I’m going with a pretty grassroots analysis here, but I’ve only done some casual polling among my acquaintances (mostly men aged 25-45) and a rough scan of discussion forums to see how the pricing of Sony’s new console and the upcoming game lineup revealed in the press were received, and the reception seems almost like Tesla hype. A friend had already inquired about these consoles in stores, and it seems all the pre-orders he checked were ‘sold out’. Then, over the weekend, while having coffee with another friend, we watched a compilation of trailers for upcoming games, and even this “max one game a year, and that too from the bargain bin” guy started asking when it would be released and at what price.

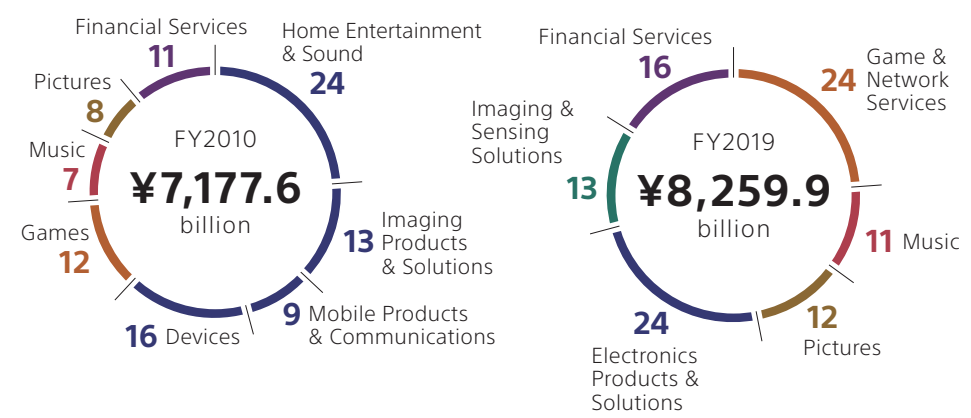

Last spring, I had planned to invest in Sony because I had read that the year preceding the release of new consoles has consistently been a growth year for console companies (source: I no longer remember which magazine I read it in, but possibly Kauppalehti), perhaps with the exception of the PS3, which was sold at a significantly higher price than the competing Xbox released at the same time, leading to a loss of market share. However, the pandemic altered my investment plans, and I completely forgot about Sony. Now, I haven’t really been following Sony, but I should check their quarterly reports and calculate how, for example, Q2 went for the company in other aspects during the pandemic, and how large a share of the company the console side covers. The marketing for the new console will, of course, take a large chunk, so I should probably dig up some estimates of what it has cost during this unusual time, as, for example, huge gaming E3 conventions where much of the marketing is done were not held. I can say this much about marketing costs: Sony’s management announced in the summer that they want to sell the console as cheaply as possible, but they didn’t yet know the marketing costs, which is why the pricing of the upcoming console was delayed. Thus, one could imagine that marketing didn’t consume too many costs, as the now-released price has been quite well received, based on what I’ve read.

In any case, the release date of the new console is in November, and if some kind of broader lockdown occurs, and it doesn’t affect Sony’s factory operations and thus the availability of the console too much, I would assume that the release date for a new generation console is nearly perfect.

If anyone has been following Sony’s results this year, or has any counter-thoughts, please let me know, because I only started thinking about whether I should start examining the numbers before the next quarterly reports last week. Q4 2020 could show pretty good results during the pandemic.

Edit. I also looked at some rumors before hitting the post button, and apparently there’s a rumor circulating that Microsoft might be buying the game studio Bethesda. That’s undeniably a game-changing move, because if Bethesda started pumping out Xbox exclusive games, it would be a pretty big blow to PlayStation. If someone doesn’t know about video games, that game studio has the world’s buggiest but at the same time immensely popular game selections. And if anyone is at all interested in Sony’s shares now, I can try to find out more when I have more time. The stock seems to be at ATH prices, so we’re not talking about digging through bargain bins from the pandemic era.

