Let’s add Elisa’s press release from yesterday about the cable incident in the Gulf of Finland, in case the markets react to this in some way: Uutishuone - Elisa

Elisa has a disruption in its subsea cable connections between Finland and Estonia in the Gulf of Finland. Disruptions were detected on Wednesday evening in two of Elisa’s subsea cables. Elisa has been in contact with Finnish and Estonian authorities regarding the incident, and they are investigating the matter. Due to the network’s redundant structure, the disruptions have no impact on Elisa’s services in Finland or Estonia. The disruptions may have affected business and operator customers who have acquired direct transmission connections from the cables. Preparations for fault repair are underway.

Elisa’s revenue and profit are more sensitive than before to the mobile business, which accounts for about half of the entire group’s revenue and, in my estimation, even over 80% of the operating margin.

I don’t believe it will be possible in the coming year to capitalize on the rise in the average price of subscriptions, as was done in the last two years – and the lower sales costs brought about by smaller sales volumes that this enabled. Therefore, maintaining the number of subscriptions becomes even more important.

Elisa’s subscription numbers have occasionally been under pressure in Finland, especially on the consumer side, as DNA/MOI gained market share.

On the corporate side, acquiring subscriptions might be easier. Although the mobile subscription market is already clearly saturated as a whole, an exception to this is the growing B2B IoT subscription market. For example, the majority of new electric cars have a subscription – though hardly worth more than a few euros. Indeed, Elisa’s number of IoT subscriptions has grown well.

/edit better picture

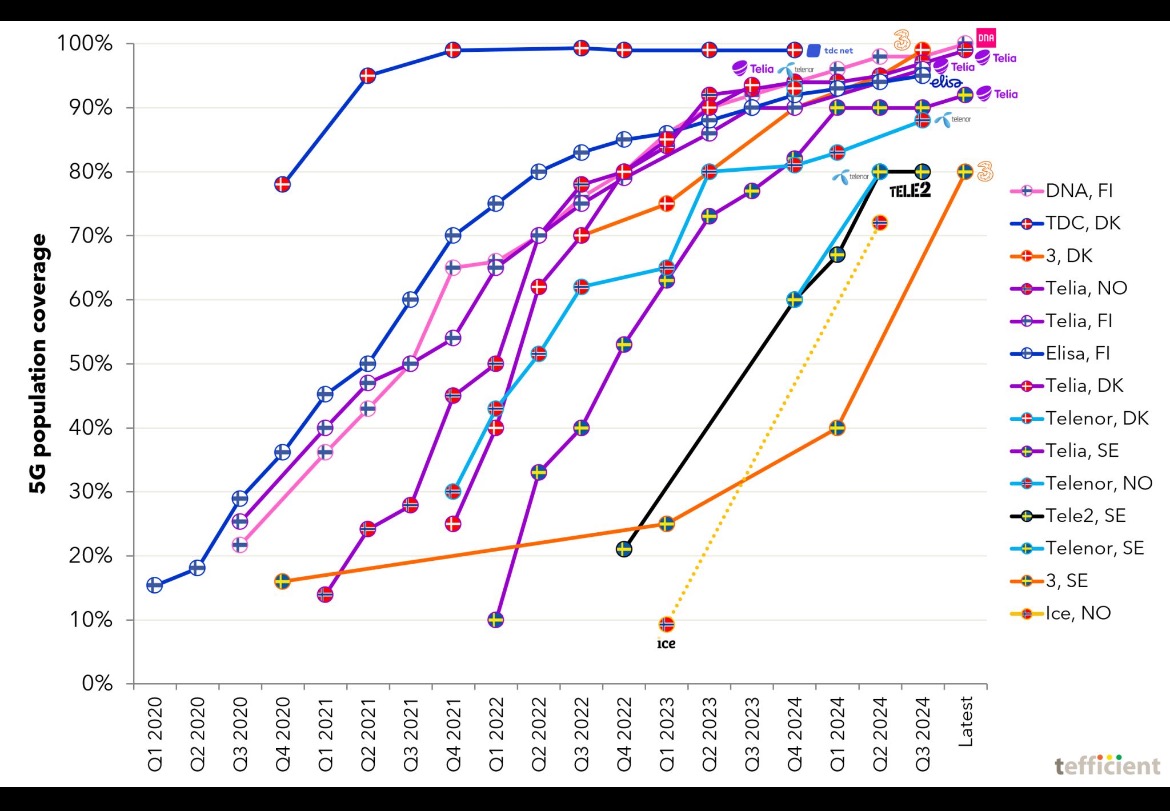

I spotted another interesting Tefficient comparison on LinkedIn, according to which Elisa, DNA, and also Telia are already reaching their limits with their 5G networks in Finland - at least when comparing how large a portion of the population is covered by the 5G network.

