I was thinking of starting a general thread about foreign SaaS companies, alongside the “FAANG” and “Semiconductor Giants” threads. Domestic companies seem to already have their own company-specific threads.

I don’t currently own any SaaS companies myself, but I’ve been following several for a long time. I’m mostly an index investor who buys a few stocks a couple of times a year when an interesting opportunity/idea comes along.

Inderes and Mikael have talked about how IT service-focused companies build digital infrastructure. I believe that SaaS companies are this to a very large extent. Less and less do companies want to use their own development resources for components that can be bought from external companies that develop them scalably.

The problem, of course, is that there seem to be enough SaaS believers among investors, and valuations are sky-high.

The best SaaS companies are, of course, excellent high-margin businesses with “negative churn,” meaning existing customers pay more year after year, for example, because the number of employees grows, requiring more licenses all the time.

In addition, the best SaaS companies also embed themselves deeply into companies’ operations, making them very difficult to get rid of.

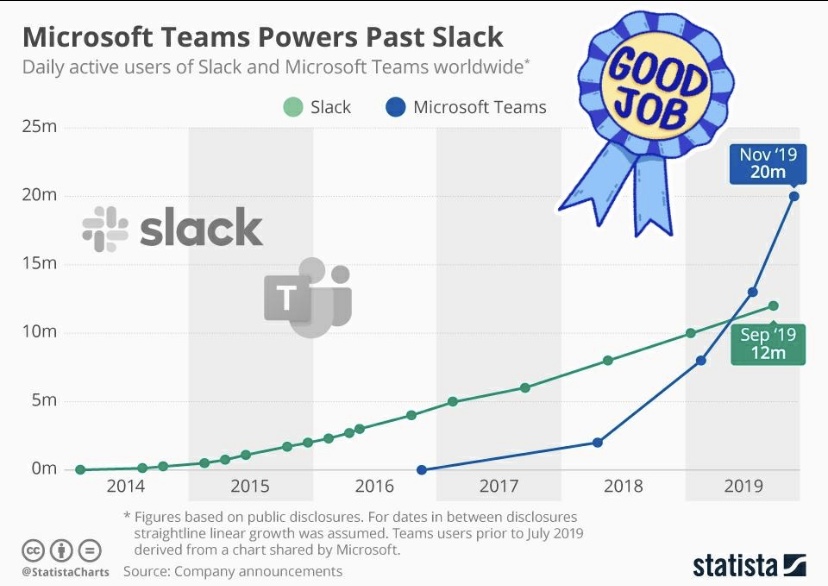

As an example, one can think of Salesforce or other CRM businesses that bill companies based on how many people use their tool and that tightly integrate themselves into various sales processes. One can also consider how easy it is to give up a Microsoft Office365 subscription once the entire organization’s emails, documents, calendars, etc., are built within Office365. Of course, both face the challenge of acquiring new customers in the long run, but there are a huge number of existing, self-growing customers to whom new features can also be continuously sold “as part of a bundle.”

A couple of questions about investing in these:

- Has anyone found an affordable ETF focused on SaaS companies? I would be interested in investing in one if there were a bigger dip in the market.

- Have you invested in foreign SaaS companies? What are your favorites?