Walmart on yhdysvaltalainen monikansallinen vähittäiskauppayritys, joka toimii hypermarkettien, halppistavaratalojen ja ruokakauppojen ketjuna Yhdysvalloissa sekä 23 muussa maassa (yllättävän vähän mielestäni!). Yhtiön pääkonttori sijaitsee Arkansasissa ja yhtiön perustivat veljekset Sam ja James “Bud” Walton vuonna 1962 Rogersissa, Arkansasissa. Vuonna 1969 yhtiö rekisteröitiin Delaware General Corporation Law’n alaiseksi.

Lokakuussa 2022 Walmartilla oli 10 586 myymälää 24 eri maassa, ja se toimi 46 eri nimellä. Yhdysvalloissa ja Kanadassa se tunnetaan nimellä Walmart, Meksikossa ja Keski-Amerikassa Walmart de México y Centroamérica jne. Walmart on maailman suurin yritys liikevaihdolla mitattuna ja myös maailman suurin yksityinen työnantaja, jolla on 2,1 miljoonaa työntekijää. Vuonna 2023 yhtiön liikevaihto oli 611,3 miljardia dollaria.

Walmart on perheomisteinen yritys, jota hallitsee Waltonin perhe, joka omistaa yli 50 prosenttia yhtiöstä. Yhtiö on ollut erittäin menestyksekäs Yhdysvalloissa, mutta sen kansainvälistyminen on onnistunut varsin vaihtelevasti.

Sijoittajan näkökulmaa:

Walmartille avautuu jatkossakin lukuisia mahdollisuuksia, mutta myös merkittäviä haasteita. Yritys voi hyödyntää globaalin laajentumisen tarjoamia kasvumahdollisuuksia ja vahvistaa asemaansa verkkokaupassa. Myös diversifointi uusiin liiketoiminta-alueisiin, kuten terveyspalveluihin, sekä uusien teknologioiden hyödyntäminen voivat myös tuoda merkittäviä etuja, lisäksi Yhtiö pystyy suuren kokonsa avulla neuvottelemaan kilpailukykyiset ostohinnat, minkä ansiosta se pystyy tarjoamaan asiakkailleen halpoja tuotteitta samalla saaden tyydyttävän katteen. Tämän vuoksi kilpailijoiden on vaikea haastaa Walmartia - ainakaan tässä suhteessa.

Samalla Walmart joutuu kuitenkin kohtaamaan tietysti kovan kilpailun, talouden heilahtelut ja entistä nopeammin muuttuvat kuluttajatottumukset, lisäksi pohdituttaa miten yhtiö pysyy mukana AI:n säästeämässä verkkokaupassa… no… mutta toistaiseksi yhtiö on saanut siitä lisää tukea kasvulleen. Walmartin on jatkuvasti seurattava markkinakehitystä ja mukauduttava muuttuviin olosuhteisiin säilyttääkseen kilpailuedun. Kansainvälistyminen on yksi suurimmista kysymyksistä ja se on mennyt yhtiöltä vähän vaihtelevasti. ![]()

Ensi viikon torstaina yhtiö kertoo Q2-tuloksestaan. ![]()

11.8.2024:

P/E-luku: 29,06

Osinkotuotto: 1,22 %

Markkina-arvo: 546,56 mrd. USD

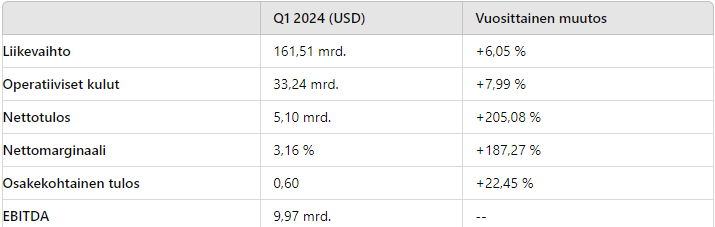

Eka kvartaali 2024:

Osakkeen historiaa: