Tuo on omaan silmään se kaikkein suurin pettymys, inderesin ennakko oli 110-140. Sinällään nyt itse kvartaalin luvut ei niin paljoa jäänyt. Valopilkkuna kuitenkin asiakasmäärät, jotka kasvoi vertailukelpoisesti hyvin. Tärkeintä kuitenkin on, että ne asiakkaat saadaan edelleen sinne kauppoihin, keskiostos ja sitä myötä myyntikate varmasti paranee sitten ostovoiman kasvun myötä.

10 tykkäystä

Positiivista raportilla tosiaan oli vertailukelpoisten myymälöiden kehitys, joissa myynti sekä asiakasmäärät nousivat selvästi. Joulumyynnissä oltiin siis onnistuttu. Myös kiinteät kulut joustivat mukavasti liikevaihdon noustessa! Tässä näkyy miten vertailukelpoinen kasvu skaalautuu kannattavuudeksi, kun kasvu vanhoissa myymälöissä ei tarvitse merkittävästi lisäresursseja.

Myyntikate-% laski odotusten vastaisesti. Tästä ei kannatta vielä tehdä pitkälle vedettyjä johtopäätöksiä, sillä tuolla päivittäistavarankasvulla saattoi olla tässä vaikutuksensa. Odotin kuitenkin, että Dollarstoressa lisääntyneiden omien tuotemerkkien parempi kannattavuus olisi nostanut Dollarstoren myyntikatetta. Kysellään tämän perään tulospuhelussa.

Synergiatavoitteesta jäätiin parilla miljoonalla. Todennäköisesti prosessi on vain viivästynyt ja synergioita saataisiin vielä kaivettua.

Tulosohjeistus olisi voinut olla parempikin, mutta odotukset ovat haarukan sisällä. En tästä olisi äärihuolissaan. Printtasin kommenttiin kuitenkin, että konsensusennusteet saattavat päivän aikana laskea. Tai sanotaan näin, ettei niissä ainakaan nousuvaraa tälle vuodelle ole ![]()

20 tykkäystä

Niin, ei kai tässä kirvestä kannata kaivoon heittää, mutta veikkaan kuitenkin, että markkinoille pettymys. Toisaalta makroympäristö voi muuttua myös suotuisammaksi, monella alalla H2/2025 nähdään parempana. Ei positiivista tulosvaroitusta tietenkään kannata tässä vaiheessa vielä sulkea pois, mutta onhan tämä varmasti toimitusjohtajalle jonkinmoinen pettymys, kun ei strategiakauden tavoitteisiin eli tuohon 150 miljoonaan todennäköisesti päästä, toisaalta maailma ja itse yrityskin on paljon muuttunut siitä, kun tavoitteita asetettiin.

5 tykkäystä

Kyllä Tokmannin omien tuotemerkkien (käyttötavaratuotteiden) pitäisi tukea Dollarstoren myyntikatemarginaalia. Molemmissa segmenteissä päivittäistavaran kasvu on ollut käyttötavaraa vahvempaa viimeaikoina, joka on tuon laskeneen katteen taustalla. Raportissa mainittiin myös, että tarjoustuotteilla oli Dollarstoren katteita laskeva vaikutus.

8 tykkäystä

@Arhi_Kivilahti otti raportin vastaan analyytikkoja positiivisemmin ajatuksin:

18 tykkäystä

Eiköhän tuo kuluttajaluottamuskin kohene. EKP laski eilen jälleen korkoa. Korkojen lasku näkyy asuntolainoissa viiveellä, jotka Suomessa sidottu useimmissa tapauksissa euriboriin. Sieltä sitten jää lisää kulutukseen, joka piristää kauppaa.

4 tykkäystä

Eipä tuo tulos suurta ihmetystä aiheuttanut. Koska kurssi on noussut viime aikoina voimakkaasti ja perinteitä noudattaen Tokmannin kurssi reagoi tulokseen aina voimakkaasti,edes kurssireaktio ei järkytä. Juna kulkee kuitenkin oikeaan suuntaan, vaikka jotkut ovat ennustaneet kovempaa kulkuvauhtia.

