There was some discussion about Protector Forsikring in the L&T thread after it flagged exceeding a 5% ownership threshold, so I decided to take the initiative and see if there’s any interest in the company here.

As a brief introduction to the company: I work in the industry as an insurance broker and came across the company by chance in 2015. I noticed its strong growth, high ROE, and low valuation (P/E 8). Later that year, the company entered its fourth market by coming to Finland, which further improved visibility into its operations. The company has also been by far the biggest success in my investment history, as in the spring of 2020, I shifted 70% of my portfolio into it when the share price (bottoming at 20 NOK) reflected refinancing fears due to a decline in securities (solvency weakened momentarily).

Business in brief:

A Norwegian insurance company.

Sells non-life insurance to businesses (i.e., no life or pension insurance).

Operates in all Nordic countries except Iceland, as well as in the UK. Operations have also begun in France, with the first quotes issued for the insurance period starting January 1, 2025.

Distribution channel is insurance brokers; no in-house sales staff.

The company is the cornerstone of my portfolio and my largest holding for the following reasons:

Due to my work, I have a good view of the Nordic insurance market. For example, every autumn I receive preliminary information from almost all domestic insurance companies regarding the market situation and premium increases for the following calendar year.

The company is a defensive growth company (CAGR approx. 21% between 2014–2023) with a low valuation and high ROE.

Growth is 100% organic and (very) profitable.

The company is very transparently and disciplinedly managed, starting from client selection.

A holistic approach to efficient capital allocation:

Insurance markets – is profitable growth available?

Investment markets – are there attractive special situations available?

Dividends and buybacks are only considered after the above.

Consequently, the company is not a “dividend play” in the traditional sense and may refrain from paying dividends even if the result is at a record high.

Dividends are typically paid quarterly based on the capital position. In the spring, after the financial statements, about 40–50% of the year’s dividend is paid.

Although the insurance industry is not completely immune to market risks, it is mostly well-protected, and so-called self-correcting mechanisms are built-in.

For example, in 2022 and 2023, high inflation was successfully passed into prices upfront by all market players without issues, because this is an industry that operates heavily on mathematics where the laws of profitability are the same for everyone.

On the other hand, market growth largely follows GDP + inflation, so a decline in both will eventually be reflected in the market. Factors like climate change, rising healthcare costs, and changes in the automotive market (EVs) bring slight additional pressure for faster premium growth.

Falling interest rates also harm the insurance market in two ways: capital seeks more risk coverage (competition intensifies), and investment returns decrease. Protector’s large equity weight (15–20%) somewhat counters the decline in investment returns.

The company’s quality improves year by year due to growth in premium income, which reduces earnings volatility. Growth also increases the possibility of lowering reinsurance levels, which has been significantly loss-making for the company. This supports net premium income growth (gross income minus reinsurance premiums) and, in my view, also profitability (expense ratio increases).

The company takes bold views on investments, enabling a higher ROE than its competitors. A high ROE also enables growth, as premium income and balance sheet growth go hand in hand (carrying risk requires capital).

Competitors mainly invest in low-risk bonds, resulting in lower investment returns than Protector. On the other hand, this allows their solvency capital relative to premium income to be small (the riskier the securities you invest in, the more capital you need).

In my view, the company would achieve better returns in equities by simply investing in indices.

Negatives of the company:

Due to the company’s small size (Gross Written Premium 11.3 billion NOK) and the lack of consumer insurance, large claims (suurvahingot) fluctuate profitability much more than for peers (e.g., Gjensidige, Tryg, If).

This also offers buying opportunities when large claims are elevated relative to averages.

The company sells insurance through brokers, meaning there is no direct customer relationship, so customer “loyalty” to the insurance company is virtually zero. Additionally, customers who do not use a broker remain out of reach.

To counter this, the company invests in good broker relationships (based on my experience, significantly more than its Finnish peers).

On the other hand, brokers provide protection from competitors, as at least in Finland, insurance salespeople cannot approach customers who have a valid broker mandate.

Protector has had high customer retention of approx. 88% over the last three years.

The company’s main competitive advantage is higher efficiency/lower prices than competitors (lower operating expenses), which competitors will eventually catch up to. It is already visible that growth in the Nordics (approx. 50% of premium income) by winning market share is no longer as easy.

Software and the automation level of claims services play a major role in efficiency. In my view, Protector’s advantage is its small databases and fresh software compared to competitors. Other insurance companies have the burden of history, which is why employees have to use multiple programs that don’t communicate with each other. For example, at Pohjola, a DOS-based claims system was still in use in the 2010s (I have personal experience with this).

The small size of local organizations also brings efficiency compared to large competitors.

I believe the tendering process is more efficient than competitors’. The company has a three-stage bidding process, where a large portion of received RFPs are rejected in the first stage. Insurance is only quoted to customers where there is a good chance of winning (high hit rate). They also rely on their own strengths in the insurance types offered.

An exceptionally large part of the company’s result comes from investment income, which causes significant volatility in earnings. Since 2020, investment returns have accounted for about 50% of the result (investment result + underwriting result).

This also creates good buying opportunities, as the “train” (a.k.a. the insurance business) moves steadily toward the northeast.

As the company grows, the prerequisites for relative growth also decrease. On the other hand, through larger scale, even lower operating expense ratios (expenses excluding claims costs) are achieved.

Valuation and Outlook

Based on analyst forecasts, the company’s 2024 P/E is approx. 12.2 (price 226.50 NOK), which I consider low for a Nordic non-life insurance company. 2025 forward P/E is 11.6. Personally, I consider P/E 15 a neutral level for the company.

