Miltä Tokmannin tulevaisuus vaikuttaa foorumilaisten mielestä?

Minkälainen sijoituskohde Tokmanni on?

Viime aikoina Tokmanni on maistunut yksityissijoittajille. Voisiko tämä olla jopa yritys, johon suomalaisella piensijoittajalla voisi olla kansainvälisiä investointitaloja parempi näkyvyys?

4 tykkäystä

Joskus ipon jälkeisinä aikoina yritin tutustua yhtiöön ja ostinkin sitä vähän. Enää en ole omistanut osaketta aikoihin. Osake lähti hyvin lentoon listautumisen jälkeen ja Anttilan konkurssi poisti vähän kilpailua. Honkkarin yrityssaneeraus sai markkinat säikähtämään (koska ei hakenut konkurssia). Kilpailu on halpatavaramarkkinoilla kovaa. Mutta sitten heikot luvut selitettiin tyyliin joko lämpimällä talvella tai kylmällä kesällä, pitikö sitten paikkansa, en tiedä. En jaksanut enää spekuloida seuraavan vuoden säätä joten möin. Lisäksi yhtiö kovasti haki kasvua kutakuinkin myymälöiden avaamisella. Ongelmana voi olla että kasvukeskuksissa kilpailu on vähintäänkin veristä ja syrjäseuduilla asiakkaat vähenevät muuten. Yhtiö operoi vain kotimaassa joten Suomen vähittäiskaupan kehityksestä liiketoiminta riippuvainen. Melkein koko tulos jaetaan osinkona ulos vaikka uusia myymälöitä avattiin nopealla tahdilla ja velkaa vielä taakkana. Yhtiöllä ei tuntunut olevan mitään kilpailuetuja.

Mutta Tokmanni laittoi johtoryhmää uusiks ja ämpärikauppahan on vetänyt hyvin. En ole enää yhtiötä pahemmin seurannut mutta yhtiö on tuntunut löytävän “oikean sävelen” haastavalla markkinalla. Lieneekö yhtiö laittanut tuotevalikoimaa uusiks ja keskittynyt tehokkaaseen jakeluun, sekä tehostanut toimintaa? Kommentoikaa jos tiedätte tarkemmin. Uudistuneen markkinoinnin jokainen on varmaan telkkarissa nähnyt. Jos kasvu perustuu uusien myymälöiden avaamiseen kannattaa kurkata osarien yhteydessä myös vertailukelpoisten myymälöiden lv kasvua. Tämäkin on näyttänyt kasvavan. Yhtiön kannattavuus on hyvällä mallilla ja liiketoiminta on loppupeleissä melko defensiivistä. Yritysostot ja kilpailijoiden karsiminen sitä myöten voisi olla kova pala jos yhtiöllä olisi varaa siihen. Tokmanni on kuitenkin ylivoimaisesti suurempi kuin moni kilpailija (bauhaus, Clas Ohlson, Hongkong, puuilo ja mitä näitä nyt on). Mutta en ole tosiaan enää paljon seurannut firmaa, kommentoikaa te jotka enemmän tiedätte.

Tästä yksi yhtiö inderesin seurantaan?

4 tykkäystä

Mulla on Tokmannia pieni määrä holdissa. Tässä omia ajatuksia:

- Perushyvä osinkopumppu

- Kasvu ollut hyvää numeroilla ja myös liikkeiden ilme on noussut viimeisen parin vuoden sisään

- Jos talous dyykkaa Tokmanni lienee defensiivisestä päästä koska halpaketju

- Kiinnostavana huomiona Google Trendissä Tokmannin hakumäärät nousseet kahdessa vuodessa ~50% suhteessa hakuehtoihin “Prisma” ja “Citymarket”

- Laajentuminen muuttotappiopaikkakunnille on mielestäni liiketoiminnan isoin riski, mutta ilmeisesti kasvu on ollut aika edullista (ostettu/vuokrattu liiketiloja lähes nollahintaan). Tavallaan luotan kyllä tässä Tokmannin johtoon ja heidän kykyihinsä laskea tuon peliliikkeen kannattavuus.

- Lapun kohtuullinen hinnoittelu (pitää mielestäni paikkaansa edelleen)

Mielestäni nykyisen hinnoittelun (+10€) kestävyys kumpaankin suuntaan suhteessa edelliseen tasoon riippuu aikalailla nyt Q3 tuloksesta. Q2 oli huikeat 60% parempi viime vuodesta ensisijaisesti prosessien parantamisen (vähennetty hävikkiä) ja kevätportfolion uudistamisen ansiosta. H2 on kuitenkin määräävä vuosipuolisko, eli markkinat hinnoittelevat edellisen osarin perusteella arvioita siitä miten suuri osa parannuksesta skaalautuu koko vuodelle - eli väheneekö hävikki koko vuoden tasolla. Toistaalta jos näin on ja portfoliota ja myyntiä on onnistuttu parantamaan myös syksyllä on varaa mennä myös ylöspäin.

