United Bankers (UB) is a medium-sized Finnish company offering investment products and services, whose business areas include asset management and capital market services. In asset management, the company specializes in real asset investment solutions. The company is one of the most active players on the buy-side of the consolidating asset management market, and inorganic growth has played a significant role in the company’s recent history. The company should not be confused with United Brotherhood (UB), which is an illegal biker gang.

Facts on the table: This is one of the stock market’s least sexy stocks. The company is stable and well-diversified in terms of revenue, but an average wealth management firm. The share price has more or less crawled sideways for five years. The company makes 1-2 acquisitions per year and distributes a 5-6% dividend. The stock is difficult to buy and sell due to very poor liquidity. The company’s name is a complete farce, as it simultaneously manages to be incredibly boring and bring to mind a biker gang. Almost no investor owns the company, and no one wants to talk about it.

However, the company is facing a special situation that may offer short-term return potential. The company is indeed moving to the main list of the stock exchange soon. The transition of debt-free, good dividend-paying companies to the main list has generally boosted share prices, especially when the company was previously unknown to investors. It’s hard to find a company more unknown than UB.

Although the move to the main list and the approximate timeline should be known to the market, it is still usually generously rewarded. For example, with the king stock of the bull market, verkkokauppacom, it was, in my opinion, completely clear that the share price would rise with the move to the main list, and this indeed happened. Dividend stocks are currently very popular in the stock market, especially if their product or service is easily understandable.

For small companies, visibility is everything, because you cannot invest in a company whose existence you do not know about. A mere news article in Kauppalehti (Finnish financial newspaper) usually prompts investors to examine the company’s key figures and share price history. UB’s sell-side has typically been bought out for about 20,000 euros, so even a small number of investors can significantly push up the share price. This kind of sudden price increase from positive news, in my opinion, creates a reasonably good short-term return expectation for small investors.

Of course, there are risks in holding the stock while waiting for the move to the main list. Wealth management firms are more cyclical than typical stock market shares, and the company’s stock is so illiquid that it may not be possible to get rid of it at the desired price. The stock is also so boring that it may not interest anyone, and in that case, the sideways crawl will continue forever. What do the gurus at Inderes think? Hit or miss?

14 Likes

Thanks for the opening, Eka.

How do you see this as part of the industry consolidation that I see happening within the next 0-5 years? Who would fit into this picture? @Sauli_Vilen, if I remember correctly, speculated last year, half-jokingly (?), about who would be a good match for whom. Do you have any insights?

2 Likes

I don’t have the real competence to evaluate that, but public interviews and the previous track record suggest that the company is wearing its buying pants and we will continue to see corporate arrangements made by the company in both Finland and Sweden. From previous monitoring, I have gained the impression that management and staff are strongly committed to the company’s development and are not willing to sell themselves at the moment.

In the industry, the general trend seems to be increasing regulation, costs generated by IT systems, pressure created by cheap index funds against profitable active funds, and growing demand for alternative investment products due to low interest rates. In addition, the industry is highly scalable and capital-light, so corporate arrangements should materialize quickly on the revenue side. All these forces, in my opinion, work against small companies and speak for continued consolidation in the industry.

Could we perhaps get Mr. @Sauli_Vilen to tell us here if the company is suitable for a kissing booth?

3 Likes

{“content”:“I beg to differ a bit with Eka. In my opinion, these are the best stocks, especially for short-term trading, and this is how I lost my lunch money, but it’s been fun for the last five years. Thanks for the lunches, and now everyone can gang up on me.”,“target_locale”:“en”}

Old video, but it immediately came to mind when we started talking about the company. The main takeaway from this interview for me was that they have never (in about 34 years) had a loss-making financial statement since their founding. I consider this a respectable achievement for a company focused on wealth management and investing. That timeframe includes a couple of major crises. So, I tip my imaginary hat to these gentlemen and ladies. ![]()