Now that earnings season is approaching again, here’s a suggestion for a topic with which one could challenge even Manner - or why not competitors too: if 5G networks are already built, would now be a good time to reduce CAPEX and thus improve cash flow - and thereby increase dividends? If there’s no longer a need to invest in the mobile radio network with the same intensity, then where can an operator in Finland get returns exceeding the required rate of return for those over 200M annual investments?

It is highly interpretive what kind of network needs to be ready, as well as what level the operator and its customers are satisfied with. In any case, there is still work to be done to get even 4G working in some way in all those areas where connections were lost due to the 3G shutdown. In urban areas and their fringes, antenna reorientations might sometimes be enough, but in many places, more hardware is needed.

“True” 5G networks, which operate without 4G network support and offer the advertised short response times of 5G, seem to be found only in limited areas of some major cities (?). I couldn’t find maps for these.

Otherwise, 5G operates on top of the 4G network, primarily bringing additional speed. In cities where 5G uses higher frequencies and wider bandwidth, 5G can significantly increase speeds. However, 5G operating on the 700 MHz frequency, built in the 5G hype, does not achieve impressive speeds, and an additional 4G transmitter could yield the same or even partially better results. The sale of 5G subscriptions will certainly go better if the 5G logo can be displayed in the corner of the customer’s phone screen.

