Could we discuss Disney? The Disney+ streaming service will be launched in the US in November, and probably in Europe in 2020.

https://www.finlandiagroup.fi/ajankohtaista/finlandia-blogi-walt-disney-company

4 Likes

The market always focuses on something trendy, like streaming services. There seem to be plenty of them already, but that’s fine. The stock price has perhaps risen partly because of this, and at these levels, I don’t find it particularly attractive. I have a bit in my portfolio around the hundred-dollar mark, where it has traded for years.

Disney’s service, with the company’s product portfolio, is perhaps the most attractive, but it won’t make money for a long time. Rather, it’s a necessary evil, especially since ESPN is in slight difficulty and the traditional TV business is in transition.

Disney’s strength lies in content production and managing the entire value chain, which no other company does better.

2 Likes

These streaming content wars are an interesting thing… As a consumer, I just don’t have the energy to think about which streaming service I should watch each show on…

Content (i.e. a company’s own IP) is certainly an interesting trend that will continue to grow. That’s why small indie content creators (like Rovio) are extremely interesting investment targets, IMO.

1 Like

7 Likes

I had to watch that set last night, very impressive. Here’s the video https://thewaltdisneycompany.com/disney-investor-day-2020/

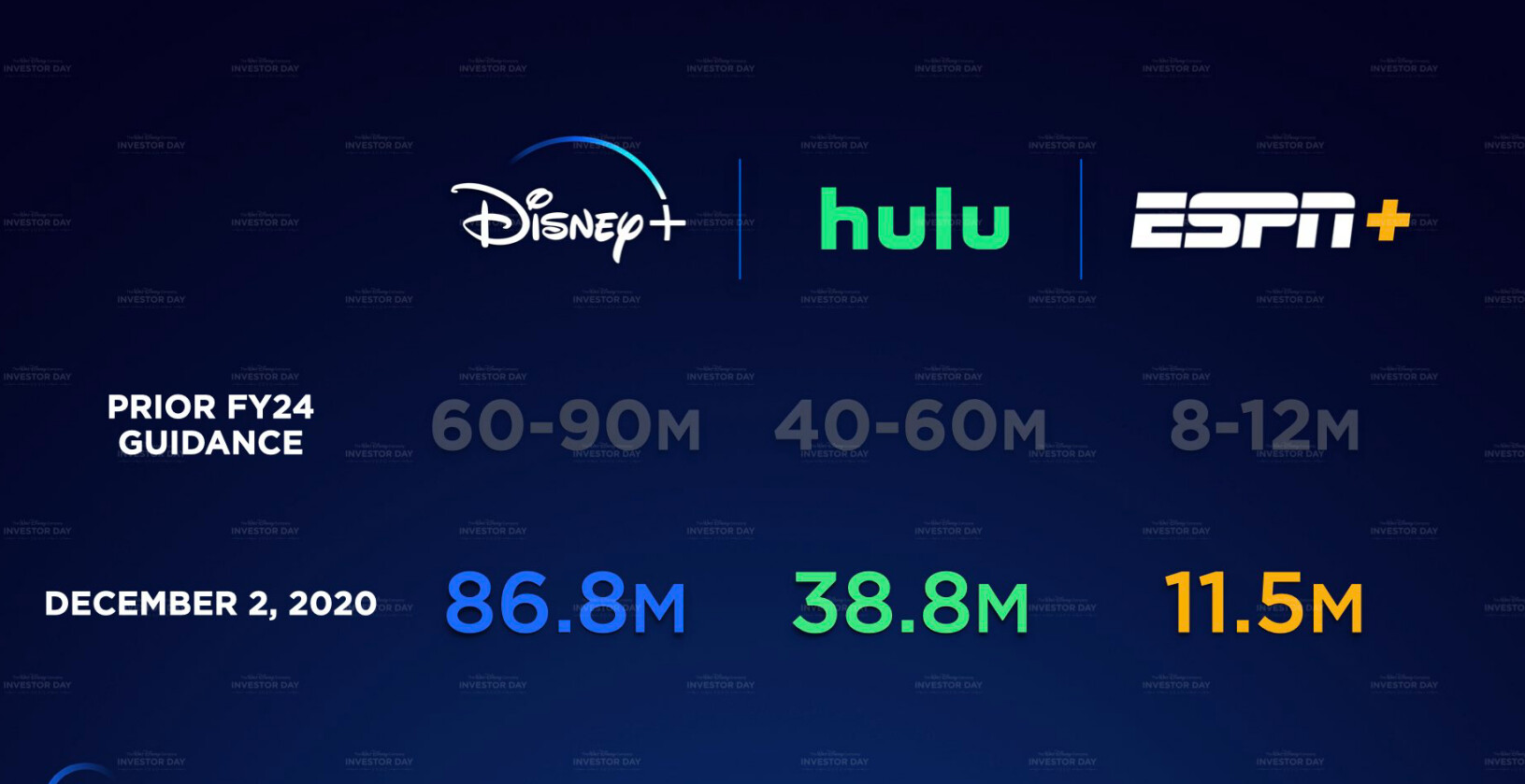

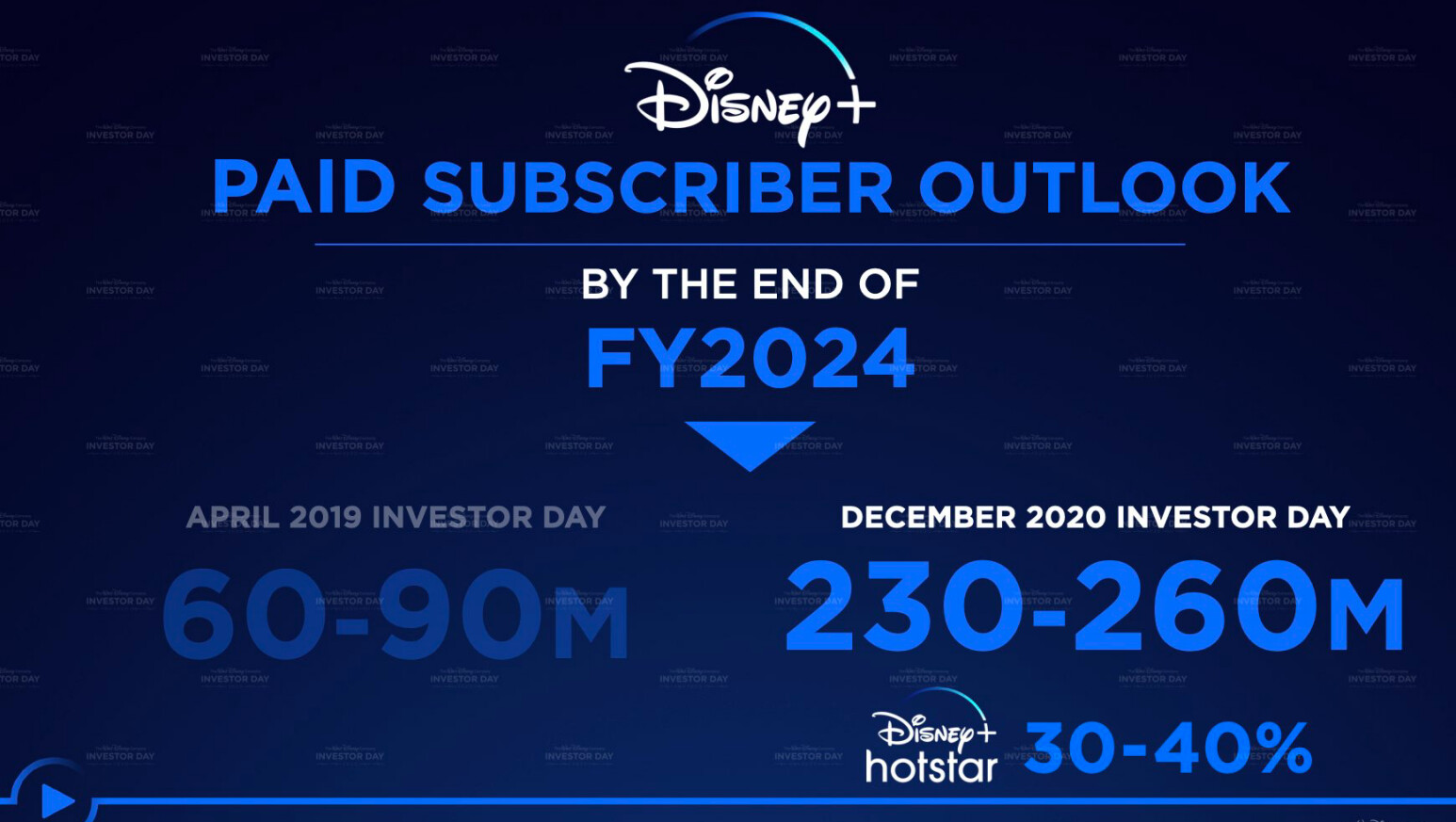

Smashed streaming targets… Also interesting insights, e.g. collaborations (MercadoLibre, etc.) and also new content coming to Disney+ from many IPs, e.g. massive series into production