7 Likes

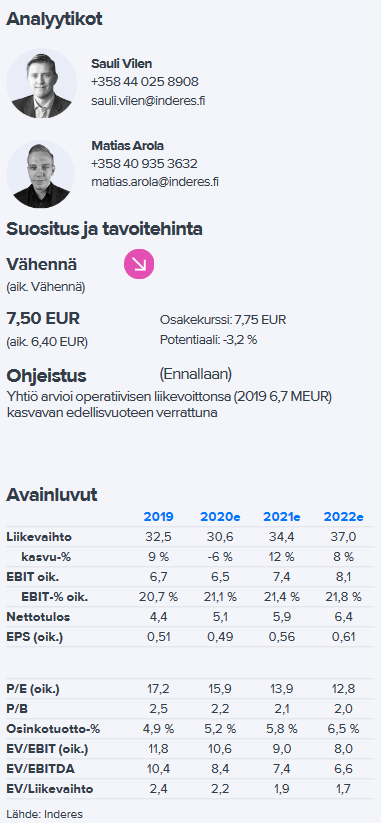

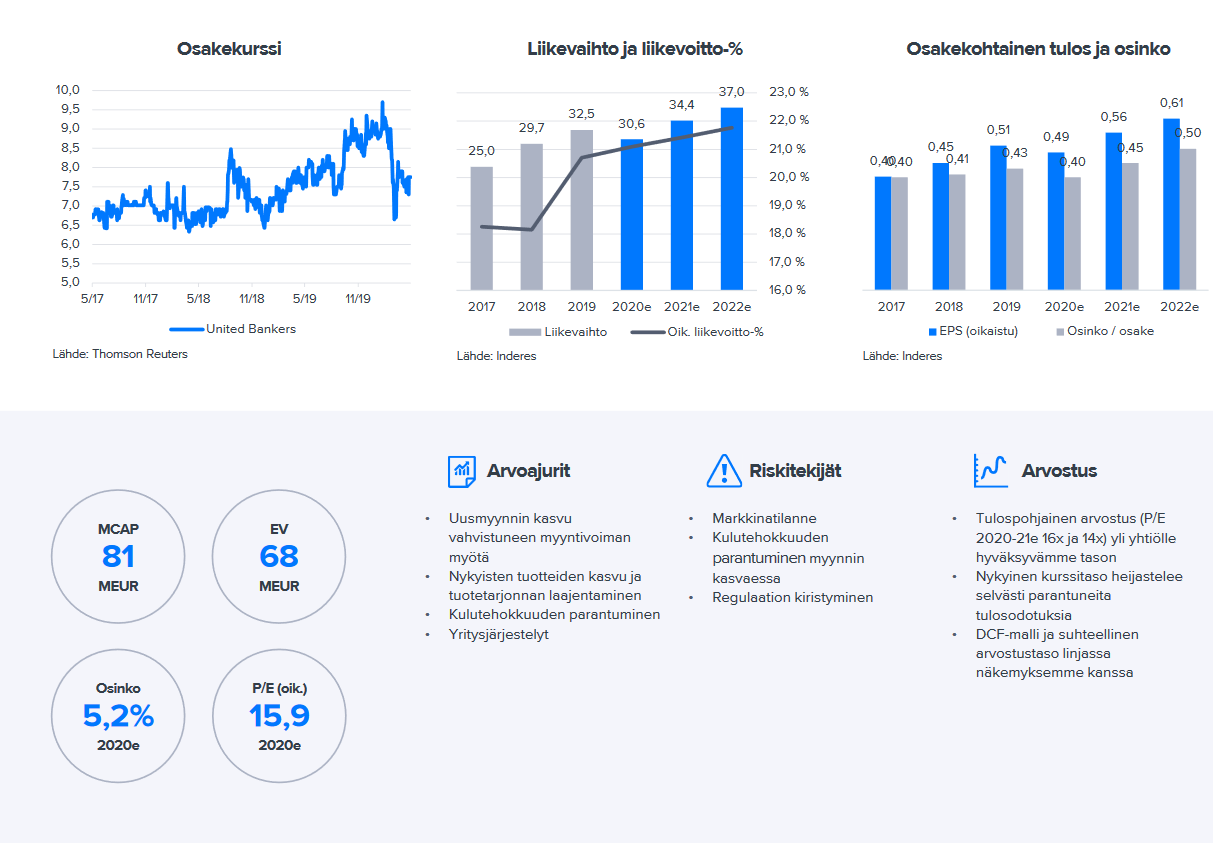

Thanks for starting this, I’ve begun familiarizing myself with the company. The first thing that caught my eye was Inderes’ update on May 14th, where, still partially amidst the COVID storm, the target price was raised from 6.5 → 7.5. What was notable, in my opinion, was the following:

"Forecasts Revised Significantly Upward

We had previously underestimated the impact of the company’s unlisted spearhead products on its fees, and these explain a large part of the forecast changes now seen. Additionally, market recovery, a more favorable cost structure than our expectations, and decreased performance fee forecasts are other factors behind the significant forecast changes. Overall, our current year’s operating profit forecast rose to 6.5 MEUR from the previous 4.1 MEUR. Operating profit forecasts for 2021 and 2022 have increased by 12% and 5% respectively. Dividend forecasts have also been significantly revised upward along with the earnings forecasts, as we expect the company to continue its generous dividend policy."

Those unlisted products might not care as much whether it was the COVID era or not, depending entirely on the industry, of course. Does anyone have more information about these unlisted spearhead products?

2 Likes

Date, Recommendation, Target, Price

07/02/2020 Reduce €9.00 €9.45

03/03/2020 Reduce €9.00 €8.90

23/03/2020 Reduce €6.40 €6.90

14/05/2020 Reduce €7.50 €7.75

It’s worth noting here that the market situation in H1 has changed so rapidly that target prices have become outdated in weeks. The company itself forecasts an increase in operating profit this year, but the report from 14/05/2020 predicts a decline for this year. In a neutral market situation and with the company’s guidance remaining unchanged, I believe it is clear that the target price and also the true value of the company are above the current price. However, it may be that we have to wait for the undervaluation to unwind until the company moves to the main list.

1 Like

Did the Inderes effect hit? +6% right away this morning. Too bad the position I opened yesterday is so small.

2 Likes

Exchange all 10 pcs ![]()

Of course, the buy/sell spread is quite wide… No sellers at yesterday’s price yet, at least.

5 Likes

After staring at the percentages for a moment, I also opened those trades. Bought at 7.4, no transactions. Its volume is unbelievably small. Getting listed on the main list could, with a little hype, significantly boost the share price. Now, even companies ripe for bankruptcy are rocketing, so why not a profitable company that pays good dividends like this one?

1 Like

Quite tough!

“The company’s first half-year result has been strong despite the difficult market situation. A significant positive impact on the result comes from the sale of the forest assets of the UB Forest Fund I Ky forest fund, announced today, June 5, 2020, to a company belonging to a European insurance group. United Bankers’ subsidiary UB Nordic Forest Management Oy has acted as the responsible partner of the fund. As a result of the transaction, United Bankers will record a performance fee of approximately 2.8 million euros for 2020.”

Didn’t dare to give a positive earnings surprise yet, but it might be coming!

“The company issued the following guidance in its financial statement release on March 2, 2020: ‘United Bankers estimates its operating profit to grow compared to the previous year.’ The company has decided to maintain its full-year guidance unchanged, as despite the favorable development in the early part of the year, the economic effects of the coronavirus pandemic still cause uncertainty in the investment markets. It is still very difficult to assess the effects of the market situation on the demand for wealth management and capital market services, and on the other hand, on the performance of funds.”

4 Likes

@Pohjolan_Eka did you interpret that bolded sentence the same way I did, that there could be some positive news coming if the situation doesn’t worsen from here?

1 Like

1 Like

UB has maintained a positive outlook throughout the coronavirus crisis, so the company has had strong faith in its own work even during darker times. I believe in the company’s forecast that this year will bring an improvement in results compared to last year, but the extent of the improvement is still uncertain. In my opinion, it is entirely correct to interpret the bolded sentence as describing that the company’s results will be excellent unless the markets collapse.

1 Like

EDIT: after writing, the company report was released

Target price raised to 8€ and forecasts look very good. Sauli interpreted the comment as a hidden positive, similar to @topsu for example.

I’m not resting on my laurels regarding returns yet, but I’m waiting for the move to the main list to raise the share price from the current level ![]()

2 Likes

I added a small batch to my portfolio last week, and I’m also planning to wait until it reaches the main list, just like @Pohjolan_Eka. If it dips, I’ll add more.

@Sauli_Vilen was also sharp; it’s good to dot the i’s and cross the t’s in these matters.

1 Like

I believe the plan was to move to the main list in 2020, but is there a more precise date known/estimated?

1 Like

Not to my knowledge, it hasn’t been announced anywhere. However, half the year is already gone, and recent performance has been very good, so I think it’s reasonable to expect the move “soon.” I have some shares of the company in my portfolio both as a hold investment (a reasonably good growing dividend case, especially since I got it at a favorable average price) and a larger position as a speculative investment (target price increase and move to the main list).

2 Likes