Yeah, I would think that Teleste’s profitability is strong once the operating profit margin has doubled; right now it was 5.8%… But it’s in the right direction and now we just need significantly more volume, though the order book doesn’t seem to be heading that way…

1 Like

Atte interviewed Teleste CEO Esa Harju following the company’s Q1 release ![]()

Topics:

00:00 Introduction

00:11 Q1 Highlights

01:21 Broadband Networks unit

03:28 European market situation

04:32 Public Safety and Mobility unit

05:48 New customer accounts

07:47 Component availability status

09:33 Guidance remains unchanged

1 Like

Here is the company report on Teleste from Atte and Roni ![]()

We reiterate our Accumulate recommendation and target price of EUR 4.2 for Teleste. The company’s Q1 results exceeded our forecasts, and we have slightly revised our estimates upwards. Although the merger of the largest customer in the Networks segment still creates uncertainty for order development in the coming quarters, the recovery of the European market, as well as the expanded customer base in both businesses and the efficiency measures taken, provide the foundation for continued earnings growth. This is also anticipated by Teleste’s outlook. Mirrored against the earnings growth outlook for the coming years, Teleste’s valuation (2026e adj. P/E 10x) looks moderate.

2 Likes

Here are the comments from our friend Atte on how Teleste is strengthening its position in Europe through cooperation with Vecima, with whom the company offers an open distributed access architecture solution for the European market. ![]()

2 Likes

Here are Roni’s comments regarding the improved loan terms received by Teleste. ![]()

Teleste announced that it has agreed on improved syndicate loan terms with its lender banks. The updated terms include lower loan margins than before, reflecting the company’s strengthened financial position. Additionally, guarantee limits have been expanded. The news is positive, but quite expected considering the company’s recent earnings turnaround and the strengthening of its balance sheet position.

1 Like

"According to the EU Market Abuse Regulation (MAR), a person discharging managerial responsibilities (PDMR) and persons closely associated with them must notify transactions promptly and no later than three business days after the date of the transaction. Both the person subject to the notification obligation and the company must ensure this deadline is met.

If the trades were made on March 4–5, 2026, the market should normally have received the information by approximately March 9–10, 2026, depending on the calculation of business days."

The CFO bought about €25k worth of shares in early March, at which point Q1 is already well underway and information asymmetry vs. the market can be assumed.

Doesn’t seem like this went quite by-the-book? It says something, even though purchases are generally a positive signal.

1 Like

Good catch. I didn’t notice the dates. That insider notification went completely wrong, and it’s the CFO we’re talking about. Sigh (Hohhoijaa)

Brothers Atte and Roni have published a new comprehensive report on Teleste. Like their other extensive reports, this one is also available for everyone to read. ![]()