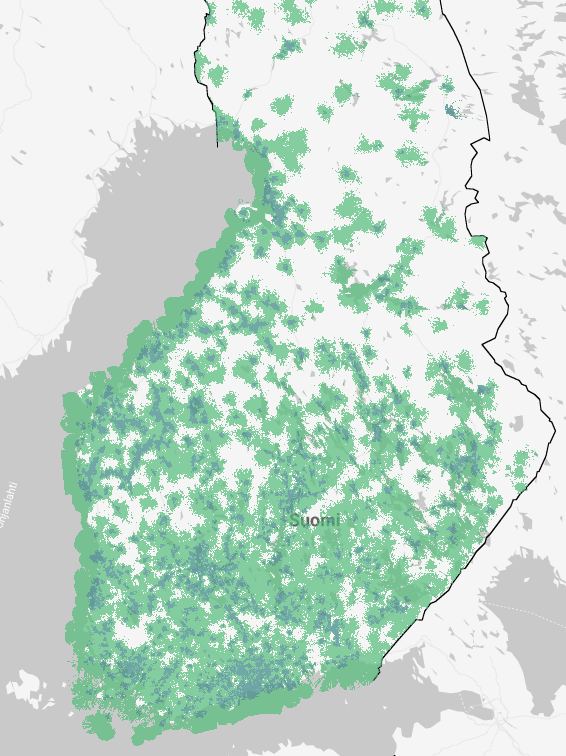

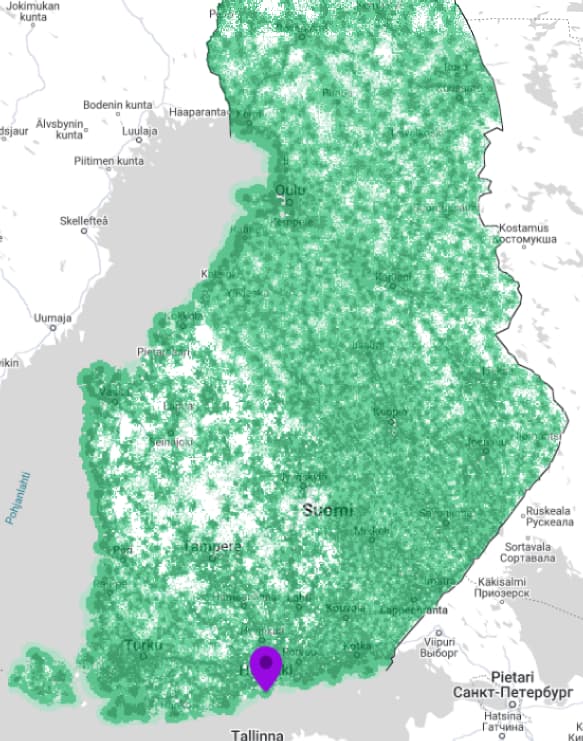

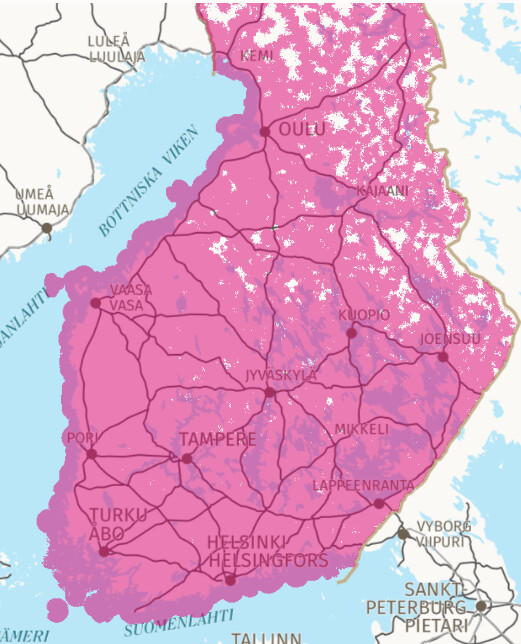

Below are the 5G coverage maps for all operators, which provide some idea of the coverage areas.

Will that investment money be saved, or will it next be invested where it hasn’t been enough until now due to prioritization? At least the DNA CEO is of the opinion that investments will continue in the radio network as well.

The geographical coverage area is of course different from the population coverage area. There are certainly good reasons why this higher frequency 5G is not usually built in areas with low population coverage.

Flash news from Kauppalehti: ABG Sundal Collier raised Elisa’s stock recommendation to buy, previously hold. Target price still 50 euros

@Joni_Gronqvist hasn’t yet had time to change his recommendation following the share price; the ‘reduce’ recommendation was probably only relevant for a couple of days in October, as the price immediately started to fall. Is it even the case now that Inderes is currently the only one with a ‘reduce’ recommendation? This, of course, negatively affects the consensus, though an informed investor can draw their own conclusions about whether to buy the stock now. Elisa’s financial statement release is then due on Friday, January 31st.

Adding a flash news item from Kauppalehti on Jan 23rd to maintain the consensus recommendation: DNB Markets lowers Elisa’s target price to 47.00 euros (previously 48.00 euros), reiterates hold recommendation.

Elisa recruits 100 AI experts. Could the underlying belief be that companies with a lot of customer data will be the next to benefit from the AI trend?

Here’s Joni’s preview as Elisa publishes its Q4 report on Friday.

Elisa will publish its Q4 report on Friday at approximately 8:30 AM, and the company’s earnings release can be followed here at 12:00 PM. The operator market has been better than in years for some time now, creating a good operating environment. Furthermore, Elisa’s business has long been highly predictable and a leader in the sector, based on long-term and consistent strategy execution. For Q4, we forecast moderate revenue growth and profitability to have remained at the comparison period’s level. We expect typical guidance from the company, indicating growth or a level consistent with the comparison period. Additionally, we expect the board to propose an increasing dividend for the past year as well. Elisa’s share valuation has become attractive due to the share price decline (2025e P/E 17x and EV/EBIT 16x).

According to a Kauppalehti article, Elisa is the largest owner of fiber optic operator Lounea. Is Elisa trying to continue its creeping acquisition before Lounea manages to list - as they state their plan in the article? Lounea has many customers in the growing fiber market for detached houses, where Elisa is still lagging behind.

Below are Joni’s comments on the morning’s result.

