Meltwater sparked discussion on the forum and is a company I’m partially familiar with from its previous operations, alongside the Esmerk and M-Brain services at the time. I had already been thinking about researching these more thoroughly as investment targets, and now I got the necessary motivational push when the company’s name came up in the Buy/Sell thread.

Meltwater is originally Norwegian, with its current headquarters in San Francisco. Some sources, however, list the HQ location as the Netherlands ![]()

It’s listed on the Oslo Stock Exchange, with a possible dual listing coming to the US market.

The IPO was on 02.12.2020, after which the stock price has fallen sharply.

IPO Prospectus, contains significant essential information about companies at the time of listing:

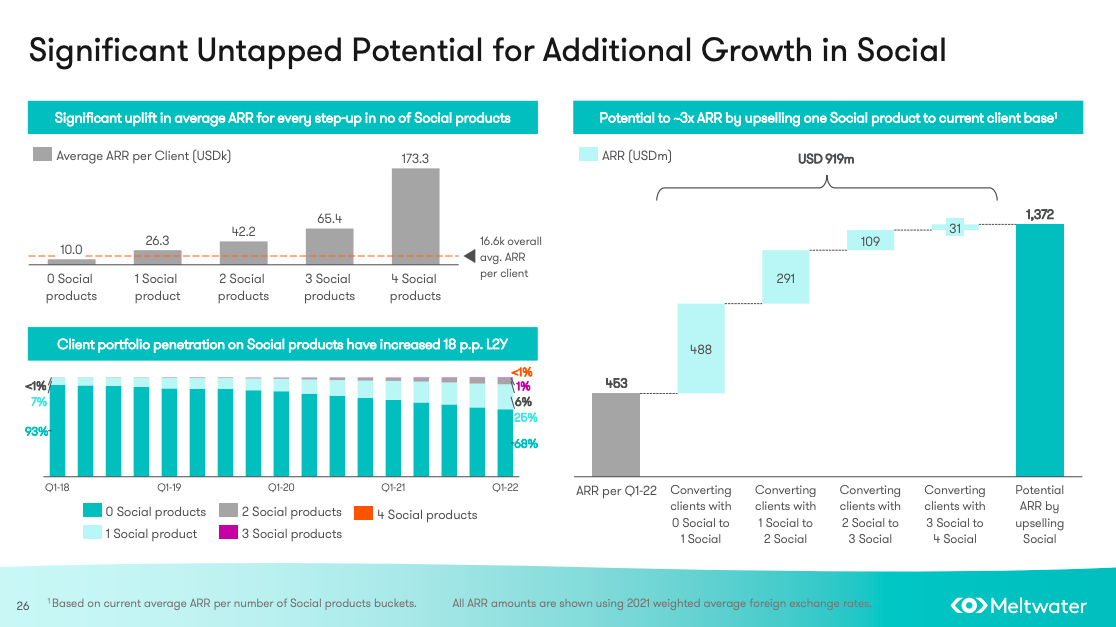