Ennen osaria on mielestäni mahdollisuus ottaa näkemystä portfoliosta, prosesseista ja varmaan makrostakin. Osarin jälkeen nähdään paremmin päästäänkö tämän vuoden tavoitteisiin ja suurempi sisäinen epäselvyys kurssista ainakin omassa mielessäni poistuu.

Evli seuraa ja julkaisee Tokmannista analyysia: Equity research.

4 tykkäystä

Itsellä oli useaan otteeseen positioita Tokmannissa 7,5 euron kohdilla, rahastin sitten viimeisimmän kympin kohdilla. Aliarvioin pahasti Tokmannin potentiaalin, koska en ollut ylipainottanut sitä, kun halvalla olisi saanut. Se taas perustui siihen, että noin kerran viikossa käyn jossakin Helsingin alueen Tokmannissa ja tuntui, että juuri koskaan ei ollut paljon asiakkaita eli meni pahasti pieleen tämä omakohtainen havainnointi🙂 Mietin uuden position ottamista, mutta taidan kuitenkin odottaa Q3:n yli, koska markkinoilla niin paljon hermostuneisuutta.

2 tykkäystä

Täälläkin on ollut pari kertaa positio Tokmannissa, ja voittoakin on tullut. Kuten @NukkeNukuttaja, myin itsekin tuossa viimeisimmästä huipusta kaikki Tokmannit kuitenkin pois ja ajattelin odottaa jospa tuo osake vähän halpenisi niin voisi ottaa uuden position.

Sinänsä Tokmanni vaikuttaa omasta mielestäni ihan hyvältä ja kohtuuhintaiselta sijoituskohteelta. Tällä nykyisellä markkinatilanteella en kuitenkaan uskaltanut holdata Tokmannia kauempaa, koska en usko, että Tokmannin kurssi ainakaan nousee jos yleinen markkinatilanne tästä kovin paljon huonontuu. Toki positiivista on se, että Tokmanni on saanut jo tänä vuonna parannettua kannattavuuttaan verrattuna viime vuoteen. Lisäksi Tokmanni on viime aikoina laajentanut myymäläverkostoaan, mikä voi kyllä lyhyellä aikavälillä rasittaa kannattavuutta. Jos kaikki menee hyvin, pidemmällä aikavälillä tulosta alkaa ehkä tulla enemmän.

1 tykkäys

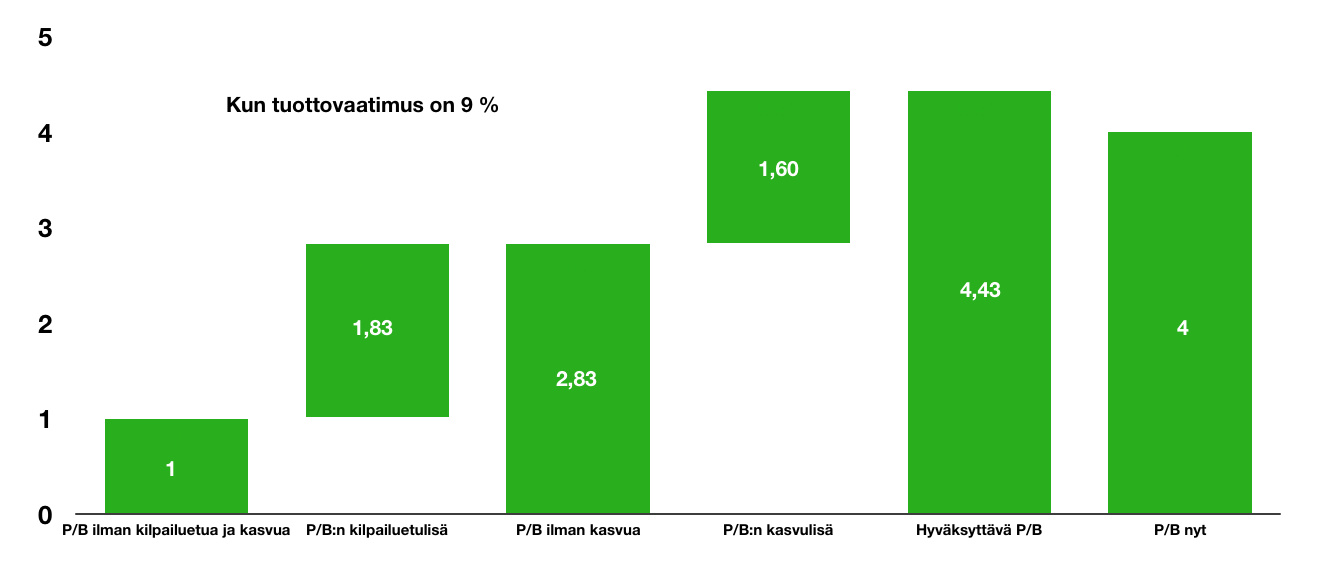

Tässä pieniä laskelmia Tokmannista ja sen hyväksyttävästä P/B-arvosta.

Tokmannin ROE 25,5 % ja nykyinen P/B 4,0x.

Tuottovaatimuksena laskuissa käytetty 9,0 %.

Tokmannin kasvuvauhdiksi on oletettu 4,2 %, joka on viiden vuoden keskiarvo tuloksen vuosittaisesta kasvusta.

Tuloksena saadaan hyväksyttäväksi P/B kertoimeksi 4,43x. Arvosijoittaja haluaisi kuitenkin mieluiten kasvulisän “ilmaiseksi”, jolloin olisi valmis maksamaan vain P/B ilman kasvua (2,83x) mukaisen hinnan.

2 tykkäystä

Viimeisin iso yritysosto Tokmannilta Ale-Makasiinit. Jännä nähdä miten kauppa käy näissä pienillä paikkakunnilla, kun esimerkiksi Saarijärvellä on kaksi Tokmannia nyt ja Äänekosken seudulla jopa kolme Tokmannia. Saivat toki kaupan myötä hyville paikkakunnille kauppoja missä ei vielä ollut Tokmannia.

2 tykkäystä

mikä se Tokmannin vallihauta on, ja mistä se kasvu tulee?

Liikevaihdon kasvu tulee lähinnä uusien myymälöiden avaamisella ja vanhojen laajentamisella. Yhtiöllä tavoitteena saada 200 myymälää avatuksi. Tällä hetkellä taisi olla 186 myymälää 2018 vuoden lopulla. Liikevoittoa saadaan lisäksi hilattua ylemmäksi mahdollisesti vielä tehokkuutta lisäämällä.

2018 tilinpäätöksessä kerrotaan hyvin kilpailueduista. Lyhyesti sanottuna kilpailuedut tulevat mm erottuminen kilpailijoista tuotevalikoimalla, hintamielikuvalla ja sijainnilla etc. Yhtiöllä on maanlaajuinen myymäläverkosto. Yhtiö pyrkii lisäksi esim saamaan suuria eriä tavaraa myymälöihin mahd halvalla ja myymään sitä kilpailijoita edullisemmalla hinnalla. Tämä taitanee olla osa sitä tehostamistoimia, mihin ei moni pienempi yritys pysty.

Itse olisin silti tarkkana tuon kilpailuetu -käsitteen kanssa (periaatteessa oli mikä yhtiö tahansa kyseessä). En tiedä onko Tokmannilla mitään (kestäviä) kilpailuetuja. Silloin olin varma että ei ole kun siihen viimeksi sijoitin. Vahvuuksia voi aina toki olla. Riskeistä; Kauanko Tokmanni pystyy kasvamaan Suomessa? Ja mitenhän Tokmanni on positioitunut kaupan alan murrokseen. Myöskin uuden sijainnin valinnassa saa olla tarkkana. Itsellä ei ole henkkoht tarvetta ollut Tokmanniin, Pirkkalassa hain remonttijuttuja Bauhaussista, jonain päivänä motonetistä autojutut ja cittarista loput. Kaikki oli Tokmannin naapurissa. Tämä nyt ei kerro vielä mitään tietenkään, ja helpompihan se olisi hakea kaikki tavarat saman katon alta. Onhan Tokmannin liiketoiminnassa riskejä ja epävarmuustekijöitä pitkä lista, jotkut luonnollisesti suurempia kuin toiset.

Ps. Se on todella hyvä merkki kun liikevoittonarginaalia saadaan nostettua vaikka uusi myymälä saavuttaa kannattavuuden vasta suunn. 12kk aikana. Kannattaa tosiaan lukea tilinpäätös 2018

2 tykkäystä

Pitäisi varmaan lukea tuo tilinpäätös. Sinulla oli hyviä pointteja paljon ja koen ajattelevani samoin. Itsekään oikein tule Tokmannilta haettua hirveästi mitään, varsinkaan sellaista mitä muualta saisi. Varsinkin elintarvikepuoli minulle täysin vieras. Jotenkin nämä matalan katteen liikkeet, jotka perustuvat tehokkuuteen pelottavat. Tehokkuus kun tuntuu jotenkin häviävän jossain vaiheessa.