4 Likes

By the way, CNBC had an interesting analysis of Disney’s investor day and the strengths it demonstrated in the company’s operations relative to other entertainment companies:

https://www.cnbc.com/2020/12/11/disney-is-executing-streaming-better-than-competition.html

For pretty much every other company in the streaming wars, the goal is to acquire the most popular content to entice paying month subscribers. That turns content spending into an arms race as companies including Netflix, AT&T’s WarnerMedia, Comcast’s NBCUniversal, ViacomCBS and Discovery throw darts at series, producers, actors and ideas in the hopes of generating zeitgeist-y hits.

But Disney’s strategy is different.

Disney is methodically building movies and shows off its own intellectual property and then using hit characters to introduce new ones. It has turned actors into superheroes - - and will repeatedly use them in feature films, Disney+ series and cameo appearances. It announced a dozen “Star Wars” pieces of content, reviving actors in old roles - - and creating new stars.

Disney then takes those movies and series and builds theme park rides based on them. It sells merchandise off of them. It builds a world of American culture off of them.

4 Likes

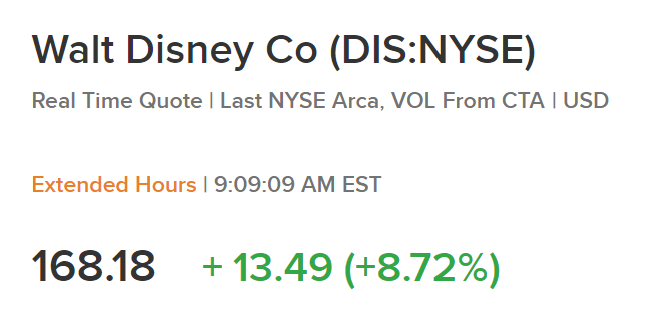

It was a small payday for us owners again.

It’s been quite stormy for a couple of years since I’ve owned it, but now light is starting to peek through the clouds. If the dollar exchange rate were a bit stronger, this would become the biggest holding in my portfolio.

Disney continues on a good path, as @JK-32 referred to above. At this rate, as the coronavirus recedes, there could be a nice amount of additional growth. Currently, many sectors are idling, and there is hardly any income.

