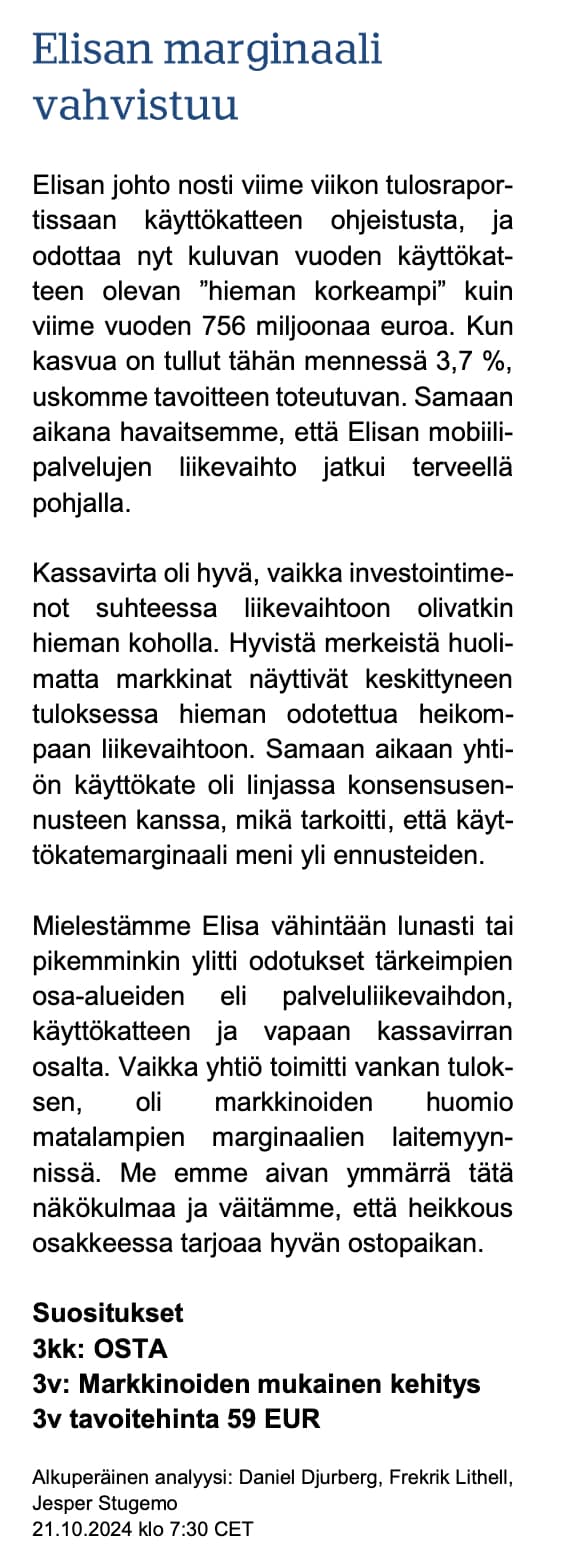

Here is the earnings preview by @Joni_Gronqvist. The forecasts for the key line items are exactly in line with the consensus. As Gröni writes, it will be interesting to read and hear Elisa’s comments on the corporate customer environment, as in the previous quarter, it was noted that the situation had moved in a better direction.

13 Likes

Elisa announces the acquisition of sedApta Group, which employs over 500 professionals and serves more than 1,500 customers. The company’s revenue in 2023 was EUR 49 million.

Elisa and the owners of sedApta Group have signed an agreement under which Elisa will acquire the remaining share capital (81 per cent) of sedApta Group. Elisa acquired a minority stake (19 per cent) in sedApta in 2021. The transaction is expected to close in October 2024.

