We also received a small M&A announcement from another Swedish peer today. This time it was Lifco, which announced the acquisition of Swedish Sendoline. Sendoline is a niche manufacturer specializing in dental care products and has also generated sales of around 4 MEUR in recent years. According to the Orbis database, the last couple of years have been somewhat lean from a profitability perspective, but in 2015 and 2016 the company made a very robust 14% net profit margin.

Lifco itself is a company operating on a very similar basic template as Lagercrantz (i.e., an industrial owner for leading players in niche areas). According to its own words, Lifco aims to be a safe haven for small and medium-sized companies. Acquisitions are therefore the alpha and omega of its operating model. These have been carried out quite vigorously, as 11 arrangements have been implemented in the past year alone. In total, Lifco’s portfolio includes over 160 companies.

Lifco directs its operations through three business areas: Dental (as its name suggests, manufacturers and distributors specializing in dental care), Demolition & Tools (operators specializing in servicing heavy equipment such as cranes and excavators), and Systems Solutions (operators offering various industrial solutions, such as contract manufacturers). Lifco’s and Yleiselektroniikka’s businesses therefore have certain commonalities (e.g., presence in the construction industry’s value chain). However, the geographical footprints of the companies are still quite different (Lifco’s companies operate at most indirectly in Finland, while Finland is the main market area for the Yleiselektroniikka Group), and among the companies under Lifco, there are no players fighting on exactly the same fronts as Yleiselektroniikka’s counterparts. Of course, competition can be waged, at least to some extent, at the level of potential acquisition targets, despite the structural and focal differences of the groups.

In a nutshell, Lifco’s acquisition strategy is touchingly simple. Lifco aims to be a long-term owner for companies operating at good profitability levels, carrying low technological risk, and being in healthy value chain positions. The company also gives acquired companies the freedom of independent decision-making and emphasizes the importance of an entrepreneurial culture. Thus, Lifco’s model also does not aim to create value through seemingly attractive operational synergies on paper. A concrete example of this is that Lifco has not changed the location of any of the companies it has acquired in its history.

