One more thing: Why does Elisa keep its towers in its own ownership? Could Elisa get a better return on capital by selling its towers, either partially or in full?

1 Like

Maybe some conclusions can already be drawn from these ![]()

Elisa agreed with Voimatel on constructing a fiber optic network

Elisa continues to strengthen its fiber optic network and has agreed with Voimatel on building a network for 40 million euros in the coming years.

8 Likes

I’m not quite sure if these are the right questions to ask right now, but I’ll post them anyway. ![]()

1. What strategic measures have you implemented to achieve this positive development, especially regarding ARPU (Average Revenue Per User) growth and the decrease in churn?

2. Then an interesting question: what are the key factors through which you aim to keep the net debt to EBITDA ratio at an appropriate level in the future as well?

2 Likes

Results were very closely in line with consensus estimates.

- Revenue grew by 2 per cent, or EUR 9 million, to EUR 541 million.

- Mobile service revenue grew by 4.7 per cent to EUR 252 million.

- EBITDA grew by 4 per cent, or EUR 7 million, to EUR 190 million.

- Operating profit grew by 5 per cent, or EUR 6 million, to EUR 121 million.

18 Likes

Here are the initial analyst comments on the results.

It’s good to see and read that the international business has returned to rapid growth (+21%) and to see the comments about the recovery of corporate investments in general.

21 Likes

Here is Sijoittaja.fi’s piece on Elisa; there shouldn’t be much new if you’ve been following Inderes’ materials. ![]()

During the second quarter, Elisa continued to expand the coverage of our high-speed connections and services. In line with the company’s strategy, Elisa has also continued to carry out acquisitions that complement its business, and the acquisition of Leanware Oy, announced in April, was completed, which accelerates the growth of Elisa IndustrIQ’s industrial software business.

9 Likes

Analyst briefing materials published on Elisa’s website conveniently just as the webcast starts now at 12:00.

9 Likes

Here is the interview from the results day. ![]()

Topics:

00:00 Introduction

00:12 “Outlook improved in the corporate segment”

00:48 International software business is growing

01:21 First signs of investment recovery

02:18 5G momentum

03:25 Mobile service revenue growing faster than competitors

04:42 Pricing and trends for consumer and corporate subscriptions

05:46 Price competition and market share

07:10 “Investing more in fiber networks than ever before”

08:10 Does fiber compete with mobile broadband?

08:37 “We will not over-invest”

08:57 Towers are a strategic asset

09:47 Green bonds and loans as a form of financing

14 Likes

I was most surprised by the information that fiber optic connections do not significantly compete with mobile broadband.

Based on empirical observations, at least in this medium-sized city, streets are dug up in practically all detached house areas as multiple companies are laying fiber. When I randomly checked broadband availability on Elisa’s and Telia’s websites, very few addresses were offered anything other than 4G/5G.

In all likelihood, those opting for fiber are more likely to be those currently using unreliable mobile internet rather than those who already have a well-functioning fixed connection.

It seems clear that if Elisa has a 40% market share on the mobile side by some metric, it is not possible to achieve a similar share in the fiber market in a healthy way.

Personally, I see revenue growth opportunities for operators as the number of internet subscriptions for various homes, cottages, vehicles, etc., continues to grow. A “five-euro SIM” is more cost-effective and secure for many use cases than rigging up extra Wi-Fi antennas and connecting every possible device to the same internal network.

3 Likes

Why didn’t Elisa’s share price react positively after the Q2 results? The results were slightly better than expected…

3 Likes

Market expectations and consensus forecasts can differ from each other, and they often do. Otherwise, no stock price reaction to an earnings report would ever be surprising.

5 Likes

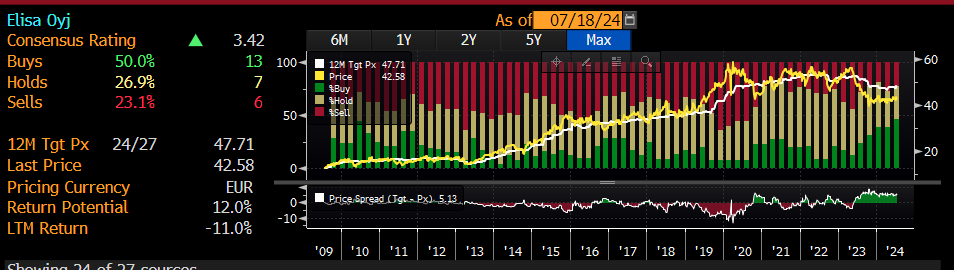

A snapshot from Bloomberg regarding analysts’ views on Elisa based on current data. On the left, we can see that current recommendations lean toward the positive side, and on the right, the historical development of the recommendation distribution. In Bloomberg’s system, “Add” recommendations are categorized here as “Buy” and “Reduce” as “Sell”. “Hold” is “Hold”. Based on this data, the recommendation distribution is currently exceptionally positive compared to its history. This shift is also visible in the target prices. In the bottom right, the spread between the share price and target prices is shown.