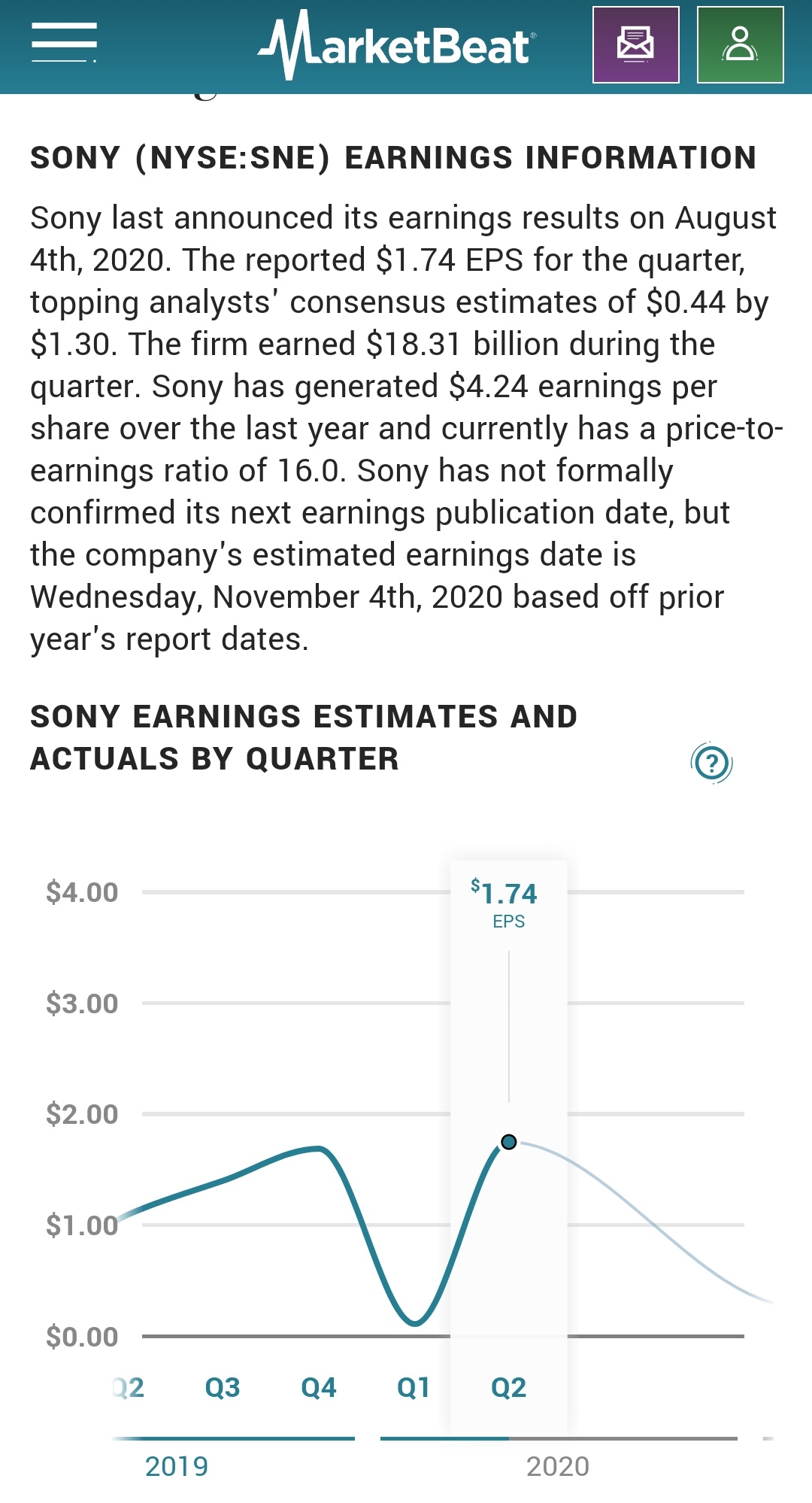

Edit2. I also linked a screenshot of the first target price that came up with a quick Google search to add some color to the message. It’s nice to see that when I started writing this message based purely on guesswork, and immediately thought of PlayStation lockdowns, it turns out some real analyst also likes the stock.