Specifically, this market has been grown through price increases. In particular, the price level of mobile subscriptions in the consumer segment has risen significantly over the past 12 months. Since the actual number of subscriptions in the market is barely growing, this trend has been very profitable for all players. This has been reflected in how all three operators have actively followed each other’s price hikes. I personally suspect that by next spring at the latest, the game will change and they will start chasing market share in addition to overall market growth.

5 Likes

An individual operator certainly has limited opportunities to raise prices, as switching plans is easy and most customers don’t see significant differences between networks. Otherwise, the industry can raise prices to whatever level they wish, provided there is no direct cartel or price-fixing.

It remains to be seen what the basis for competition will be in the future; perhaps more focus on data speeds than currently.

One would expect the number of cheap data plans to increase alongside the rise of various remote-operated devices. For example, more and more cabins have surveillance cameras, heating control/monitoring, etc., which people want to function 24/7/365.

A cheap and fast data plan for a customer in some sparsely populated cottage community. Sounds expensive for the operator. Costly to build and only a few users.

In new cars, especially electric ones, all of them seem to have some kind of subscription. There could be room for growth here, but expansion there won’t happen without competition either.

So, what remains is cost cutting. Laying people off in droves, and when the whining starts in the papers that services are deteriorating, bringing a few back to fix the worst trouble spots.

At Elisa, specifically the number of these device internet (laitenetti) etc. subscriptions grew well in the last quarter:

“The number of postpaid subscriptions grew by 42,100 during the quarter. The number of M2M and IoT subscriptions

grew by 47,100.”

My guess is that the growth won’t slow down anytime soon, as there are more and more different devices being connected to the internet and, for one reason or another, they can’t or aren’t wanted to be put on Wi-Fi.

Typically, these subscriptions have low speeds and data amounts, but on the other hand, also low prices—and the lower the monthly fees, the lower the threshold for getting them. In my own work, it is often found to be more cost-effective to get a 4G modem and a cheap subscription than to start tinkering with an internet connection by other means, even though there would generally be no technical obstacle to it. Over years or even decades, of course, those monthly fees also add up to a certain sum.

2 Likes

Telia starts change negotiations to improve profitability:

6 Likes

A particular risk to the stock is posed by sales practices where customers are sold expensive subscriptions they cannot use or which see zero usage. The primary risk group is elderly people who don’t understand what they are signing up for. Sales ethics aren’t necessarily high when personal commissions are on the other side of the scale.

If children or acquaintances were to check these subscriptions, I believe there would be quite an outcry. My personal experience is that sales tactics have no moral limits. I recommend checking your relatives’ mobile bills; you might be truly surprised.

Is the operator’s bottom line partly based on selling unnecessary services? This is not necessarily a good equation for shareholders.

1 Like

Isn’t a large part of consumer business exactly this kind of selling to manufactured needs? In reality, people would get by with a fraction of the goods and services they acquire driven by marketing.

3 Likes

That is exactly what economic growth is based on. However, everything has its limits. You don’t sell tractor tires for a car, do you? Or do they?

No, nor water utility connections for mobile phones. For both, suitable and functional solutions are sold, but ones that are too expensive for their intended purpose.

3 Likes

Lauri Nikula’s article on Elisa, which can be read in a couple of minutes. Mostly familiar information for those who have followed the company.

Elisa’s organic growth is quite slow, which is reflected in low growth points. The stock’s valuation is also slightly higher than average. Currently, Elisa’s P/E ratio, measured by the 2024 earnings per share forecast, is 19.6.

https://www.sijoittaja.fi/418740/viikon-laatuosake-elisan-osake-on-kaantynyt-tasaiseen-nousuun/

7 Likes

Elisa has launched a benefit program, and there has been a lot of marketing in recent days, for example on the radio.

11 Likes

I wonder if that is a good thing?

As an investor, this feels like an attempt to create additional costs for the company (program administration and the benefits granted). So, will customer retention improve enough to pay for itself? I wonder if the program will be reported as a subscription cost or as general marketing?

As a customer, I am only interested in benefits related to the service I have purchased. For example, getting a discount for being a long-term customer or receiving a free week after a certain duration of membership.

2 Likes

The good thing here, of course, is that the benefits seem to be either those that don’t cost Elisa very much or are benefits linked to additional purchases. This type of benefit program is fundamentally different in terms of costs compared to, for instance, the S-Group (S-Ryhmä) program, where actual cash is returned.

For example, at the Platinum level, phones, devices, Oma Guru (Personal Guru), and maintenance services are offered at a discount. No one is saying that a margin wouldn’t still be made on these. And even if there were some subsidization, the business case may remain positive if loyalty toward the core products (mobile or broadband subscriptions) increases at the same time.

Of course, from the customer’s perspective, this kind of program may seem like nonsense compared to other bonus programs that provide tangible cash.