And in the streaming platform war, Disney will take the market leader position by 2022 at the latest, at least in my books.

1 Like

It definitely tells you something about the company’s focus when, in a 3.5-hour investor day stream, they talk about segments other than direct-to-consumer for a maximum of a few words ![]() This part was still only 13% of the company’s revenue in 2019. Hopefully, those cash cow businesses aren’t completely forgotten.

This part was still only 13% of the company’s revenue in 2019. Hopefully, those cash cow businesses aren’t completely forgotten.

But the company’s “content, content, and content” mantra definitely makes me smile, as my own investment decision was made precisely because of that content competitive advantage, which should carry them quite far. It was a small surprise to me how many successful movies and series are owned by Disney. I wondered, if all of those disappeared from Netflix and appeared on Disney+, how would consumers behave?

4 Likes

Analysts in the U.S. have predicted that Disney+ will surpass Netflix in subscriber numbers by 2026. The estimated subscriber counts are 294 million for Disney+ and 286 million for Netflix. However, these estimates factor in that one-third of subscribers will come from Asia and will pay only one-third of what an American subscriber pays for the subscription. This means an annual revenue of $20.76 billion for Disney+ versus Netflix’s $39.52 billion.

Currently, the most watched series globally is Disney and Marvel’s WandaVision, and The Falcon and the Winter Soldier is coming next month.