Päivittäistavaroiden myyntiosuuden kasvu ja käyttötavaroiden osuuden lasku on tietenkin katteen kannalta huono suunta, mutta toisaalta lisää mielestäni Tokmannin defensiivisyyttä sekä parantaa kilpailuasetelmaa halpakaupan saralla. Se myös korostaa Spar-yhteistyön mielekkyyttä.

30 tykkäystä

Maksumuuri ofc.

1 tykkäys

Palstan sääntöjen mukaan olisi tietenkin tervetullutta siteerata linkitettyjen maksumuuriartikkelien sisältöä. Joku toinen referoikoot halutessaan tarkemmin, mutta lainaan nyt vain tämän lyhyen pätkän, josta nyt noin suunnilleen selviää mitä otsikon takana on:

“Merkittävimmiksi kuormitustekijöiksi tarkastuksella nousivat epärealistiset tai kohtuuttomat tavoitteet, liiallinen työmäärä työaikaan nähden, vaihtelun puute työssä, työn yksitoikkoisuus, ja työn tekemisen jatkuva keskeytyminen,”

24 tykkäystä

Tämä ei liene yksin Tokmannin tai edes kaupan alan ongelma. Tuota olen kokenut itse monen vuoden ajan ns. “asiantuntijatyössä”. Siihen voi itse vaikuttaa vaikka vaihtamalla työpaikkaa.

13 tykkäystä

Osakkeen arvostus on edelleen maltillinen

Näemme osakkeen arvostuskuvan edelleen houkuttelevana. Yhtiötä hinnoitellaan varsin maltillisin tuloskertoimin (2025e P/E 12x ja IFRS 16 oik. EV/EBIT ~12x), joissa näemme lievää nousuvaraa. Etenkin P/E-kerroin sijaitsee reippaasti verrokkiryhmän mediaanin alapuolella, joka niin ikään puoltaa osakkeen nousuvaraa. Myös PEG-mittarin (2024 0,8x) perusteella ennustamaamme tuloskasvua ei ole täysimääräisesti huomioitu osakekurssissa. Tämän lisäksi tuotto-odotusta tukee ~7 %:n osinkotuotto. Näkemystämme maltillisesti hinnoitellusta osakkeesta niin ikään tukee reilu 15 euron tasolla sijaitseva DCF-arvo. Näemme osakkeen tarjoavan sijoittajalle riittävän tuotto-odotuksen lyhyen tähtäimen epävarmuustekijöiden tueksi.

26 tykkäystä

Nyt pitää kysyä, onko yleensä mielekästä tehdä ennustemuutoksia juuri ennen tulosjulkaisuja? Tokmannille tehtiin ennustemuutos tulosennakossa 3.3. jolloin tavoite nostettiin 15,5 euroon. Nyt viikko myöhemmin se laskettiin 14,5 euroon. @Arttu_Heikura , onko teillä joku linjaus siihen, muutetaanko ennustetta juuri ennen tulosjulkaisua?

6 tykkäystä

Ei ole linjausta siitä, että ennen tulosta pitäisi tehdä muutoksia ennusteisiin.

Mikäli osakekurssi kuitenkin kohoaa tavoitehinnan tasolle niin tällöin on kuitenkin mielekästä tarkistaa ennusteet ja näkemys. Tästä syystä tein ennen tulosta päivityksen, jonka yhdeydessä myös ennusteet ja tavoitehinta muuttuivat. Näkemys muuttui silloin osta → lisää ja jatkuu nyt lisää.

20 tykkäystä

“Joku saattoi hieraista silmiään selatessaan halpakauppayhtiö Tokmannin tuoretta tarjouslehtistä. Sen sivuilla on nimittäin tarjous varsin nostalgisesta tuotteesta, tyhjästä c-kasetista.”