For example, Gjensidige and Tryg have a P/E of approx. 20, but they are higher quality in terms of earnings stability, although their growth follows market growth.

In my opinion, Protector will (never) deserve similar valuation levels due to higher earnings volatility (high share of investment income and lack of consumer insurance).

2024/Q2 P/B = 4, which is at the same level as its Norwegian competitor Gjensidige, but clearly higher than, for example, Sampo (2.6). Compared to the average ROE of 40% between 2020–2023, the valuation is cheap, but it is expected that investment returns will not continue as strong and ROE will decline. Of course, 2024 and 2025 returns will still be relatively high due to the interest rate market.All in all, I have been increasing my position at the current levels of approx. 220 NOK, as the large claims in Q2 and the temporary weakness in the investment market have put the market in a selling mood. At the same time, however, I am keeping an eye on the weakening of the fixed income market, which will affect investment returns. On the other hand, the current weakness of the Nordic equity markets acts as a counterweight, which could compensate for the decline in fixed income yields if it recovers.

Disclaimer: While this is not investment advice, I highly recommend looking into the company.

PS. I’ve had quite a bit of wine by now, so I will share tables on the company’s development and information on its recent history (especially the weak 2018 and 2019) later.

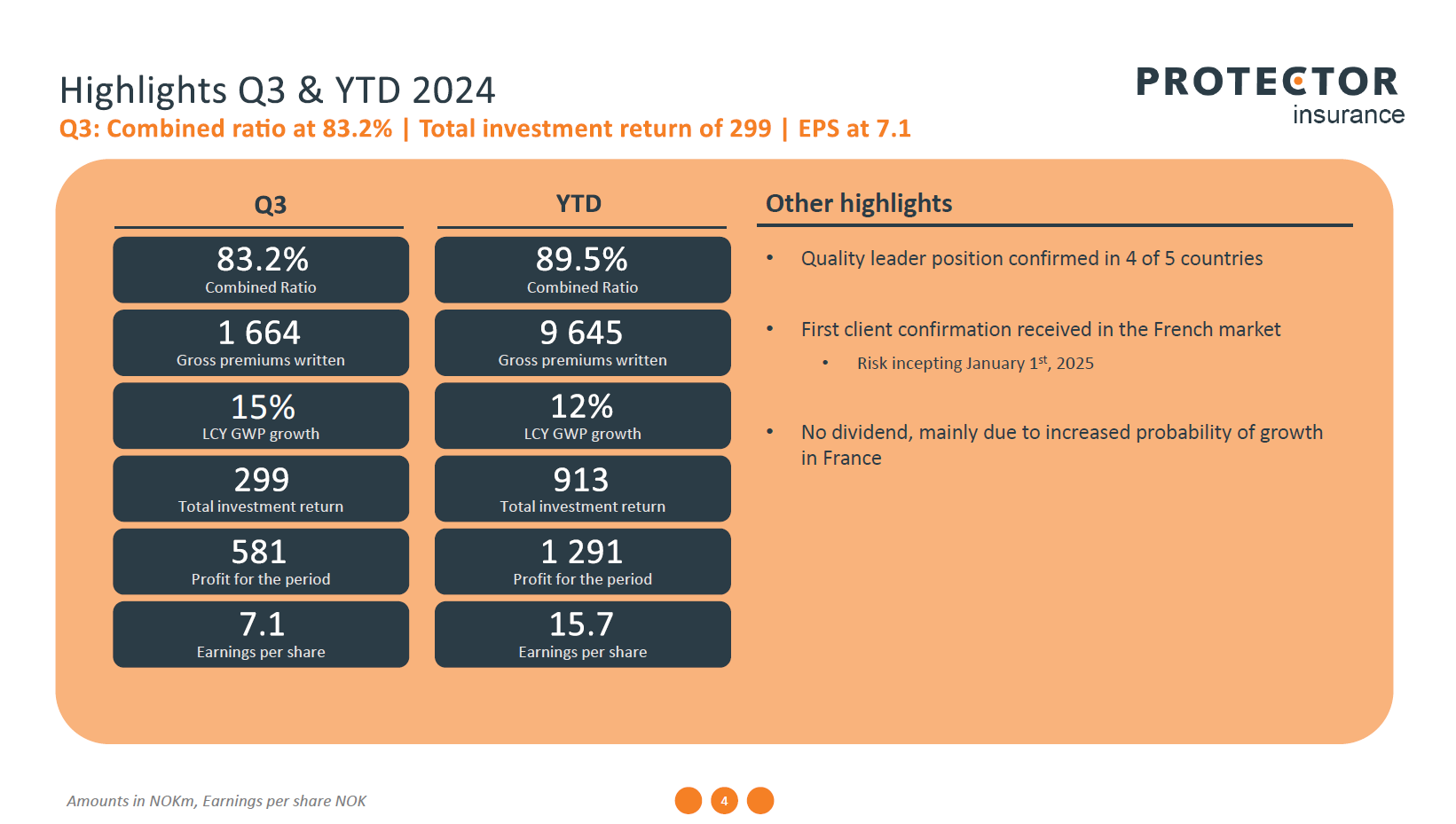

Protector’s Q3 numbers came out yesterday evening. The train just keeps on chugging along:

Growth of 15% in local currencies.

Combined ratio of only 83.2%

First customer secured in France and no quarterly dividend will be paid, as they are preparing for growth in France.

Solvency capital rose to 194% relative to the minimum requirement.

