Is there really not a single thread about foreign companies…?

The portfolio has performed brilliantly in recent years, largely thanks to domestic microcaps, but the diversification benefit to be gained should not be forgotten. Domestically, there are still too many engineering workshops and other cyclical companies.

One of my favorites, Bufab, published its results today. Reliable development in a challenging market, grabbing market shares. Well, market sentiment isn’t the best possible, but it’s an excellent example of a relatively stable and capital-light company.

Earnings season is also about to begin. “Misses on revenue” seems to be the prevailing sentiment of the day, but the situation doesn’t seem entirely catastrophic.

I looked into this about two years ago, but wasn’t too enthusiastic about it due to the challenging price tag. Short sellers also found the stock, which has kept the price in check over the past year.

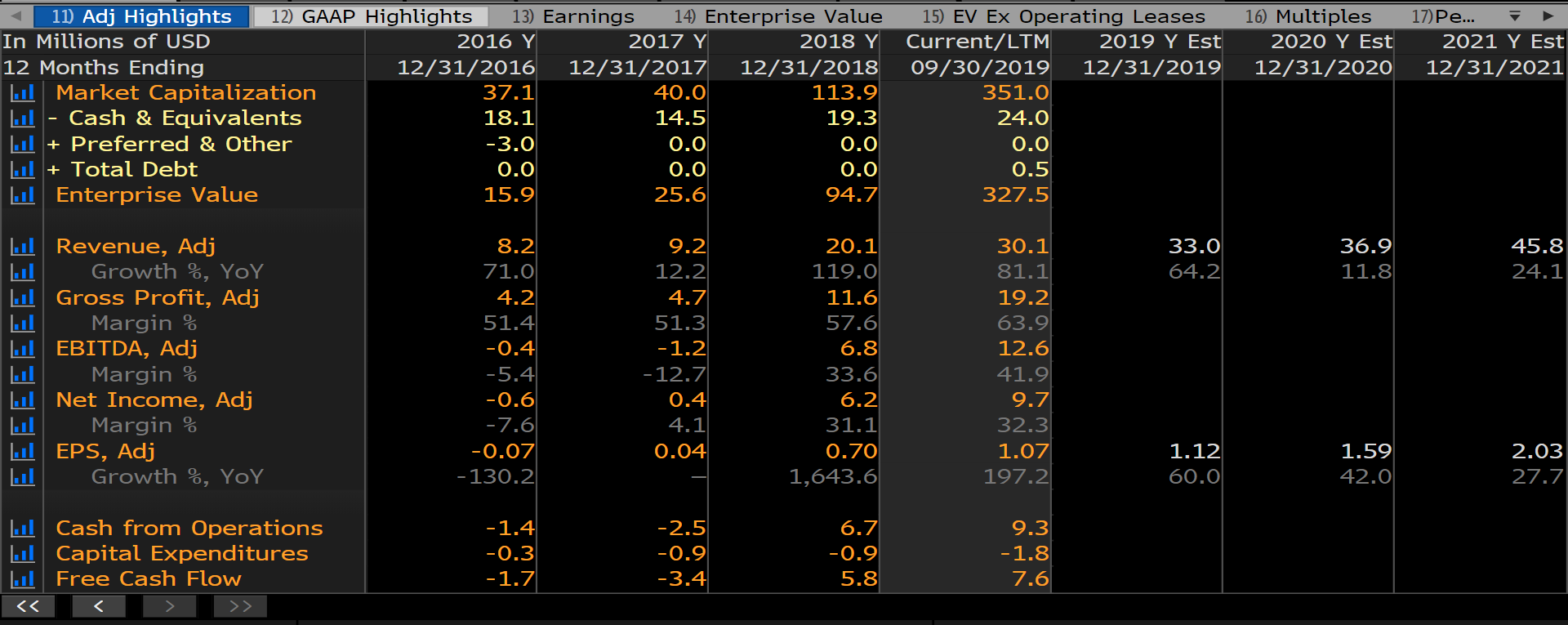

The main point is that the company provides backend systems for Goldman Sachs for the Apple Card, although this hasn’t been officially admitted. With sales currently around nine million on a quarterly basis, there is huge potential from just one client.