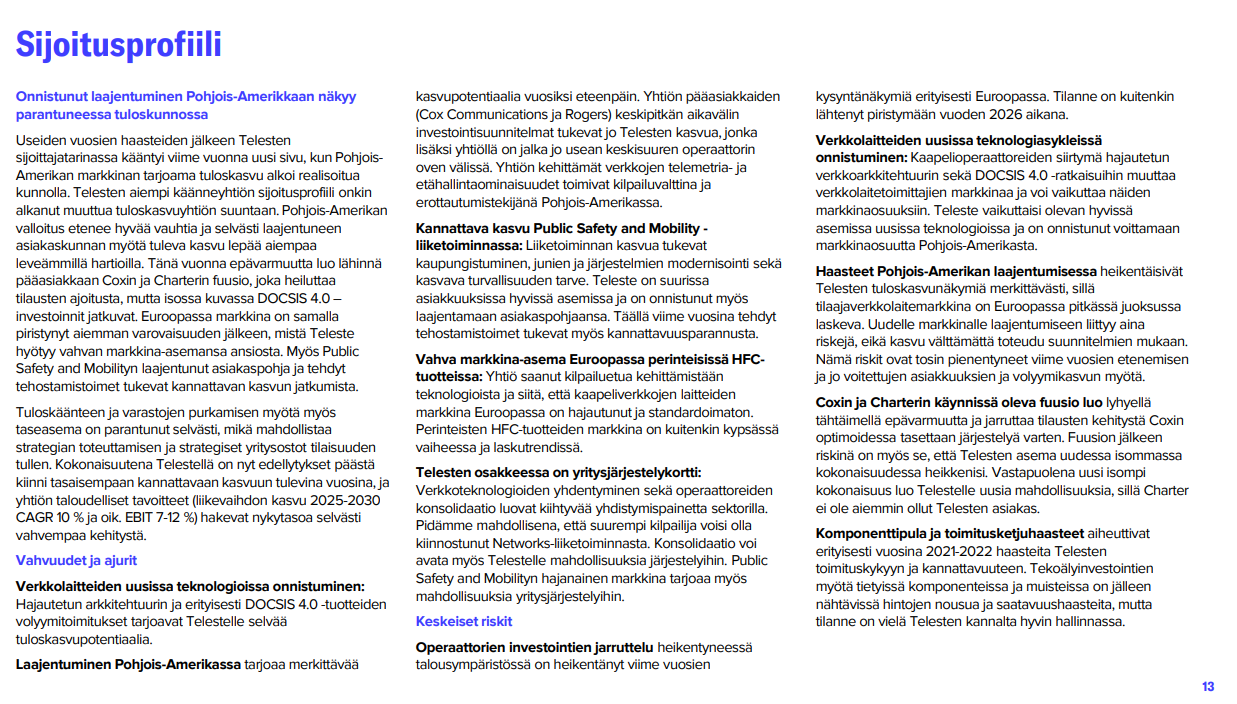

We reiterate Teleste’s “Accumulate” recommendation and €4.2 target price. The conquest of North America by Teleste’s Networks segment is progressing at a good pace, and with a clearly expanded customer base, future growth rests on broader shoulders. This year, uncertainty is mainly created by the merger of key clients Cox and Charter, which affects the timing of orders, but in the big picture, investments in DOCSIS 4.0 continue. In Europe, the market has picked up after previous caution, which Teleste is benefiting from thanks to its strong market position. New client relationships and efficiency measures taken in Public Safety and Mobility also support the continuation of profitable growth. Reflected against the earnings growth outlook for the coming years, Teleste’s valuation (2026e adj. P/E 9.5x) looks very moderate.

Quoted from the report:

Overall, Teleste is well-positioned to continue growing in both of its business segments in the coming years. With an improved cost structure, this growth should also scale to the bottom line, which the company’s financial targets also anticipate. With an improving earnings level, the company also has the potential to increase its dividend in the medium term, unless capital is allocated more heavily to areas such as acquisitions.

1 Like

It has been a pleasure to follow Teleste over the last few years, now that the business has started moving in the right direction after a long and challenging period. Of course, this is the result of long-term work in both business units, which has enabled the company to win new customers while simultaneously streamlining operations across several areas. From 2025 onwards, these efforts have begun to show in the company’s upward earnings trend, and there is still plenty of potential for improvement. In this light, the current valuation of the stock looks very attractive.

2 Likes

I don’t necessarily disagree with the report, but I feel it doesn’t give enough weight to the merger.

Personally, I see it such that the merger and the information trickling out from it will define the share price level in the short to medium term. The current bearish trend of late is due to waiting for the merger, as there is a fear that the larger Charter will kick Teleste out (which is a relevant risk).

If the larger Charter integrates Teleste into its current suppliers, the share price will drop. If Charter starts using Teleste, the share price will surge. I consider the most likely outcome to be the same as Inderes’s view, that deliveries to “Cox” will normalize at least for a while, but that no expansion will happen in the short term.

I don’t have the energy to start digging up ownership data right now, but I think this is such a clear catalyst that one would assume Teleste’s own staff is also keeping a close eye on this, one way or the other.

1 Like