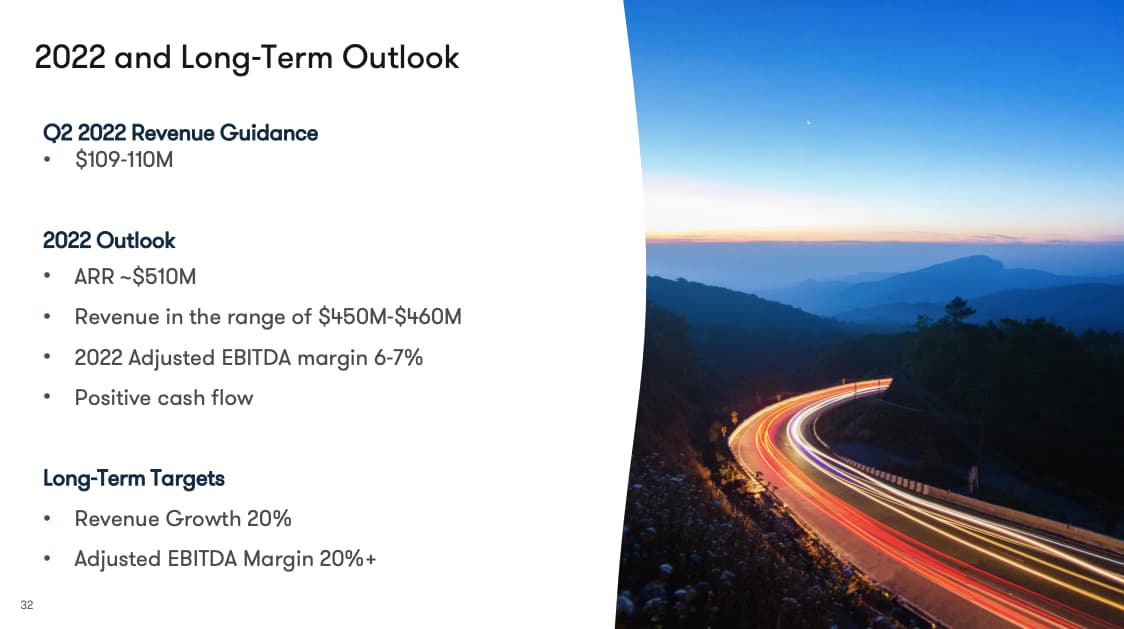

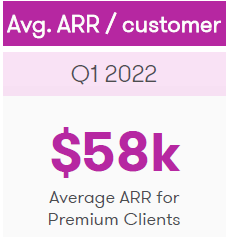

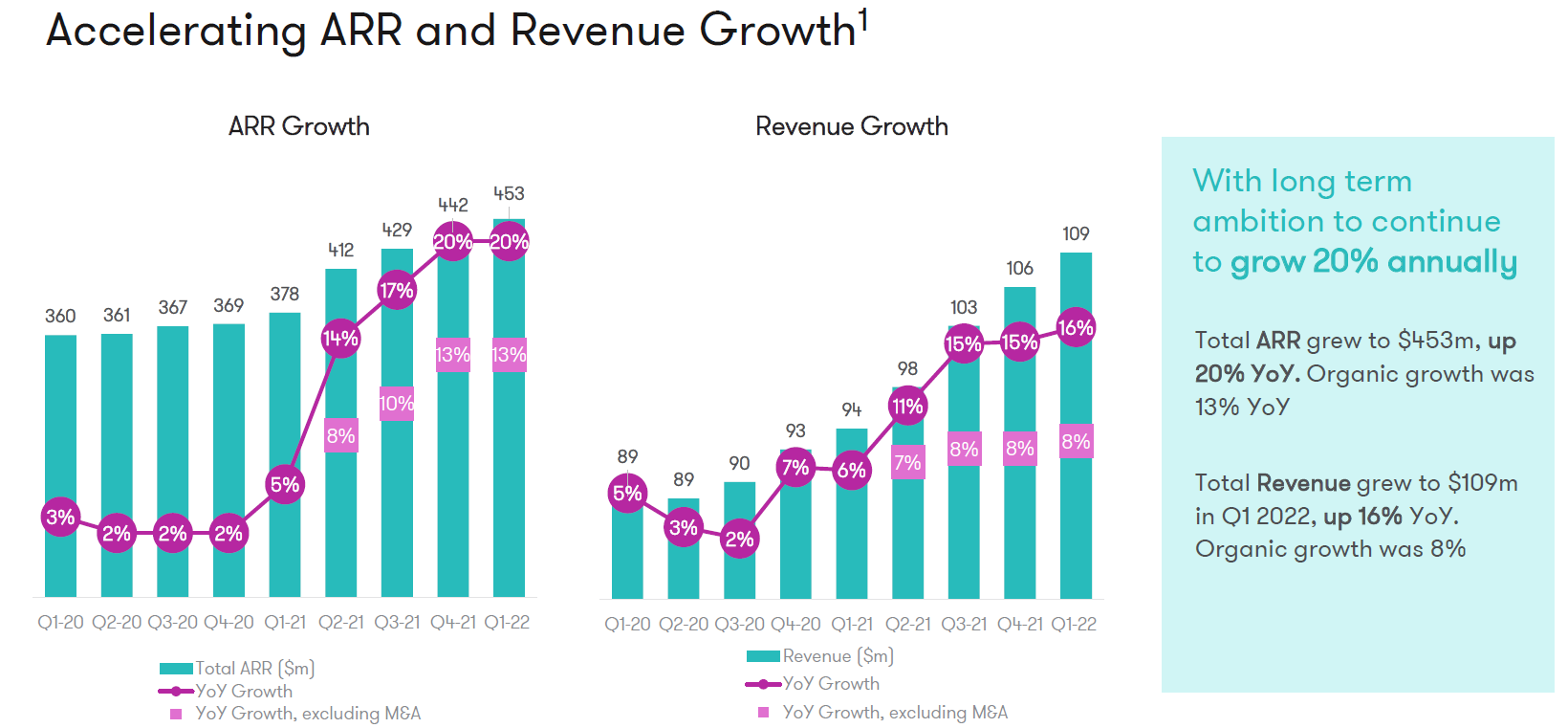

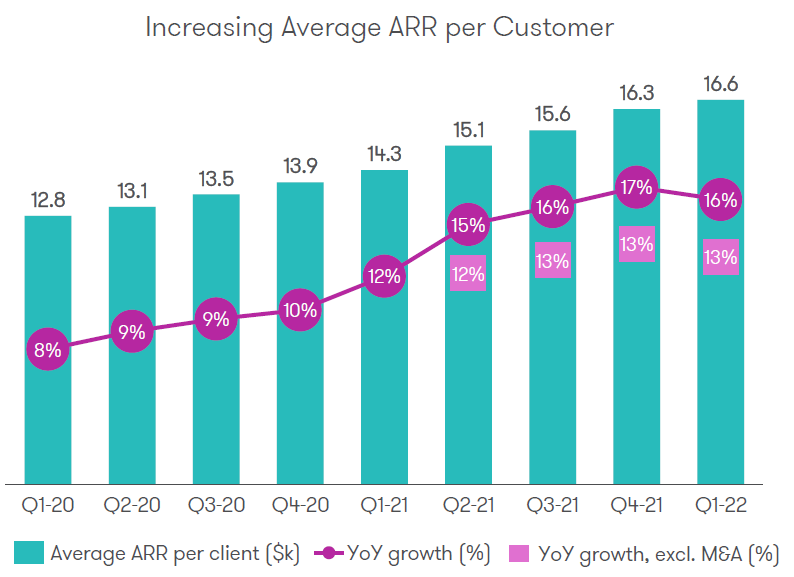

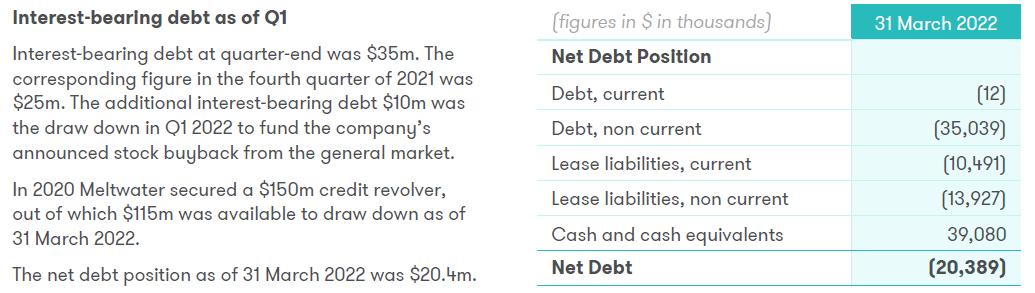

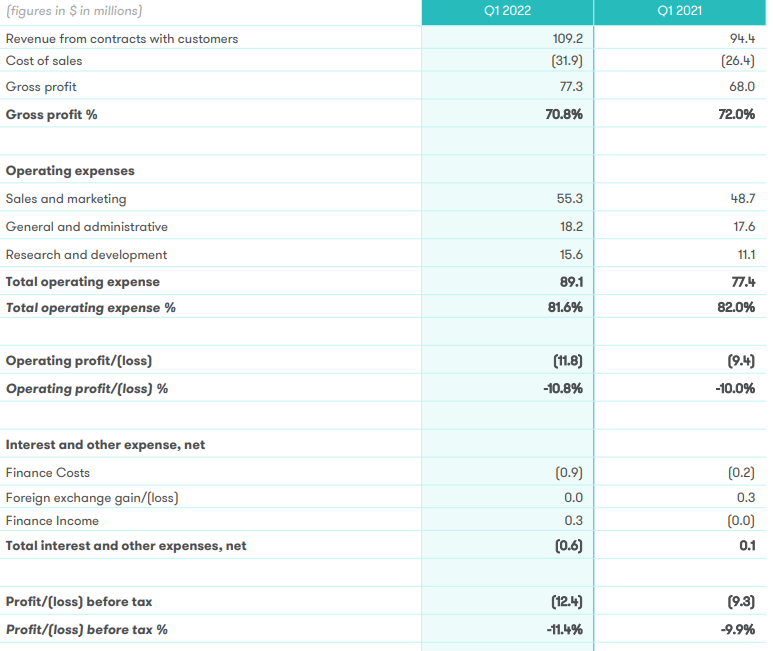

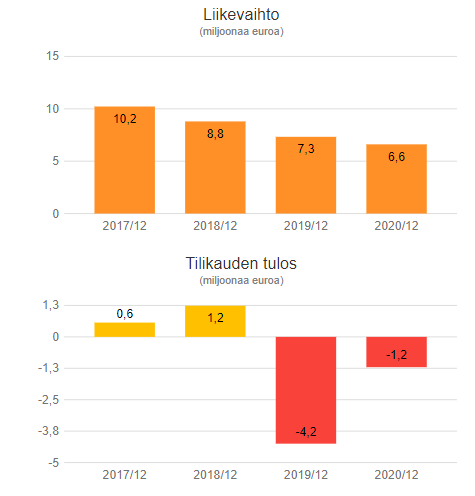

Figures, source Yahoo Finance. Got it into a neat concise format there. More detailed info from the annual report:

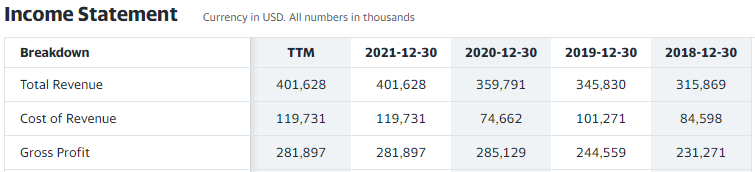

So, in terms of profitability, losses are being made, but development costs and acquisitions partly distort the figures. The gross margin for a SaaS service is naturally at a good level. Scalability will at some point bring positives to the bottom line as well.

2021 Annual Report

Sources monitored, e.g.

The number of searches is quite staggering ![]()

![]()

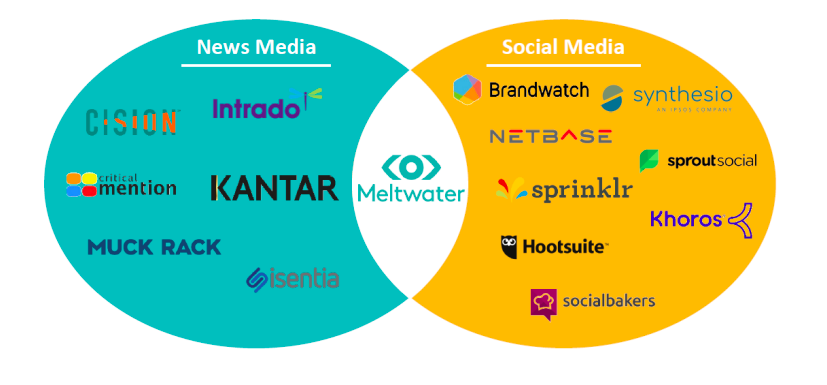

Inorganic growth sought through acquisitions, integrated into service offerings

Expansion via Acquisition and Integration

Meltwater has a proven track record of integrating technology and functionality from newly acquired companies into our flagship media intelligence product, having done this with Sysomos, Infomart, Encore Alert and many more acquisitions over the years.After the acquisitions of Linkfluence, Klear, Owler and DeepReason.ai in 2021, Meltwater’s product offering now spans far beyond the use cases we have primarily served, and through deeper integration, will give our customers a wider lens and more detailed insights to help them inform and execute on their strategies

CEO in Nordnet’s interview 08/2021

Media monitoring in general covers collecting information from various sources, screening and summarizing material for the end-user for different purposes. Typically, its use supports management decisions, monitors the effectiveness of marketing and advertising, gathers leads for sales, or provides summarized industry monitoring information to company employees.

In my previous work life, Meltwater was a newer player in Finland, and material was collected by scraping various online sources. There was a significant amount of “junk,” which in many cases made the service of poor quality. For other users, the amount of extra clutter was more limited, and the service mostly worked well. Correspondingly, the price level was more affordable than domestic competitors.

Among competitors, Esmerk was then clearly the most comprehensive and functional service, especially in domestic industry monitoring. The service was produced by summarizing articles, and through that, users gained significant added value in the form of a better and more tailored service.

M-Brain Oy acquired Esmerk from Sanoma Oyj and still operates in the market today. M-Brain Insight is a subsidiary and apparently produces more tailored Business Intelligence services.

