I am opening a new discussion thread for the UB Nordic Property (UB Pohjoismaiset Liikekiinteistöt) fund. During the past week, we launched a fund page for the fund, which will henceforth bring together quarterly reviews and other fund-related content, including regular inderesTV interviews, the first of which was filmed a few days ago. At this point, it is worth noting that UB Asset Management (UB Rahastoyhtiö) is a client of Inderes.

In the future, the intention is to also collect questions and ideas for the interviews from here. I have also encouraged UB’s portfolio managers to join the Forum to participate in the discussion. For my part, there is nothing stopping us from also discussing questions related to the Nordic real estate market at a general level in this thread.

Salkunhoitajat kävivät haastattelussa. Sopivaa kuunneltavaa varmasti myös kiinteistösektorista yleisesti kiinnostuneille.

Aiheet kellotettuna

00:00 Aloitus

00:25 Ruotsin asuntomarkkinoiden tyrsky

02:40 Ulkomaiset sijoittajat pitävät kiinni Pohjoismaista

04:20 Pohjoismaissa kiinteistöltä vaaditaan enemmän tuottoa

06:00 Kiinteistökohteiden uudelleenhinnoittelu

08:58 Uutta tietoa saadaan alati lisää

10:27 Inflaation merkitys

13:48 Uusi sijoitus Oslossa

16:53 Käteinen on kuningas

UB’s portfolio management has released its January–March quarterly review. It is interesting reading for anyone generally interested in the real estate market as well. Significantly fewer transactions are being made than before, but the market is not completely frozen.

Many real estate investors seem to be using the time freed up from trading to improve and optimize their current real estate holdings. - - Consequently, many properties will be in even better condition when the market turns.

Inflation has shown the first signs of easing, which could mean an end to interest rate hikes in the near future. - - The end of rate hikes and, eventually, a decrease in interest rates will bring activity back to the real estate market.

Many investors still seem to have plenty of cash to deploy as soon as the economic outlook clears up a bit. A good example is Blackstone, which announced in April that it had raised a record $30 billion for its new real estate fund. Large investors thus seem to have faith in the recovery of the real estate market in the near future.