A year ago, results were weighed down by Storm Hans in Norway. If nothing similar happens this year, the early winter remains mild (vehicle damages decrease), and investment returns pick up slightly, then we are looking at an EPS in the range of 22-24 NOK for the full year (Q1-Q3 2024: 15.7 NOK).

Perhaps the clearest downside in the report for me was the 5% growth in the UK, which was affected by the loss of one major customer. Of course, YTD growth there is still 14%, so no need to panic, even though the CEO already warned last year that the rocket-like growth in the UK wouldn’t be repeated every year.

Preliminary information on 2024 insurance premiums and 1.1.2025 growth.

*GROSS WRITTEN PREMIUM (GWP) FULL YEAR (FY) & QUARTER FOUR (Q4) 2024 * FY 2024 GWP came in at MNOK 12,333, up 18% (15% in local currencies (LCY)) relative to 2023.

In Q4 2024 GWP amounted to MNOK 2,688, up 30% (27% in LCY) relative to Q4 2023.

*UK makes up 82% of total growth in GWP this quarter. *

*GWP INCEPTING JANUARY 1ST 2025 * January 1st, 2025, GWP growth was 19% in LCY relative to 2024. The growth is driven by a high renewal rate and our entrance to the French market. The new sale in France accounted for 8%-points (MEUR 25) of the total company growth.

So:

Q4/2024 growth 27% and full year 2024 15% compared to the previous year

1.1.2025 concluded insurance contracts show 19% growth compared to the previous year, of which the new French market accounts for 8%-points.

Insurance premiums recorded in France on 1.1.2025 are thus 25 MEUR, which is the same amount as Protector’s total in Finland during 2023. Operations in Finland started in 2015, and in France, offering only began in H2/2024.

One can only marvel at such strong growth. One must hope that pricing in France has not been too aggressive. The UK was the previous new market where pricing went perfectly.

It would be nice to hear others’ views on the company and/or the earnings report, so feel free to analyze

My own takeaways from the earnings report:

Underwriting result vs. year ago +40% in Q4 and +30% in FY 24.

I had somewhat anticipated the weak investment result in Q4 (-96mNOK vs. 860mNOK Q4/23), but the weakness in bond yields was a surprise. However, Tryg also seemed to have a disappointment in that area, which is not surprising given the slight upward pressure on interest rates at the end of the year.

The total investment return of 4.9% in FY 24 is, however, very good for an insurance company, and a 5.2% yield on bonds going into the current year means manna for 2025 investment returns.

Denmark still seems to be a headache in terms of profitability. Efforts to get it in order have been ongoing for almost 7 years. An indication that it’s not easy in all markets.

Renewal rate 99% including an estimated 9% (my own estimate) premium increases, meaning customer retention is at an excellent level.

Indeed, to my surprise, a dividend of 4kr, which on the other hand is understandable when looking at the solvency ratios. Typically, they have also distributed quarterly dividends, but their fate will likely depend on growth in France and potential special situations in the capital markets.

With the 2024 results, the current valuation is, in my opinion, at an acceptable level, but when calculating a simplified 2025 result based on basic performance, it can be stated that the valuation is cheap:

Premium income growth +20% => premium income ~14.800mNOK FY 2025

Combined ratio 88% => underwriting result ~1.800mNOK

AUM 22.000mNOK, of which bonds ~18.500mNOK and equities ~3.500mNOK

From bonds, interest income alone 5.2% => 960mNOK and from equities 10% => 350mNOK, total 1.300mNOK

Other expenses and insurance finance expenses total -500mNOK

Taxes -600mNOK

Net result 2.000mNOK vs. 1.539mNOK FY 2024, i.e., EPS approx. 24.3NOK (30% growth)

Calculated with that, forward P/E 13.50. The underwriting result has been quite stable in recent years, so I don’t expect major surprises in that area, but investments can fluctuate in one direction or another. However, if one believes that interest rates will fall, in addition to interest income, there will be returns from appreciation.