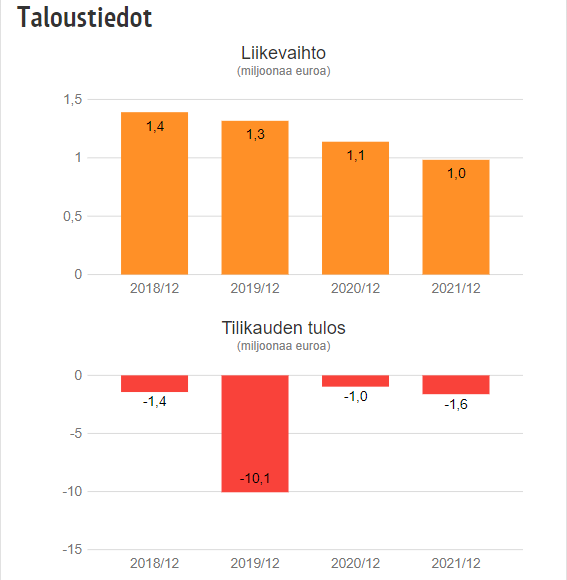

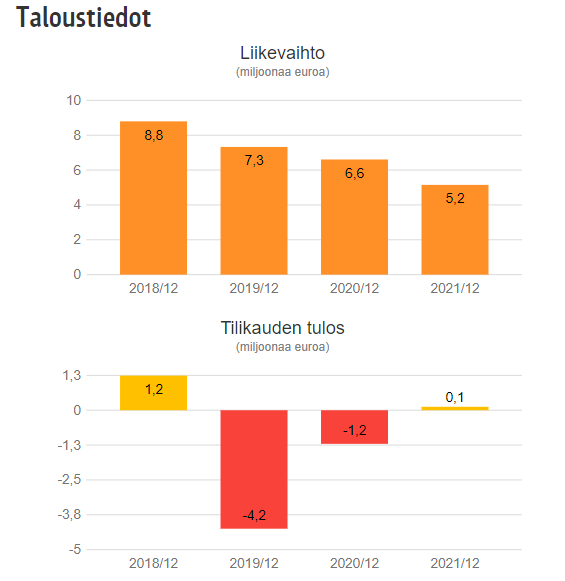

M-Brain has been a company long awaited to be listed on the domestic stock exchange. However, profitability should be improved before listing – or rather, capital should be obtained specifically to finance growth and pay off potential debts.

M-Brain Oy

M-Brain Insight Oy

So, the industry is not necessarily a goldmine, even if the services are functional. However, news and various monitoring services are available in abundance. A good service can still be truly valuable in the right use when the essential can be filtered for the end-user to utilize.

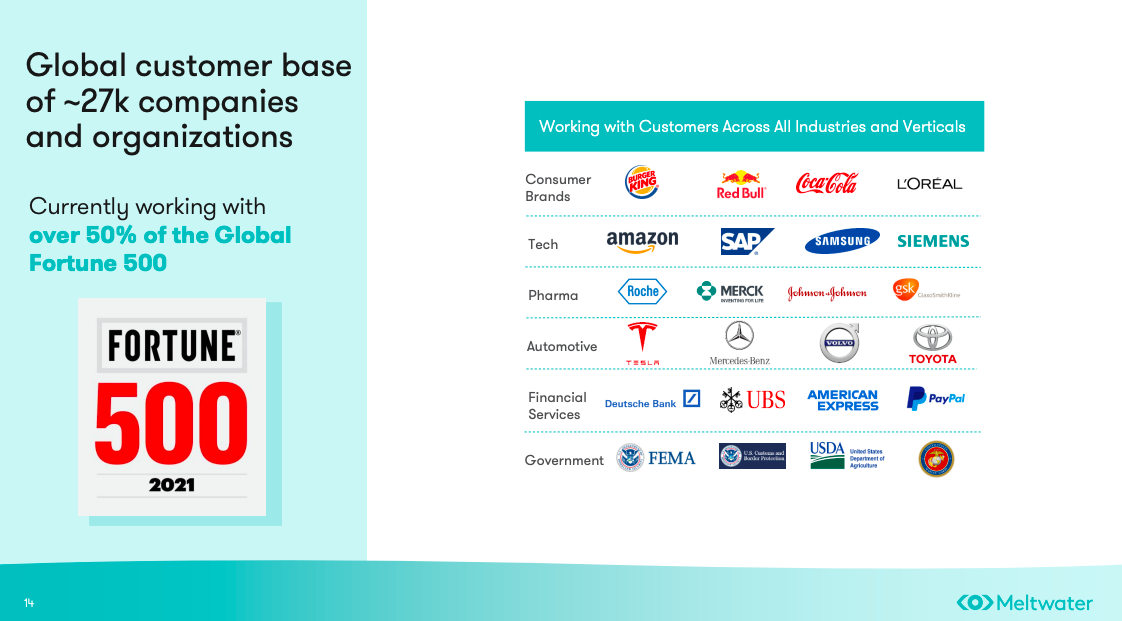

Currently, the level of services is likely very different, and Meltwater has, for example, acquired an AI services company through an acquisition. Analytics and data screening have advanced tremendously in the last few years, so the situation is likely very different now. Meltwater, at least, is growing globally, while M-Brain’s revenue has decreased year after year.

@Timo_Huhtamaki commendably supplemented the thread’s opening in the 4th message ![]()