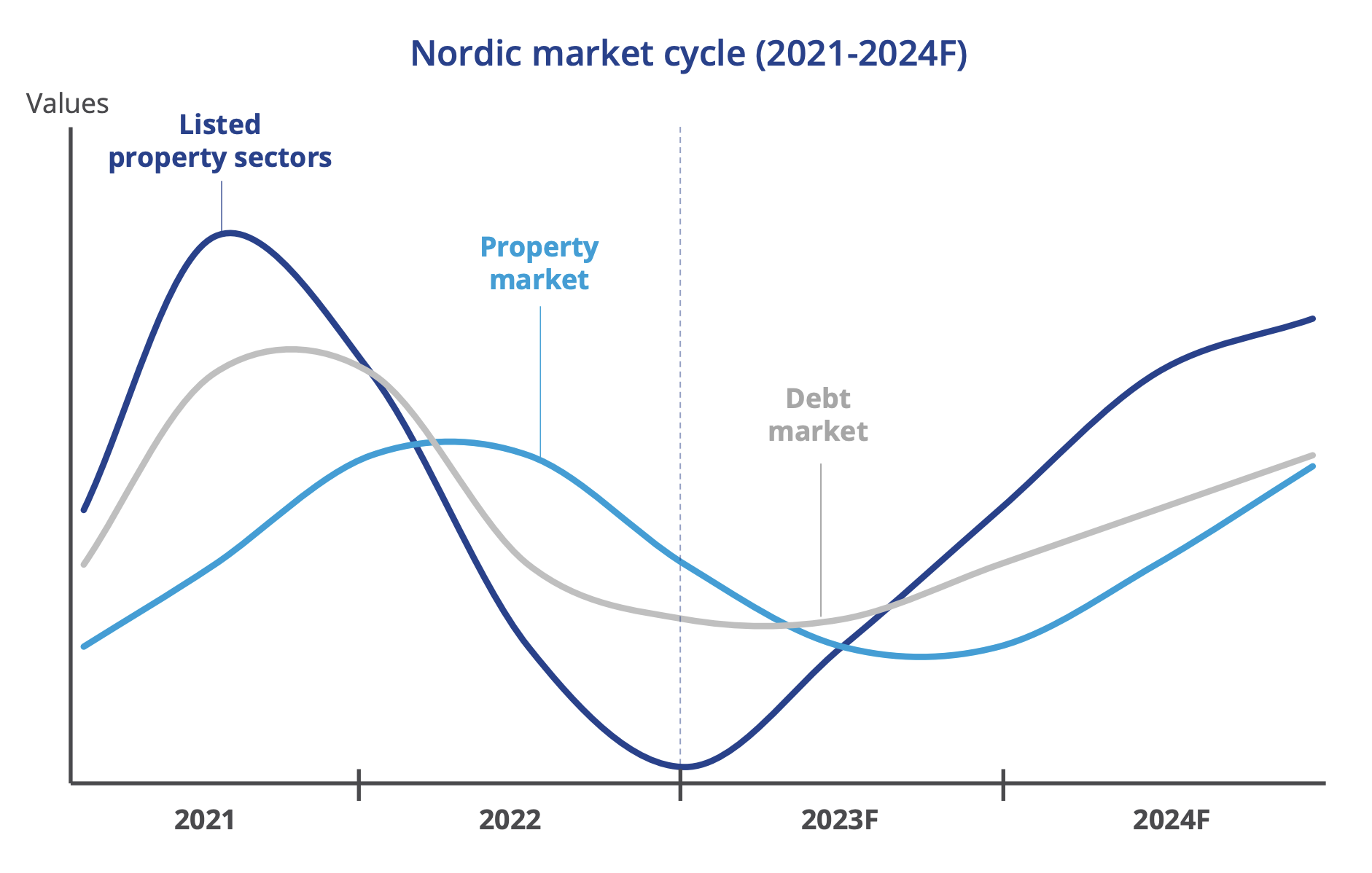

Here is the latest interview with the portfolio managers. We started by discussing the market situation and then, among other things, why the listed and unlisted real estate markets seem to be living completely different lives.

UB’s portfolio managers will be interviewed on inderesTV in the coming days. Here are some initial insights from them regarding the situation and market outlook for the real estate sector.

The first signs of a recovery in the real estate investment market have already been seen in the listed real estate market, which appears to have reached its bottom in October 2023. Historically, direct real estate investments have followed the listed real estate market with a lag of approximately 6–12 months.

Here is the promised interview. It is definitely worth a listen for everyone interested in the situation of property managers and the real estate sector in general.

Timestamps:

00:00 Introduction

00:16 The year 2023

01:30 “Secondary offices suffer the most”

02:24 Turnaround in the listed market

03:23 Interest rates as the catalyst for the turnaround

05:38 Yield requirements and value declines

08:57 Market stress and redemptions

10:55 Yield gap and real interest rates

12:25 Differences in fund returns

14:12 The mechanics of return calculation

20:03 The significance of Norway

22:11 How has the “new normal” changed real estate investing?

Here is a fresh review from UB’s Jaakko Onali and Mikko Hentinen.