I still need to examine it more closely, but it initially seems appealing.

Go read it there. It pretty much follows the same pattern as in numerous other cases. Some individual files taken out of context, pictures of offices, assumptions about business weakness, etc. I think it’s the same party that predicted BofI (now Axos Bank) would go bust some years ago.

Sometimes I follow these short-seller targets with keen interest. Wirecard is currently hooked with a quite reasonable stake.

“Relentless hype on social media has propelled shares to all-time highs and a monster valuation of roughly 15x trailing sales and 40x trailing EBITDA”

That’s less than Admicom Currently, EV/EBITDA is probably around 26 after recent earnings growth.

Yeah, familiar name, I was on board with BOFI for a while later when the stock was driven so cheap. Interesting bank, but it’s been in a slump for years now? It’s really hard to see inside banks; only crises reveal the truth…

Haha, and Admicom’s multiples just keep getting better (worse) day by day. That INS is interesting, I’ll have to dig into it a bit.

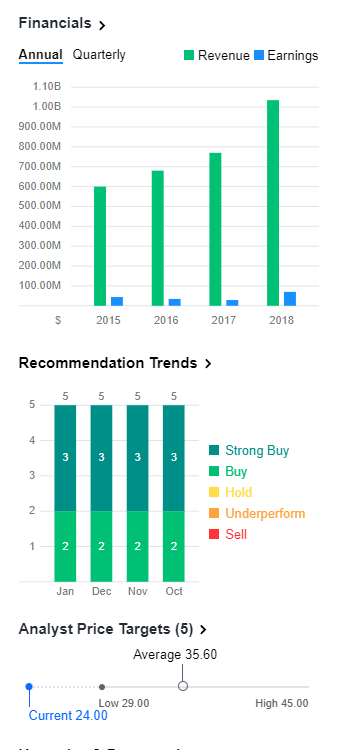

Axos’s story in recent years has been purely about preparing for the $10 billion asset threshold under the Dodd-Frank Act. The company first had to slow down and then use some clever maneuvering to halt growth, so that this limit wouldn’t be exceeded prematurely. This, of course, increased costs upfront, slowed growth, and weakened the cost ratio. The good news is that this is now behind them, and growth has returned to “normal” lately. The next significant asset threshold seems to be $50 billion, which is still a good way off.

The company is showing fairly consistent growth, so I haven’t done anything with the position. I think I sold a tiny bit over a year ago somewhere around the $35 mark, but otherwise, there are no plans to divest. I believe a well-managed bank operating online will maintain a cost advantage and agility far into the future compared to the masses of traditional banks. It’s difficult to develop anything on top of legacy systems when you have to hire developers out of retirement

How do you see INS’s competitive advantages? Stripe and other giant challengers are lurking on the same lot? In terms of numbers, it’s an attractive company, but forecasting revenue growth is probably quite difficult. If a big client comes, BOOM, and if not, then no… no.

“For 2020, we see continued growth but not at the pace we had for the full year 2019 over 2018. But we do expect to grow and see the 2020 year as the one to catch our breath, while hardening our infrastructure to line up for higher growth in the future years. So that pretty well sums up both the third quarter and how we see the future. I think I will spend most the rest of our time talking about questions.”

The P/S has come down nicely. At the same time, the cash balance is starting to swell quite quickly as cash flow begins to pick up.

Hey, I don’t have any particular insight/expertise into which company would be better and where. Fiserv is the number one player there, and they even merged with First Data, so the company size is probably hundreds of times larger and resources are accordingly. There could be more competitors, but apparently software isn’t developed just by snapping your fingers, so there’s already a competitive advantage through this.

The company at least markets itself as providing the service more affordably, being able to tailor services more agilely, and offering software licensing, among other things. I guess that brings some advantage if it has managed to compete with industry giants.