20 Likes

Helsingin Sanomat reports on Elisa’s legal proceedings in Estonia regarding the government’s decision to ban the use of Huawei in networks (no paywall). One might interpret the headline as if this had just happened, but the lawsuit in question was filed in late 2022. According to HS, a decision may still be years away, as a preliminary ruling on the case is now being sought from the Court of Justice of the European Union.

In Estonia, Elisa uses Huawei equipment and software in its 4G network and Nokia in its 5G network, meaning Huawei must be replaced in the 4G network. According to the article, Elisa’s network in Finland consists mainly of Nokia and Ericsson, while Huawei’s share is just under 15%.

A few key takeaways from the content:

“In the lawsuit we filed in the Tallinn Administrative Court in December 2022, we are not questioning the regulation itself, but rather who should be responsible for the costs. Many other states compensate for costs if telecommunications operators are required by law to replace equipment and software."

“At this stage, we are unable to estimate how much replacing Huawei equipment will cost. The final costs depend on many factors, such as what kind of changes we have to make to individual base stations.”

The dispute is very likely about at least tens of millions of euros. The costs will be spread over several years, as the deadline for replacing Huawei products expires in just over five years.

13 Likes

I’m currently looking into Elisa as a potential cornerstone for my portfolio. Everything was going fine until I started thinking about the company’s actual competitive advantages. Are there even any? ![]() The brand could probably be counted as one, given that the company is Finnish, but otherwise, I couldn’t figure out what the company does significantly better than its competitors, even though the numbers (e.g., ROE/ROIC) would suggest so

The brand could probably be counted as one, given that the company is Finnish, but otherwise, I couldn’t figure out what the company does significantly better than its competitors, even though the numbers (e.g., ROE/ROIC) would suggest so ![]() I certainly don’t underestimate the brand, but it would be nice to hear others’ thoughts on Elisa’s competitive advantages and their sustainability.

I certainly don’t underestimate the brand, but it would be nice to hear others’ thoughts on Elisa’s competitive advantages and their sustainability.

At least they have customer service. Emphasis on the word service. I have no experience with DNA, but when I’ve been forced to make comparisons between Telia and Elisa at different times, the difference is absolutely massive. In a company where the share of consumer sales is large, I would give weight to things like that.

5 Likes

I added Elisa as a cornerstone for my equity savings account specifically because it’s a domestic company and because I’ve been a satisfied customer on their network for 26 years, dating back to the Radiolinja days. Visiting their brick-and-mortar stores has also been pleasant and smooth. Elisa is one of those stocks that has been a joy to own.

Domestically, Elisa is the leader in telecommunications services, and as the only publicly listed operator since DNA was delisted, this was an easy pick for my portfolio. Elisa also seems like it will continue to be a solid cornerstone due to its dividend, as the share price doesn’t fluctuate wildly enough to cause any major concern. I’ll keep adding to my position and remain a satisfied customer, occasionally lowering my mobile plan’s monthly fee through win-back offers, of course.

6 Likes

When discussing the mobile business and its customer service, one thing that distinguishes Elisa from Telia and DNA is the Shared Network (Yhteisverkko) used by the latter two.

These two operators have a jointly owned company whose base stations Telia and DNA use in Eastern and Northern Finland. At its best, the shared network achieves cost savings, as it is sufficient for these companies to build/maintain one base station in a given area instead of two.

In the Shared Network area, all base stations have been upgraded (or are at least being upgraded) with Nokia’s technology. This project hasn’t gone entirely smoothly, but as I understand it, it is constantly moving in a better direction.

The way this shared network manifests in customer service is that when a consumer makes a complaint about network issues, they first contact Telia/DNA/Moi customer service. From there, a ticket might be forwarded to the technical support of the Shared Network (Yhteisverkko), which slows down processing times and creates a “broken telephone” effect.

1 Like

Clear price increases became apparent when updating the plan. The change fee has also risen; it seems to be around ten euros now, whereas before it was maybe 5 €. Operators seem to have pricing power.

2 Likes

Pricing power is massive, especially in voice calls. Prices for business subscriptions could be raised significantly before companies would give up their phone numbers. The same applies to consumer customers.

If expensive volume-based pricing were introduced for mobile data, people would probably keep their phones on Wi-Fi at least at home. Few would want to be completely without mobile data.

Entering the industry as a completely new operator is also challenging, at least if the plan is to build a nationwide network.

1 Like

The mindset that a customer remains a customer until they want to give up the service entirely only works if you are Caruna or some company in a monopoly position providing a basic utility. Operators do not have this pricing power; otherwise, they would raise prices. They are all limited companies whose purpose is to generate profit for their shareholders.

Raising current prices is not sensible because customers will switch to a competitor. No operator in Finland is in a monopoly position, if a few very small marginal areas in remote regions are not taken into account. And if all operators raise prices significantly at the same time, it starts to smell like a cartel. However, there are 4-5 operators in Finland, depending on whether you want to count Moi as an operator, given that DNA owns it entirely.

Winning market share on the mobile side is difficult due to extreme competition; consequently, it would eat into margins and force additional investment in the network, so it’s not even beneficial. It’s better to just defend the current market share and let the money flow into the company. Meanwhile, growth (and future cash flows, hopefully) happens on the software and cybersecurity side.

1 Like