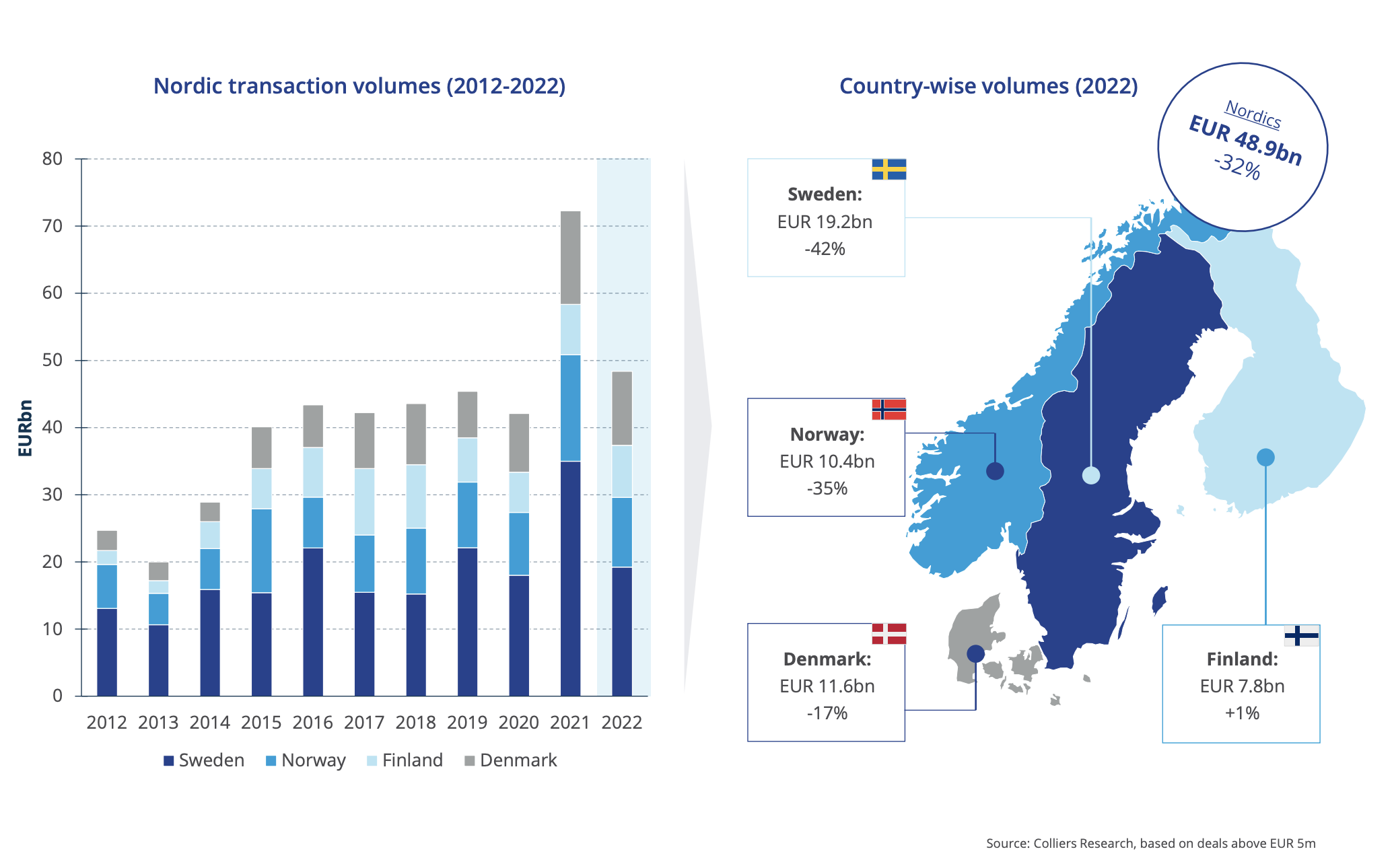

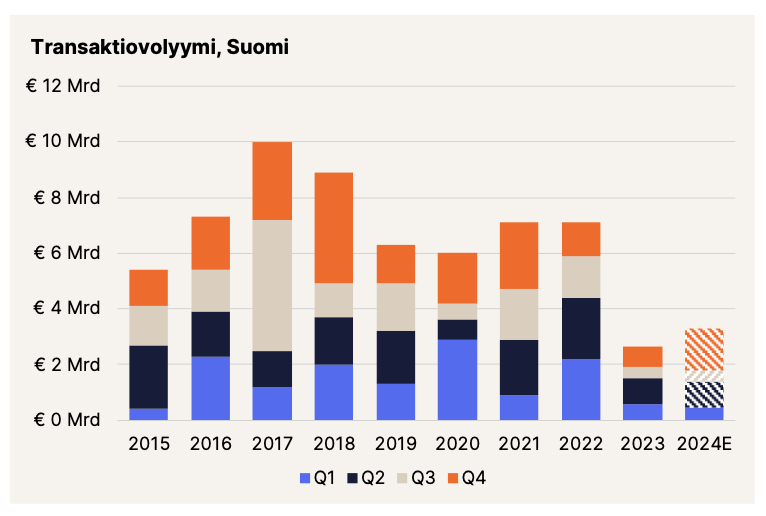

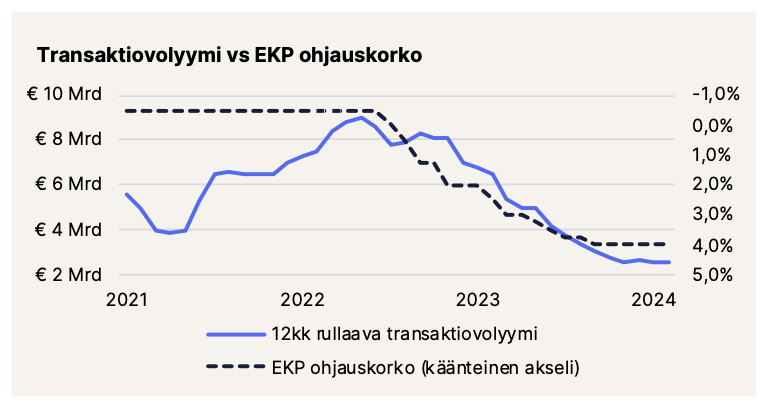

In the previous quarterly report, we wrote that the real estate market’s transaction volume seems to have stabilized at 4–5 billion euros per quarter in the Nordics. Many surely hoped that the real estate market would see a “Santa Claus rally” toward the end of the year, and although there was a small final spurt, the 2023 transaction volume in the Nordics remained just under 20 billion euros as predicted. It was the quietest year since the financial crisis.

Newsec’s Spring 2024 Finnish property market report was published earlier this week. It can be downloaded täältä. Downloading requires providing contact information. If you do not wish to do so, I can send it via email if necessary.

Although the report focuses on Finland, the drivers are practically the same regardless of the country: inflation, interest rates/monetary policy, a sluggish economic situation, and general uncertainty. What did I forget to list?

The real estate market is expected to normalize and turbulence to decrease towards the end of the year, as long as inflation falls and interest rates follow: “The biggest risk in the current scenario is that inflation refuses to drop the ‘last mile’. This may be due to new supply disruptions caused by geopolitical disturbances. Inflation may also refuse to fall because economic growth is stronger than expected and wage increases are larger than anticipated.”

According to Newsec, there are more potential buyers in the market than before. However, the willingness to buy does not guarantee an increase in transaction activity. Everyone is waiting for interest rates to drop.