1 tykkäys

Itse kiinnitin huomioni siihen joskus pari-kolme vuotta sitten, että Tokmannin paikallinen myymälä on asiakkaan näkökulmasta kuin perinteinen halpahalli, eli tavarat esillä vähän miten sattuu, ”vähemmän hienostuneesti” - ja kuitenkin tuotteiden hintalapuissa luki vähintään sama hinta kuin muissakin kaupoissa. Lakkasin käyttämästä Tokmannia kun huomasin, että naapuritontilla Citymarketissa samojen tuotteiden hinnat ovat jopa halvempia.

En tiedä onko tässä tapahtunut muutosta, kun en ole siellä enää vuosiin asioinut. Kun en tykkää maksaa ylimääräistä ”halpahallikokemuksesta”.

2 tykkäystä

![]()

Meidän puutarhatuolit on kestävän kehityksen mukaiset.

Ei ole asiaa Tokmannille niissäkään merkeissä.

Kuva on pihamme pergolasta päättyneeltä kesältä.

2 tykkäystä

Vastoin @Masse -sedän ennakko-odotuksia, Tokmannin voittokulku jatkui, vahvaa kasvua ja positiivinen ohjeistusmuutos! Nyt minä tuuletan!

Lisäys: Mainitaan tosin veronpalautusten ajoittuminen raportoidulle kvartaalille, joka voi näkyä joulusesongin myynnissä.

Lisäys 2: En siis tuuleta sitä, että @Masse -setäkin voi joskus olla erehtyväinen, vaikkakin se on harvinaista, vaan hyvää tulosta.

3 tykkäystä

Kyllä kyllä… Todellä hyvältä kyllä näyttää nyt.

1 tykkäys

masse setä taitaa alkaa olla aikamoinen legenda täällä palstalla ja onneksi pitää lippua korkealla kun osuu oikeaan :)!

2 tykkäystä

Itse tulikin vähän kevennettyä q2-osarin jälkeen, kun en luottanut kurssin pitävyyteen enkä ollut varma q3sesta. Olisi toki pitänyt ottaa huomioon tuo veronpalautusten vaikutus. Mutta q4 tulee myös olemaan vahva ja kurssi pitänyt tasonsa, joten mitään tarvetta ei ole kevennellä lähitulevaisuudessa.

Kävin nappaamassa lisää lappuja kyytiin. Tokmanni kasvattanut 10% liikevaihtoaan tänä vuonna suhteessa vertailukauteen, sekä nosti nyt ohjeistustaan kannattavuuden parantamiseksi koko vuodelle. Kannattavaa kasvua!

Pyörittelin luvut ja näyttää halvalta jo 2019e, saati sitten 2020e. Evli näyttää yleensä julkaisseen seuraavan rapsan aika pian, niin ei tarvitse sitten olla omien lukujen varassa.

1 tykkäys

Lyhyellä tähtäimellä toki Tokmannille jää vielä todistettavaa Q4:lle eli joulumyynnin pitää onnistua, mutta kasvaneen liikevaihdon myötä en näe tässä ongelmaa. Riippuu tietenkin paljon siitä, minkälaiset kertoimet markkinat hyväksyvät, toki jos kvartaali kvartaalin perään liikevaihto ja tulos paranee niin hyväksyttävät kertoimetkin kasvavat. Kausiluonteisuuden näen hieman negatiivisena seikkana.

2 tykkäystä

Samaa mieltä! Samoin jos osinkoa pystytään nostamaan, niin markkina reagoi varmasti positiivisesti. Nyt en näe ainakaan vielä yhtään syytä miksi hyppäisin pois kyydistä, joten pysytään mukana ja katsotaan kuinka pitkälle tässä päädytään

2 tykkäystä

Päätin käydä koeostoksilla Tokmannilla. Viime kerrasta on jo vuosia kun satuin tarvitsemaan mitäpä muutakaan kuin ämpärin ja kannen.

Perusfiilis hyvä. Tuotteet oli nätisti hyllytetty ja niitä oli. Ämpäreitä en meinannut löytää kuin lopulta kaljahyllyn vierestä 30-litraisia kiljusankoja. Valikoima periaatteessa sama kuin isommassa Prismassa, mutta ilman ruokaa. Omaan matkaan tarttui lopulta yksi tölkki limonaatia.

Tokmanni on nykyään ajan hermoilla. Hinta- ja trenditietoinen nuoriso käy uudelleensijoittamassa osingot limuhyllylle.

2 tykkäystä