Growth is not reflected in the key figures:

Trailing P/E: 8.69

Forward P/E: 5.42

With the average ROE over the past four-plus years, the latest reported equity, and a 10% required rate of return, the share price is very much in line with EPV (Economic Value Added). Of course, the company has recently made better returns on equity, so the EPV metric might even be underestimated if the company’s return on equity stabilizes above 20% in the future. In addition, the company’s equity has swelled at a commendable rate of 29.5% per year for the last 4 years. If I have read Jarkko Ahola’s long writings carefully enough, he might say that an investor in this company at this price does not pay anything for potential growth.

Analyst consensus forecasts for next year from Yahoo:

EPS growth: 13%

Revenue growth: 10.3%

This is despite the fact that the company is apparently winding down its operations in Brexitland. If someone has studied and understands the business model of this particular company, it would be quite interesting to know. It didn’t quite open up with a quick review.

At first glance, it looks like a relatively risky payday lender for less creditworthy people. Businesses in Brazil and Brexitland are unlikely to boost investor sentiment. Earnings have been heavily adjusted, hence the low P/E (non-GAAP bumtsi bum).

Comparables include the nearly crashed OnDeck and Lending Club. The entire industry is currently plagued by abuses, increased regulation, and a poor reputation. Stock pickers should be careful

After a couple of days of refreshing my memory, the old urge started to kick in, and I ended up buying a tiny bit of Axos Financial bank just before their earnings release. The bank’s consistent performance is reassuring, even though the potential of the latest acquisitions is yet to be fully realized. Another thing that slightly worries me is the sustainability of its competitive advantages. A few years ago, the benefits of operating as an online bank were obvious, as other banks struggled with brick-and-mortar branches and the initial steps of digitalization. Now, the banking sector is commoditizing rapidly, and Axos too needs to maintain a swift pace to stay ahead.

The forward P/E of 9x also smells deceptively cheap, but the company’s key figures and margins have remained stable in recent years. In the long run, if a 15-17% ROE can be maintained, this has the makings of a steady accumulator for the corner of the portfolio.

Axos’ FY Q2’20 diluted EPS was pretty much in line with expectations

SAN DIEGO–(BUSINESS WIRE)-- Axos Financial, Inc. (AXO) (NYSE: AX) (“Axos”), parent company of Axos Bank (the “Bank”), today announced financial results for the second fiscal quarter ended December 31, 2019. Net income was $41.3 million, an increase of 6.3% from $38.8 million for the quarter ended December 31, 2018. Earnings attributable to Axos’ common stockholders were $41.2 million or $0.67 per diluted share for the second quarter of fiscal 2020, an increase of 6.3% from $38.8 million or $0.62 per diluted share for the second quarter ended December 31, 2018.

Intrum’s excellent result was rewarded with a small share price increase today. The result (adjusted for one-off items) was approximately SEK 27 and the 2020 EPS guidance is still SEK 35 - the share price is currently SEK 278. The dividend was raised from SEK 9.50 to SEK 11. All in all, quite favorably priced with the 2020 guidance.

Related to the topic: what foreign Inderes-style sites do you use or could recommend for tracking foreign stocks? English, German, and Swedish sites would be fine.

I just went through the report and it looked really good The morning’s mess-ups due to the trade freeze and the result, without cleaning up one-off items, made my heart skip a few beats when I quickly looked at it.

Intrum is by far my biggest holding, and today I bought a good amount more right at the open I’ve been sleeping peacefully with this one, and now I can go to sleep with a good feeling again!

It’s a tough performance if they reach those 2020 targets, and it seems to be looking good. There’s also a new strategy update at CMD in the summer, so that could give it more wind in its sails.

Here’s a summary of how the wind business is currently performing from the perspective of the two largest players (Vestas & Siemens Gamesa). The article was written before the earnings releases but provides guidance for the future.

Bill Ackman’s hedge fund has sold all of its holdings in both Starbucks and ADP (Automatic Data Processing Inc). Profits were cashed in on time, with Starbucks up 73% and ADP up 50%. This year, there will probably be more nervousness and temptations to cash in profits – those downturns can always present buying opportunities.

Has anyone invested in music industry companies? Spotify or record labels?

I noticed that Warner Music Group is listing on the US stock exchange. I don’t know if it was Ed Sheeran’s picture or the billions mentioned in the article that made me a bit more interested in this