Sources:

5 Likes

Reasons why I have Disney in my portfolio:

- Market leader in content production and brands

- Adaptable: many strategic options. Failures are tactical and do not easily escalate into existential questions.

- Survived the lockdown period with honor, even though the whole world seemed to be against it

- Accomplished management

- Strong position in the streaming competition. Even if this market saturates, it is not Disney’s only option.

- Even if Disney itself doesn’t win the platform competition, others would still need its content

Nothing is eternal, of course, and even a company like Disney can eventually run into a crisis by making enough mistakes amidst changes. As a cultural icon, Disney has once again become a tool in the American culture war.

I still feel that Disney has been compared too much to Netflix and has suffered a largely undeserved -30% stock price drop this year as a result. We are now at 2019 price levels, before the Disney+ transition. For my part, I decided to load up.

14 Likes

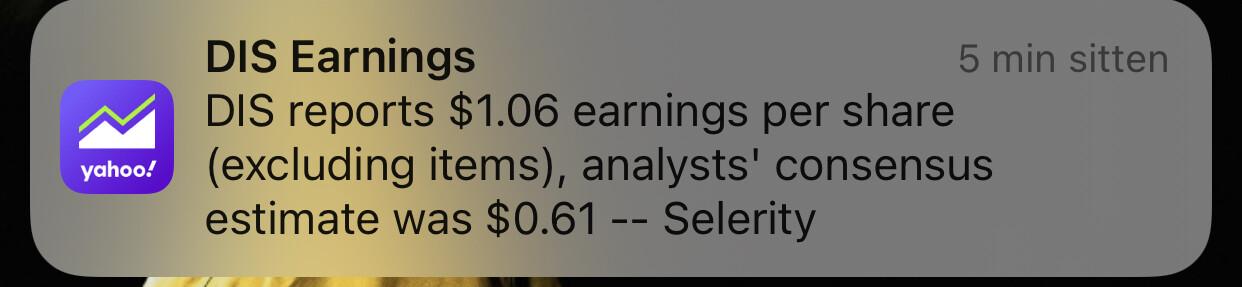

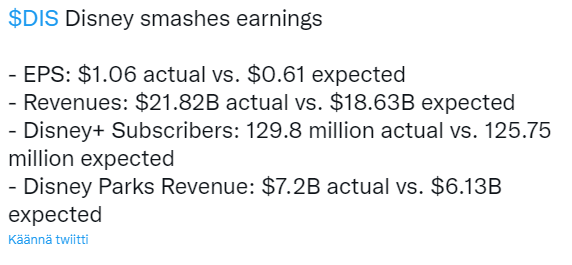

DIS earnings on Tuesday evening. It’s been on a downward trend, will there be a turnaround on Wednesday? Opinions?

1 Like

You can find analysis of Disney by Sifter on the Inderes website:

A link to a related video can also be found in Sifter’s thread on the discussion forum.

3 Likes

Thanks. I never really get anything out of those analyses. ![]()

I’m a bit bearish on this one. Would love to hear other people’s opinions…

1 Like

Things didn’t go quite as planned for Disney. Revenue and profit fell well short of forecasts. Theme parks performed quite well, but for example, Disney+ made a significant loss despite an increase in subscribers. One has to look far into the future with this one if intending to keep it in the portfolio.

4 Likes

It was a bad quarter, nothing to do about it. On the other hand, Disney+ subscribers exceeded forecasts, and now, for example, a new Black Panther movie is coming very soon.

Chapek assures that streaming will turn profitable in 2024. That’s probably the most critical point of tension for the coming years; the theme parks have already proven their strength.

The stock is currently almost at its COVID-19 dip prices, even though at that time, businesses were closing down and the future was uncertain. In my opinion, this is a buy/add price.

7 Likes

Indeed, soft results on many fronts. I can say that the timing of my purchases hasn’t been ideal, but on the other hand, there was nothing in this quarterly result that would have changed my investment hypothesis.

In the short term, there might be more headwinds if the US economy turns into a recession, and competition in the VOD (Video On Demand) market with Netflix and Amazon will be brutal. However, I believe Disney has all the ingredients to overcome these challenges well in the long run.

I’m staying in.

7 Likes

Bob Chapek finally got fired, and not so surprisingly, Iger is back as CEO.

5 Likes