous.

However, reliable coffee money can always be obtained this way because limiting the subscription to the minimum amount or close to it removes the risk of a large loss, while even the very best offering still provides a fixed minimum number of shares. In that case, the average already describes the realized result quite well.