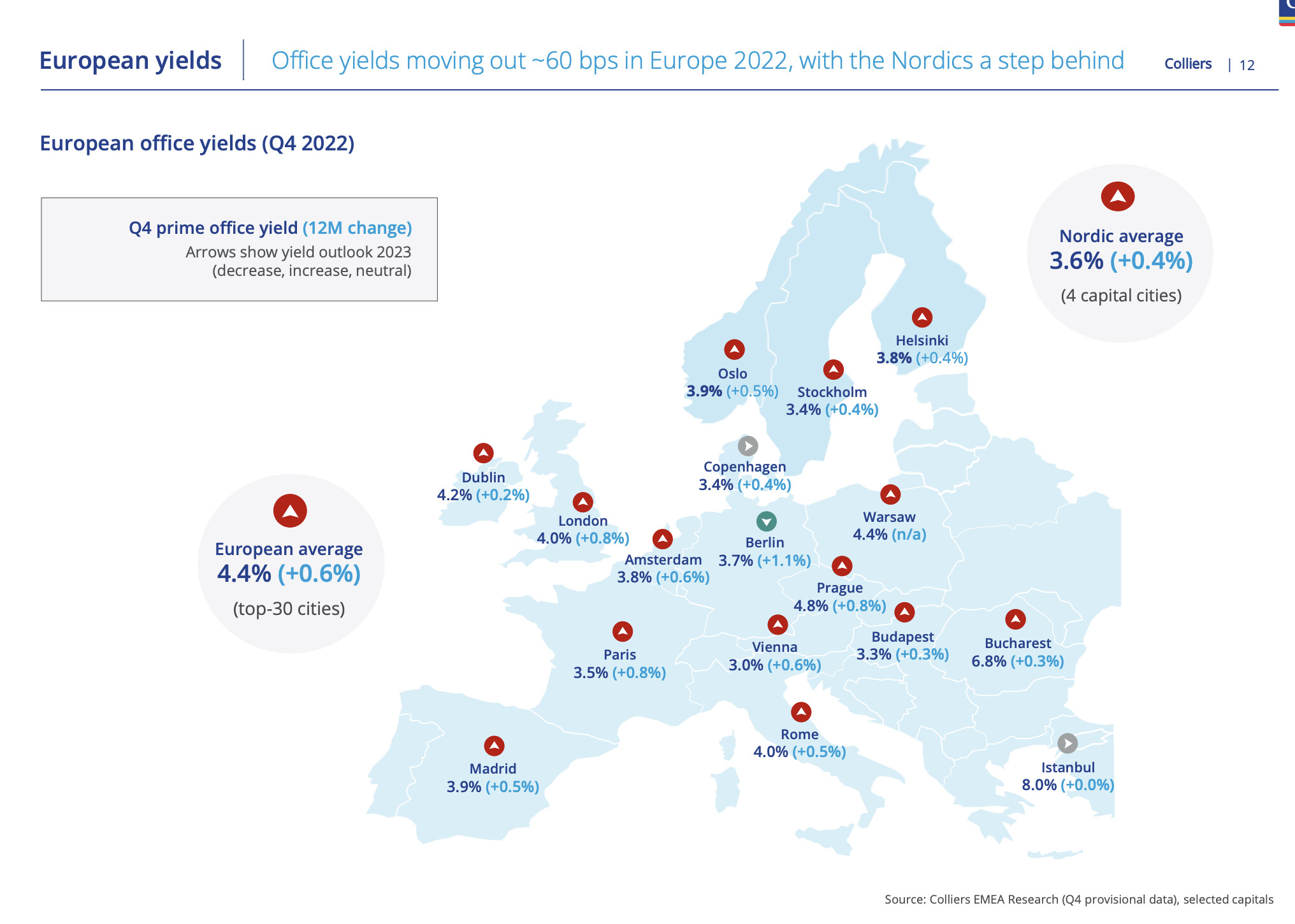

On the other hand: “Although prime yield requirements have risen by 70–170 basis points during the current cycle, the rise is still smaller than the 320 basis point rise in the Finnish government bond yield” – “due to uncertainties in the real estate market, it is unclear whether the current narrowed risk premium is sufficient to revitalize the market.”