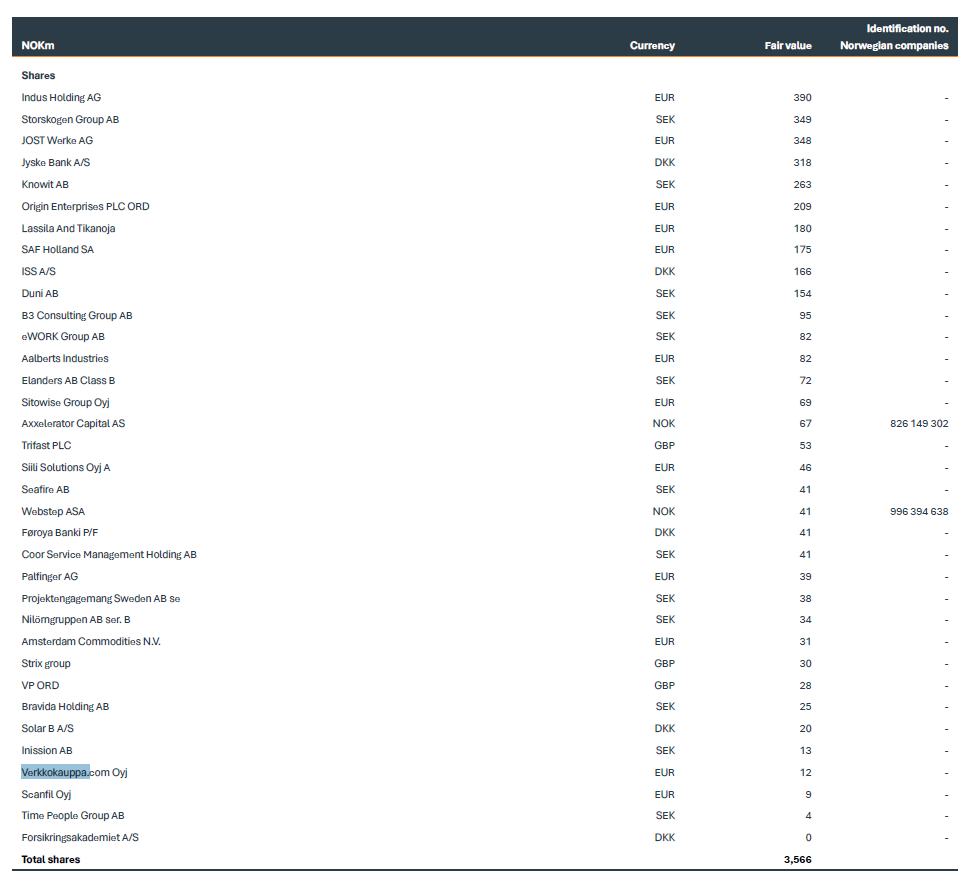

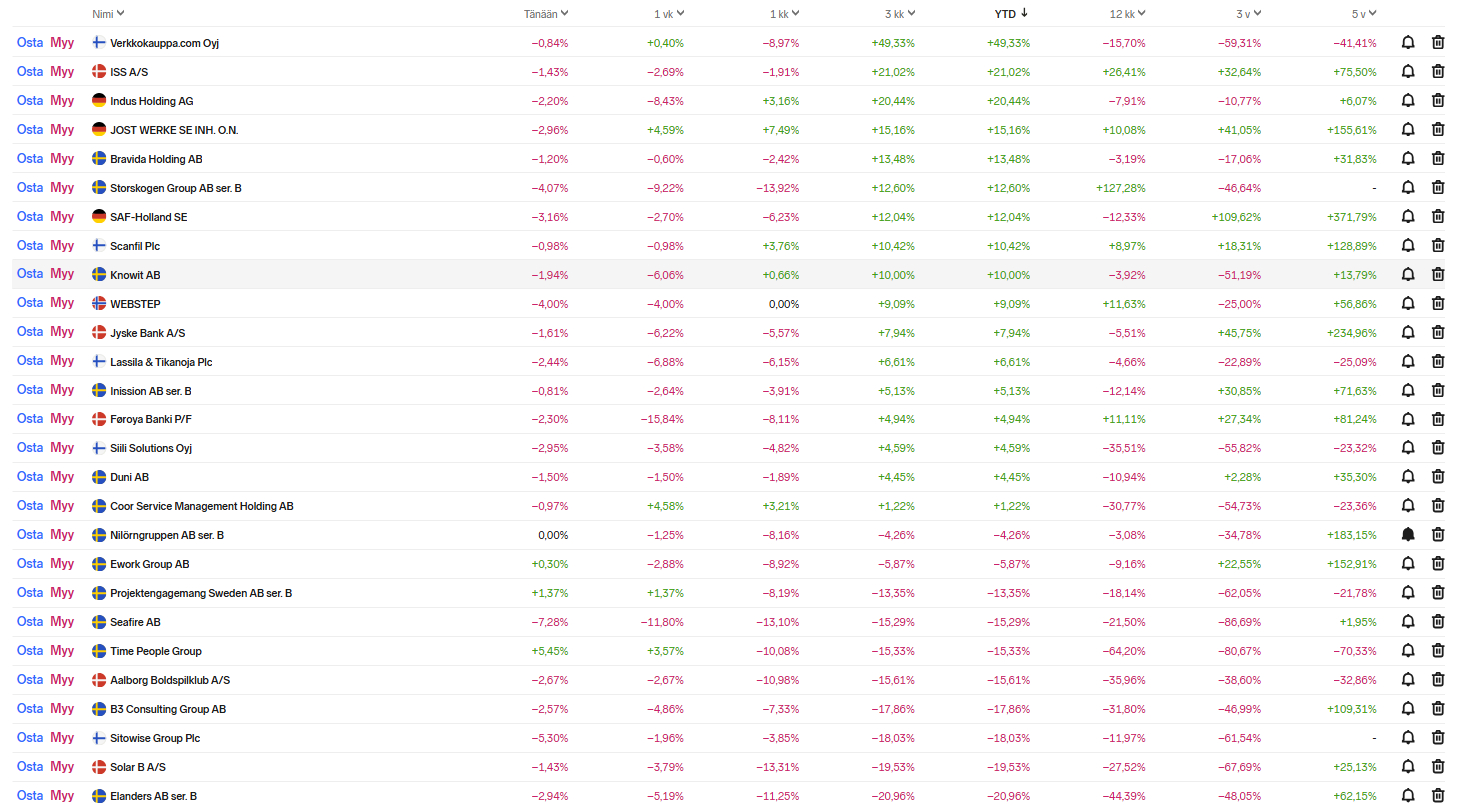

Below is a picture from Protector’s 2024 annual report, showing stock holdings in order of size as of 31.12.2024. That list becomes outdated quite quickly, but is quite useful for Q1-Q2. When compared to the 2023 annual report list, only one third of the 31.12.2023 holdings remain.

I added the stocks found on Nordnet to the watchlist. The largest holdings have performed quite impressively YTD, meaning the Q1 investment result should be very strong, also considering bond yields.