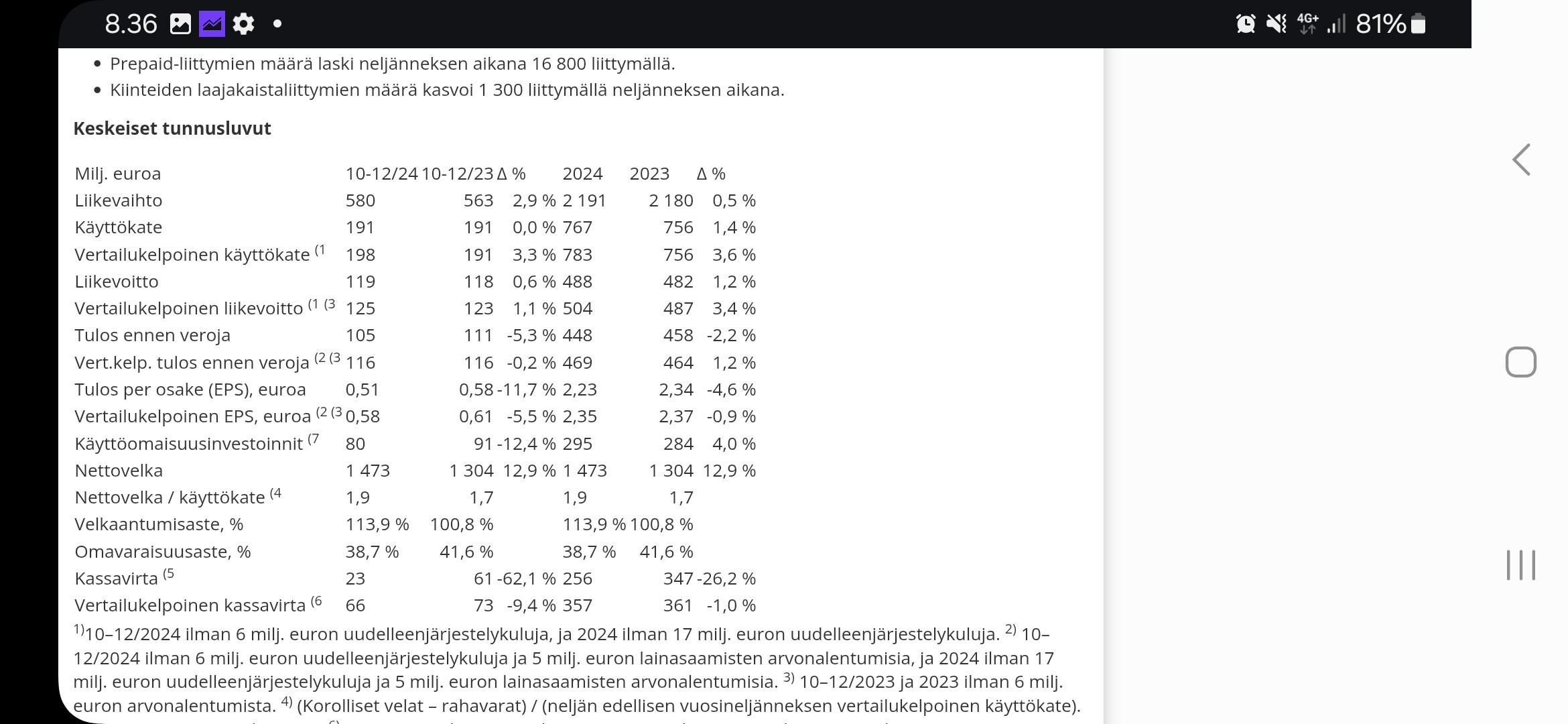

Elisa’s Q4 report, published this morning, was overall in line with our and market expectations. Revenue grew slightly better than expected, while comparable EBITDA was well in line with expectations. On the lower income lines, results were slightly below forecasts. The company guided, as is customary, that revenue and EBITDA would be at the comparable period’s level or grow slightly in 2025. The Board’s dividend proposal was slightly higher than the market expected and a small positive surprise.

The melting of the subscriber count looked quite ugly in that report. On the consumer side, they probably lost over 30k units, and on the business side, they also went negative if those low ARPU m2m subscriptions are excluded from the calculations. Elisa can still raise prices, but they can’t ride that forever…

If I read the reports correctly, Telia’s subscription numbers are also decreasing in all Nordic countries if those various device network subscriptions are not taken into account. This development is perhaps surprising if the subscription numbers are truly decreasing and Telia’s and Elisa’s customers have not switched to other operators.

In Finland, at least, the fiber optic boom has somewhat reduced subscriptions as home internet has switched from mobile to fiber. I don’t know if there have been any changes in the number of employee subscriptions. I can’t think of any other reasons offhand.

Device network subscriptions can also be good business as long as billing and subscription management costs can be kept sufficiently low. Usually, the amount of data transferred in these is small and thus does not burden the network much. The growth in the number of these subscriptions is not surprising.

Here’s the earnings day interview from Pasila. Quite a wide range of topics. In my opinion, the most important ones are the competitive environment, AI investments and AI’s broader market impact, as well as capital allocation, including share buybacks.