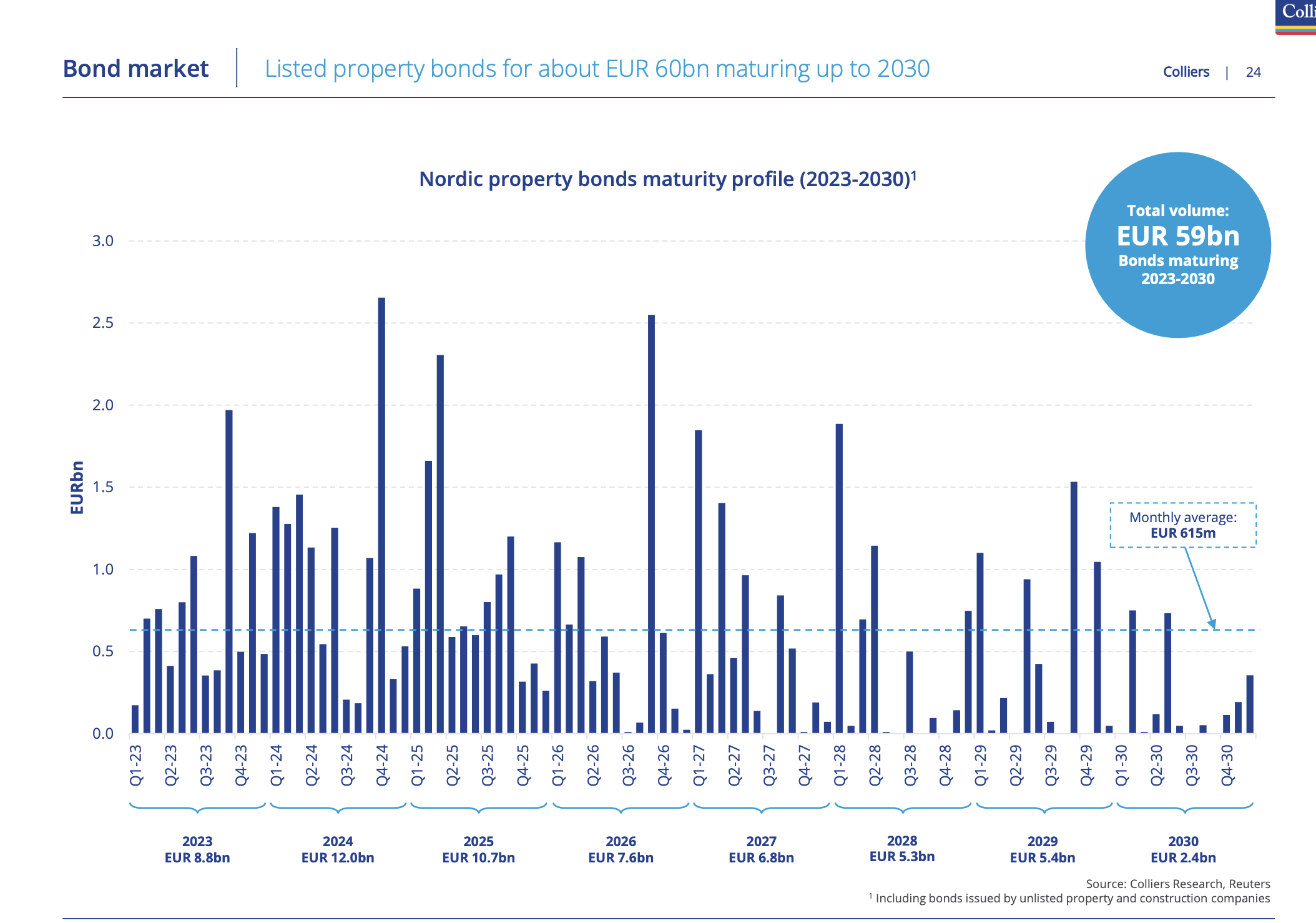

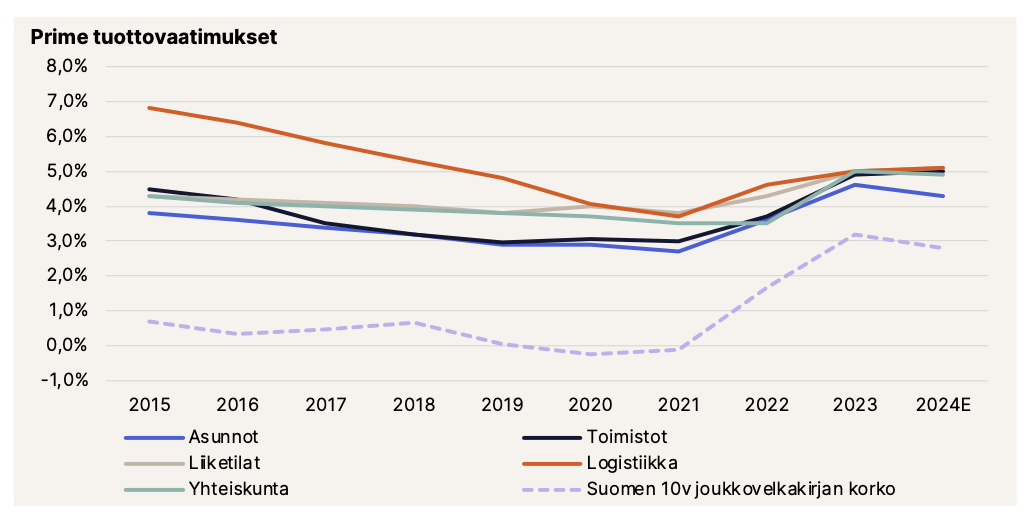

A few useful graphs picked from the report. The report has separate sections for each property class (residential, offices, industrial and logistics, retail, social infrastructure, hotels).

Here is an interesting piece by UB’s Jaakko Onali and Mikko Hentinen.

In the Q4/2023 quarterly report published at the beginning of the year, we wrote that property values would likely find a new equilibrium during the current year. Looking at the changes in our property values in the first quarter of the year, we notice that the largest decreases in value appear to be behind us for now. Property appraisers will hopefully gain more evidence of property values from transactions during the current year, so smaller adjustments to property values will certainly still be made based on realized transactions.

UB portfolio managers Jaakko Onali and Mikko Hentinen were interviewed by @Antti_Jarvenpaa.

Topics:

00:00 Introduction

00:22 Market situation

05:50 It’s not all about interest rates

11:25 Problems are concentrated in offices

15:19 Capital allocation focuses on reallocation

19:52 Property development is more emphasized than before

23:37 Value changes remain moderate

27:27 Outlook for the rest of the year

Below is a fund review from UB portfolio managers Jaakko Onali and Mikko Hentinen.

In the fund’s previous quarterly reviews and materials, we have shown a chart from international consulting firms suggesting that a turnaround in the direct real estate market would occur during the current summer. The first interest rate cut by the European Central Bank (ECB) in June is likely to facilitate the valuation of real estate and thus the forecasting of returns. Going forward, the impact of rate cuts on real estate values may already be cautiously positive. Due to slow transaction processes, effects in the real estate market manifest slowly, so we will likely have more clarity in this regard only in the autumn.