11 Likes

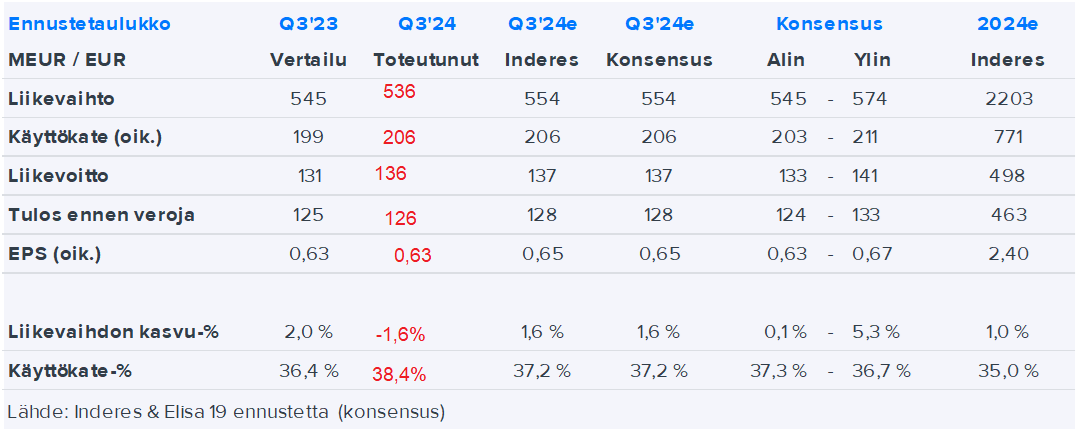

Interim report is out: https://www.inderes.fi/releases/elisa-oyj-elisan-osavuosikatsaus-q3-2024

ELISA OYJ INTERIM REPORT RELEASE 18 OCT 2024 AT 8:30 AM

Key figures for the third quarter of 2024

- Revenue decreased by EUR 9 million to EUR 536 million, mainly due to a decline in equipment sales and regulated revenue, as well as the net effect of acquisitions and divestments.

- Mobile service revenue increased by 4.8 per cent to EUR 254 million.

- EBITDA increased by EUR 7 million to EUR 206 million.

- EBIT increased by EUR 5 million to EUR 136 million.

- Comparable cash flow increased by EUR 4 million to EUR 111 million.

- In Finland, mobile postpaid ARPU rose to EUR 23.2 (23.1 in the previous quarter) and postpaid churn rose to 16.8 per cent (15.0).

- The number of postpaid subscriptions increased by 27,700 during the quarter. The number of M2M and IoT subscriptions increased by 39,800.

- The number of prepaid subscriptions increased by 14,000 during the quarter.

- The number of fixed broadband subscriptions increased by 8,200 during the quarter.

- Regarding EBITDA, the guidance for 2024 has been raised to “slightly higher” (previously “at the same level or slightly higher”).

Actuals vs. estimates quickly punched into a table:

20 Likes

Traditional greetings from Pasila at Elisa’s briefing in the spirit of the earnings season. Analysts seemed to have plenty of questions today, as the briefing stretched to 1.5 hours, and our interview wasn’t short either, reaching a full 20 minutes. Hopefully, this will be of interest and benefit to many.

In addition to the traditional quarterly questions, we discussed Elisa’s competitive advantages, the new loyalty program, and the growth in the number of employees, topics that have been discussed on the Forum. I believe it is important to always include investor-related topics and questions in these interviews, and for this reason, it is good to follow the discussion on the board and participate in it yourself. As usual, timestamps can be found below, so everyone can skip to the parts most relevant to them.

Timestamps:

00:00 Q3’24 highlights

01:38 Lower revenue, better profitability

03:55 Competitive landscape and subscription churn

06:35 Key growth drivers for mobile service revenue

07:37 Elisa Loyalty Program (Etuohjelma), “Share of Wallet” and the termination of S-bonus cooperation

10:22 Changes in headcount and personnel structure

12:08 Active utilization of AI as part of Elisa’s daily operations

14:38 The Huawei dispute between Estonia and Elisa

17:35 Elisa’s competitive advantages and their sustainability

19 Likes

Tough questions and high-quality answers from Topi, considering he has only been at the helm for six months ![]()

Regarding business numbering, I might challenge the answer: as I understand it, its margins were significant before the legislative change at the end of last year – although some of the lost margin has been recovered by maneuvering them into consumer subscriptions through various means.

Regarding the interim report, I was a bit surprised by the ARPU development on the corporate side. While the growth continued on the consumer side, postpaid ARPU in corporate subscriptions dropped. Has Elisa perhaps taken on large accounts based on price?

As for the comment on headcount, it is of course true that you can grow very capital-efficiently in the IT business. Naturally, this requires that the utilization rate of consultants and experts is at a high level. I wonder what it might be at Elisa? I would also be interested to know if the corporate business is being grown through third-party license businesses, where margins can be slim.