Topics:

00:00 Q4’24

01:41 “International software business is Elisa’s way of internationalization”

02:34 5G upselling and competitive environment

06:20 Gulf of Finland cable breaks and securing Elisa’s network

08:10 Significant investment in AI

09:38 DeepSeek and the acceleration of AI development

10:48 How does Elisa benefit from AI?

12:05 Principles of capital allocation

14:30 Return to old ways in CAPEx

15:17 Share buybacks

16:15 Upcoming CMD: “Faster, profitable growth”

I’m also sharing these charts I’ve been working on in the thread. The data source is Elisa’s IR pages and the Excel file “Operational and Financial Data Q4 2024 (.xlsx)” from there.

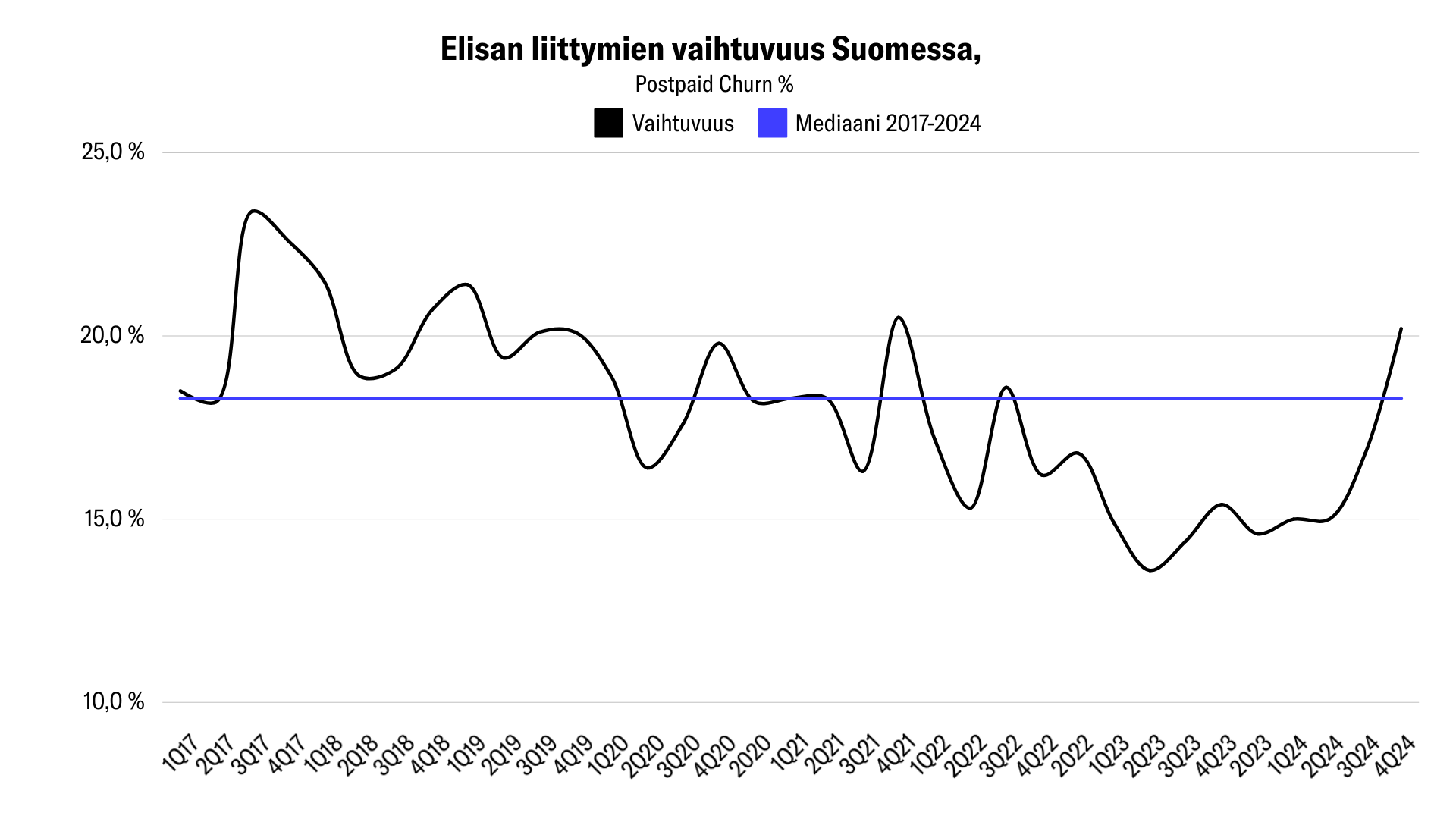

Postpaid subscription churn 2017-2024 quarterly. Campaigning has been evidently aggressive during “black weeks,” especially in 4G. Median around 18% 2017-2024, Q4’24 jump to 20.2%.