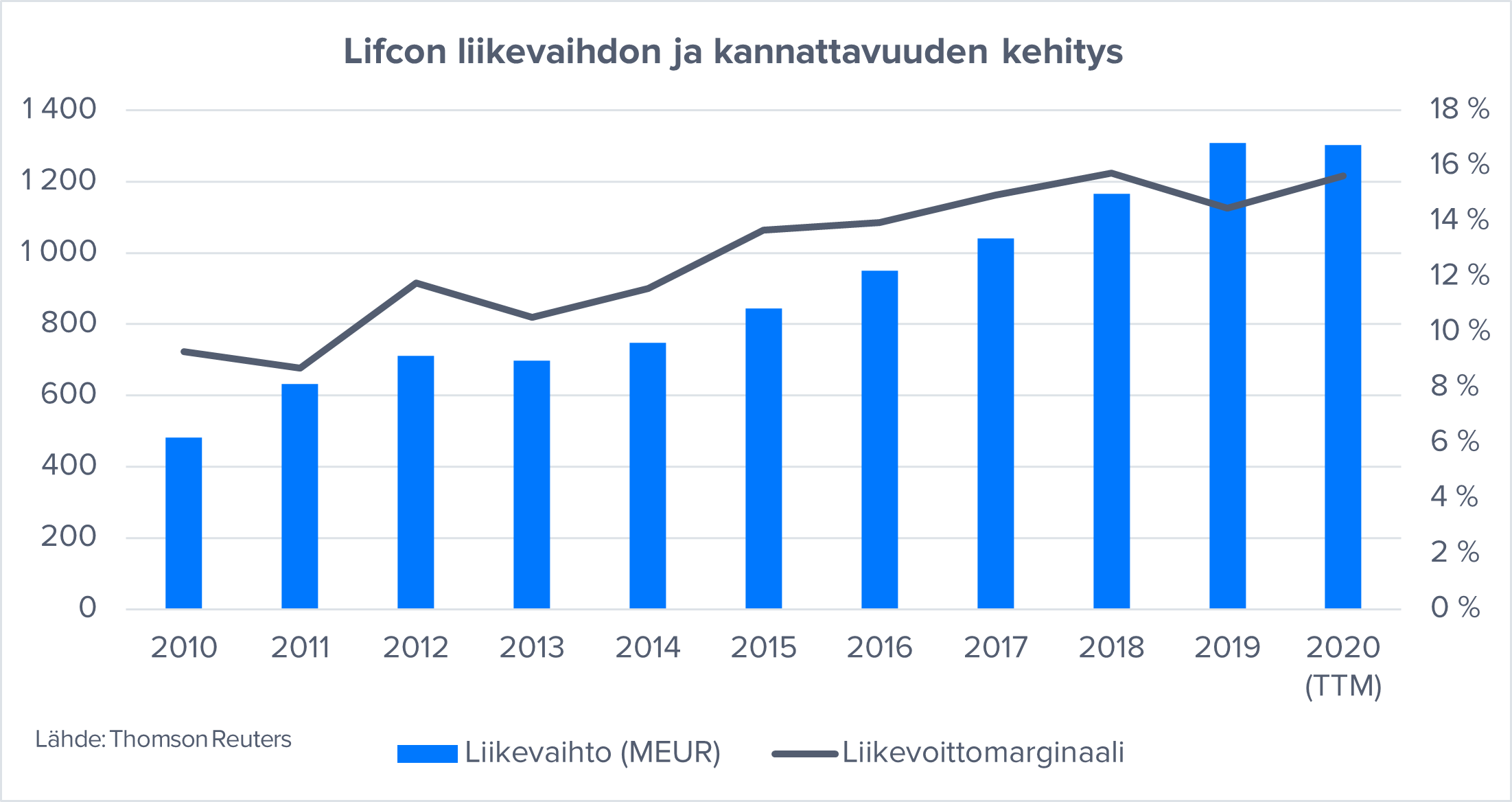

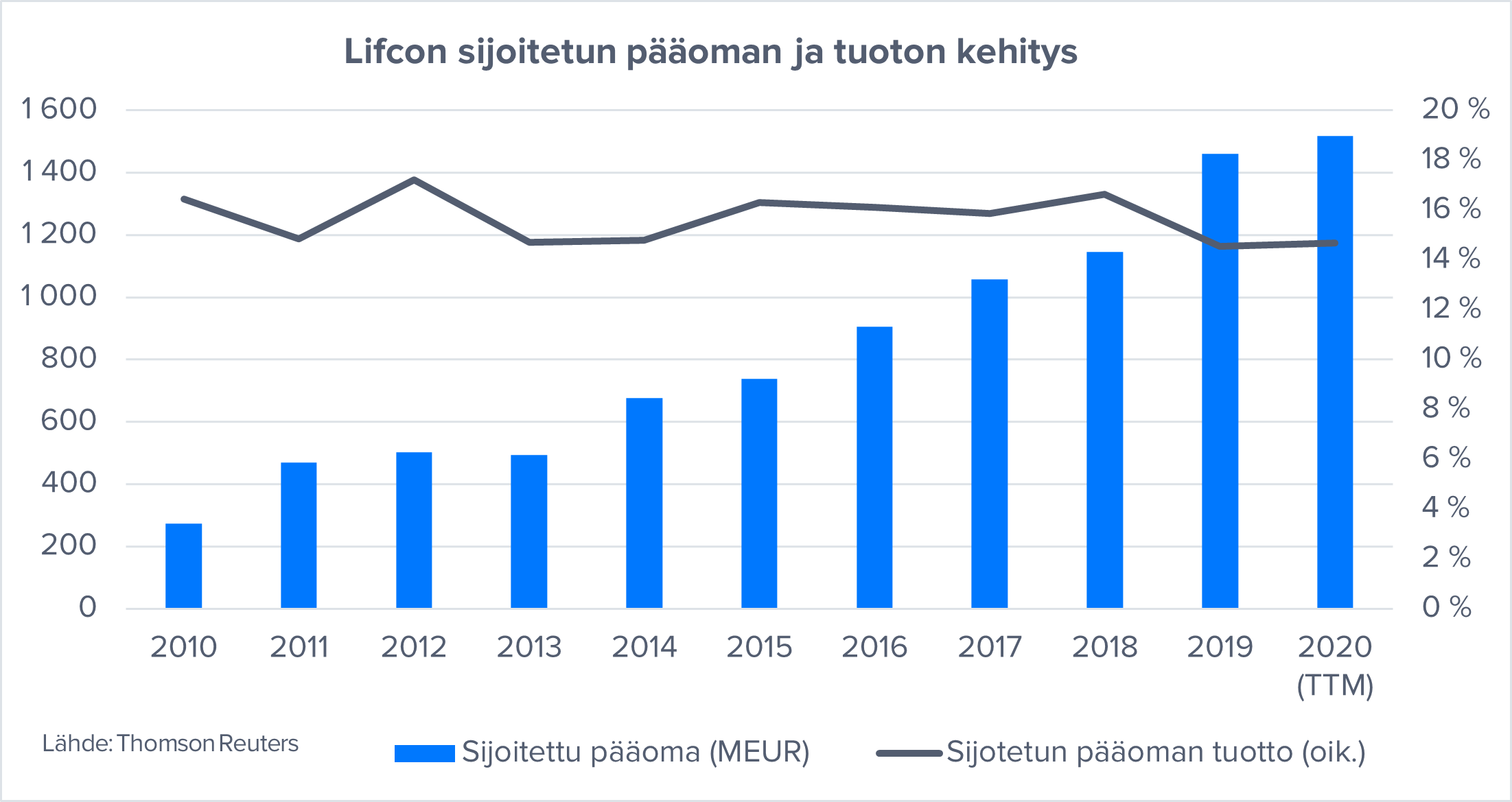

Lifco’s primary financial project is to achieve sustainable earnings growth. In the company’s terminology, this means that operational earnings growth organically exceeds the target market’s GDP growth. This is then supplemented by corporate arrangements. In terms of its balance sheet, the company aims to keep net debt/EBITDA in the 2-3x range. This is in the same ballpark as the comfort zone we estimate for Yleiselektroniikka. In 2010-2020 (TTM), Lifco’s performance has been strong, evidenced by an annual growth of 10% in sales and 16% in operating profit. The financial targets have therefore been met more than handsomely in this light.