5 Likes

The Head of the Consumer Customers unit has sold more than half of their shares (had 35,379 shares, of which 20,000 were sold here).

10 Likes

Handelsbanken’s morning briefing featured an analysis of Elisa.

13 Likes

To follow up on HB’s comments, here is a summary of OP’s view on the past quarter and the stock’s valuation.

According to OP, Elisa’s revenue miss relative to expectations was not particularly dramatic, as performance was strong in the “revenue items essential for the result.” Regarding customer churn, OP commented that the quarter saw “a few irrational campaigns” from competitors, and Elisa lost 12,000 postpaid customers. Risks for aggressive price campaigning still exist heading into the end of the year (e.g., Black Friday and Christmas campaigns).

The stock’s valuation is high, as is customary. On a rolling 12-month forward EV/EBITDA basis, it is currently around the 10-year median (~11-12x). During 2019–2022, levels were significantly higher than this, largely driven by zero interest rates. OP’s recommendation based on current information is Reduce.

Regarding the sedApta acquisition, OP notes that Elisa paid a “quite reasonable” price for the business (9–10x EBIT).

12 Likes

Oh yes, thank you!!!

I am the dividend party.

![]()

![]()

![]()

9 Likes

On Saturday, the print edition of Hesari featured a full-page article (non-paywalled) about energy storage/battery systems sold to households, using a household that had chosen Elisa as its provider as an example. I didn’t know that Elisa sells this solution to households in addition to telecommunications operators. At Elisa’s scale, this naturally has only a small impact on the company’s figures, but it illustrates how their own innovations (“Distributed Energy Storage”) are being commercialized on the B2C side in addition to B2B.

Energy is naturally stored in the battery when it is cheap and released for use when it is expensive. Elisa’s AI-driven system controls the use of the battery and, simultaneously, the entire house’s electrical system. The battery capacity is also used in the reserve markets, and the resulting benefit is shared between Elisa and the customer. However, the premise of the system is that the battery is primarily the home’s “energy storage.”

The article goes through theoretical calculations regarding the solution’s profitability for the consumer: the example household pays 6,000 euros for the battery via an installment plan over 10 years and 2,000 euros for installation. According to Elisa’s calculation, the battery generates an average monthly saving of about 17 euros for the household. In the calculation presented for the household featured in the article, the market return was estimated at 35 euros per month.

According to Hesari, Elisa sells battery systems with a ten-year installment plan. The interviewed household pays 49.99 euros per month for the battery, totaling 6,000 euros over ten years. In addition, the installation work cost 2,000 euros.

It will be interesting to see what kind of business this might potentially become in the future. Large-scale energy storage would at least be an important safety valve for the electrical system. In this case as well, the actual sale of equipment is unlikely to have higher margins for Elisa than typical hardware sales.

13 Likes

Target price and recommendation updated in the right direction ![]()

![]()

![]()

16 Likes

Speaking of which: By the way, here is another fairly recent experiment from Elisa in the field of home monitoring:

In this business, the market in Finland is already quite large (in the 60-80M range) with 5-10% annual growth – driven, of course, by the aggressive sales tactics of Verisure and Sector Alarm. Of course, only the former seems to be profitable yet.

In my opinion, these kinds of hardware-related experiments are probably more acceptable for Elisa because they can leverage built-up capabilities. Otherwise, for telecom operators, new services carry the pitfall risk of unprofitable diversification. For example, under the Vahti brand, Elisa has already played in the home security market twice before over the years, ending in the service being discontinued.

Good to try new things, as long as that 40% EBITDA margin remains ![]()

5 Likes

Yum yum ![]()

![]()

![]()

![]()

![]()

![]()

10 Likes

Telia is taking jabs at its competitors Elisa and DNA over the use of Huawei in their networks (paywall).

The matter is not new in itself, and if I recall correctly, this has also been one of the key points in Telia’s marketing.

In the previous earnings day interview, I asked what share Huawei has in Elisa’s networks. The answer was 15% from memory. According to Hesari, DNA utilizes “clearly the most Huawei products based on information obtained by HS from several sources.”

Telia’s country manager comments in this article that the company’s decision to build the 5G network with Nokia products was based on a “careful risk assessment” and that “it was more expensive with Nokia’s equipment and software than with Huawei’s products.” Costs are not commented on.