No totta puhuen, ei noita varmasti kamalasti myydä. Mutta taas yksi esimerkki markkinoinnista, joka herättää positiivisia fiiliksiä tarjouskuvastoja selaavissa kaleveissa ja ylittää uutiskynnyksen.

13 tykkäystä

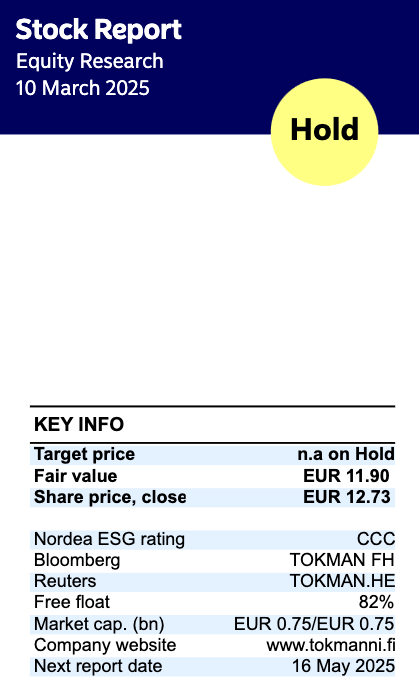

Nordea julkaisi päivitetyn Tokmanni-analyysinsä. Suositus pysyy PIDÄ-tasolla, Fair value tarkentuu 11,90 euroon (edellinen: 13,10 €). ![]()

Key upside risks: Tokmanni could post higher-than-expected LFL growth and increase its gross margins further. An increasing share of high-margin products, e.g. clothing and other private-label products, could support earnings going forward. A sudden recovery in consumer confidence could affect Tokmanni’s sales and earnings. In a downturn, the company could increase its market share considerably without hurting its gross margin. The integration of and synergies from the Dollarstore acquisition could also offer more upside than expected.

Key downside risks: Gross margins and earnings could be negatively affected if Tokmanni refrains from increasing its selling prices todefend market share. Its product assortment remains sensitive to weather. Consumers could shift from general discounters to specialised discount stores. A general downturn in the economy could have an impact on performance, as witnessed by the recent profit warning. Ambitious growth targets could operationally increase risks due to more challenging category management. The Dollarstore acquisition increases leverage, and integration synergies might not be achieved.

11 tykkäystä

Seurakuntamme pastori saarnaa väkevästi kaupan alan pörssiyhtiöistä:

Varsin hyvä puheenvuoro myös Tokmannista. Maallikkosarnaajana totean, että turhan pessimistisesti monissa sijoittajakeskusteluissa on otettu vastaan Tokmannin Q4. Samalla muistutan että vielä tyyliin viime marraskuussa jotkut analyytikot arvelivat, ettei yhtiö tule välttämättä saavuttamaan päivitetyn ohjeistuksensa alalaitaa.

20 tykkäystä

Miten Tokmanni menestyy Julan ym. kilpailijoiden tullessa markkinoille? Tokmanni on selvästi erilainen verrattuna Biltemaan, Julaan, Puuiloon, Motonettiin ja Claes Ohlsonin. Jos olette Tokmannikssa käyneet, niin huomaatte, että yli puolet pinta-alasta on vaatteita. Näin ei ole muilla mainituilla. Joten Tokmannin pääkilpailijoita käytännössä ovat Citymarket ja Prisma. Miten Tokmanni voi menestyä näitä jättejä vastaan. Syy on se, että pienemmillä paikkakunnilla ei ole Citymarkettia tai Prismaa. Näin Tokmanni on vaatetuksen kaupan suhteen markkinajohtaja hyvin laajalla alueella Suomessa. Siinä kalsareita ostaessaan tulee myös muuta rompetta ostettua. Näin Tokmanni voi varsin hyvin. En oikeastaan voisi käsittää, että kukaan menisi kalsareita Biltemasta tai Motonetistä ostamaan.

11 tykkäystä