Danish Tryg reported strong figures today. Particularly, the Q1 combined ratio (CR) for corporate insurance was 79.3% vs. 82.7% a year ago. Investment income was also stronger vs. a year ago, but Tryg’s investment portfolio is hardly comparable with Protector’s, as they have reduced risk and shifted weight to fixed-income securities and especially short-term Scandinavian fixed-income securities.

Protector takes more risk, e.g., with high yield fixed-income securities and stocks. I believe they have also capitalized on the recent volatility in the fixed-income market. This was the case at least during the COVID spring of 2020.

In a couple of weeks, Protector’s earnings report will be available.

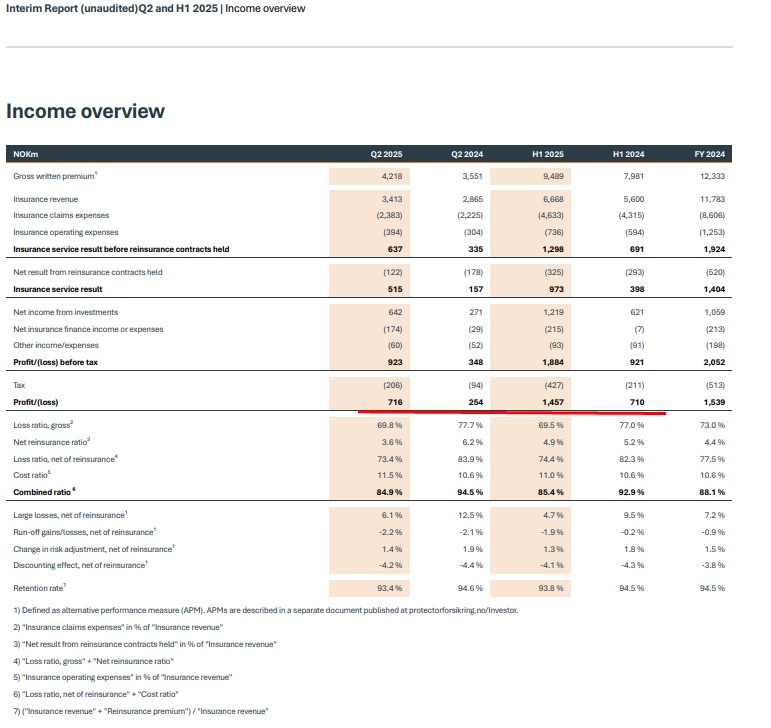

And there came the Q1 earnings report, and the progress looks great. For the quarter, earnings per share were 9.00 NOK and dividends 3.00 NOK per share. Things are going well, and apparently nothing significantly negative occurred during the quarter. In Q4, CR was 84.2%, now 85.9%. In Q1 2024, CR was 91.2%. The retention rate was 94.2%, which has remained at the same level as a year ago.

A very good result. CR surprised me, although the impact of a low-snow and warm winter should have been recognized. Major claims were also low, which helped with the CR surprise despite the cost burden from starting operations in France. The Danish occupational accident insurance portfolio was sold off, which immediately helped the Danish figures and resulted in an 8 percentage point improvement in CR there.

Stocks performed well and contributed slightly over a third of the net profit after taxes (gross 323 mNOK / 8% return). It must be remembered that stocks are unlikely to yield significant returns for the rest of the year (my own assumption is 10% for the full year). AUM grew by 13% from the 31.12.2024 situation, which is absolutely tremendous growth.