The article states that in many EU countries, the use of Huawei equipment in critical parts of mobile networks is prohibited based on a recommendation issued by the Commission. In Finland, the starting point is that network technology is treated neutrally, an official comments.

11 Likes

Elisa’s Marketing Director is changing.

It is unusual, at least among Finnish operators, to have a Marketing Director at all. At Telia and DNA, the function is within customer segments.

5 Likes

@Karo_Hamalainen interviewed Elisa’s Topi Manner in their latest interview session. ![]()

Dividends are an essential part of Elisa’s investment story. Although Elisa distributes 80–100 percent of its net profit as dividends according to its dividend policy, its dividend yield does not reach the top positions in the operator world.

The key to Elisa’s dividend story is dividend growth. This year, the dividend increased for the tenth consecutive time.

“A dividend is a clearly understandable and easily communicable way from the shareholders’ perspective, and very concrete in the sense that cash comes to one’s own account,” says Elisa’s CEO Topi Manner.

He admits that buying back own shares is more tax-efficient for some owners than dividend payment, but assures that Elisa will stick to its dividend policy.

“If there are, so to speak, additional distribution opportunities, then share buybacks are also a useful tool,” Manner adds.

Unlike many other companies, Elisa has not canceled its own shares. Portions of them have been carved out for share-based compensation needs, but they could also be used as a means of payment in acquisitions.

“We have a lot of firepower on our balance sheet for potential acquisitions,” Manner points out. “We will use it in a targeted, carefully considered manner for complementary acquisitions. Not for large acquisitions, but for complementary, value-creating acquisitions when we see that the target meets our strict criteria.”

13 Likes

Corporate Responsibility Director Minna Kröger spoke about her company as an investment target at the ESG Days. ![]()

3 Likes

Since I found it in the Nokia thread, let’s share the fruit of Elisa’s and Nokia’s cooperation here too: Uutishuone - Elisa

Peeking into the future of networks in Espoo: Europe’s first 5G cloud network opened for customer traffic

Cloud-based mobile networks are arriving in Finland: Elisa and Nokia have opened Europe’s first 5G cloud network (Cloud Radio Access Network) for customer traffic in Espoo. This is a concrete step towards the 6G era, when mobile networks are expected to be largely cloud-based. Cloudification also serves Elisa’s goal of developing autonomous, self-steering and self-healing networks.

6 Likes

More discontinuity, the chairman of the board will change next spring and Christoph Vitzthum, who only joined the board this year, will take the helm; also Antti Vasara, who has been on the board since 2017, will step aside in the spring: Elisa Oyj: Osakkeenomistajien nimitystoimikunnan ehdotus Elisan hallituksen kokoonpanoksi ja hallituksen palkkioiksi | Kauppalehti

“The Shareholders’ Nomination Board proposes two new members to Elisa’s Board of Directors. Urs Schaeppi is an experienced industry expert, and Tuomas Hyyryläinen has diverse management experience from various companies. Current chairman Anssi Vanjoki and Antti Vasara are stepping down from the Board. The Nomination Board wishes to thank them at this stage for their long and valuable work for the company. During Vanjoki’s chairmanship, Elisa has developed excellently, and a CEO change has been successfully implemented in the company. We propose current board member Christoph Vitzthum as the new chairman, who is an experienced business leader and has previously successfully served as chairman of the board for Konecranes, among others,” says Pauli Anttila, Chairman of Elisa’s Shareholders’ Nomination Board.

6 Likes

Here’s a SalkunRakentaja article about Elisa that can be read in a couple of minutes, quoting OP. ![]()

OP raises Elisa’s recommendation from the previous ‘reduce’ level to ‘add’ level, but the target price decreases from 47 euros to 45 euros.

The bank states in its morning report that Elisa’s stock valuation is again attractive, as the EV/EBITDA multiple has decreased to 9.5x. Elisa is traditionally a good dividend payer, and OP expects a 5.8 percent dividend yield for next year. However, a key risk for the company is the potential stagnation of mobile communications service revenue growth. According to OP, the 5G transition still offers an opportunity for higher average billing, but especially for consumer customers, current 4G connection speeds are well sufficient for current services.

9 Likes