UB’s portfolio manager Jaakko Onali was interviewed by Antti.

Topics:

00:00 Intro

01:34 Transaction activity picking up

02:36 Sweden leads the way, Finland follows

03:25 Market drivers and most popular asset classes

06:35 Office market challenges centered in Finland

08:18 “Best buying opportunities of the decade”

14:05 Is sustainability greenwashing?

17:12 Real estate development

19:02 Strategically important real estate locations

21:42 Room for improvement in occupancy rates

23:45 Redemptions and net subscriptions

Antti’s guest was UB’s portfolio manager Jaakko Onali.

The decisions of several housing and real estate funds to suspend redemptions of fund units have generated a lot of discussion in the market early this year. What has led to this situation? UB’s portfolio manager Jaakko Onali explains the situation of real estate funds and the market.

Topics:

00:00 Introduction

00:40 “Liquidity is really weak”

04:40 Problems are concentrated in Finland

05:37 Housing market

06:45 Why don’t unit holders get their money?

09:46 Are open-ended real estate funds truly “liquid”?

11:53 Who defines the interests of unit holders?

12:35 Could redemptions be financed with debt?

14:39 What kind of cash allocations are typical for real estate funds?

16:03 Why aren’t properties forced to be sold, and what would be the consequences?

19:27 Real estate valuation and the principal-agent problem (conflict of interest)

22:30 How to monitor and evaluate the real estate market and funds?

24:03 Situation of the UB Nordic Commercial Properties fund

26:08 Market situation in the Nordics by country

28:30 Why has the cooling of the construction market not supported the existing property stock?

30:35 Long-term interest rates, inflation, and real interest rate

32:40 Expectations for 2025