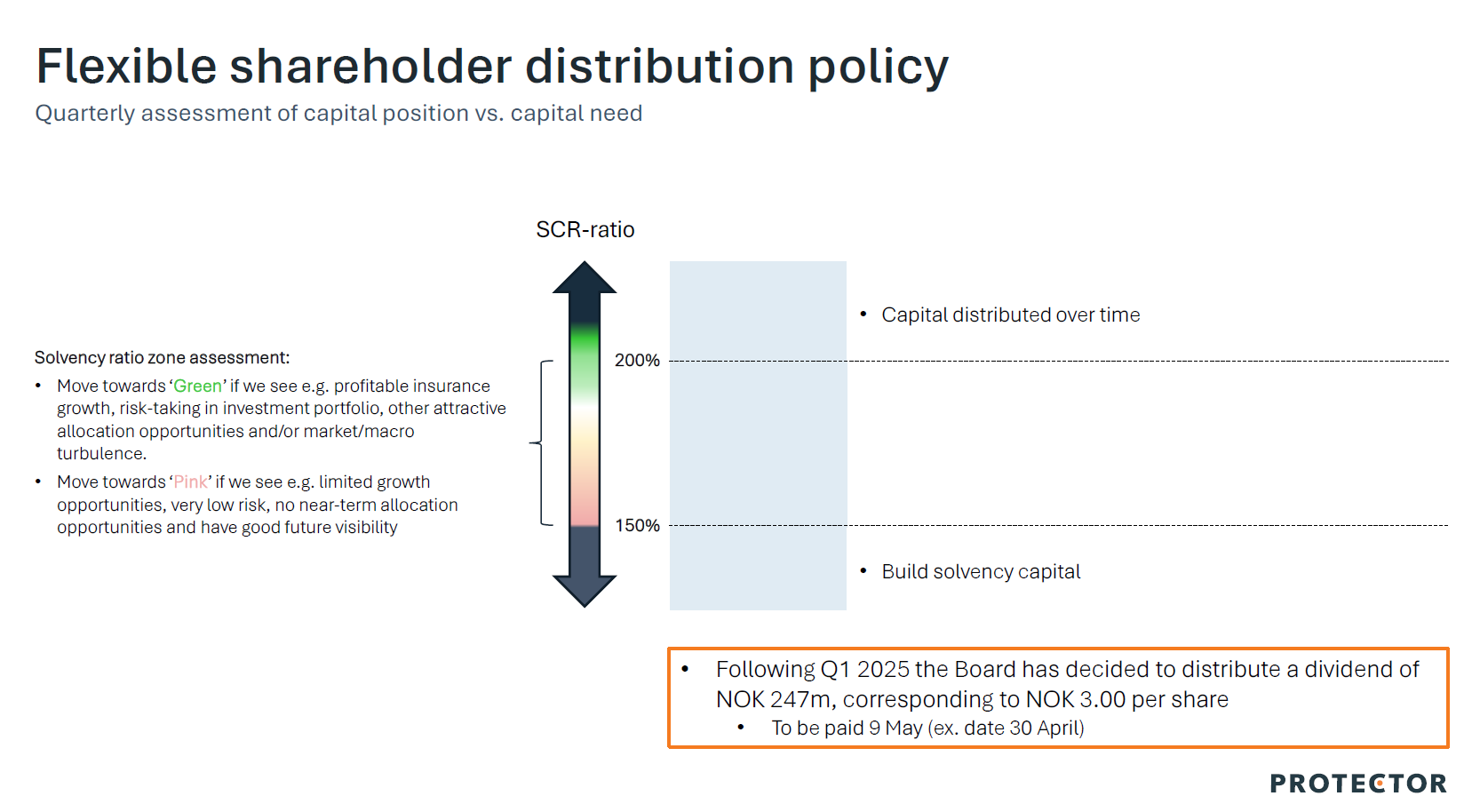

Quarterly dividend will be 3 NOK per share and solvency 222% relative to the required solvency capital. Below is a reminder of the distribution of funds.

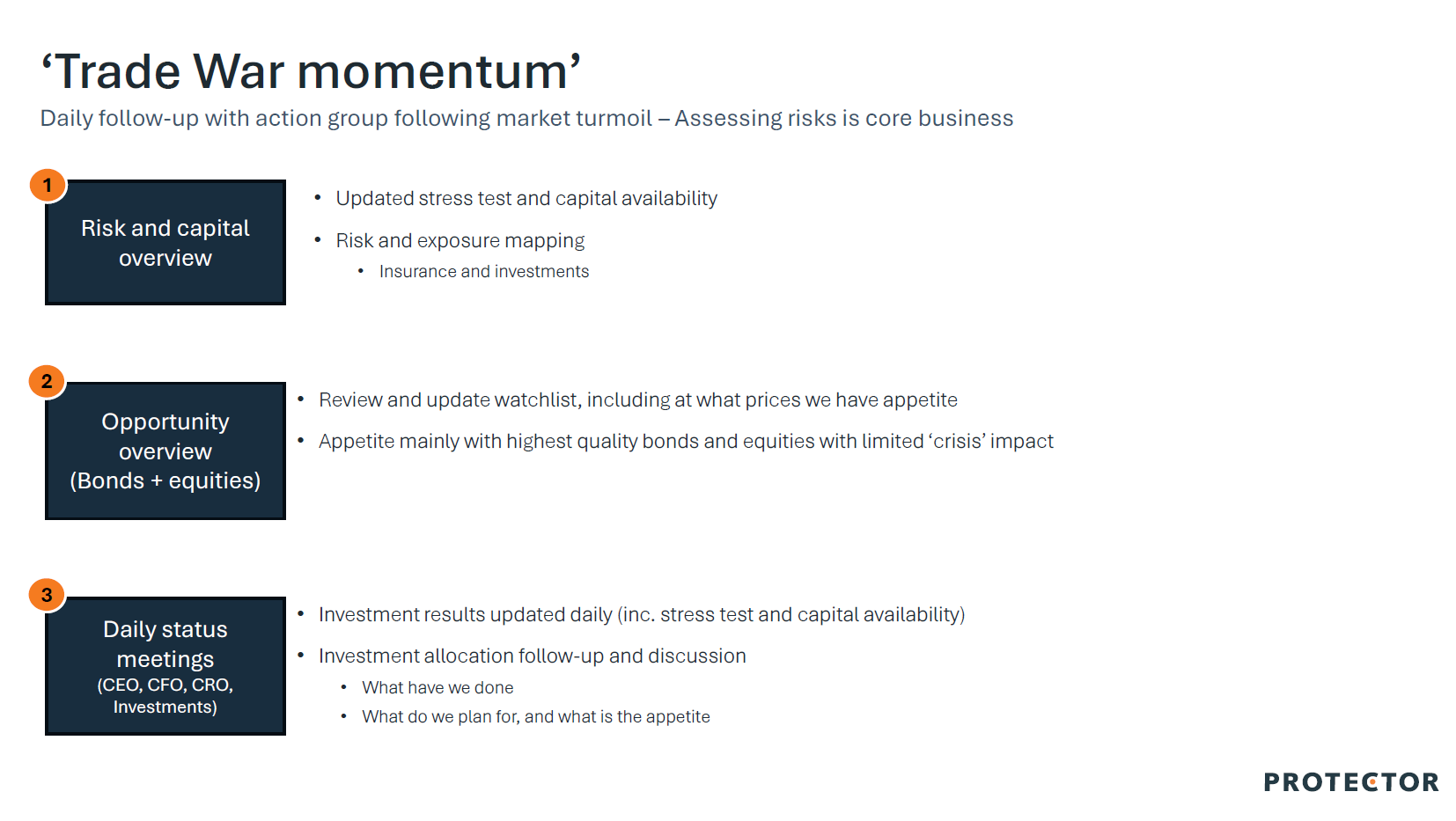

And as I suspected, the opportunities brought by the customs confusion are under close scrutiny:

I’m updating my simple forecast below. Growth needs to be slowed down a bit and profitability increased. Also, investment returns slightly up. In the previous one, I incorrectly used GWP instead of insurance revenue, which in Proten’s case is slightly behind GWP and 5-7% smaller than GWP.