3 Likes

Finland has a fairly high churn rate in mobile phone subscriptions. In such a situation, it is worth fine-tuning “retention programs”. An annual 15% turnover of the customer base is incredibly expensive, and even a small change in the churn rate has a surprisingly drastic direct impact on profitability…

6 Likes

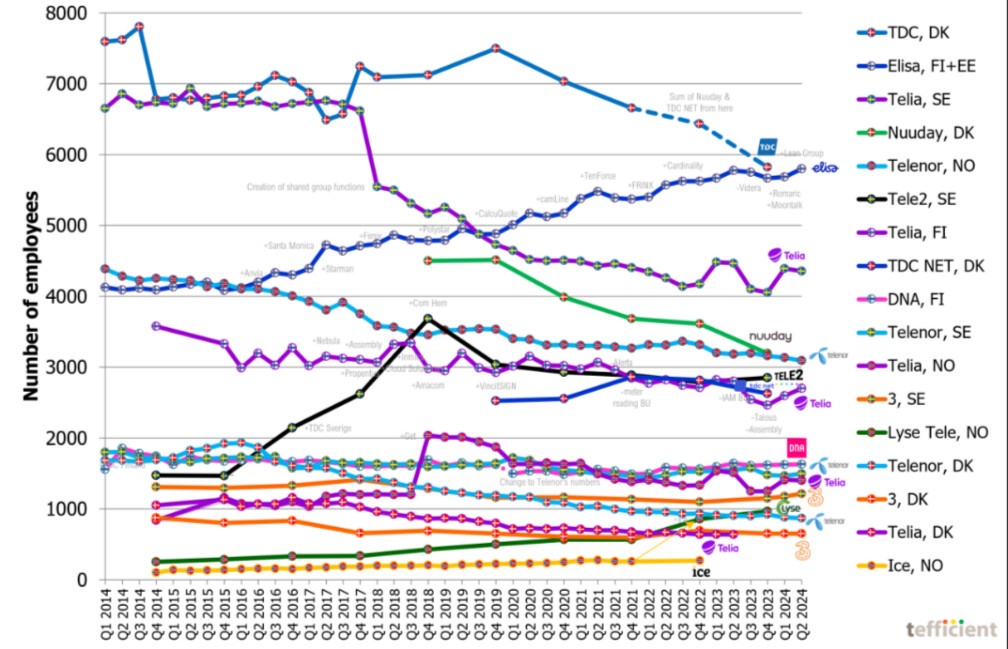

By the way, here is a comparison spotted recently on Tefficient’s LinkedIn page, showing the headcount of Nordic telecom operators in various countries. Telia recently announced major layoffs, which seem to continue the trend of Telia’s decreasing employee numbers in different countries.

Elisa seems to be going in the completely opposite direction. The headcount appears to have been on a growing trend almost continuously over the past ten years (of course, also due to the impact of M&A). What do you think – could there be room for efficiency improvements at Elisa in this regard?

2 Likes

I am not familiar enough with these companies to know exactly what services each one offers or to what extent they use outsourced services.

For example, the headcount at Telia and DNA may have been affected by the fact that they have significantly downsized their own networks. Different companies have likely chosen different strategies regarding which services they produce in-house and which they outsource.

A few posts above, there was some talk about the bonus cooperation with the S Group; it will end at the end of 2024.

S Group Bonus on Elisa’s mobile and internet subscriptions - Elisa

3 Likes

Earnings season is once again just around the corner, and as a sign of that, OP has released its preliminary expectations for Elisa’s report. To avoid plagiarism, I’ll summarize these in my own words. OP expects slight earnings growth from Elisa (EBITDA +3%, EPS +5%) and a refinement of the full-year guidance for revenue and profit growth slightly upwards, as Elisa has been prone to do at this stage of the calendar year for many years.

According to OP’s interpretation, the competitive situation appears to have remained unchanged, and list prices for subscriptions have stayed above 30 euros. Naturally, sales “under the counter” occur at lower prices. Consequently, mobile service revenue is likely to continue showing solid growth of a few percent in this context. However, OP sees growth slowing down in the coming years as comparison figures become increasingly tough.

Over the past 6 months, Elisa’s share price has outperformed the sector, and along with the commentary, the recommendation turned from positive to negative: “A quality company, but the valuation is a bit too demanding.”

As usual, the earnings day interview will be conducted at the conclusion of the afternoon briefing. Suggestions for topics and questions can be left in the thread or sent via message. For example, the previously raised question here regarding views on Elisa’s competitive advantage is definitely worth asking the CEO himself.

10 Likes

Stronger than the sector perhaps, but looking at clear Finnish peers, Telia 6M +22.34% and Elisa +15.6%.

5 Likes

A note regarding Elisa: the difference between the list price and the “under-the-counter” price seems to only be growing. A few observations from the market:

- Elisa’s salespeople are openly selling using “rescue offers.” I’ve come across these a lot: they sell a 200M subscription for, say, €25.90, and at the same time, advise the customer to initiate a number porting process to, for example, Telia after a couple of months, after which an Elisa salesperson will call and offer a “rescue deal” at a price of €18.90.

- Elisa is fighting another price war against MOI. Those who switched to MOI are being lured back with an eight-euro monthly price. S-bonus benefits are being removed from Elisa’s subscriptions by the end of the year at the latest, which could further play into MOI’s hands.

Despite these factors, the average price of the customer base is indeed rising steadily and approaching the prices mentioned by Antti, as the share of customers who shop around for their subscription every month is only 1-2%.

7 Likes