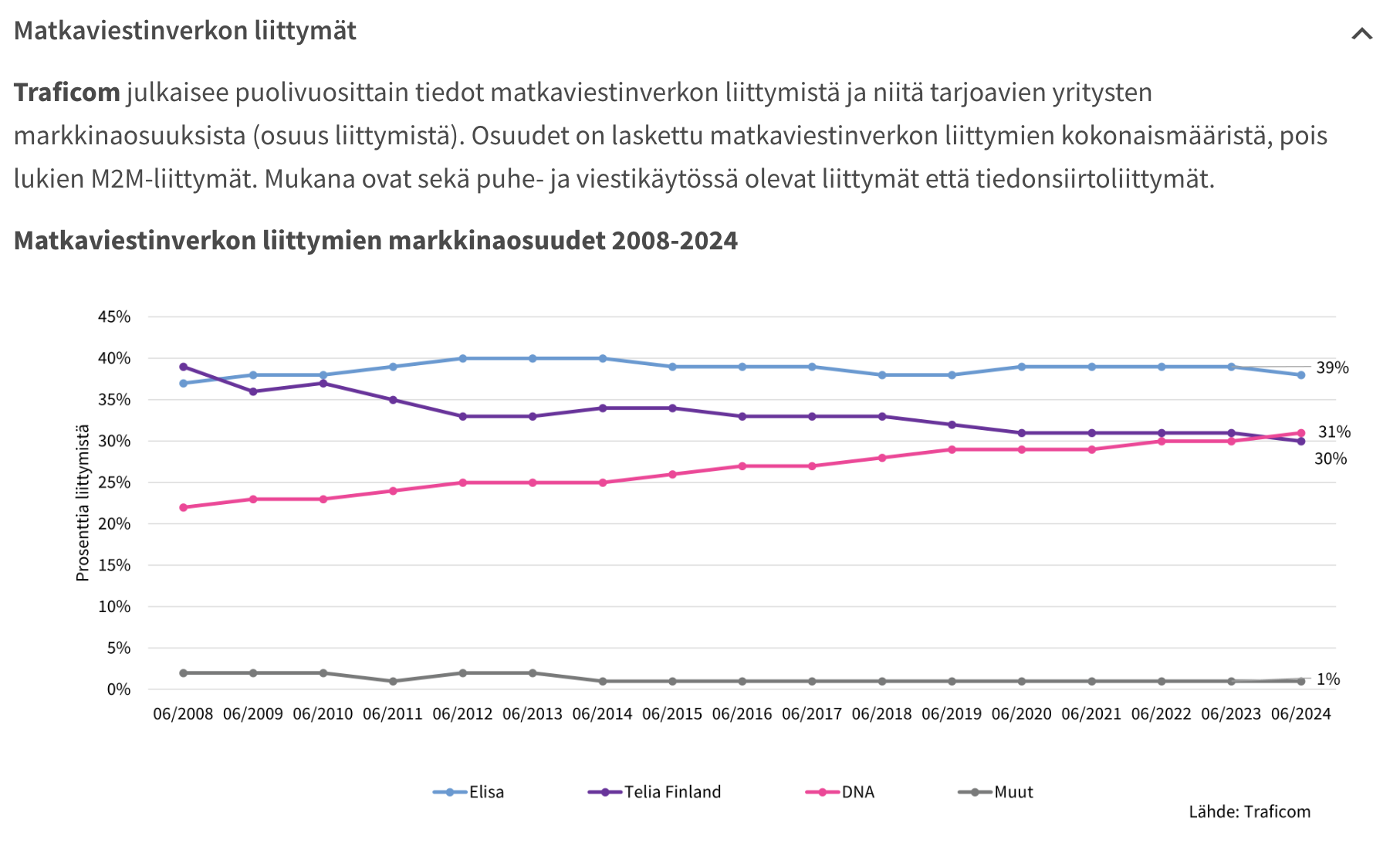

DNA has overtaken and secured the 2nd place in the Finnish market. Source: FiCom

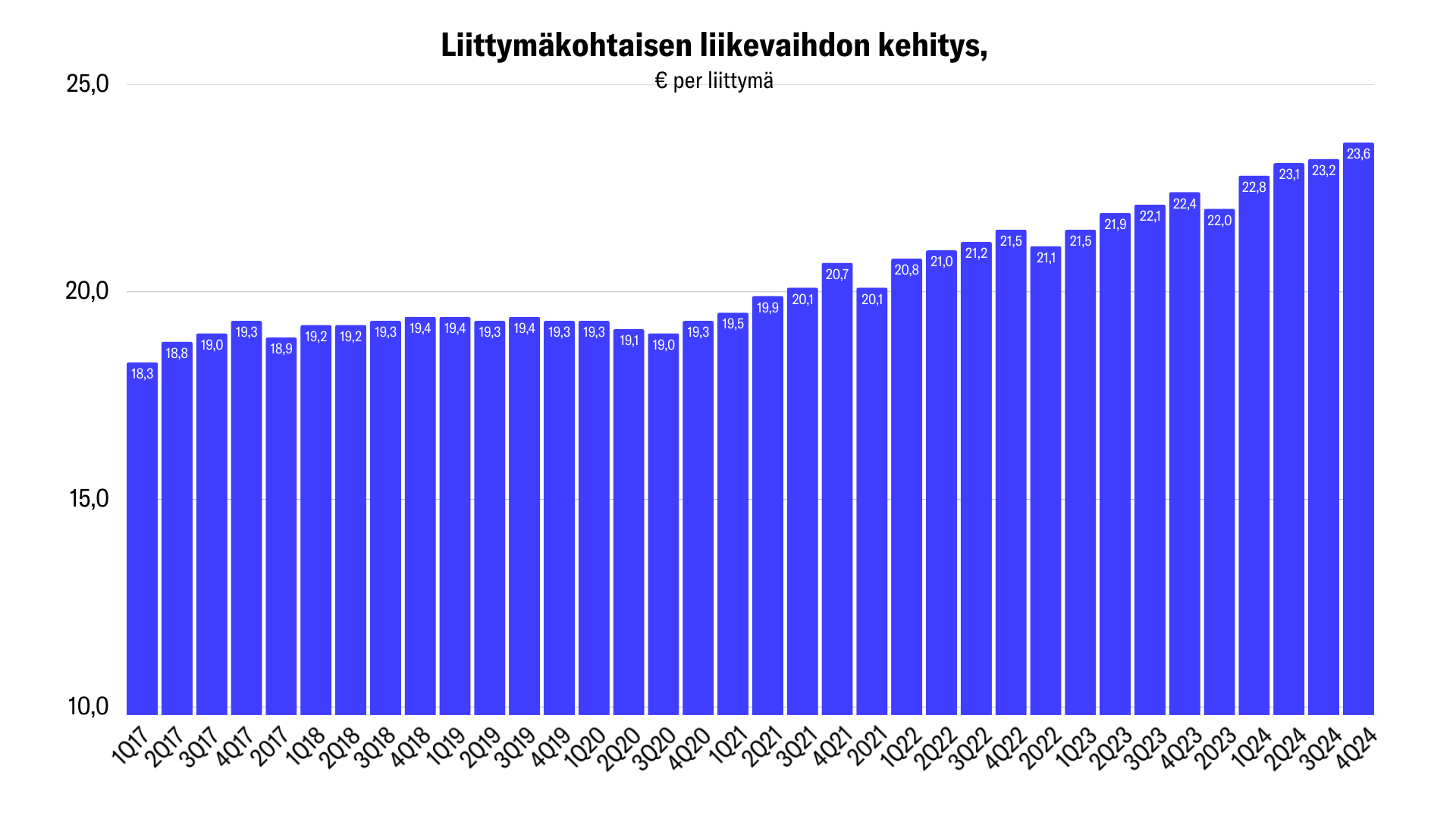

5G upselling and 4G price increases are also reflected in ARPU (average revenue per subscription). Significantly more euros have been generated in recent years, with inflation, of course, being present.

I’ll share my perspective on the impact of Finland’s fiber optic boom on Elisa’s subscription numbers.

There are currently a large number of aggressively expanding fiber optic operators in Finland, and I would imagine that in Q3-Q4 2024, these operators completed the construction of something in the order of 100,000 new fiber optic connections (gut feeling/guess). Many of these households had 5G FWA from major operators, which were then terminated during the end of the year.