Sverre doesn’t mince words much and already promised a bit before his departure in spring 2021 that the share price would rise above 100NOK within a year But so far, his views on the company and the share’s development have been very accurate, which is no wonder, as he knows the company and its DNA inside out.

It certainly seems like I’ll have to put my hand in my pocket and buy more if the market gives an opportunity and the price drops to around 300-320 NOK. The market, with Trump’s whims, might still give a good opportunity for that

From Protector’s former CEO (Hvaler Invest), a target price update (480) and a good summary of the investment case. To my taste, the investment return assumptions are perhaps a bit on the high side for the current year and going forward (e.g., stocks 13.4% / 2025 and thereafter an average of 10% / year). In the same breath, it must be noted again that he has been astonishingly accurate about the business development, and the share price has always caught up with the target price. However, even he cannot predict investment returns on the stock side. In fixed-income securities, it is naturally easier to predict.

The comments that stood out were that Protector’s market share in the public sector in the UK would already be approx. 25%, but it is more difficult on the corporate side. The information that caused a satisfied chuckle was that Protector also explored expansion into Canada, Spain, and the Netherlands, but they proved to be poor markets. Perhaps it was learned from the expansion into Finland and Denmark that cost leadership does not guarantee success everywhere. I cannot comment on the sources for the aforementioned information. It is possible that these came up in some earnings release or general meeting (if only I had the energy to listen to them).

The UK continues strong profitable growth in Q2 (17% LCY) in the so-called big quarter (April 1st is the general start date for the insurance period in the UK).

Equity returns of 13.7% in H1 and accounted for approx. 30% of pre-tax profit. H2 is unlikely to see equally strong returns.

Break-even in France already in the second quarter. It happened to be a low-claims quarter. There will certainly still be loss-making quarters, but not a bad performance.

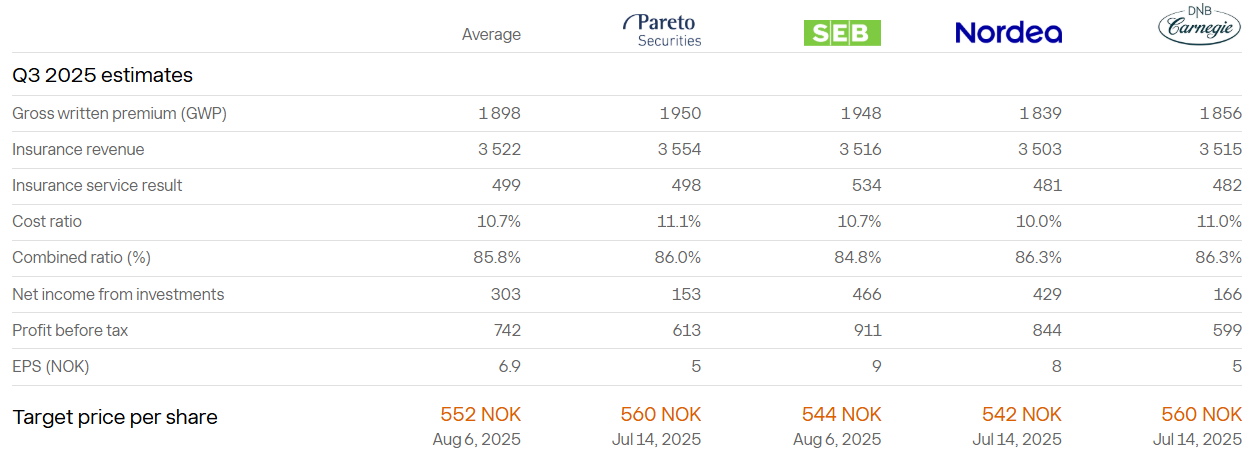

Protector’s former analyst Sverre adjusted his own target price upwards to 617kr. Below are the justifications – take them with a grain of salt.

better-than-expected Q2 results and slightly improved short-term outlook

increased expectations for growth in France

Increased P/E ratio from 17x to 20x. If you want to argue this point, please read the relevant section from our previous comment here first – Hint: How do you value a growth engine with 20%++ ROE…?)

a gradual increase in combined ratio from 2025 (85%) to 2027 (87%)

To my taste, despite the growth and ROE, the earnings are not of such quality that they would deserve a P/E ratio of 20, which is, of course, at the peer level. This is due to the fact that half of the earnings come from investment income, which fluctuates more significantly. In other words, if that valuation level is reached with a record-high CR and above-average % investment income, then I will certainly reduce my position significantly.

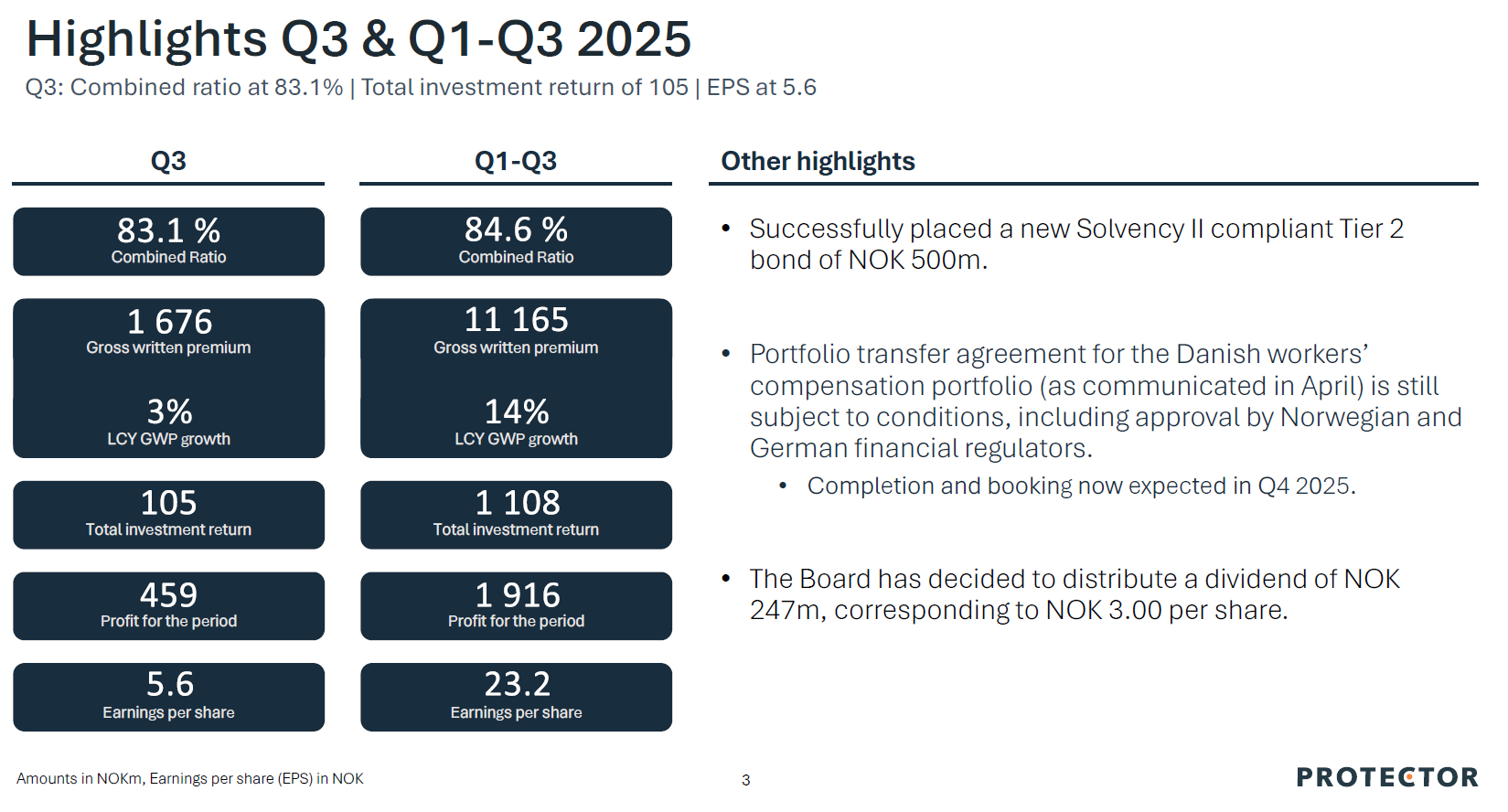

The quarterly report will be available for viewing tomorrow or tonight after the market closes.

Earnings report is out. In summary, the underwriting result exceeded expectations, but investment income disappointed, especially due to negative equity investment returns. EPS fell short of expectations, but I still believe it will lean slightly positive, as quarterly equity returns are unlikely to be given such high weight.

France’s 1.1.2026 tender pipeline looks promising: 460mEUR worth of requests for proposals, of which Prote is bidding on 70-75%. Quite a high percentage, as they are much more selective in other markets, but they are apparently getting a feel for the market, which is perfectly fine. In the UK, the first real estate client was won - let’s hope this provides a new growth opportunity Denmark, which had been problematic for a long time, was the star performer this quarter with a remarkable CR of 71.9%. This can be attributed to the sale of the workers’ compensation insurance portfolio earlier in the year.

It was also noted that Prote’s investor pages have been revamped, and a quick scroll gives, in my opinion, the most essential information about the company.

I am updating my simple forecast below. Growth needs to be slowed down a bit and profitability increased. Also, investment returns slightly up. In the previous one, I incorrectly used GWP (Gross Written Premium) instead of insurance revenue, which in Proten’s case is 5-7% lower than GWP and comes slightly after GWP.

Combined ratio 85% => underwriting result ~2,100mNOK

AUM avg. 25,000mNOK, of which bonds ~21,000mNOK and equities ~4,000mNOK

From bonds, interest income only 5.2% => 1,090mNOK and from equities 10% => 400mNOK, total 1,490mNOK

Other expenses and insurance finance expenses total -500mNOK

Taxes 25% / -770mNOK

Net result 2,320mNOK vs. 1,539mNOK FY 2024, i.e., EPS approx. 28 NOK (50% growth)

Largely, we are proceeding at the pace of my previous forecast. Q4 CR (Combined Ratio) is expected to rise slightly as winter weather increases vehicle claims. If equity returns turn profitable, investment income could be well over 300mNOK in Q4, bringing us close to 28NOK.